Global Automotive Center Console Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD7935

December 2024

96

About the Report

Global Automotive Center Console Market Overview

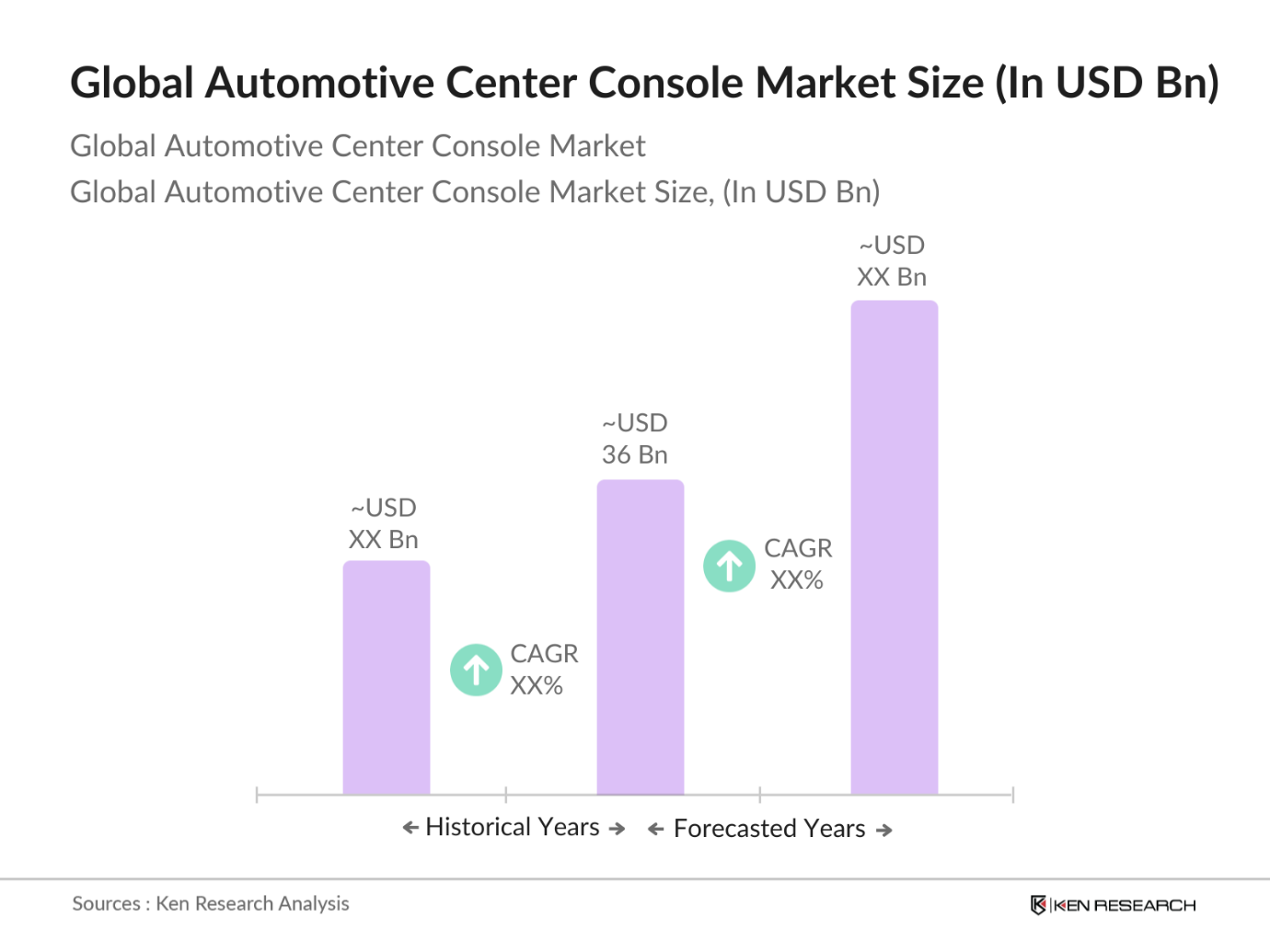

- The Global Automotive Center Console Market is valued at USD 36 billion, based on a five-year historical analysis. The market's growth is predominantly driven by the increasing demand for advanced vehicle interiors, which are equipped with infotainment systems, smart technologies, and ergonomically designed components. Additionally, rising consumer preferences for comfort, integrated functionalities such as wireless charging, and storage within vehicles are key drivers for the center console market.

