Global AdTech Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD11022

Region:Global

Author(s):Mukul

Product Code:KROD11022

November 2024

87

The AdTech market is dominated by key players like Google LLC, Meta Platforms, Inc., and Amazon Advertising. These companies hold a significant share of the global market due to their vast user bases, comprehensive advertising solutions, and advanced technological integrations. Furthermore, the consolidation of smaller players through mergers and acquisitions highlights the influence of these industry giants in shaping the future of AdTech.

Growth Drivers

Market Restraints

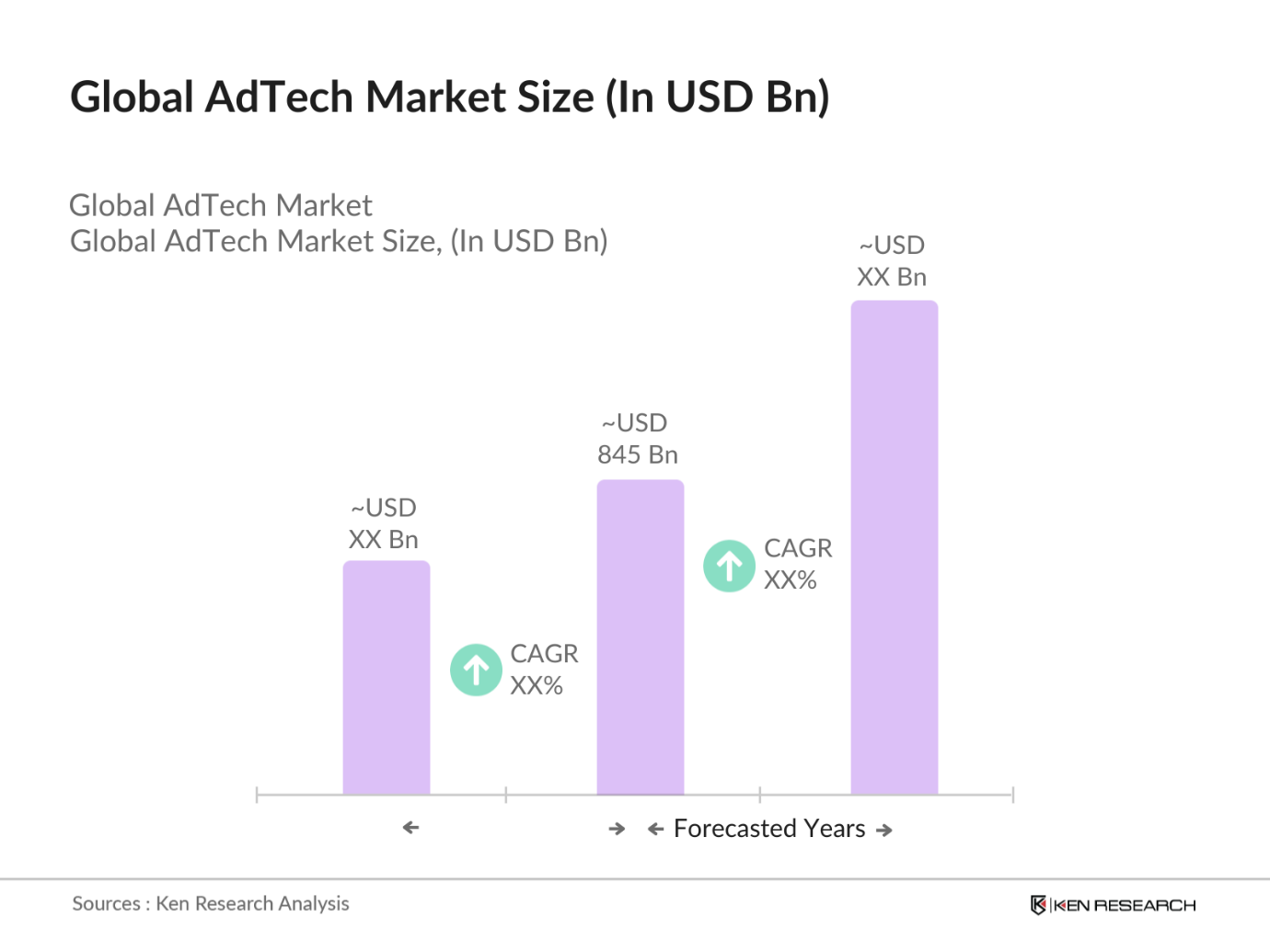

Over the next five years, the AdTech market is expected to experience significant growth, driven by technological innovations in programmatic advertising, AI-powered targeting, and the rise of immersive technologies such as AR and VR. Additionally, the proliferation of connected TV and OTT platforms is expected to further drive revenue, as advertisers seek to capitalize on evolving consumer media consumption patterns. The introduction of stricter privacy regulations will also lead to a shift towards first-party data solutions and contextual advertising.

