Europe Vending Machine Market Outlook to 2030

Region:Albania

Author(s):Shreya Garg

Product Code:KROD8654

Region:Albania

Author(s):Shreya Garg

Product Code:KROD8654

December 2024

81

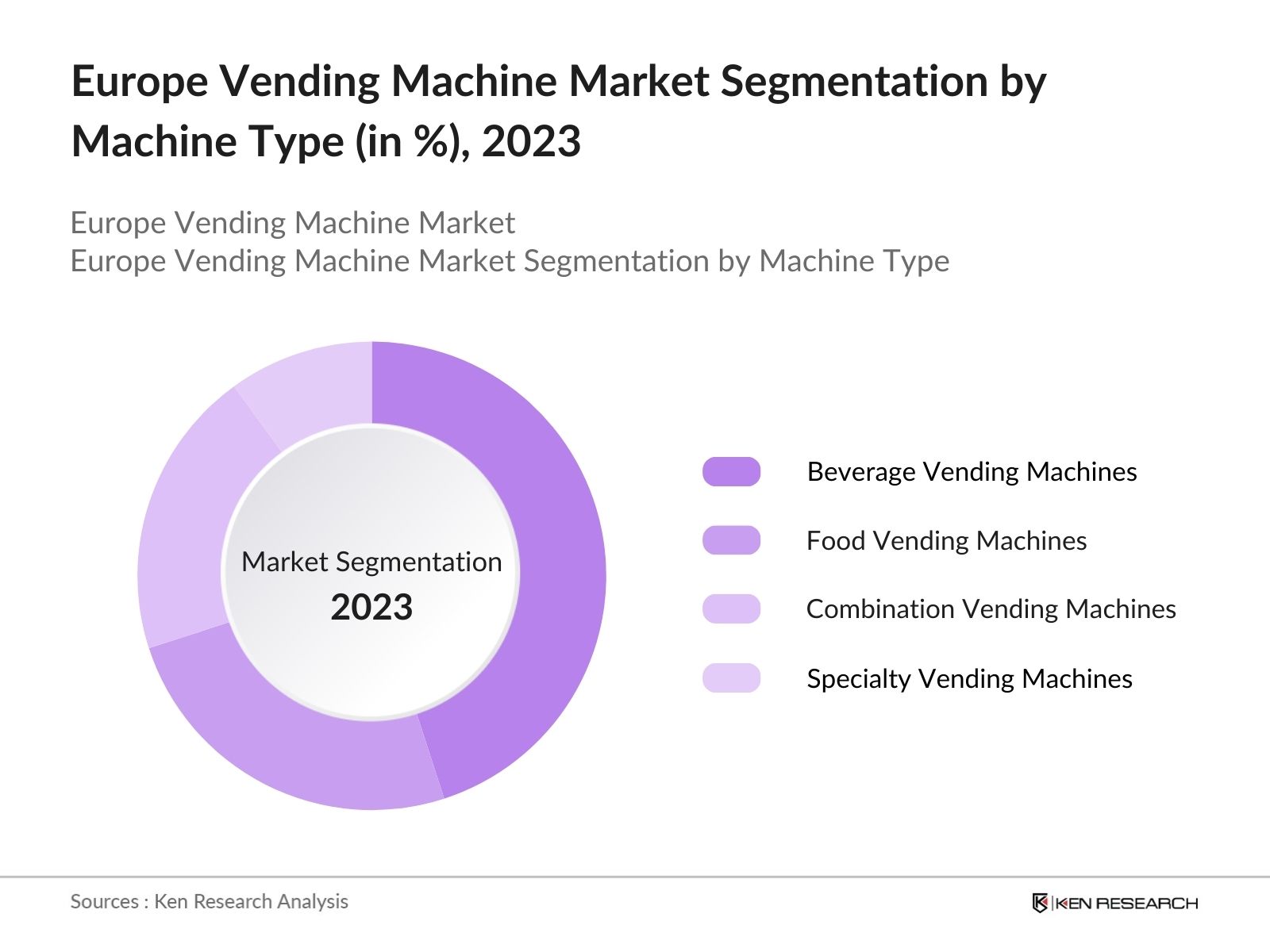

By Machine Type: The market is segmented by machine type into Beverage Vending Machines, Food Vending Machines, Combination Vending Machines, and Specialty Vending Machines. Recently, Beverage Vending Machines hold a dominant market share within this segment due to the increasing demand for on-the-go beverages among busy urban populations. Beverage vending machines are particularly popular in high-traffic locations such as transportation hubs, corporate buildings, and shopping centers, where quick and easy access to drinks is highly valued. This segments dominance is also supported by advancements in machine technology, enabling them to offer various beverages, including hot and cold options, to cater to diverse consumer preferences.

By Payment Mode: The market is segmented by payment mode into Cash-Based, Card-Based, Contactless Payments, and Mobile Wallets. Contactless Payments have emerged as the dominant segment due to the shift towards cashless societies across Europe and the convenience contactless options provide in busy, fast-paced environments. High adoption rates of contactless technology in public transportation and retail settings make contactless vending options more attractive to consumers. Additionally, recent health-conscious trends, especially post-pandemic, have emphasized the preference for contactless interactions, making this payment mode particularly popular.