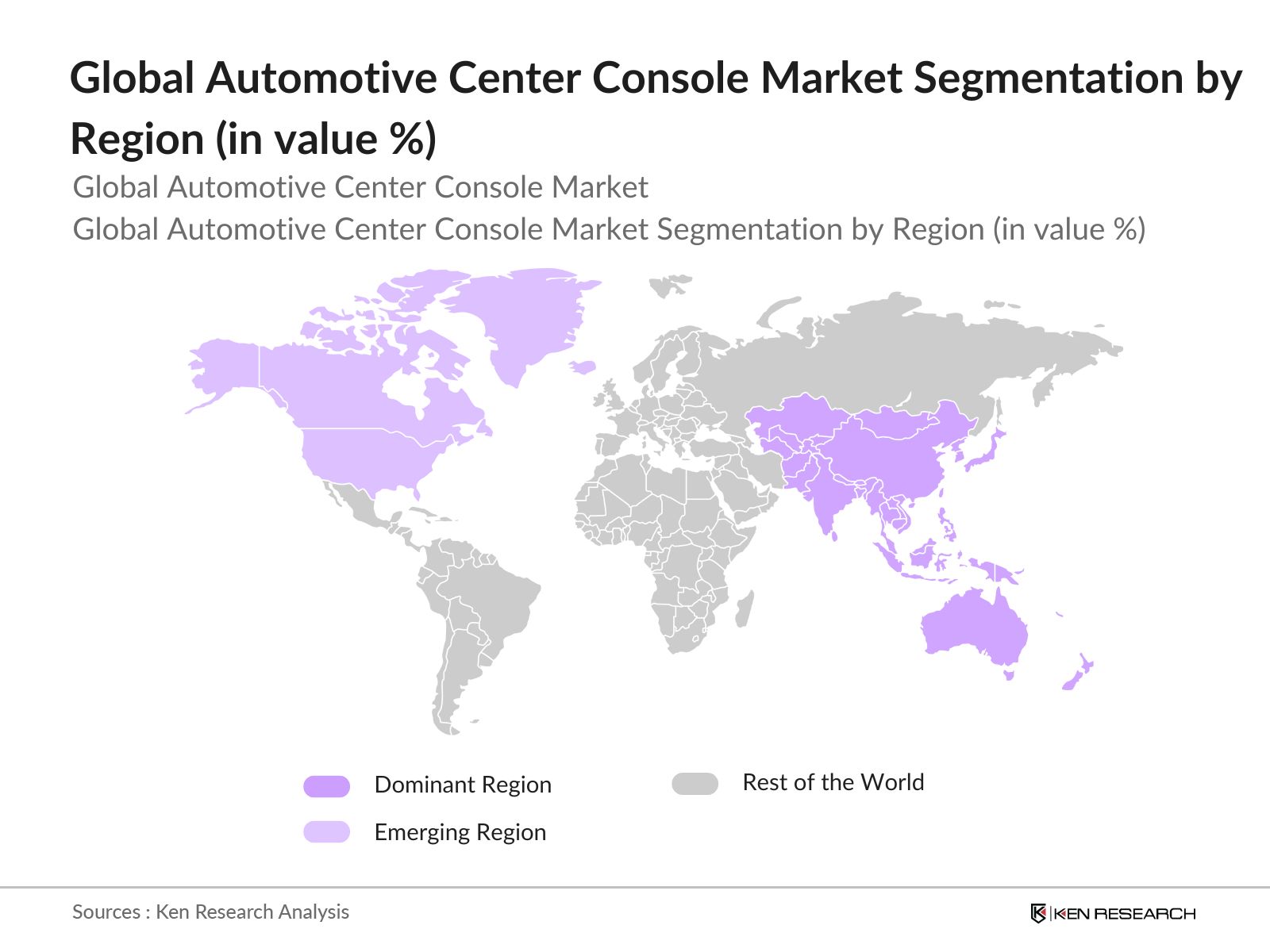

- Countries such as China, Germany, and the United States dominate the automotive center console market. These countries house major automobile manufacturers and have strong technological infrastructures. Chinas dominance is attributed to its robust automotive manufacturing sector, which is the largest globally, while Germany is renowned for its innovation in luxury vehicle interiors. The U.S. market is led by high consumer demand for premium and technologically advanced vehicles.

