Global Aircraft Carrier Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD9951

November 2024

100

About the Report

Global Aircraft Carrier Market Overview

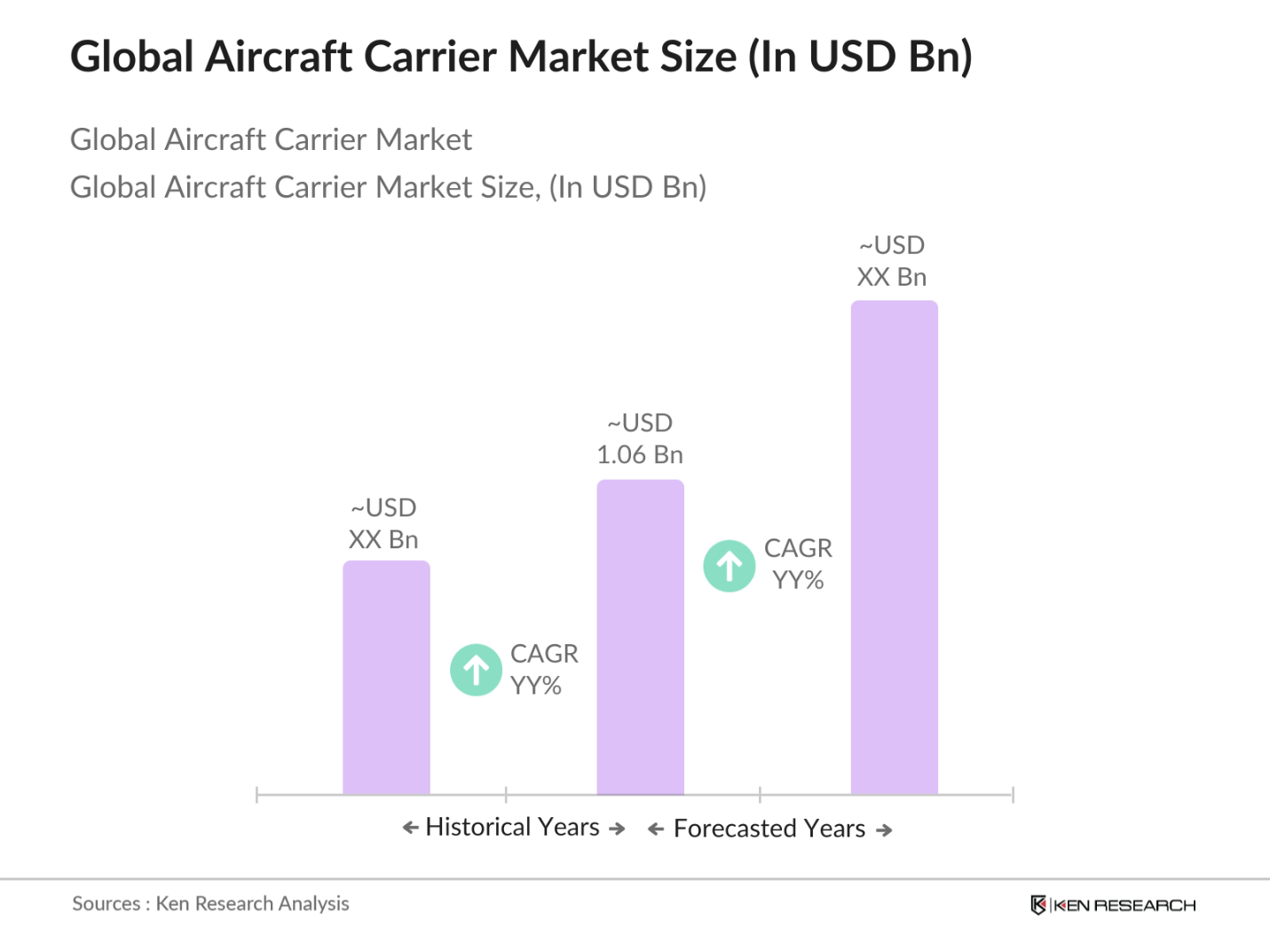

- The global aircraft carrier market was valued at approximately USD 1.06 billion, driven by increasing defense budgets, technological advancements, and growing geopolitical tensions. Countries such as the United States, China, and India are heavily investing in expanding their naval capabilities, which has significantly boosted the demand for aircraft carriers. Additionally, advancements in nuclear propulsion technology have made aircraft carriers more versatile, capable of long-term operations with minimal refueling requirements. These factors are creating strong momentum in the aircraft carrier market, ensuring steady growth through continuous investment in national security.

