Global Automotive Powertrain Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2447

November 2024

99

About the Report

Global Automotive Powertrain Market Overview

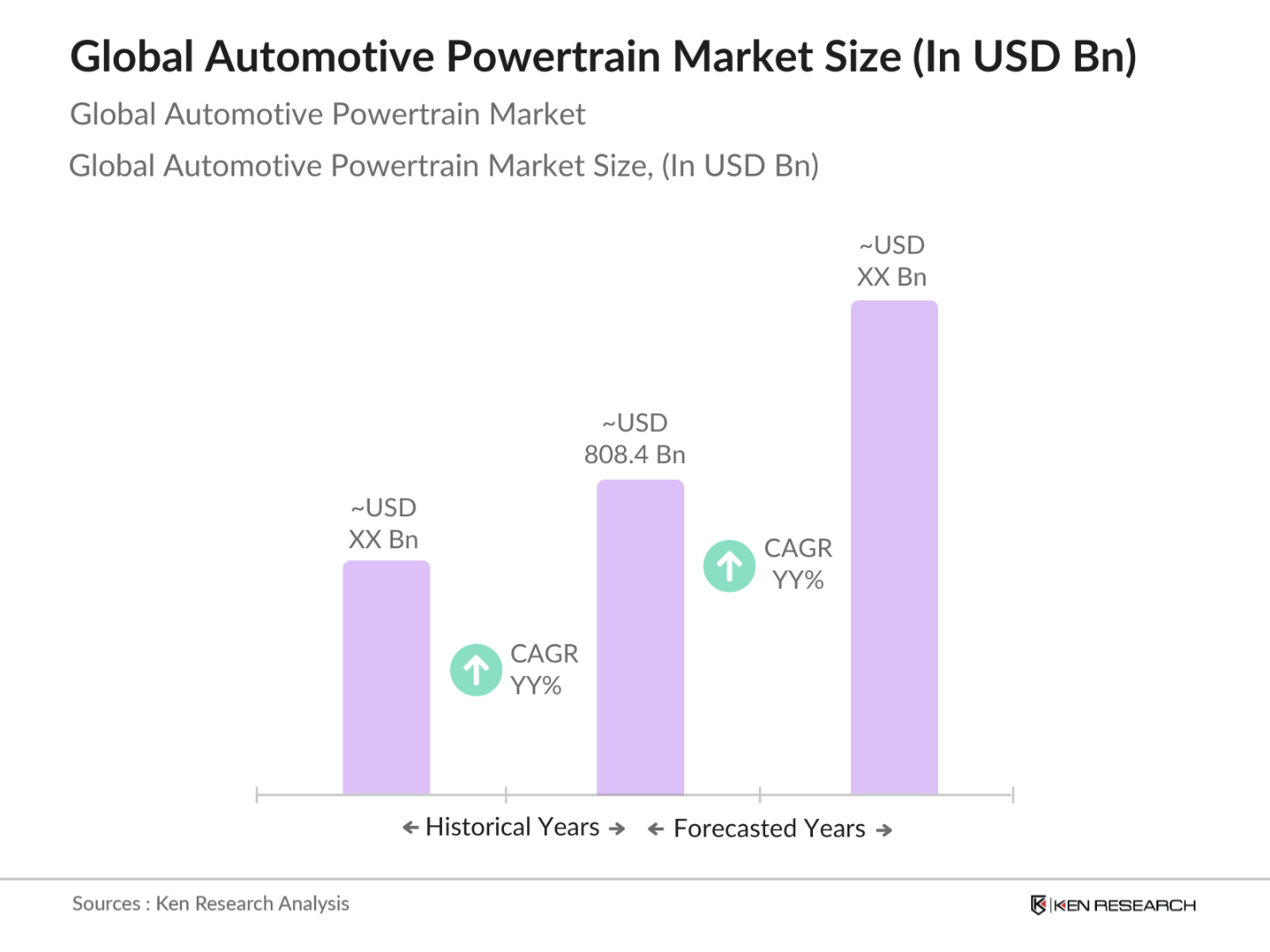

- The Global Automotive Powertrain Market is valued at USD 808.4 billion, based on a five-year historical analysis. This robust market size is driven by the increasing demand for fuel-efficient vehicles, technological advancements in powertrain systems, and the ongoing transition towards electrification. Key trends such as stringent emission regulations and rising consumer awareness about environmental sustainability also play a significant role in shaping market dynamics.