The Europe vending machine market is characterized by the presence of both regional and global players, with major players including Crane Co., Azkoyen Group, Selecta Group, Fuji Electric Co., Ltd., and N&W Global Vending S.p.A. dominating the market. This consolidation highlights the influence these companies have due to their technological innovation, extensive distribution networks, and strategic partnerships across Europe.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

R&D Investments |

Revenue |

Geographic Presence |

Sustainability Initiatives |

Payment Integration |

Service Contracts |

|

Crane Co. |

1855 |

Stamford, USA |

|||||||

|

Azkoyen Group |

1945 |

Navarra, Spain |

|||||||

|

Selecta Group |

1957 |

Cham, Switzerland |

|||||||

|

Fuji Electric Co., Ltd. |

1923 |

Tokyo, Japan |

|||||||

|

N&W Global Vending S.p.A. |

1963 |

Valbrembo, Italy |

The Europe vending machine market is projected to experience steady growth, supported by rapid advancements in digital payment systems, the integration of IoT in vending technologies, and a growing preference for convenience-oriented retail solutions. As smart city initiatives across European countries gain momentum, vending machine applications are expected to diversify, catering to a wide array of consumer needs. Increased collaboration between vending machine operators and food and beverage companies is anticipated to offer consumers more options and contribute to further market expansion.