- Countries like the United States, China, and India dominate the aircraft carrier market due to their large-scale defense budgets and strategic importance in global geopolitics. The United States remains the leader with its fleet of advanced nuclear-powered supercarriers, while China and India are rapidly expanding their naval presence to secure influence in key strategic waterways such as the South China Sea and the Indian Ocean. These nations prioritize aircraft carriers as a symbol of military strength and a critical tool for power projection.

- Technological advancements are a key growth driver for the aircraft carrier market. In 2023, the U.S. Navy's Gerald R. Ford-class carriers are equipped with Electromagnetic Aircraft Launch Systems (EMALS), which enhance the carrier's ability to launch heavier aircraft. The integration of advanced stealth technology and radar-absorbing materials reduces the visibility of carriers to enemy radar. Additionally, integrated weapons systems, such as the F-35 Lightning IIs deployment capabilities, enhance the strike range and precision of aircraft carriers, making them formidable assets in modern naval warfare.

Global Aircraft Carrier Market Segmentation

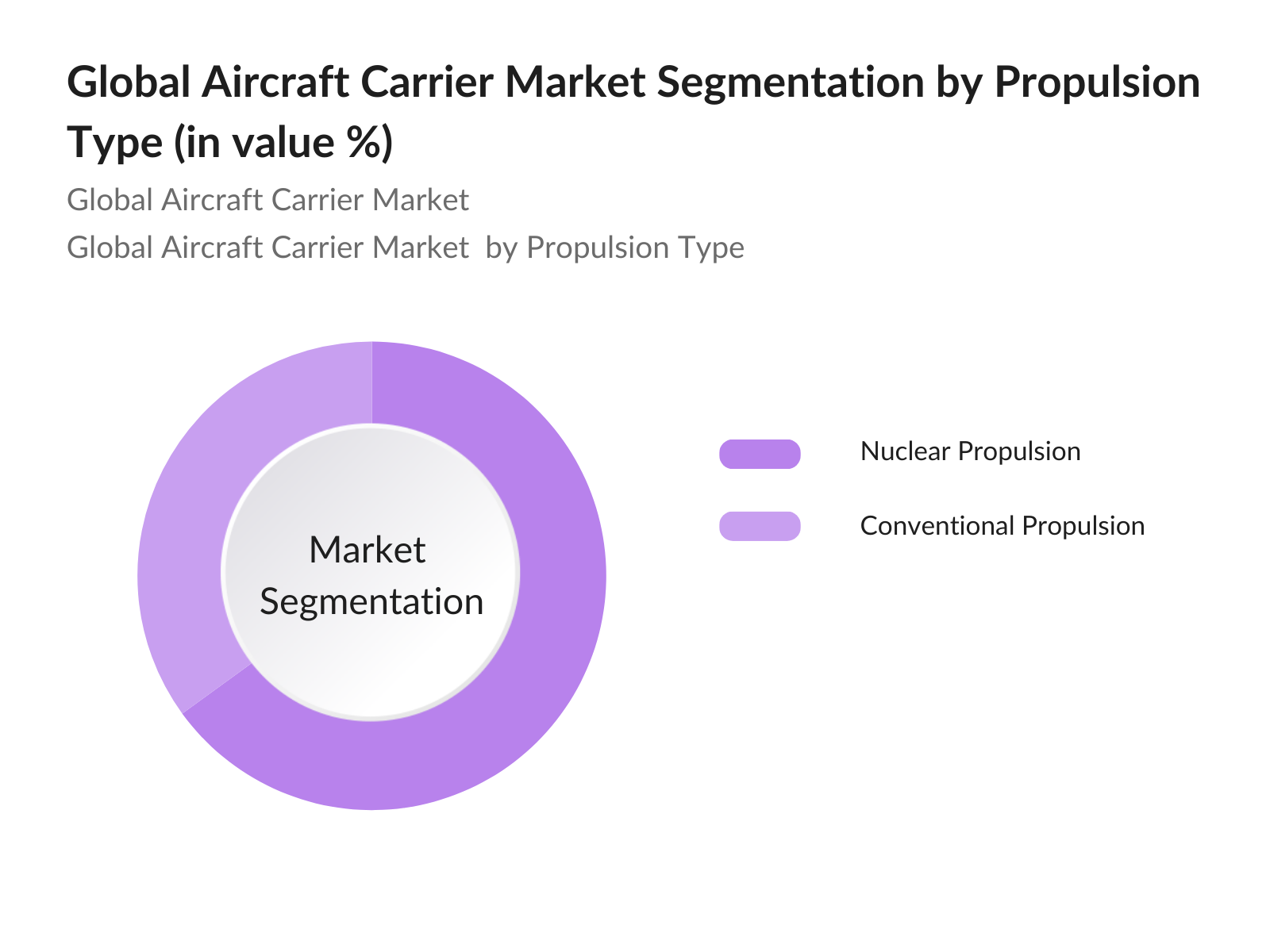

By Propulsion Type: The global aircraft carrier market is segmented by propulsion type into conventional propulsion and nuclear propulsion. Nuclear propulsion dominates the market as it offers superior operational capabilities compared to conventional propulsion. Nuclear-powered carriers are capable of staying at sea for longer periods without refueling, making them ideal for extended missions in remote regions. The ability to generate vast amounts of power onboard also allows for the operation of advanced systems, including electromagnetic catapults and high-powered radar systems.