- Countries like the United States, Germany, and China dominate the automotive powertrain market due to their strong automotive manufacturing bases and investments in innovative technologies. The U.S. remains a leader with its substantial automotive industry and commitment to R&D, while Germany's reputation for engineering excellence ensures its position as a powerhouse in powertrain technology. China's growing electric vehicle market and supportive government policies further bolster its influence.

- Governments worldwide are establishing stringent emission standards to combat climate change and promote cleaner automotive technologies. In 2023, California implemented regulations requiring that a certain percentage of new passenger vehicles sold must be zero-emission vehicles. This regulation pushes manufacturers to develop electric and hybrid powertrains, as non-compliance could lead to significant penalties and restricted access to key markets. Such government actions are pivotal in shaping the automotive landscape, encouraging innovation, and ensuring that manufacturers align with environmental goals.

Global Automotive Powertrain Market Segmentation

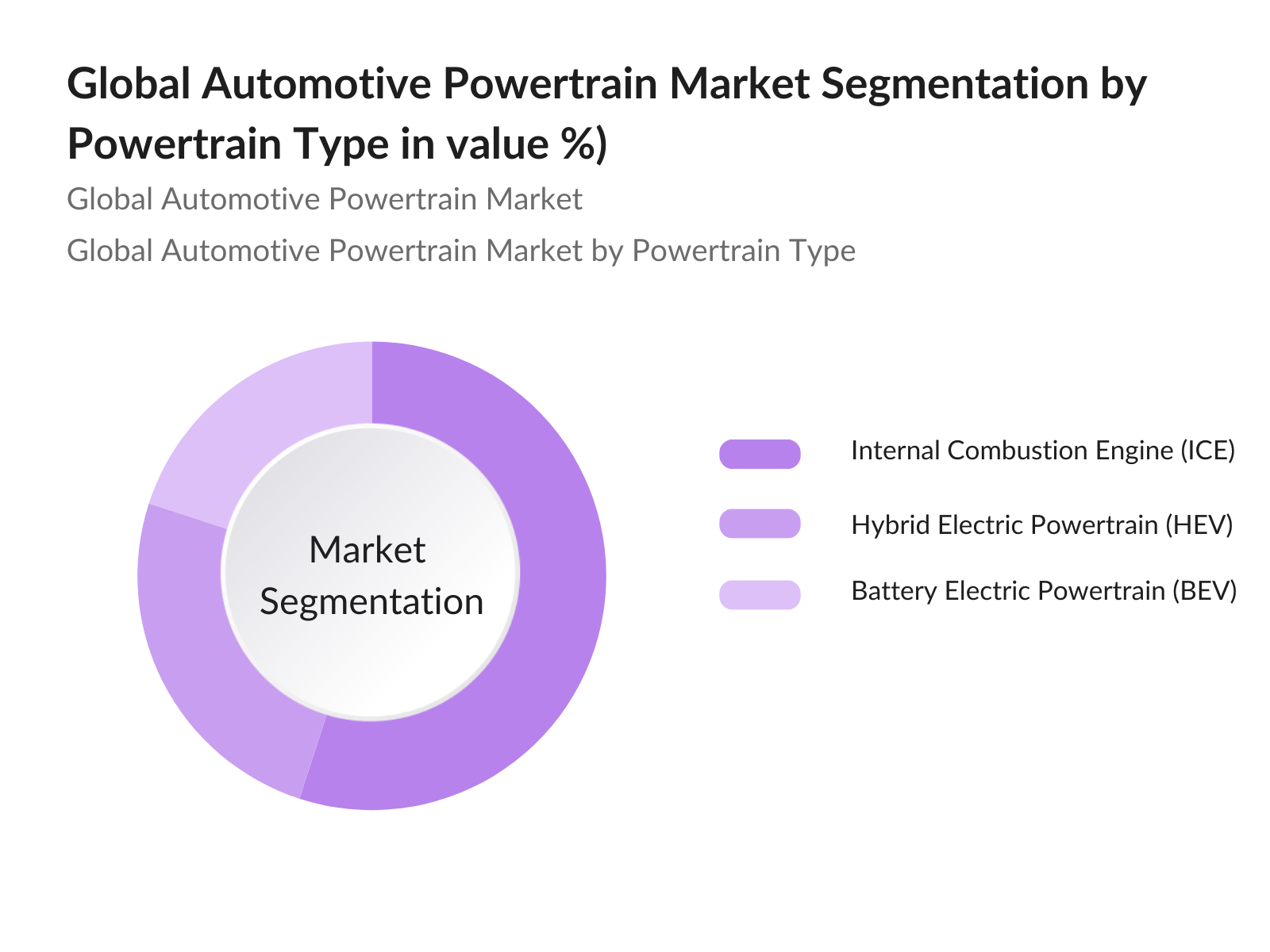

By Powertrain Type: The Global Automotive Powertrain Market is segmented by powertrain type into Internal Combustion Engine (ICE), Hybrid Electric Powertrain (HEV), and Battery Electric Powertrain (BEV). The Internal Combustion Engine segment holds a dominant share due to its longstanding presence and widespread use in vehicles worldwide. This segment benefits from the existing infrastructure, established manufacturing processes, and consumer familiarity, which contribute to its continued relevance despite the shift towards electrification.

