GCC Activated Carbon Market Outlook to 2030

Region:Middle East

Author(s):Paribhasha Tiwari

Product Code:KROD4505

December 2024

90

About the Report

GCC Activated Carbon Market Overview

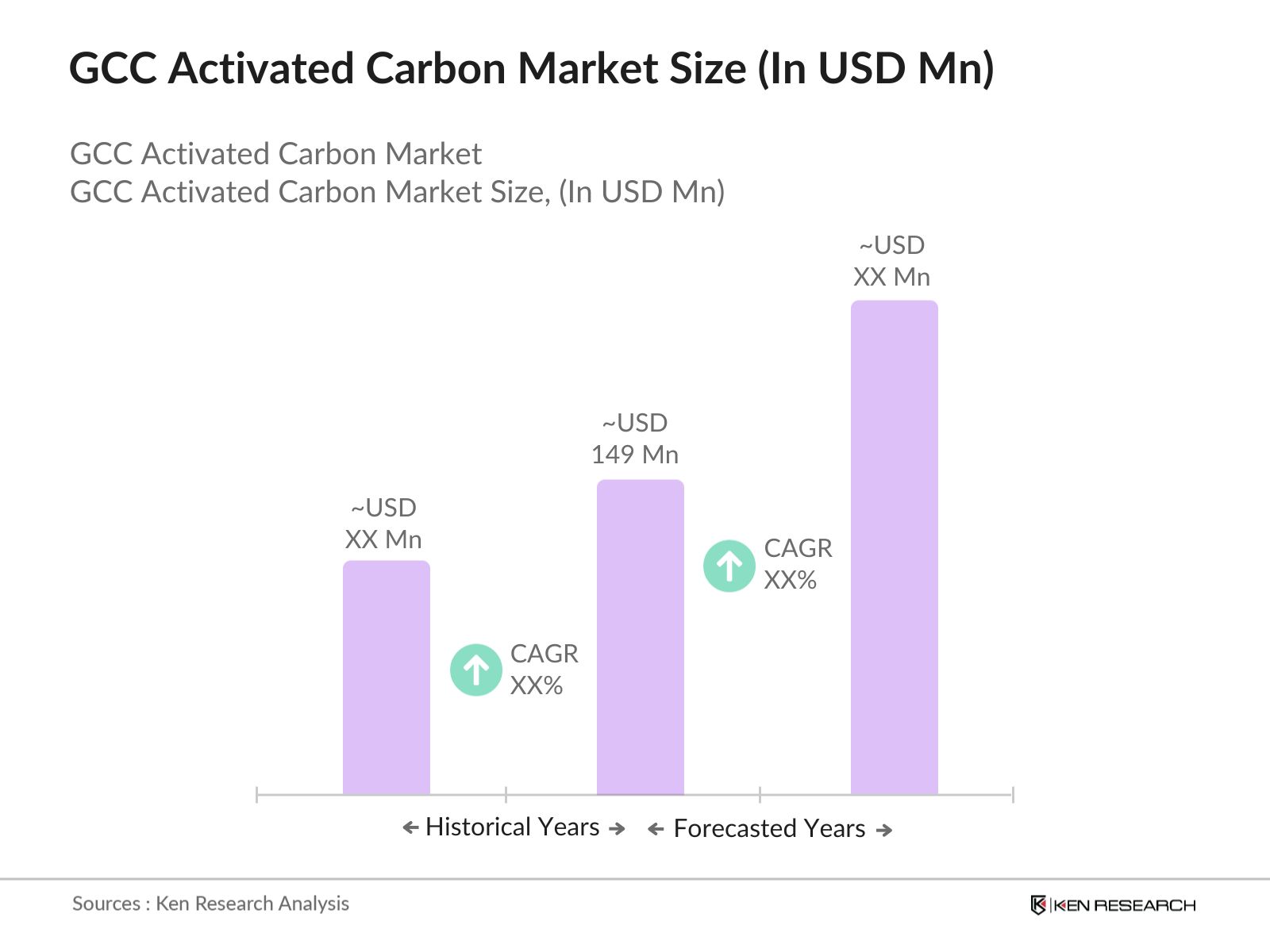

- The GCC Activated Carbon market, valued at USD 149 million, based on a five-year historical analysis, driven by significant investments in water and air purification systems across the region, in response to rising concerns about environmental sustainability and pollution control. The demand for activated carbon is primarily driven by the rapid expansion of industries such as water treatment, pharmaceuticals, and food & beverage processing, which require activated carbon for filtration and purification purposes.