Market Opportunities

|

Ad Format |

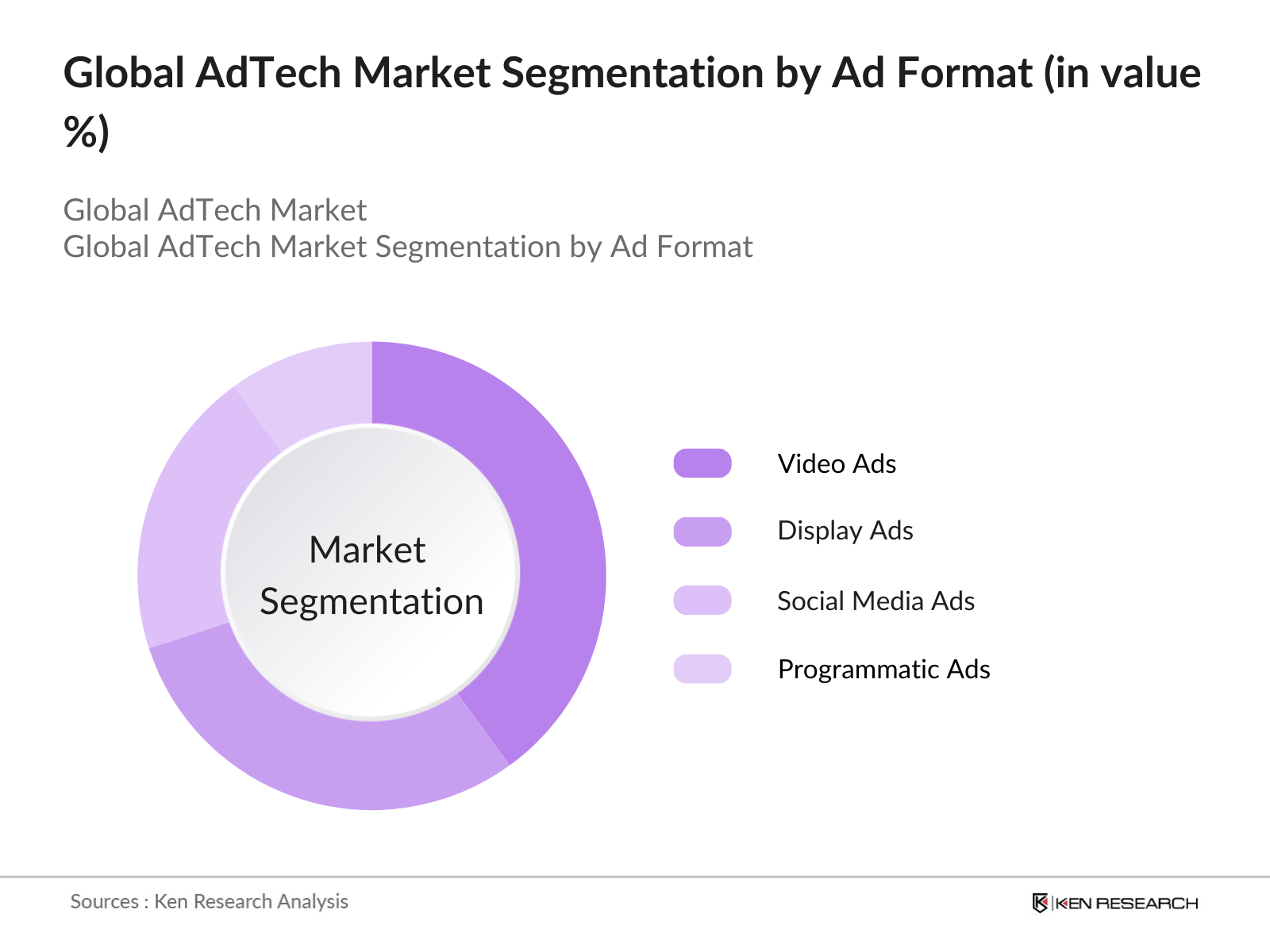

Display Ads, Video Ads, Native Ads, Social Ads, Programmatic Ads |

|

Platform |

Mobile, Desktop, Connected TV, OTT Platforms |

|

Target Audience |

B2C, B2B |

|

Technology |

Programmatic Ad Buying, AI-Driven Targeting, Machine Learning Algorithms |

|

Region |