- Governments worldwide are imposing stricter safety compliance regulations on in-car infotainment systems to reduce driver distraction. In 2023, over 20 countries, including the United States and members of the European Union, implemented new safety standards that require automotive center consoles to meet ergonomic design guidelines that minimize driver interaction time. These regulations have spurred innovation in hands-free and voice-activated technologies, aligning with broader vehicle safety measures globally.

Global Automotive Center Console Market Segmentation

- By Product Type: The Automotive Center Console Market is segmented into fixed center consoles, adjustable center consoles, and modular center consoles. Recently, modular center consoles hold a dominant market share due to their flexibility and the ability to incorporate various functions such as armrests, infotainment control panels, and storage compartments. Their popularity is particularly pronounced in high-end and luxury vehicles, where consumer demand for customization is strong.

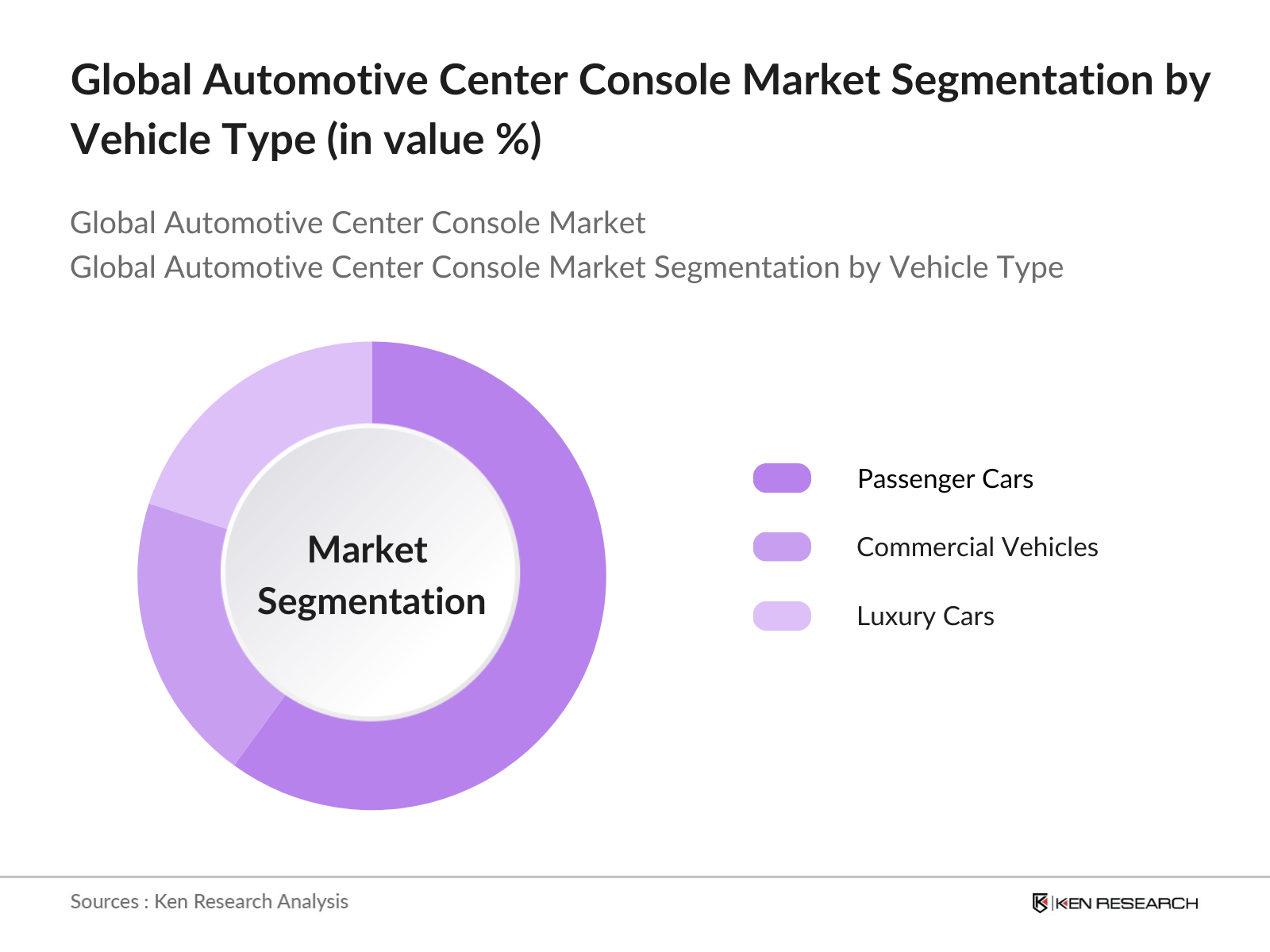

- By Vehicle Type: The market is further segmented by vehicle type into passenger cars, commercial vehicles, and luxury cars. Passenger cars dominate the market share due to the sheer volume of production and the need for center consoles to offer both functionality and comfort. Additionally, the integration of smart and infotainment features has become a necessity for passenger car manufacturers to stay competitive.

- By Region: Geographically, the market is segmented into Asia-Pacific, Europe, North America, Middle East & Africa, and Latin America. The Asia-Pacific region, particularly China and Japan, holds a notable share of the global automotive center console market due to high vehicle production and strong domestic demand. Additionally, growing automotive manufacturing capabilities in India and Southeast Asia contribute to this region's market dominance.

Global Automotive Center Console Market Competitive Landscape

The Global Automotive Center Console Market is characterized by the presence of key players with strong portfolios in automotive interiors. The competitive landscape shows a mix of global giants and specialized interior solution providers. Many companies focus on innovation, introducing smart consoles with integrated infotainment, wireless charging, and customizable modules.

Global Automotive Center Console Market Analysis

Global Automotive Center Console Market Growth Drivers