- The dominant countries in the GCC Activated Carbon market are Saudi Arabia and the UAE, driven by their significant investments in industrial development and strict regulatory frameworks concerning environmental protection. Saudi Arabias large-scale oil refineries and petrochemical industries also contribute to the high demand for activated carbon, especially for air and water purification. The UAE, with its rapid urbanization and growing water treatment sector, further dominates the market.

- The UAE's Water Security Strategy, launched to safeguard water resources, includes a focus on wastewater treatment and desalination. The government has invested USD 4 billion in new water treatment plants that heavily rely on activated carbon for filtration. With plans to treat an additional 1 billion cubic meters of water by 2025, the need for advanced filtration systems, including activated carbon, is expected to rise.

GCC Activated Carbon Market Segmentation

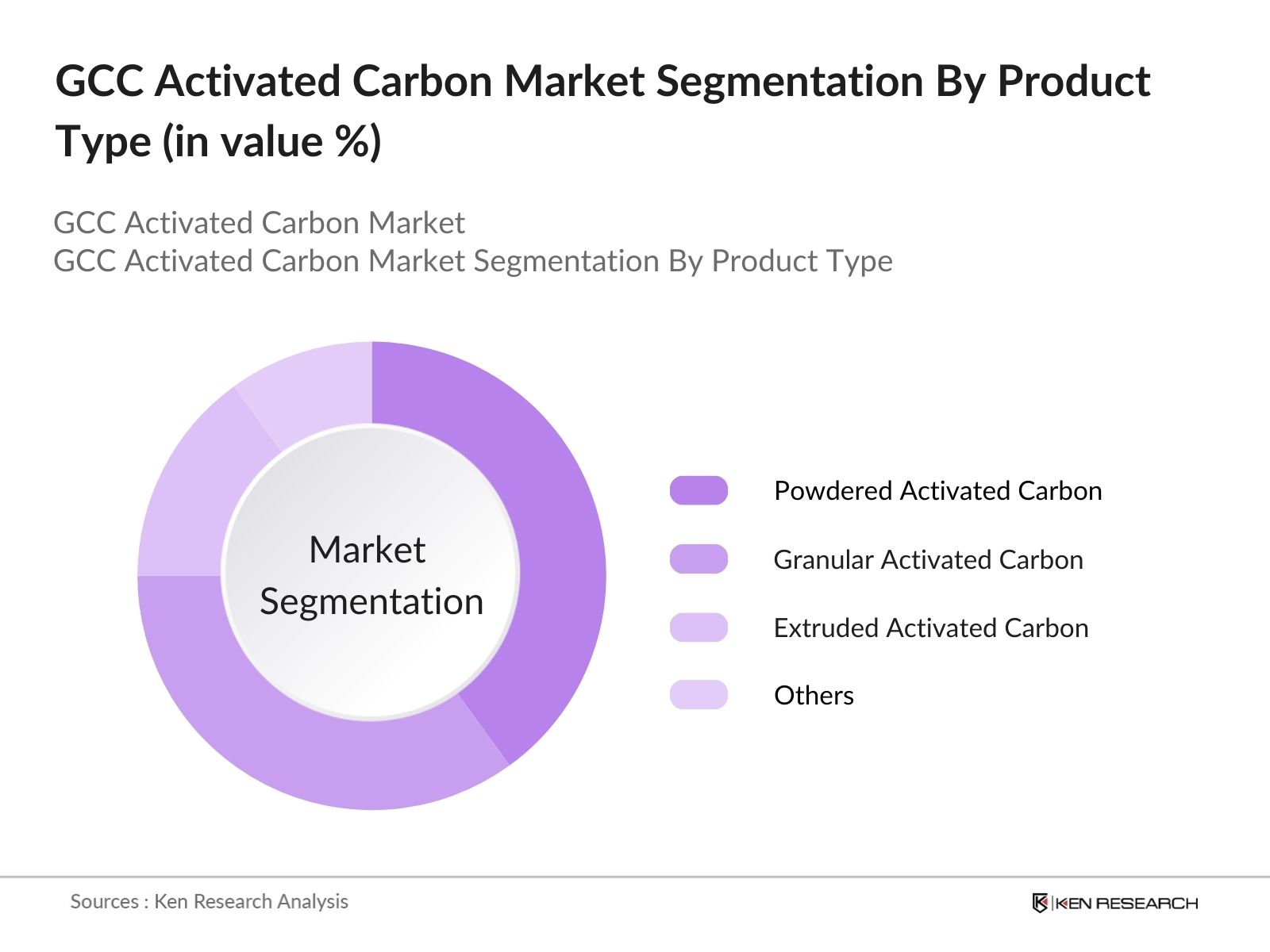

By Product Type: The GCC Activated Carbon market is segmented by product type into powdered activated carbon (PAC), granular activated carbon (GAC), extruded activated carbon, and others (such as fibrous activated carbon). Recently, powdered activated carbon has held a dominant market share within this segmentation. This dominance is due to its extensive application in water treatment plants across the GCC, where it is used to remove organic contaminants and chemical pollutants effectively. Moreover, PAC is favored for its quick absorption capabilities and higher surface area, which makes it ideal for high-demand filtration systems in industrial settings.

