European Chocolate Market Outlook to 2030

Region:Europe

Author(s):Meenakshi Bisht

Product Code:KROD6903

Region:Europe

Author(s):Meenakshi Bisht

Product Code:KROD6903

December 2024

85

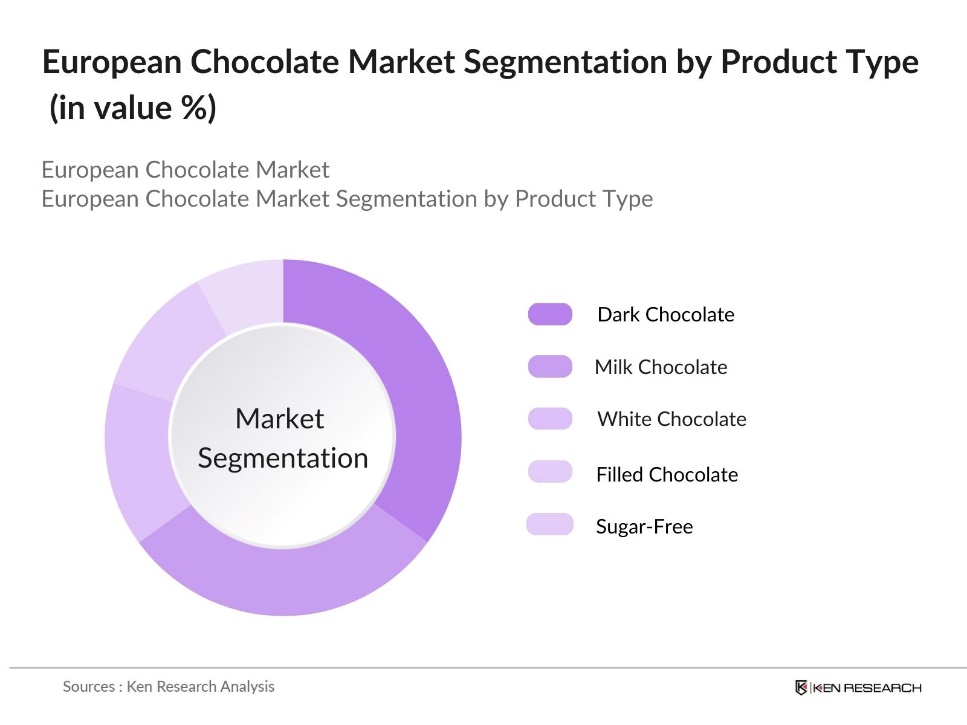

By Product Type: The market is segmented by product type into dark chocolate, milk chocolate, white chocolate, filled chocolate, and sugar-free chocolate. Dark chocolate holds a dominant market share within this segment, driven by the shift toward healthier, lower-sugar options, supported by growing awareness of the antioxidant benefits associated with dark chocolate. Additionally, the unique, intense flavor profile of dark chocolate appeals to a broad consumer base, aiding its popularity.