- Demand for In-car Connectivity: In 2024, the global push for vehicle electrification and connectivity has driven automotive manufacturers to focus on integrating advanced in-car connectivity solutions. This includes wireless communication systems, internet-based applications, and real-time navigation tools. According to the International Telecommunication Union (ITU), the number of connected vehicles globally surpassed 237 million in 2023, with an increasing percentage of vehicles adopting 5G technology for enhanced infotainment and telematics. The demand for real-time traffic updates, multimedia streaming, and connected devices has made the automotive center console a crucial interface for vehicle-to-device communication.

- Integration of Infotainment Systems: Infotainment systems have become integral to modern vehicles, with nearly all new vehicles produced in 2023 featuring some form of in-car entertainment and information interface. The demand for larger touchscreens and multifunctional control centers has grown rapidly, with automakers like Tesla, BMW, and Audi focusing on cutting-edge technologies. Data from the World Bank indicates that 1.4 billion vehicles were in use globally by the end of 2022, and a proportion of new models now include enhanced infotainment systems, which contribute to the rapid growth of the automotive center console market.

- Rise of Electric Vehicles (EVs): With the ongoing electrification of the global automotive industry, electric vehicles (EVs) have reached a cumulative total of over 16.5 million units by 2023, according to the International Energy Agency (IEA). The rise of EVs has influenced the design of automotive interiors, with more emphasis on creating streamlined, minimalistic consoles that accommodate digital interfaces and electric-specific functionalities, such as battery monitoring and energy efficiency displays. The growth of the EV market is driving demand for advanced center consoles that are highly integrated with electric vehicle systems.

Global Automotive Center Console Market Challenges

- High Production Costs: The production of automotive center consoles involves high material and manufacturing costs, especially as consumers demand advanced features like touchscreen displays and wireless connectivity. The rising cost of semiconductors, essential for infotainment systems, further exacerbates production expenses. According to the U.S. Bureau of Labor Statistics, manufacturing costs for automotive components rose by an average of 7% between 2022 and 2023 due to global inflation and supply chain disruptions, especially in Asia-Pacific regions where many electronic components are sourced.