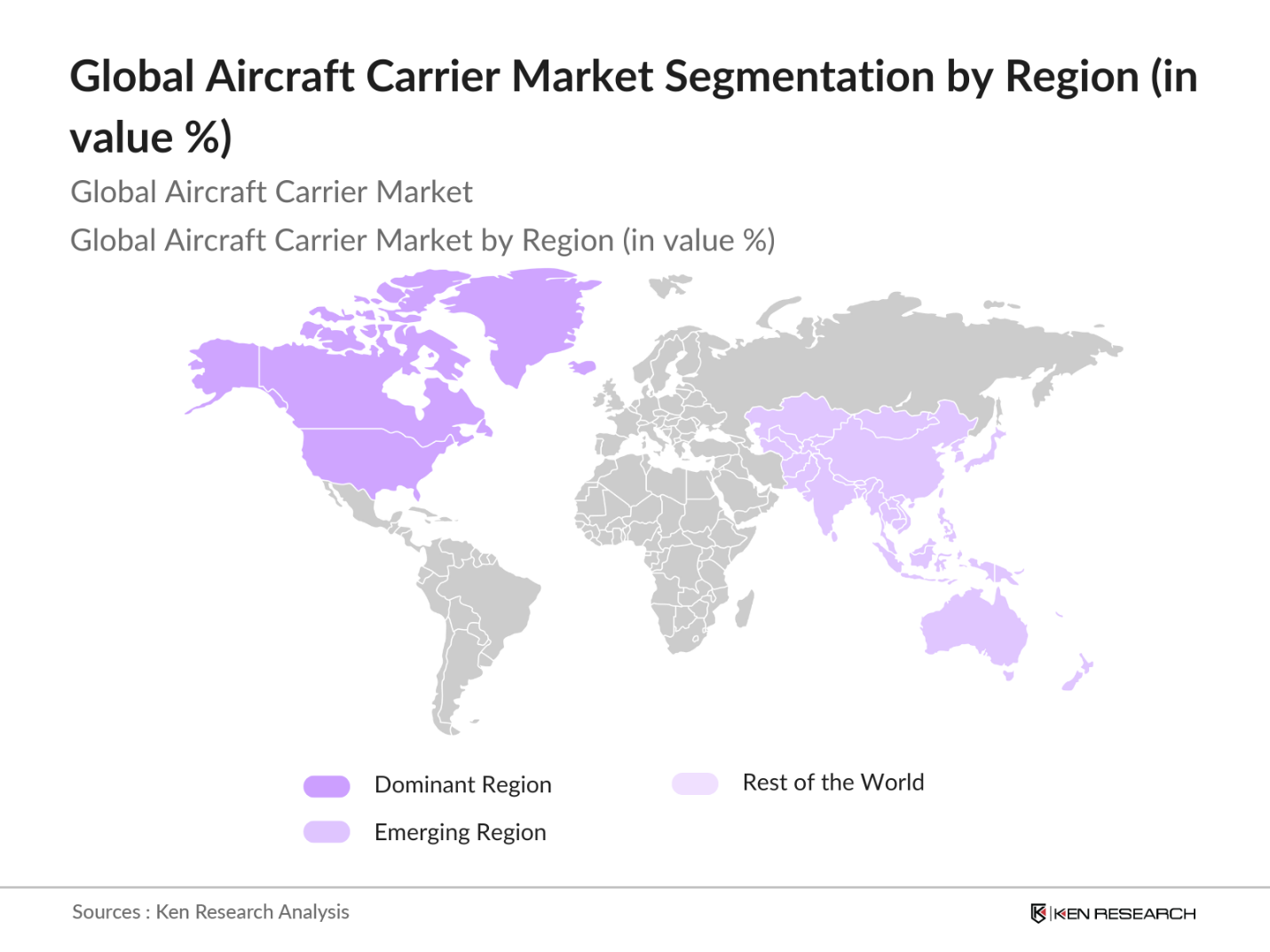

By Region: The global aircraft carrier market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. North America holds the largest share in the market, driven by the presence of the United States, which maintains the worlds largest fleet of aircraft carriers. The U.S. operates advanced nuclear-powered carriers, giving the region a strategic advantage in global naval operations and power projection.

Global Aircraft Carrier Market Competitive Landscape

The global aircraft carrier market is highly consolidated, with a few major players dominating the industry. Countries such as the United States, France, China, and Russia have their own established defense contractors responsible for building and maintaining these massive warships. The major defense contractors work closely with government agencies to design, construct, and deliver the latest-generation aircraft carriers.

|

Company Name |

Establishment Year |

Headquarters |

Employees |

Annual Revenue (USD) |

Key Contracts |

Market Share |

R&D Expenditure |

Fleet Size (2023) |

Technology Innovations |

|

Huntington Ingalls Industries |

1886 |

Virginia, USA |

42,000 |

- |

- |

- |

- |

- |

- |

|

General Dynamics |

1899 |

Virginia, USA |

100,000 |

- |

- |

- |

- |

- |

- |

|

BAE Systems |

1999 |

London, UK |

89,600 |

- |

- |

- |

- |

- |

- |

|

Naval Group |

1631 |

Paris, France |

15,000 |

- |

- |

- |

- |

- |

- |

|

Fincantieri S.p.A |

1959 |

Trieste, Italy |

19,000 |

- |

- |

- |

- |

- |

- |

Global Aircraft Carrier Market Analysis

Market Growth Drivers

- Rising Defense Expenditures (Government defense budgets, National security priorities): Rising global defense budgets are a significant driver of the aircraft carrier market. In 2023, the U.S. allocated approximately $842 billion to its defense budget, prioritizing naval advancements, including aircraft carriers. The U.K.'s defense budget in 2024 stood at 48 billion, reflecting a continued focus on maritime dominance. China, another major player, has dedicated 1.55 trillion for defense in 2023, a portion of which supports its aircraft carrier programs. These figures reflect an upward trend in defense allocations globally, driven by the need to strengthen naval capabilities for national security.

- Geopolitical Tensions (Regional conflicts, Territorial disputes, Military presence in strategic waters): Geopolitical tensions, particularly in regions like the South China Sea and the Arctic, are driving demand for aircraft carriers. In 2023, critical maritime routes used for transporting oil and other resources have become points of strategic importance for national security. Countries such as the U.S., China, and Russia have increased their naval presence to protect territorial claims and ensure the safety of energy transport routes. This has led to the commissioning of new aircraft carriers by nations like India, which is developing its second carrier, and Japan, which is modifying its Izumo-class ships to operate fixed-wing aircraft.