|

By Machine Type |

Beverage Vending Machines |

|

By Payment Mode |

Cash-based |

|

By Location |

Transportation Hubs |

|

By Product |

Snacks |

|

By Country |

Germany |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Penetration Rate

1.4 Key Market Developments

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Milestones and Achievements

3.1 Growth Drivers

3.1.1 Increasing Automation Demand in Retail

3.1.2 Technological Advancements (e.g., AI-enabled Vending Solutions)

3.1.3 Expanding Cashless Transactions

3.1.4 Changing Consumer Preferences (Healthier Options)

3.2 Market Challenges

3.2.1 High Initial Investment

3.2.2 Maintenance and Service Requirements

3.2.3 Stringent Regulatory Compliance

3.2.4 Security Concerns (Data and Physical Vandalism)

3.3 Opportunities

3.3.1 Integration with Smart City Initiatives

3.3.2 Expansion in Underdeveloped Regions

3.3.3 Customized Product Offerings

3.3.4 Partnerships with E-commerce for Delivery Points

3.4 Trends

3.4.1 Shift Toward Contactless Payment

3.4.2 Sustainability in Vending Machine Materials

3.4.3 Increased Adoption of IoT

3.4.4 Integration with Customer Loyalty Programs

3.5 Regulatory Framework

3.5.1 Health and Safety Regulations

3.5.2 Energy Efficiency Standards

3.5.3 Consumer Protection Guidelines

3.5.4 Data Protection Policies (GDPR Compliance)

3.6 Market Structure Analysis

3.7 Stakeholder Ecosystem (e.g., Manufacturers, Retailers, Service Providers)

3.8 Porters Five Forces

3.9 Competitive Ecosystem

4.1 By Machine Type (In Value %)

4.1.1 Beverage Vending Machines

4.1.2 Food Vending Machines

4.1.3 Combination Vending Machines

4.1.4 Specialty Vending Machines (e.g., Health Products)

4.2 By Payment Mode (In Value %)

4.2.1 Cash-based

4.2.2 Card-based

4.2.3 Contactless Payments

4.2.4 Mobile Wallets

4.3 By Location (In Value %)

4.3.1 Transportation Hubs

4.3.2 Educational Institutions

4.3.3 Corporate Offices

4.3.4 Hospitals and Health Centers

4.4 By Product (In Value %)

4.4.1 Snacks

4.4.2 Beverages

4.4.3 Health and Wellness Products

4.4.4 Fresh Food Items

4.5 By Country (In Value %)

4.5.1 Germany

4.5.2 United Kingdom

4.5.3 France

4.5.4 Italy

4.5.5 Spain

5.1 Detailed Profiles of Major Companies

5.1.1 Crane Co.

5.1.2 Azkoyen Group

5.1.3 Selecta Group

5.1.4 Royal Vendors Inc.

5.1.5 Sanden Corporation

5.1.6 Seaga Manufacturing Inc.

5.1.7 Fuji Electric Co., Ltd.

5.1.8 Jofemar Corporation

5.1.9 N&W Global Vending S.p.A.

5.1.10 Bianchi Vending Group

5.1.11 Westomatic Vending Services Ltd.

5.1.12 Rhea Vendors Group

5.1.13 FAS International S.p.A.

5.1.14 Venditalia

5.1.15 Evoca Group

5.2 Cross Comparison Parameters (Revenue, Number of Machines, Production Capacity, Sustainability Initiatives, Geographic Presence, Payment Integration, Service Contracts, R&D Investments)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants and Subsidies

5.9 Technological Collaborations

6.1 Compliance and Certification Requirements

6.2 Environmental Regulations and Standards

6.3 Energy Efficiency Directives

6.4 Consumer Safety Regulations

7.1 Future Market Size Projections

7.2 Key Drivers Impacting Future Market Growth

8.1 By Machine Type

8.2 By Payment Mode

8.3 By Location

8.4 By Product

8.5 By Country

9.1 TAM/SAM/SOM Analysis

9.2 Competitive Positioning Strategies

9.3 Key Marketing Initiatives

9.4 Identification of White Space Opportunities

Disclaimer Contact UsThis initial phase involved constructing a market ecosystem map, identifying primary stakeholders such as manufacturers, operators, and technology providers in the Europe vending machine market. This step utilized in-depth desk research and proprietary data sources to define variables affecting market dynamics.

In this phase, historical data for the Europe vending machine market was analyzed to gauge market penetration, sales distribution, and service quality metrics. This provided a foundation for reliable revenue estimates and performance assessments within each segment.

Hypotheses on market trends and potential growth areas were validated through interviews with industry experts using computer-assisted telephone interviews (CATIs). These discussions provided operational insights directly from industry leaders, refining our data.

The last phase involved engaging with multiple European vending machine companies for in-depth insights into product segments, technological advancements, and consumer trends. This primary research ensured a robust and verified analysis, complementing the bottom-up approach for accurate market assessment.