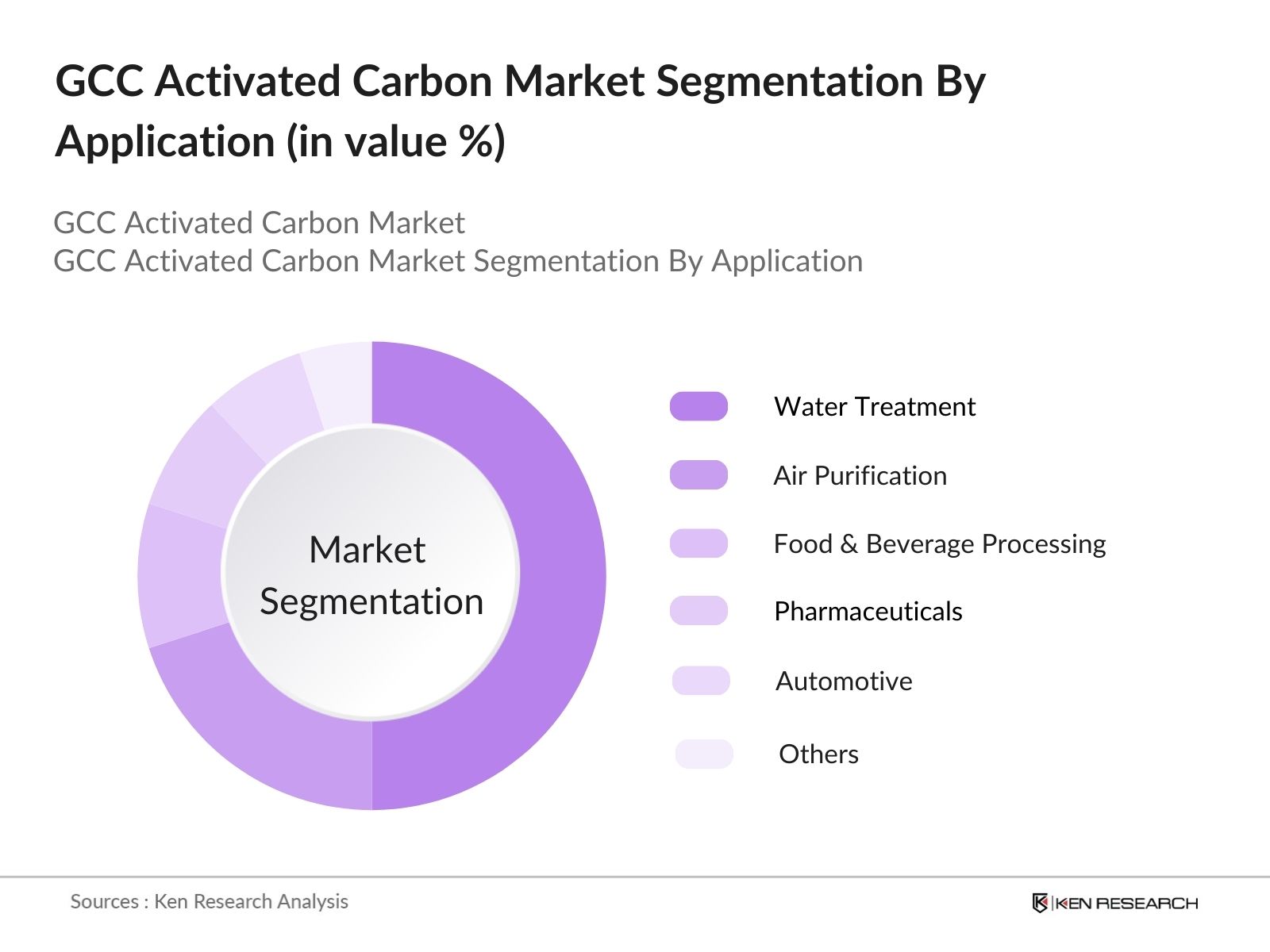

By Application: In terms of application, the GCC Activated Carbon market is segmented into water treatment, air purification, food & beverage processing, pharmaceuticals, automotive, and others (such as chemical industries). Among these, water treatment has dominated the market share due to the region's growing demand for safe and sustainable water sources. The GCCs arid climate and reliance on desalination processes mean that activated carbon plays a crucial role in removing organic contaminants, chlorine, and odors from water supplies. Government initiatives to increase water reuse and ensure clean drinking water have further bolstered the demand for activated carbon in this segment.

GCC Activated Carbon Competitive Landscape

The GCC Activated Carbon market is consolidated, with major international players dominating the scene due to their strong distribution networks, high R&D investments, and advanced technologies. Local manufacturers also play a significant role in addressing the specific needs of GCC-based industries. The competitive landscape is shaped by companies that provide high-performance products for key applications such as water treatment and air purification. Companies like Cabot Corporation and Calgon Carbon Corporation are recognized leaders due to their well-established market presence and diversified product portfolio.

|

Company |

Establishment Year |

Headquarters |

Employees |

Product Range |

R&D Investment |

Market Share |

Manufacturing Units |

Revenue (USD) |

|

Cabot Corporation |

1882 |

USA |

- | - | - | - | - | - |

|

Calgon Carbon Corporation |

1942 |

USA |

- | - | - | - | - | - |

|

Haycarb PLC |

1973 |

Sri Lanka |

- | - | - | - | - | - |

|

Donau Carbon GmbH |

1927 |

Germany |

- | - | - | - | - | - |

|

Jacobi Carbons AB |

1916 |

Sweden |

- | - | - | - | - | - |

GCC Activated Carbon Market Analysis

Growth Drivers