- Technological Advancements (Advanced propulsion systems, Stealth technologies, Integrated weapons systems): Technological advancements are a key growth driver for the aircraft carrier market. In 2024, the U.S. Navy's Gerald R. Ford-class carriers are equipped with Electromagnetic Aircraft Launch Systems (EMALS), which enhance the carrier's ability to launch heavier aircraft. The integration of advanced stealth technology and radar-absorbing materials reduces the visibility of carriers to enemy radar. Additionally, integrated weapons systems, such as the F-35 Lightning IIs deployment capabilities, enhance the strike range and precision of aircraft carriers, making them formidable assets in modern naval warfare.

Market Challenges:

- High Capital Costs (Construction, maintenance, modernization expenses): The capital expenditure required for aircraft carrier construction and maintenance is a significant challenge. The U.S. Navy's Gerald R. Ford-class carriers cost approximately $13.3 billion per unit in 2023. Additionally, modernization expenses for carriers, including upgrading propulsion systems and integrating advanced weaponry, are substantial. The long-term operational costs, including fuel, crew salaries, and periodic overhauls, further contribute to the financial burden on defense budgets, making it difficult for nations with limited resources to invest in aircraft carriers.

- Regulatory and Environmental Issues (Emission standards, Global defense procurement protocols): Aircraft carriers face regulatory and environmental challenges, particularly related to emission standards and compliance with international defense procurement protocols. In 2023, the International Maritime Organization (IMO) imposed stricter regulations on sulfur emissions from naval vessels, pushing for cleaner propulsion systems. Moreover, countries purchasing aircraft carriers must navigate complex global defense procurement laws, such as the U.S. Foreign Military Sales (FMS) program, which can delay acquisitions and increase costs. These regulatory hurdles impact the timeline and cost-effectiveness of carrier development.

Global Aircraft Carrier Market Future Outlook

The global aircraft carrier market is poised for steady growth over the next five years, driven by increasing global defense expenditures, advancements in carrier design, and the need for power projection capabilities in strategic regions. Governments around the world are investing in modernizing existing fleets and commissioning new carriers, particularly in the Asia-Pacific and Middle East regions, where maritime security is a top priority. Nuclear propulsion and modular designs will continue to play a pivotal role in shaping the future of aircraft carriers, allowing for longer deployments and more flexibility in missions. The introduction of autonomous systems and advanced AI-based technologies will further transform the operational capabilities of aircraft carriers, making them a cornerstone of 21st-century naval strategy.

Market Opportunities:

- Adoption of Nuclear Propulsion (Fuel efficiency, Long-term deployment benefits): Nuclear propulsion presents a significant opportunity for the aircraft carrier market due to its fuel efficiency and extended operational capabilities. As of 2024, 11 U.S. Navy carriers, including the Nimitz and Gerald R. Ford classes, are nuclear-powered, allowing them to remain at sea for up to 20 years without refueling. This capability reduces operational costs and enhances long-term deployment in strategic waters. The adoption of nuclear propulsion is being explored by nations like India and the U.K. for their next-generation carrier programs.

- Expansion into Emerging Defense Markets (Asia-Pacific, Middle East carrier procurement trends): The expansion of the aircraft carrier market into emerging defense regions like Asia-Pacific and the Middle East offers significant growth opportunities. In 2023, India allocated 5.94 trillion for defense spending, with a portion dedicated to expanding its naval fleet, including aircraft carriers. Similarly, the United Arab Emirates and Saudi Arabia are exploring carrier procurement to enhance their maritime capabilities in the Persian Gulf. The increasing military budgets in these regions reflect a strategic interest in acquiring aircraft carriers for regional security and maritime control.

Scope of the Report

|

By Propulsion Type |

Conventional Propulsion Nuclear Propulsion |

|

By Carrier Size |

Supercarriers (>70,000 tons) Medium Carriers (40,000-70,000 tons) Light Carriers (<40,000 tons) |

|

By Aircraft Type |

Fixed-wing aircraft Rotary-wing aircraft Unmanned Aerial Vehicles (UAVs) |

|

By End-User |

Naval Defense Forces Homeland Security Private Maritime Security |

|

By Region |

North America Europe Asia-Pacific Middle East Latin America |

Products

Key Target Audience

Naval Defense Forces

Government and Regulatory Bodies (e.g., U.S. Department of Defense, Ministry of Defence - UK, Ministry of National Defense - China)