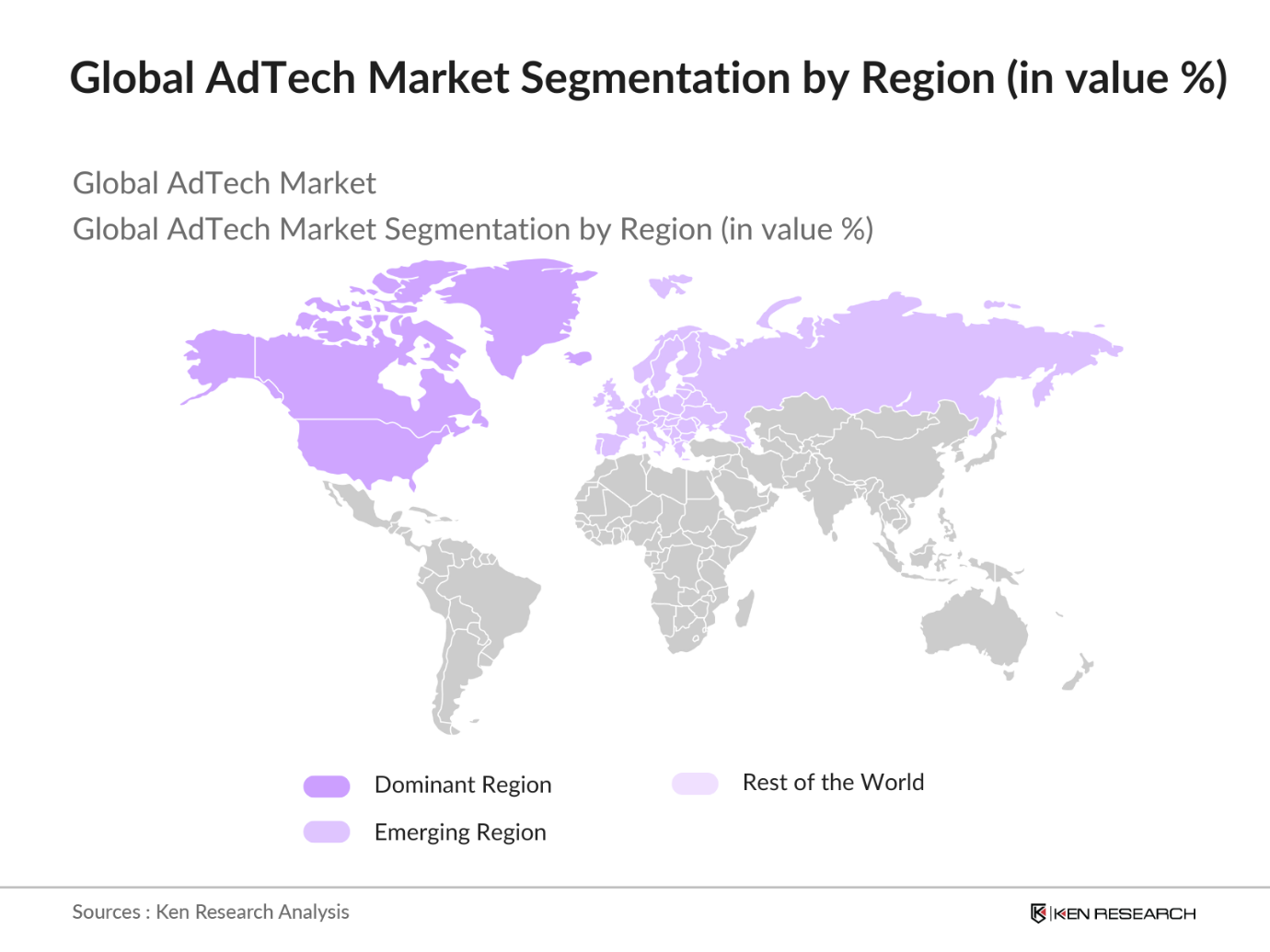

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

1.1 Definition and Scope

1.2 Market Taxonomy (By Ad Formats, Platforms, Geographies, Target Audiences)

1.3 Market Growth Rate (Revenue Growth, Adoption Rate, Tech Penetration)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increase in Digital Ad Spend (Revenue by Platform)