- Stringent Environmental Regulations: Government regulations across the GCC have enforced strict environmental standards, particularly in the industrial and power sectors. For example, Saudi Arabia's efforts to reduce carbon emissions through its Saudi Green Initiative have introduced a requirement for companies to install air filtration systems. The UAE has also enforced regulations on emissions from power plants, driving demand for activated carbon in air pollution control measures. With Saudi Arabias industrial sectors investing over USD 15 billion in compliance with new environmental guidelines, demand for activated carbon in emission controls is rapidly rising.

- Expansion of Water Treatment Facilities: In response to water scarcity, GCC governments have significantly invested in wastewater treatment plants. Saudi Arabia has committed over USD 6 billion to expand its water treatment infrastructure, while Kuwait plans to treat an additional 200 million cubic meters of wastewater annually by 2025. Activated carbon, a key component in filtration systems, is increasingly essential for treating both potable and industrial water. These investments have increased demand for high-performance activated carbon products in various industrial and municipal water treatment applications across the GCC.

- Rise in Industrial Air Purification Demand: GCC countries have witnessed a surge in demand for air purification technologies, especially in industrial zones. Qatar, for instance, launched its Clean Air Plan in 2024, setting stricter standards for industrial air emissions. As part of this initiative, the government plans to install 120 air monitoring stations and activated carbon filters in high-pollution areas. The Saudi petrochemical sector, which accounts for 30% of its GDP, is implementing filtration technologies for industrial processes, further boosting demand for activated carbon in air purification.

Market Challenges

- Volatility in Raw Material Prices: GCC countries rely heavily on imports for raw materials required to manufacture activated carbon, particularly coconut shells and coal. In 2023, the price of coal increased significantly due to supply chain disruptions caused by geopolitical tensions. The cost of importing these raw materials has driven up production costs, creating financial strain for local manufacturers. For example, the price of raw materials for activated carbon production in Bahrain increased by over USD 50 per ton, affecting manufacturing efficiency.