Private Maritime Security Companies

Defense Contractors and Subcontractors

Aircraft Manufacturers

Shipbuilding Companies

Investments and Venture Capital Firms

Autonomous System Technology Providers

Companies

Players Mention in the Report

Huntington Ingalls Industries

General Dynamics

BAE Systems

Naval Group

Fincantieri S.p.A

Lockheed Martin Corporation

Thales Group

Northrop Grumman Corporation

Kawasaki Heavy Industries

Mitsubishi Heavy Industries

Daewoo Shipbuilding & Marine Engineering

China Shipbuilding Industry Corporation (CSIC)

United Shipbuilding Corporation (USC)

Larsen & Toubro Limited

Thyssenkrupp Marine Systems

Table of Contents

1. Global Aircraft Carrier Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy (Categories of carriers, Role in defense strategy, Regional and global deployment significance)

1.3. Market Growth Rate (Current fleet expansion, Carrier commissioning timelines, Defense budget allocations)

1.4. Market Segmentation Overview (By propulsion type, By carrier size, By region, By aircraft type)

2. Global Aircraft Carrier Market Size (In USD Bn)

2.1. Historical Market Size (Value and volume, Fleet modernization programs)

2.2. Year-On-Year Growth Analysis (Fleet expansions, Procurement trends, Military strategies)

2.3. Key Market Developments and Milestones (Carrier development programs, Major defense deals, International cooperation)

3. Global Aircraft Carrier Market Analysis

3.1. Growth Drivers

3.1.1. Rising Defense Expenditures (Government defense budgets, National security priorities)

3.1.2. Geopolitical Tensions (Regional conflicts, Territorial disputes, Military presence in strategic waters)

3.1.3. Technological Advancements (Advanced propulsion systems, Stealth technologies, Integrated weapons systems)

3.1.4. Strategic Military Partnerships (NATO, Joint naval exercises, Multi-national carrier collaborations)

3.2. Market Challenges

3.2.1. High Capital Costs (Construction, maintenance, modernization expenses)

3.2.2. Regulatory and Environmental Issues (Emission standards, Global defense procurement protocols)

3.2.3. Prolonged Development Timelines (Delays in carrier construction, Budget overruns)

3.3. Opportunities

3.3.1. Adoption of Nuclear Propulsion (Fuel efficiency, Long-term deployment benefits)

3.3.2. Expansion into Emerging Defense Markets (Asia-Pacific, Middle East carrier procurement trends)

3.3.3. Upgrading Existing Fleets (Modernization programs, Aircraft integration)

3.4. Trends

3.4.1. Increase in Aircraft Carrier Construction (New shipyards, Technological advancements)

3.4.2. Focus on Multi-role Capabilities (Enhanced air, surface, and underwater capabilities)

3.4.3. Modular Design (Adaptable designs for different missions, Reduced construction time)

3.5. Government Regulations

3.5.1. Defense Acquisition Regulations (Procurement standards, National defense budgets)

3.5.2. Environmental Compliance (Nuclear reactor regulations, Green energy integration)

3.5.3. International Maritime Laws (Carrier operations in international waters)

3.6. SWOT Analysis (Strategic analysis based on Strengths, Weaknesses, Opportunities, Threats specific to aircraft carriers)

3.7. Stakeholder Ecosystem

3.7.1. Shipbuilders (Government contractors, Naval shipyards, Leading private shipbuilders)

3.7.2. Technology Providers (Radar systems, Combat systems, Aircraft integration technology)

3.8. Porters Five Forces (Competition, Threat of new entrants, Bargaining power of suppliers and buyers, Threat of substitutes)

3.9. Competition Ecosystem (Key players, Market positioning, Strategic alliances)

4. Global Aircraft Carrier Market Segmentation

4.1. By Propulsion Type (In Value %)

4.1.1. Conventional Propulsion (Diesel-electric, Gas turbine)

4.1.2. Nuclear Propulsion

4.2. By Carrier Size (In Value %)

4.2.1. Supercarriers (>70,000 tons)

4.2.2. Medium Carriers (40,000 70,000 tons)

4.2.3. Light Carriers (<40,000 tons)

4.3. By Aircraft Type (In Value %)

4.3.1. Fixed-wing aircraft

4.3.2. Rotary-wing aircraft

4.3.3. Unmanned Aerial Vehicles (UAVs)

4.4. By Region (In Value %)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia-Pacific

4.4.4. Middle East

4.4.5. Latin America

4.5. By End-User (In Value %)

4.5.1. Naval Defense Forces

4.5.2. Homeland Security

4.5.3. Private Maritime Security

5. Global Aircraft Carrier Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors (Including financial analysis, strategic initiatives, recent projects, and innovations)