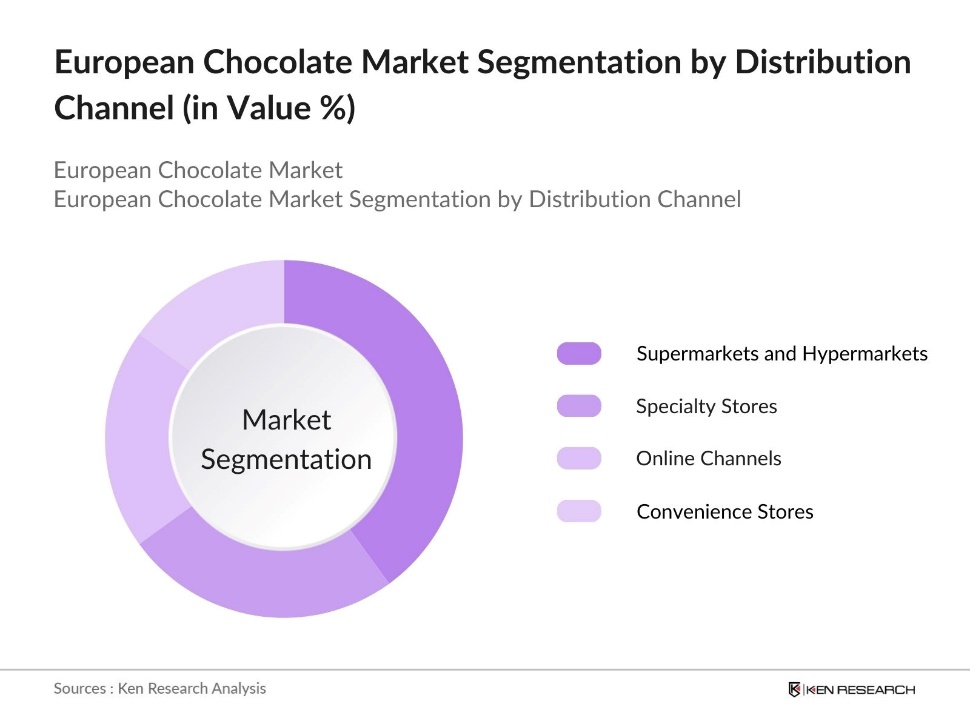

By Distribution Channel: The market is segmented by distribution channels into supermarkets and hypermarkets, specialty stores, online channels, and convenience stores. Supermarkets and hypermarkets hold the largest share in this segment due to their wide reach, consumer accessibility, and the availability of varied chocolate brands and types. This dominance is further reinforced by in-store promotions and seasonal displays, which significantly drive impulse purchases in this category.

The European chocolate market is dominated by a select few global and local companies, including Ferrero Group, Lindt & Sprngli AG, and Mondelez International. The competitive landscape underscores the prominence of established players who leverage their robust distribution networks and product innovation to maintain a competitive edge in the market.

Over the next five years, the European chocolate market is anticipated to experience significant growth, driven by increased consumer interest in health-conscious options, demand for premium products, and digital retail expansion. The market's upward trajectory will likely be influenced by sustainability efforts in the sourcing of cocoa, alongside an increase in vegan and functional chocolates as consumer preferences evolve.

|

Product Type |

Dark Chocolate Milk Chocolate White Chocolate Filled Chocolate Sugar-Free Chocolate |

|

Application |

Confectionery Bakery Products Beverages Snacks Functional Foods |

|

Distribution Channel |

Supermarkets and Hypermarkets Specialty Stores Online Channels Convenience Stores |

|

Ingredient Type |

Cocoa (Organic, Non-Organic) Sugar (Natural Sweeteners, Artificial Sweeteners) Milk Nuts and Additives |

|

Region |

West East North South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Dynamics

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Consumer Shift to Premium Products (Premiumization)