- Limited Aftermarket Opportunities: While the aftermarket for vehicle components is robust, automotive center consoles are less commonly replaced or upgraded due to the complexity and cost of integrating advanced electronics into existing vehicle systems. In 2023, the global aftermarket was valued at over $400 billion, but automotive interior components, including center consoles, represented a minimal share. This is largely because consoles are typically customized for specific vehicle models, making aftermarket replacements less feasible for consumers, which limits growth opportunities.

Global Automotive Center Console Market Future Outlook

The Global Automotive Center Console Market is expected to see advancements over the next five years. The market is poised for growth due to the increasing shift toward electric vehicles, autonomous driving, and connected car ecosystems. Moreover, rising consumer demand for premium vehicle interiors and personalized design options will likely fuel this growth. Companies focusing on lightweight materials, smart technology integration, and sustainable solutions are expected to outperform others in this competitive space.

Global Automotive Center Console Market Opportunities

- Opportunities in Electric and Hybrid Vehicles: The adoption of electric and hybrid vehicles presents a significant growth opportunity for the automotive center console market. In 2023, electric and hybrid vehicles made up nearly 14% of all vehicles sold globally, with substantial demand coming from Europe and China, according to the International Energy Agency. As EV and hybrid vehicles continue to gain market share, center consoles will play a critical role in managing battery systems, range monitoring, and energy efficiency controls, creating new avenues for console innovation and integration.

- Digital Interface Advancements: The increasing integration of digital interfaces within vehicle center consoles offers a lucrative opportunity for market growth. According to the International Data Corporation (IDC), by the end of 2023, over 90% of new vehicles globally featured digital display interfaces in their center consoles, up from 75% in 2021. These interfaces allow consumers to control navigation, media, and connectivity features, increasing the value and functionality of the console, and offering an expanding market for OEMs focused on digital innovation.

Scope of the Report

By Product Type | Fixed Center Consoles Adjustable Center Consoles Modular Center Consoles |

By Vehicle Type | Passenger Cars Commercial Vehicles Luxury Cars |

By Material Type | Plastic Metal Leather and Fabric |

By Technology | Integrated Infotainment HVAC Integration Wireless Charging |

By Distribution Channel | OEMs Aftermarket |

By Region | Asia-Pacific Europe North America Middle East & Africa Latin America |

Products

Key Target Audience

Automotive Manufacturers

OEM Suppliers

Interior Design Companies

Banks and financial Institutions

Component Manufacturers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (NHTSA, European Union Commission)

Technological Solution Providers

Automotive Dealership Networks

Companies

Players Mentioned in the Report

Faurecia

Continental AG

Yanfeng Automotive Interiors

Toyota Boshoku Corporation

Magna International Inc.

Lear Corporation

Hyundai Mobis

Grupo Antolin

Johnson Controls

DURA Automotive Systems

Table of Contents

1. Global Automotive Center Console Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Automotive Center Console Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Key Market Developments and Milestones

2.3. Year-On-Year Growth Analysis

3. Global Automotive Center Console Market Analysis

3.1. Growth Drivers (Increasing vehicle production, Electrification, Consumer demand for advanced features, OEM innovations)

3.1.1. Demand for In-car Connectivity

3.1.2. Integration of Infotainment Systems

3.1.3. Rise of Electric Vehicles (EVs)

3.1.4. Enhanced Interior Aesthetics and Comfort

3.2. Market Challenges (Cost constraints, Design complexities, Supply chain disruptions, Regional disparities)

3.2.1. High Production Costs

3.2.2. Limited Aftermarket Opportunities

3.2.3. Technological Standardization Issues

3.3. Opportunities (Growth in autonomous vehicles, Customization trends, Expansion in developing markets, Lightweight materials)

3.3.1. Opportunities in Electric and Hybrid Vehicles

3.3.2. Digital Interface Advancements

3.3.3. Expanding Autonomous Driving Integration

3.4. Trends (Customization and personalization, Smart center consoles, Materials innovation, Collaboration with tech companies)