- Limited Local Manufacturing Capabilities: The lack of advanced local production technologies remains a significant challenge for the GCC activated carbon market. In 2024, only 20% of activated carbon used in the region is produced domestically, while the rest is imported. Countries like Oman and Bahrain face challenges in adopting energy-efficient production processes, limiting their ability to scale production. Additionally, reliance on outdated technologies reduces the competitiveness of local manufacturers, further hampering market growth.

GCC Activated Carbon Market Future Outlook

Over the next five years, the GCC Activated Carbon market is expected to show steady growth, driven by continued investments in water and air purification technologies, stricter environmental regulations, and the expansion of industrial sectors such as oil & gas and pharmaceuticals. Additionally, the growing demand for renewable energy solutions, particularly in carbon capture and storage applications, will provide further momentum for the activated carbon market. The rise of urbanization, combined with government initiatives to reduce environmental impact, will continue to support the demand for high-performance activated carbon products across the region.

Market Opportunities

- Technological Advancements in Manufacturing: There is a growing opportunity for technological innovation in activated carbon production in the GCC. Governments in the region are encouraging industries to adopt advanced manufacturing techniques to improve efficiency and sustainability. For instance, the UAE government has introduced incentives for companies investing in cleaner production technologies, reducing energy consumption by 15% across sectors like water treatment. These advancements could significantly boost the production of high-quality activated carbon, positioning the GCC as a competitive hub for activated carbon manufacturing in the global market.

- Expansion into Healthcare and Pharmaceuticals: The healthcare and pharmaceutical industries in the GCC offer substantial growth opportunities for activated carbon applications. In 2024, the Saudi healthcare sector, valued at over USD 70 billion, has expanded its usage of activated carbon in drug formulations and as a detoxifying agent in medical treatments. Similarly, the UAE's rapidly growing pharmaceutical market presents opportunities for activated carbon to be used in air and water purification systems within hospitals and laboratories. This expansion into healthcare is driven by rising demand for advanced filtration systems to ensure clean environments in medical settings.

Scope of the Report

|

By Product Type |

Powdered Activated Carbon Granular Activated Carbon Extruded Activated Carbon Others (Fibrous Activated Carbon, Pelletized Carbon) |

|

By Application |

Water Treatment Air Purification Food & Beverage Processing Pharmaceuticals Automotive Others (Chemical Industries) |

|

By Raw Material |

Coal-Based Activated Carbon Coconut-Shell-Based Activated Carbon Wood-Based Activated Carbon Others (Petroleum Pitch) |

|

By End-User |

Municipalities Industrial Processing Plants Residential, Commercial Buildings Healthcare & Pharmaceuticals Automotive |

|

By Region |

Saudi Arabia UAE Oman Kuwait Bahrain Qatar |

Products

Key Target Audience

Activated Carbon Manufacturers

Water Treatment Facilities and Companies

Pharmaceutical Companies

Oil & Gas Refineries

Government and Regulatory Bodies (such as GCC Environmental Authority)

Automotive Manufacturers

Food & Beverage Processing Companies

Investments and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Cabot Corporation

Calgon Carbon Corporation

Haycarb PLC

Donau Carbon GmbH

Jacobi Carbons AB

Evoqua Water Technologies LLC

Kuraray Co., Ltd.

Carbon Activated Corporation

ADA-ES Inc.

Oxbow Activated Carbon LLC

Silcarbon Aktivkohle GmbH

Ingevity Corporation

CarboTech AC GmbH

Kureha Corporation

Veolia Water Technologies

Table of Contents

1. GCC Activated Carbon Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. GCC Activated Carbon Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. GCC Activated Carbon Market Analysis