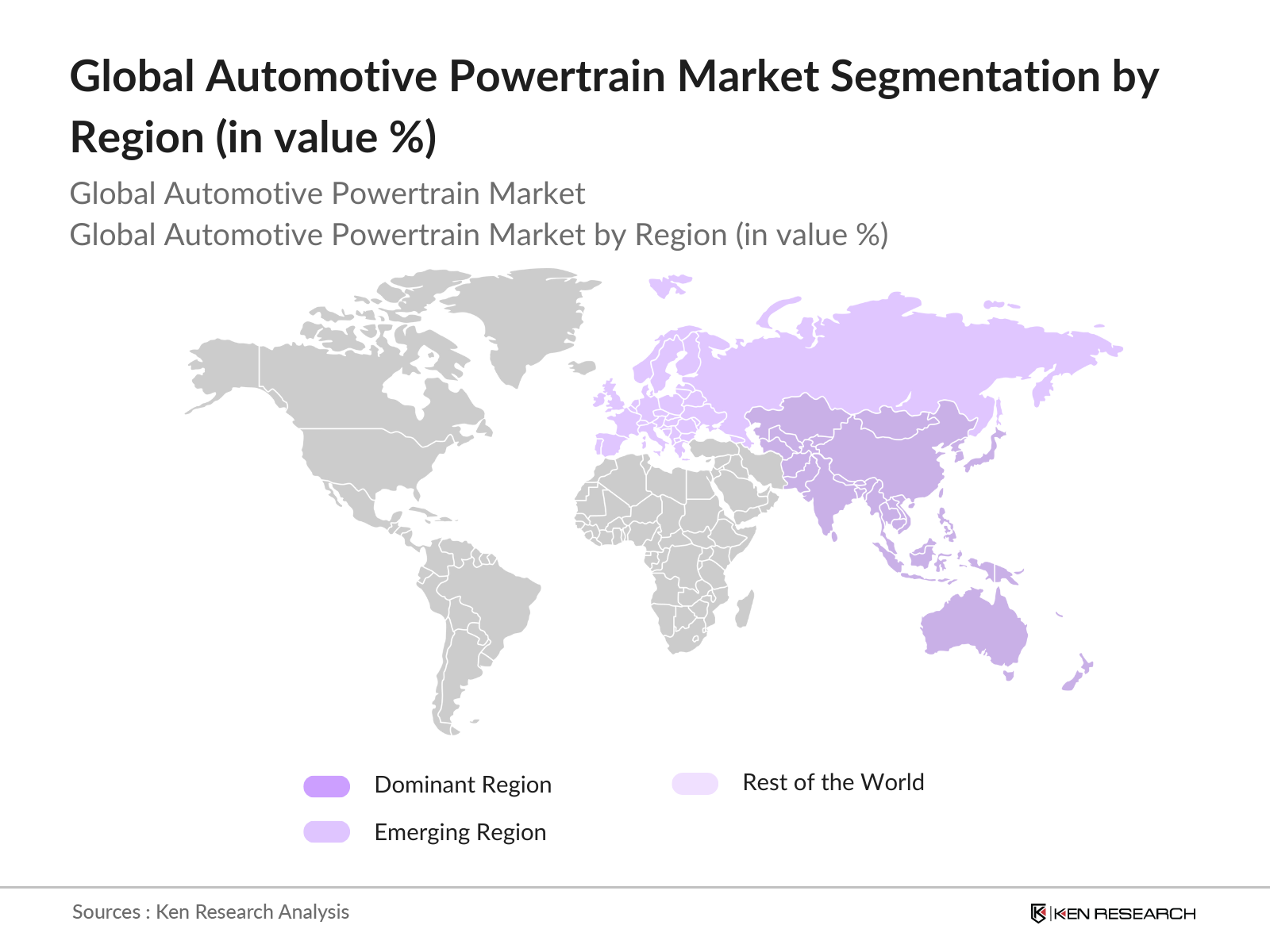

By Region: The Global Automotive Powertrain Market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The Asia-Pacific region holds a significant market share, driven by the high production and consumption of automobiles in countries like China and Japan. Rapid urbanization, growing disposable incomes, and increased investments in automotive manufacturing contribute to the dominance of this region.

Global Automotive Powertrain Market Competitive Landscape

The Global Automotive Powertrain Market is characterized by a few key players, including local manufacturers and global automotive giants. The competitive landscape is primarily influenced by these companies' technological innovations, strategic collaborations, and market expansion efforts.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

Market Share (%) |

Product Portfolio |

R&D Investment (USD Bn) |

Global Presence |

|

Bosch |

1886 |

Germany |

- |

- |

- |

- |

- |

|

Continental AG |

1871 |

Germany |

- |

- |

- |

- |

- |

|

General Motors |

1908 |

USA |

- |

- |

- |

- |

- |

|

Toyota Motor Corporation |

1937 |

Japan |

- |

- |

- |

- |

- |

|

Ford Motor Company |

1903 |

USA |

- |

- |

- |

- |

- |

Global Automotive Powertrain Market Analysis

Market Growth Drivers

- Shift towards Electrification: The automotive industry is witnessing a significant shift towards electrification, driven by global policy initiatives aimed at reducing carbon emissions. In 2023, electric vehicle (EV) sales reached 10 million units globally, with substantial increases in demand as governments incentivize EV adoption through subsidies and tax breaks. For instance, the European Union has committed to reducing greenhouse gas emissions by specific targets in the coming years, which necessitates an increased reliance on electric powertrains.

- Increasing Demand for Fuel Efficiency: As fuel prices fluctuate and environmental concerns escalate, there is a growing demand for vehicles that maximize fuel efficiency. In 2022, the average fuel consumption of new passenger cars in the EU was recorded at 5.6 liters per 100 kilometers, down from 7.2 liters. This trend is bolstered by stringent regulations requiring automakers to achieve a fleet-wide average CO2 emission target of 95 grams per kilometer by 2025. Consequently, innovations in powertrain technologies such as turbocharging and direct fuel injection are expected to enhance fuel efficiency in the coming years.