3.1.2 Programmatic Advertising Growth (Automation, Targeting, Ad Exchanges)

3.1.3 Mobile Ad Ecosystem Expansion (Mobile Ad Revenue, App Ads)

3.1.4 Data Privacy Regulations Impact (GDPR, CCPA Compliance)

3.2 Market Challenges

3.2.1 Ad Fraud and Bot Traffic (Fraudulent Ad Revenue Losses)

3.2.2 Ad Blocker Proliferation (Ad Blocker Adoption Rates)

3.2.3 Attribution and ROI Measurement Challenges (Cross-Platform Attribution)

3.3 Opportunities

3.3.1 Expansion of Connected TV (CTV Ad Spend, Viewer Engagement Metrics)

3.3.2 Rise of First-Party Data Solutions (Data Ownership, Privacy Enhancements)

3.3.3 Emergence of AI-Driven Campaign Optimization (AI in Ad Targeting, Personalization)

3.4 Trends

3.4.1 Hyper-Personalization of Ads (Ad Customization Metrics, Real-Time Bidding)

3.4.2 Voice Search Optimization (Voice Ad Engagement, Search Ad Revenue Shift)

3.4.3 Growth in Influencer Marketing Platforms (Influencer Ad Spend, Engagement Metrics)

3.4.4 Expansion into AR/VR Advertising (Immersive Ad Experiences, Adoption Rates)

3.5 Regulatory Environment

3.5.1 Data Privacy Laws (Compliance Costs, Regional Variations)

3.5.2 Content Moderation Policies (Impact on Ad Revenue, Compliance Frameworks)

3.5.3 Consumer Protection Regulations (Transparency Metrics, Advertiser Accountability)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Ad Networks, DSPs, SSPs, Advertisers, Publishers)

3.8 Porters Five Forces

3.9 Competitive Ecosystem

4.1 By Ad Format (In Value %)

4.1.1 Display Ads

4.1.2 Video Ads

4.1.3 Native Ads

4.1.4 Social Media Ads

4.1.5 Programmatic Ads

4.2 By Platform (In Value %)

4.2.1 Mobile

4.2.2 Desktop

4.2.3 Connected TV

4.2.4 OTT Platforms

4.3 By Target Audience (In Value %)

4.3.1 B2C

4.3.2 B2B

4.4 By Technology (In Value %)

4.4.1 Programmatic Ad Buying

4.4.2 AI-Driven Ad Targeting

4.4.3 Machine Learning Algorithms

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1 Google LLC

5.1.2 Meta Platforms, Inc.

5.1.3 Amazon Advertising

5.1.4 Adobe Advertising Cloud

5.1.5 The Trade Desk, Inc.

5.1.6 MediaMath

5.1.7 Criteo S.A.

5.1.8 Xandr (AT&T)

5.1.9 Verizon Media

5.1.10 Roku Advertising

5.1.11 PubMatic

5.1.12 Magnite

5.1.13 InMobi

5.1.14 AppLovin

5.1.15 Taboola

5.2 Cross Comparison Parameters (Headquarters, No. of Employees, Revenue, Market Position, Inception Year, Global Reach, Ad Format Focus, Market Share)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Data Privacy Compliance (GDPR, CCPA)

6.2 Consumer Protection Guidelines

6.3 Industry Standards and Certifications

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Ad Format (In Value %)

8.2 By Platform (In Value %)

8.3 By Target Audience (In Value %)

8.4 By Technology (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

This step involves identifying all key variables impacting the AdTech market, including platform dynamics, technological adoption, and regulatory frameworks. Extensive desk research was conducted utilizing proprietary databases and secondary research tools to gather comprehensive market data.

The second phase involves analyzing historical data of the AdTech market. Key metrics such as ad spend, platform performance, and revenue generation by ad format are considered to construct an accurate picture of market dynamics.

Market hypotheses were developed based on collected data and validated through interviews with key AdTech industry experts. This method ensured the reliability of market estimates, including engagement with top industry leaders.

In this final phase, data from both primary and secondary research sources were synthesized to create a comprehensive, actionable report. Cross-validation with digital advertising companies and platforms further solidified the accuracy of the analysis.

The global AdTech market, valued at USD 845 billion, is driven by increased digital ad spending and technological advancements like AI, programmatic buying, and mobile advertising growth.

Key challenges include ad fraud, bot traffic, data privacy concerns, and measurement issues in cross-platform attribution. Stricter regulations and a higher reliance on third-party cookies also create challenges.

The market is dominated by industry giants like Google LLC, Meta Platforms, Inc., Amazon Advertising, The Trade Desk, and Criteo S.A., thanks to their vast global reach and advanced tech-driven solutions.

Key growth drivers include the rise in digital ad spending, the proliferation of mobile devices, the adoption of programmatic advertising, and advancements in AI for personalized ad targeting.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.