3.1.2 Health-Conscious Consumption Patterns (Low-Sugar, Vegan)

3.1.3 Rising E-commerce Penetration (Digital Channels)

3.1.4 Favorable Trade Regulations (Import/Export Incentives)

3.2 Market Challenges

3.2.1 Fluctuating Cocoa Prices (Raw Material Costs)

3.2.2 Sustainability Concerns (Environmental Impact)

3.2.3 Supply Chain Disruptions (Logistics and Storage)

3.3 Opportunities

3.3.1 Growing Demand for Functional Chocolates (Nutraceuticals)

3.3.2 Expansion in Emerging Economies (Eastern Europe)

3.3.3 Innovative Flavor and Ingredient Introductions (Exotic Flavors)

3.4 Trends

3.4.1 Plant-Based Chocolate Alternatives (Vegan Market Growth)

3.4.2 Sustainable Sourcing Initiatives (Fair Trade, Organic Cocoa)

3.4.3 Experiential Marketing in Retail (Pop-Up Stores)

3.5 Regulatory Landscape

3.5.1 EU Health and Nutrition Claims Regulation

3.5.2 Cocoa and Chocolate Products Regulation (Quality Standards)

3.5.3 Sustainability Certification Requirements (Rainforest Alliance, Fairtrade)

3.6 SWOT Analysis

3.7 Supply Chain Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Product Type In Value %)

4.1.1 Dark Chocolate

4.1.2 Milk Chocolate

4.1.3 White Chocolate

4.1.4 Filled Chocolate

4.1.5 Sugar-Free Chocolate

4.2 By Application (In Value %)

4.2.1 Confectionery

4.2.2 Bakery Products

4.2.3 Beverages

4.2.4 Snacks

4.2.5 Functional Foods

4.3 By Distribution Channel (In Value %)

4.3.1 Supermarkets and Hypermarkets

4.3.2 Specialty Stores

4.3.3 Online Channels

4.3.4 Convenience Stores

4.4 By Ingredient Type (In Value %)

4.4.1 Cocoa (Organic, Non-Organic)

4.4.2 Sugar (Natural Sweeteners, Artificial Sweeteners)

4.4.3 Milk

4.4.4 Nuts and Additives

4.5 By Region (In Value %)

4.5.1 Western

4.5.2 Eastern

4.5.3 Northern

4.5.4 Southern

5.1 Detailed Profiles of Major Competitors

5.1.1 Ferrero Group

5.1.2 Nestl S.A.

5.1.3 Mondelez International, Inc.

5.1.4 Lindt & Sprngli AG

5.1.5 Mars, Inc.

5.1.6 The Hershey Company

5.1.7 Godiva Chocolatier

5.1.8 Barry Calleaut AG

5.1.9 Ritter Sport

5.1.10 Thorntons Ltd.

5.1.11 Neuhaus NV

5.1.12 Galler Chocolatier

5.1.13 Valrhona S.A.

5.1.14 Chocoladefabriken Lindt & Sprngli

5.1.15 Fazer Group

5.2 Cross Comparison Parameters (Production Capacity, Marke Share, Geographic Reach, Innovation Index, CSR Initiatives, Revenue, Key Product Categories, Brand Positioning)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital and Private Equity Funding

6.1 Cocoa Content Standards

6.2 Labeling and Health Claims Regulations

6.3 Import and Export Compliance

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Distribution Channel (In Value %)

8.4 By Ingredient Type (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThe initial stage involves mapping out the major stakeholders within the European chocolate market. Extensive desk research is conducted using a blend of proprietary databases and public sources to gather a complete overview of critical market dynamics.

In this phase, we compile and assess historical data relevant to the European chocolate market, including revenue generation by product types and distribution channels. This enables us to produce a reliable analysis that underpins our overall market estimates.

We validate our research hypotheses by consulting with industry experts via structured interviews. These insights help refine our estimates, ensuring that the data is both accurate and reflective of market conditions.

The final stage includes synthesizing all collected data and insights from expert consultations, which is further refined through bottom-up analysis. This produces a comprehensive and validated assessment of the European chocolate market.

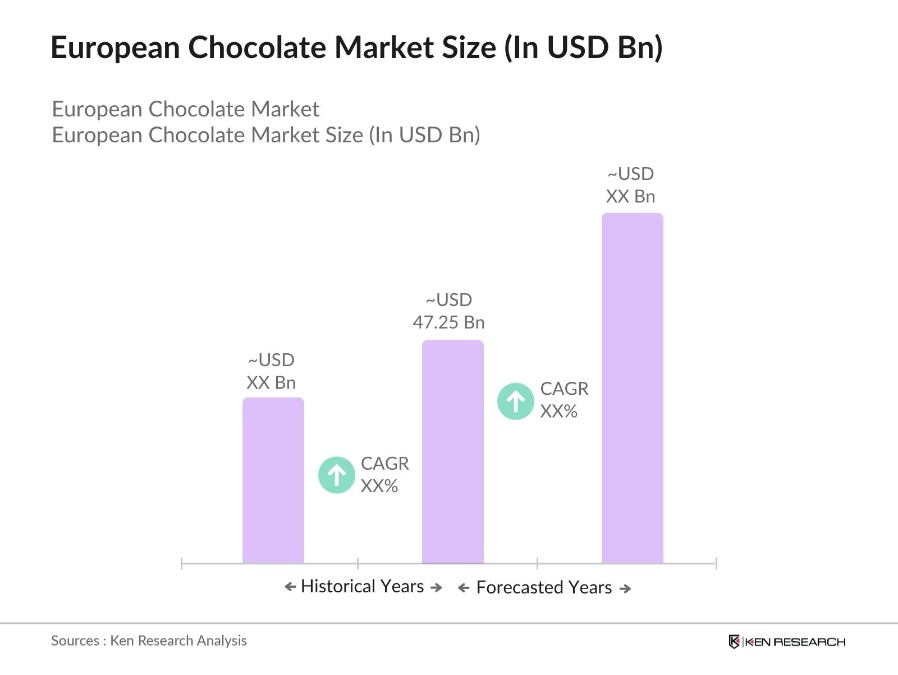

The European chocolate market is valued at USD 47.25 billion, driven by strong consumer demand for premium and health-focused chocolate products.

Challenges in European chocolate market include fluctuating cocoa prices, sustainability concerns, and supply chain disruptions due to logistics and storage issues.

Key players in European chocolate market include Ferrero Group, Lindt & Sprngli AG, Mondelez International, Ritter Sport, and Godiva Chocolatier, owing to their extensive distribution networks and strong brand presence.

Growth drivers in European chocolate market include increasing demand for premium chocolate, a shift toward health-conscious products, and the expansion of online retail channels.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.