- Technological Innovations in Engine Design: Technological advancements in engine design are significantly enhancing the efficiency and performance of automotive powertrains. In 2023, manufacturers are investing heavily in advanced engine technologies, including variable valve timing and hybrid systems, with research indicating that modern engines can achieve up to a 20% increase in thermal efficiency. This shift is a response to both consumer demand for better performance and the need for compliance with emissions standards, leading to the development of more efficient and less polluting powertrains.

Market Challenges:

- High Development Costs: The transition to advanced automotive technologies often comes with high development costs, impacting profit margins for manufacturers. In 2023, it was reported that the average development cost for a new internal combustion engine was around $1.5 billion, while electric powertrains could reach upwards of $2.5 billion due to the complexity of battery systems and software integration. This financial burden is compounded by the rapid pace of technological change, requiring companies to continuously invest in R&D to remain competitive.

- Supply Chain Disruptions: Global supply chain disruptions, exacerbated by geopolitical tensions, continue to challenge the automotive industry. For instance, semiconductor shortages in 2023 resulted in a production loss of approximately 3.5 million vehicles worldwide. Manufacturers are increasingly faced with extended lead times and rising costs for essential components, which can delay product launches and hinder the ability to meet consumer demand. This scenario has highlighted the necessity for automotive companies to diversify their supply chains and invest in local sourcing strategies.

Global Automotive Powertrain Market Future Outlook

Over the next five years, the Global Automotive Powertrain Market is expected to show significant growth driven by continuous government support, advancements in powertrain technology, and increasing consumer demand for eco-friendly transportation solutions. The shift towards electrification and the integration of advanced technologies will reshape the competitive landscape, creating new opportunities for manufacturers. Companies that invest in R&D and innovative solutions will likely gain a competitive edge in this evolving market.

Market Opportunities:

- Shift towards Electrification: The automotive industry is witnessing a significant shift towards electrification, driven by global policy initiatives aimed at reducing carbon emissions. In 2023, electric vehicle (EV) sales reached 10 million units globally, with substantial increases in demand as governments incentivize EV adoption through subsidies and tax breaks. For instance, the European Union has committed to reducing greenhouse gas emissions by specific targets in the coming years, which necessitates an increased reliance on electric powertrains. This transition supports ongoing growth in electric vehicle production and infrastructure development, leading to further investments in technology and resources.

- Integration of AI and IoT in Powertrains: The integration of artificial intelligence (AI) and the Internet of Things (IoT) into automotive powertrains is a growing trend that enhances vehicle performance and efficiency. By 2023, the global market for AI in automotive applications is expected to exceed $2 billion, with many manufacturers utilizing AI for predictive maintenance and real-time performance monitoring. This integration allows for enhanced data analytics capabilities, enabling manufacturers to optimize powertrain operation and improve overall vehicle efficiency.

Scope of the Report

|

By Powertrain Type |

Internal Combustion Engine (ICE) Hybrid Electric Powertrain (HEV) Battery Electric Powertrain (BEV) |

|

By Component Type |

Engine Transmission Axles Driveline |

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Two-Wheelers |

|

By Fuel Type |

Gasoline Diesel Alternative Fuels |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Automotive Manufacturers

Component Suppliers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., U.S. Environmental Protection Agency, European Commission)

Automotive Technology Developers

Industry Analysts

Trade Associations

Automotive Research Organizations

Companies

Players Mention in the Report

Bosch

Continental AG

General Motors

Toyota Motor Corporation

Ford Motor Company

Honda Motor Co., Ltd.

Volkswagen AG

Hyundai Motor Company

Nissan Motor Corporation

Daimler AG

ZF Friedrichshafen AG

Tesla, Inc.

BMW AG

Aisin Seiki Co., Ltd.