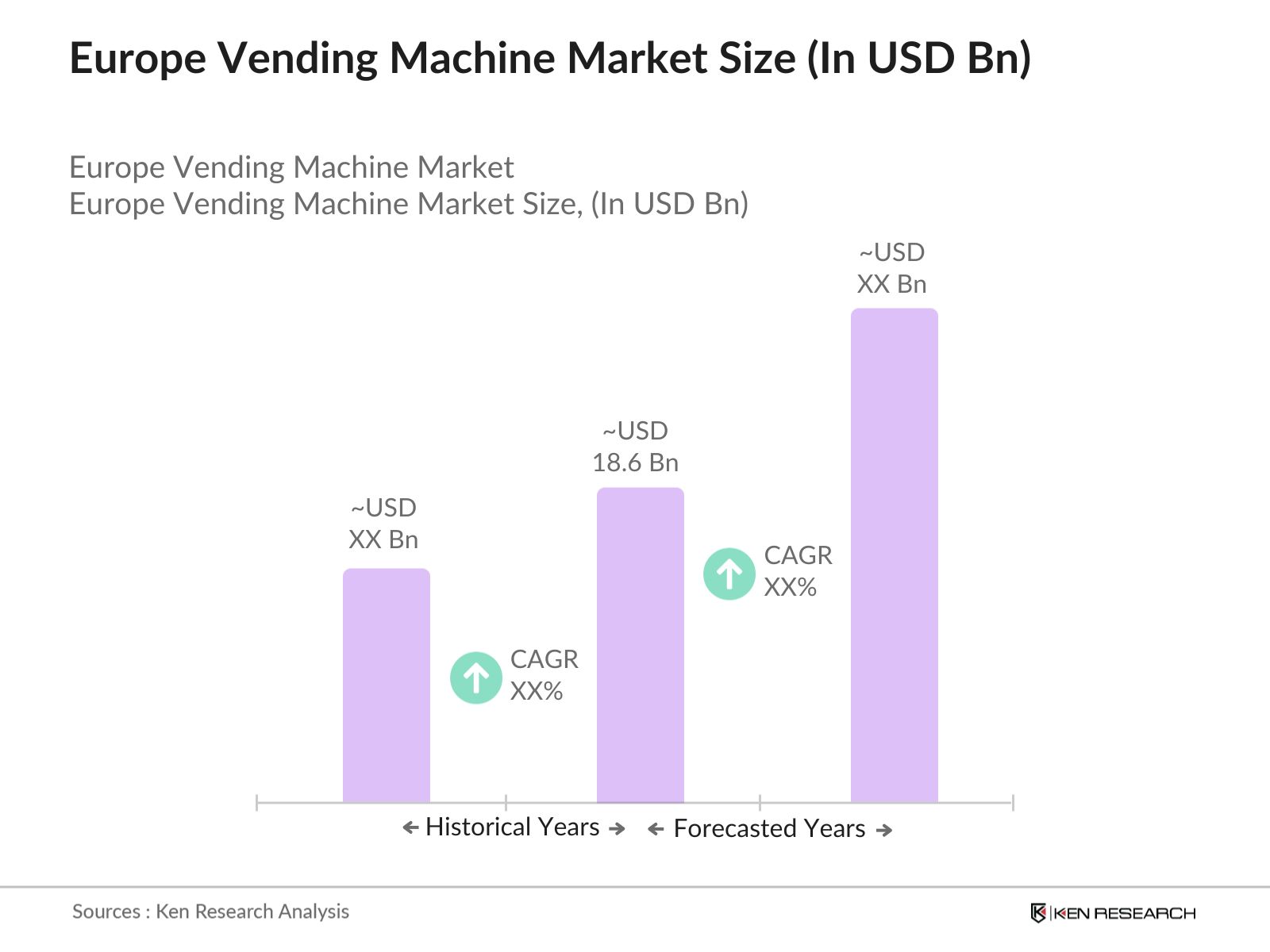

The Europe vending machine market is valued at USD 18.6 billion, driven by technological advancements, automation trends, and evolving consumer preferences toward convenient retail options.

Challenges in the Europe vending machine market include high initial investment, ongoing maintenance requirements, and stringent regulatory compliance, especially regarding payment security and energy efficiency standards.

Key players in the Europe vending machine market include Crane Co., Azkoyen Group, Selecta Group, Fuji Electric Co., Ltd., and N&W Global Vending S.p.A., with each excelling in technological integration and regional expansion.

Growth in the Europe vending machine market is propelled by rising demand for automated retail options, consumer trends toward cashless payments, and the inclusion of healthier product offerings in vending machines.

Germany, France, and the United Kingdom lead due to advanced digital infrastructure, high population density in urban areas, and supportive regulations for cashless payments and eco-friendly products in the Europe vending machine market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.