5.1.1. Huntington Ingalls Industries

5.1.2. BAE Systems

5.1.3. General Dynamics

5.1.4. Naval Group

5.1.5. Fincantieri S.p.A

5.1.6. Lockheed Martin Corporation

5.1.7. Thales Group

5.1.8. Northrop Grumman Corporation

5.1.9. Kawasaki Heavy Industries

5.1.10. Mitsubishi Heavy Industries

5.1.11. Daewoo Shipbuilding & Marine Engineering

5.1.12. China Shipbuilding Industry Corporation (CSIC)

5.1.13. United Shipbuilding Corporation (USC)

5.1.14. Larsen & Toubro Limited

5.1.15. Thyssenkrupp Marine Systems

5.2. Cross Comparison Parameters (Production capacity, Technological capabilities, Defense contracts, Global presence, R&D Investments, Revenue generation, Fleet delivery timelines, Innovation Index)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Innovations, Military contracts)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Private equity, Government grants, Defense funds)

6. Global Aircraft Carrier Market Regulatory Framework

6.1. Defense Acquisition Guidelines

6.2. Naval Construction Standards

6.3. International Defense Cooperation Treaties

6.4. Compliance with Maritime Safety Laws

7. Global Aircraft Carrier Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Rising defense budgets, Strategic regional defense expansions)

8. Global Aircraft Carrier Future Market Segmentation

8.1. By Propulsion Type (In Value %)

8.2. By Carrier Size (In Value %)

8.3. By Aircraft Type (In Value %)

8.4. By Region (In Value %)

8.5. By End-User (In Value %)

9. Global Aircraft Carrier Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Marketing Strategies for Market Expansion

9.3. White Space Opportunity Analysis

9.4. Customer Targeting Strategies

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involved identifying the primary stakeholders within the global aircraft carrier market, including naval forces, defense contractors, shipbuilders, and technology providers. This was achieved through desk research, leveraging secondary databases, and proprietary research tools to gather comprehensive industry insights.

Step 2: Market Analysis and Construction

During this phase, historical data was analyzed, focusing on aircraft carrier production rates, government defense contracts, and technological advancements. This data was used to estimate the current market size and segment it based on propulsion type, carrier size, and geographical region.

Step 3: Hypothesis Validation and Expert Consultation

Key market assumptions were validated through expert interviews with industry professionals from defense contractors, naval forces, and shipbuilding firms. These insights helped refine the data and provide additional context on market dynamics.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing the data and producing an extensive report. Direct engagement with defense contractors ensured the accuracy of the market forecasts and insights related to future carrier innovations and deployment strategies.

Frequently Asked Questions

01. How big is the Global Aircraft Carrier Market?

The global aircraft carrier market is valued at USD 1.06 billion, driven by increasing defense budgets, growing geopolitical tensions, and advancements in carrier technologies such as nuclear propulsion.

02. What are the challenges in the Aircraft Carrier Market?

Key challenges in the market include the high costs of construction and maintenance, regulatory hurdles related to environmental compliance, and prolonged development timelines due to the complexity of integrating advanced technologies.

03. Who are the major players in the Aircraft Carrier Market?

Major players in the global aircraft carrier market include Huntington Ingalls Industries, General Dynamics, BAE Systems, Naval Group, and Fincantieri S.p.A. These companies dominate due to their expertise in shipbuilding, strong relationships with government defense agencies, and access to large defense budgets.

04. What drives the growth of the Aircraft Carrier Market?

The growth of the aircraft carrier market is driven by rising global defense expenditures, increasing geopolitical tensions, and the development of advanced technologies such as nuclear propulsion, electromagnetic catapult systems, and stealth capabilities.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.