Delphi Technologies

Table of Contents

01. Global Automotive Powertrain Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR)

1.4. Market Segmentation Overview

02. Global Automotive Powertrain Market Size (In USD MN)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. Global Automotive Powertrain Market Analysis

3.1. Growth Drivers

3.1.1. Shift towards Electrification

3.1.2. Increasing Demand for Fuel Efficiency

3.1.3. Stringent Emission Regulations

3.1.4. Technological Innovations in Engine Design

3.2. Market Challenges

3.2.1. High Development Costs

3.2.2. Supply Chain Disruptions

3.2.3. Competition from Electric Vehicles

3.3. Opportunities

3.3.1. Expansion in Emerging Markets

3.3.2. Collaboration with Tech Companies

3.3.3. Advances in Hybrid Technologies

3.4. Trends

3.4.1. Adoption of Advanced Materials

3.4.2. Integration of AI and IoT in Powertrains

3.4.3. Growth of Autonomous Vehicle Technologies

3.5. Government Regulation

3.5.1. Emission Standards and Compliance

3.5.2. Incentives for Electric Vehicle Adoption

3.5.3. Policy Framework for Sustainable Mobility

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

04. Global Automotive Powertrain Market Segmentation

4.1. By Powertrain Type (In Value %)

4.1.1. Internal Combustion Engine (ICE)

4.1.2. Hybrid Electric Powertrain (HEV)

4.1.3. Battery Electric Powertrain (BEV)

4.2. By Component Type (In Value %)

4.2.1. Engine

4.2.2. Transmission

4.2.3. Axles

4.2.4. Driveline

4.3. By Vehicle Type (In Value %)

4.3.1. Passenger Vehicles

4.3.2. Commercial Vehicles

4.3.3. Two-Wheelers

4.4. By Fuel Type (In Value %)

4.4.1. Gasoline

4.4.2. Diesel

4.4.3. Alternative Fuels

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. Global Automotive Powertrain Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Bosch

5.1.2. Continental AG

5.1.3. General Motors

5.1.4. Ford Motor Company

5.1.5. Toyota Motor Corporation

5.1.6. Honda Motor Co., Ltd.

5.1.7. Volkswagen AG

5.1.8. Daimler AG

5.1.9. ZF Friedrichshafen AG

5.1.10. Hyundai Motor Company

5.1.11. Tesla, Inc.

5.1.12. BMW AG

5.1.13. Nissan Motor Corporation

5.1.14. Aisin Seiki Co., Ltd.

5.1.15. Delphi Technologies

5.2 Cross Comparison Parameters (Revenue, R&D Investment, Market Share, Number of Employees, Headquarters, Inception Year, Product Portfolio, Global Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

06. Global Automotive Powertrain Market Regulatory Framework

6.1. Emission Standards

6.2. Safety Regulations

6.3. Compliance Requirements

07. Global Automotive Powertrain Future Market Size (In USD MN)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08. Global Automotive Powertrain Future Market Segmentation

8.1. By Powertrain Type (In Value %)

8.2. By Component Type (In Value %)

8.3. By Vehicle Type (In Value %)

8.4. By Fuel Type (In Value %)

8.5. By Region (In Value %)

09. Global Automotive Powertrain Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Global Automotive Powertrain Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the Global Automotive Powertrain Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATI) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple automotive manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Global Automotive Powertrain Market.

Frequently Asked Questions

01. How big is the Global Automotive Powertrain Market?

The Global Automotive Powertrain Market is valued at USD 808.4 billion, based on a five-year historical analysis, driven by the increasing demand for fuel-efficient vehicles and advancements in powertrain technology.

02. What are the challenges in the Global Automotive Powertrain Market?

Challenges include high development costs, competition from electric vehicles, and supply chain disruptions that can hinder growth and innovation within the market.

03. Who are the major players in the Global Automotive Powertrain Market?

Key players in the market include Bosch, Continental AG, General Motors, and Toyota Motor Corporation, known for their extensive product portfolios and strong market presence.

04. What are the growth drivers of the Global Automotive Powertrain Market?

The market is propelled by factors such as increasing demand for fuel efficiency, stringent emission regulations, and technological advancements that improve performance and sustainability.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.