3.4.1. Use of Sustainable Materials

3.4.2. Increased Integration of Wireless Charging

3.4.3. Gesture and Voice Control Adoption

3.5. Government Regulations (Safety standards, Environmental guidelines, Data protection regulations, Industry-specific policies)

3.5.1. Safety Compliance Regulations

3.5.2. Regulations for Interior Design Standards

3.5.3. Mandatory Data Privacy in Infotainment Systems

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Global Automotive Center Console Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Fixed Center Consoles

4.1.2. Adjustable Center Consoles

4.1.3. Modular Center Consoles

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Cars

4.2.2. Commercial Vehicles

4.2.3. Luxury Cars

4.3. By Material Type (In Value %)

4.3.1. Plastic

4.3.2. Metal

4.3.3. Leather and Fabric

4.4. By Technology (In Value %)

4.4.1. Integrated Infotainment

4.4.2. HVAC Integration

4.4.3. Wireless Charging

4.5. By Distribution Channel (In Value %)

4.5.1. OEMs

4.5.2. Aftermarket

4.6. By Region

4.6.1. Asia-Pacific

4.6.2. Europe

4.6.3. North America

4.6.4. Middle East & Africa

4.6.5. Latin America

5. Global Automotive Center Console Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Faurecia

5.1.2. Continental AG

5.1.3. Yanfeng Automotive Interiors

5.1.4. Toyota Boshoku Corporation

5.1.5. Magna International Inc.

5.1.6. Lear Corporation

5.1.7. Hyundai Mobis

5.1.8. Grupo Antolin

5.1.9. Johnson Controls

5.1.10. DURA Automotive Systems

5.1.11. Novem Car Interior Design

5.1.12. Nifco Inc.

5.1.13. Draxlmaier Group

5.1.14. Samvardhana Motherson Group

5.1.15. Brose Fahrzeugteile GmbH & Co. KG

5.2. Cross Comparison Parameters (Headquarters, Revenue, Employee Count, Product Portfolio, Market Share, Inception Year, R&D Investment, Global Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. Global Automotive Center Console Market Regulatory Framework

6.1. Interior Safety Standards

6.2. Environmental Impact Guidelines

6.3. Compliance with Emission Norms

6.4. Data Privacy and Cybersecurity Regulations

7. Global Automotive Center Console Market Future Market Size (In USD Bn)

7.1. Key Factors Driving Future Market Growth

8. Global Automotive Center Console Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Material Type (In Value %)

8.4. By Technology (In Value %)

8.5. By Distribution Channel (In Value %)

8.6. By Region (In Value %)

9. Global Automotive Center Console Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Product Positioning Strategies

9.3. White Space Opportunity Analysis

DisclaimerContact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the global automotive center console market ecosystem. This process leverages secondary research from trusted sources and proprietary databases to identify key market variables, such as product innovations, technological trends, and industry demand drivers.

Step 2: Market Analysis and Construction

In this phase, historical data analysis is conducted to assess market growth patterns, segment-wise revenue generation, and market penetration rates. The data is validated through financial performance insights from leading market players to ensure reliability.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about the market's future trajectory are formulated and validated via structured interviews with industry experts. These include senior executives from automotive OEMs, interior solution providers, and supply chain professionals.

Step 4: Research Synthesis and Final Output

In the final step, the gathered data is synthesized to create a comprehensive market report, combining both top-down and bottom-up approaches. This ensures that the analysis is exhaustive and provides accurate insights into the global automotive center console market.

Frequently Asked Questions

01. How big is the Global Automotive Center Console Market?

The global automotive center console market is valued at USD 36 billion, driven by increasing consumer demand for advanced in-car technologies and ergonomically designed interiors.

02. What are the challenges in the Global Automotive Center Console Market?

Challenges include rising production costs, technological standardization, and the complexities associated with design integration for smart and customizable consoles.

03. Who are the major players in the Global Automotive Center Console Market?

Key players include Faurecia, Continental AG, Yanfeng Automotive Interiors, Toyota Boshoku Corporation, and Magna International Inc.

04. What are the growth drivers of the Global Automotive Center Console Market?

Growth is driven by the shift toward electric vehicles, rising consumer demand for smart interiors, and the integration of infotainment systems within center consoles.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.