3.1 Growth Drivers (Regulatory Influence, Urbanization, Industrial Growth)

3.1.1 Government Regulations

3.1.2 Increased Water Treatment Facilities

3.1.3 Rise in Air Pollution Control Measures

3.2 Market Challenges (Supply Chain, Manufacturing Costs, Environmental Impact)

3.2.1 Volatile Raw Material Prices

3.2.2 Lack of Technological Advancements in Production

3.2.3 Stringent Environmental Regulations

3.3 Opportunities (R&D, Emerging Applications, Market Expansion)

3.3.1 Technological Advancements in Manufacturing

3.3.2 Expansion into Healthcare and Pharmaceuticals

3.3.3 International Collaborations and Investments

3.4 Trends (Market Maturity, Sustainable Practices, Usage Across Sectors)

3.4.1 Increased Adoption in Water and Air Treatment Sectors

3.4.2 Growth of Renewable Energy and Carbon Management Solutions

3.4.3 Sustainable Sourcing of Raw Materials

3.5 Government Regulations (GCC Policies, Trade Agreements, Certifications)

3.5.1 GCC Waste Management Policies

3.5.2 Air Quality Control Measures

3.5.3 Water Reuse and Treatment Regulations

3.5.4 Carbon Neutral Initiatives

3.6 SWOT Analysis (For Product Efficiency, Market Demand, and Regulation Adaptability)

3.7 Stakeholder Ecosystem (Suppliers, Manufacturers, Regulatory Bodies)

3.8 Porters Five Forces Analysis (Competition Dynamics, Bargaining Power)

3.9 Competition Ecosystem (Local vs. Global Companies, Emerging Competitors)

4. GCC Activated Carbon Market Segmentation

4.1 By Type (In Value %)

4.1.1 Powdered Activated Carbon

4.1.2 Granular Activated Carbon

4.1.3 Extruded Activated Carbon

4.1.4 Others (Fibrous Activated Carbon, Pelletized Carbon)

4.2 By Application (In Value %)

4.2.1 Water Treatment

4.2.2 Air Purification

4.2.3 Food and Beverages Processing

4.2.4 Pharmaceuticals

4.2.5 Automotive

4.2.6 Others (Energy, Chemical Industry)

4.3 By Raw Material (In Value %)

4.3.1 Coal-Based Activated Carbon

4.3.2 Coconut-Shell-Based Activated Carbon

4.3.3 Wood-Based Activated Carbon

4.3.4 Others (Petroleum Pitch)

4.4 By End-User (In Value %)

4.4.1 Municipalities

4.4.2 Industrial Processing Plants

4.4.3 Residential

4.4.4 Commercial Buildings

4.4.5 Healthcare & Pharmaceuticals

4.4.6 Automotive

4.5 By Region (In Value %)

4.5.1 Saudi Arabia

4.5.2 UAE

4.5.3 Oman

4.5.4 Kuwait

4.5.5 Bahrain

4.5.6 Qatar

5. GCC Activated Carbon Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Cabot Corporation

5.1.2 Kuraray Co., Ltd.

5.1.3 Calgon Carbon Corporation

5.1.4 Haycarb PLC

5.1.5 ADA-ES Inc.

5.1.6 Donau Carbon GmbH

5.1.7 Jacobi Carbons AB

5.1.8 Kureha Corporation

5.1.9 CarboTech AC GmbH

5.1.10 Oxbow Activated Carbon LLC

5.1.11 Silcarbon Aktivkohle GmbH

5.1.12 Veolia Water Technologies

5.1.13 Ingevity Corporation

5.1.14 Evoqua Water Technologies LLC

5.1.15 Carbon Activated Corporation

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, Global vs. Local Footprint, R&D Investments)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. GCC Activated Carbon Market Regulatory Framework

6.1 Environmental Standards and Compliance

6.2 Certification Processes and Testing Requirements

6.3 Trade Regulations and Tariffs

6.4 Safety and Quality Standards

7. GCC Activated Carbon Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. GCC Activated Carbon Future Market Segmentation

8.1 By Type (In Value %)

8.2 By Application (In Value %)

8.3 By Raw Material (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9. GCC Activated Carbon Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the GCC Activated Carbon Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to the GCC Activated Carbon Market is compiled and analyzed. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of production quality statistics is conducted to ensure the reliability and accuracy of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple activated carbon manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the GCC Activated Carbon market.

Frequently Asked Questions

01. How big is the GCC Activated Carbon market?

The GCC Activated Carbon market is valued at USD 149 million, based on a five-year historical analysis. Its growth is driven by industrial expansion and regulatory demand for clean water and air.

02. What are the key drivers for the GCC Activated Carbon market?

Key drivers in the GCC Activated Carbon market include stringent environmental regulations, growth in water treatment projects, and increased demand from industrial sectors such as oil & gas and pharmaceuticals.

03. Who are the major players in the GCC Activated Carbon market?

The major players in the GCC Activated Carbon market include Cabot Corporation, Calgon Carbon Corporation, Haycarb PLC, Donau Carbon GmbH, and Jacobi Carbons AB, who dominate due to their product innovation and strong distribution channels.

04. What are the challenges in the GCC Activated Carbon market?

Challenges in the GCC Activated Carbon market include volatile raw material prices, the high cost of production, and stringent environmental regulations that can hamper the manufacturing processes.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.