Global Automotive Technology Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD11201

Region:Global

Author(s):Sanjna

Product Code:KROD11201

November 2024

84

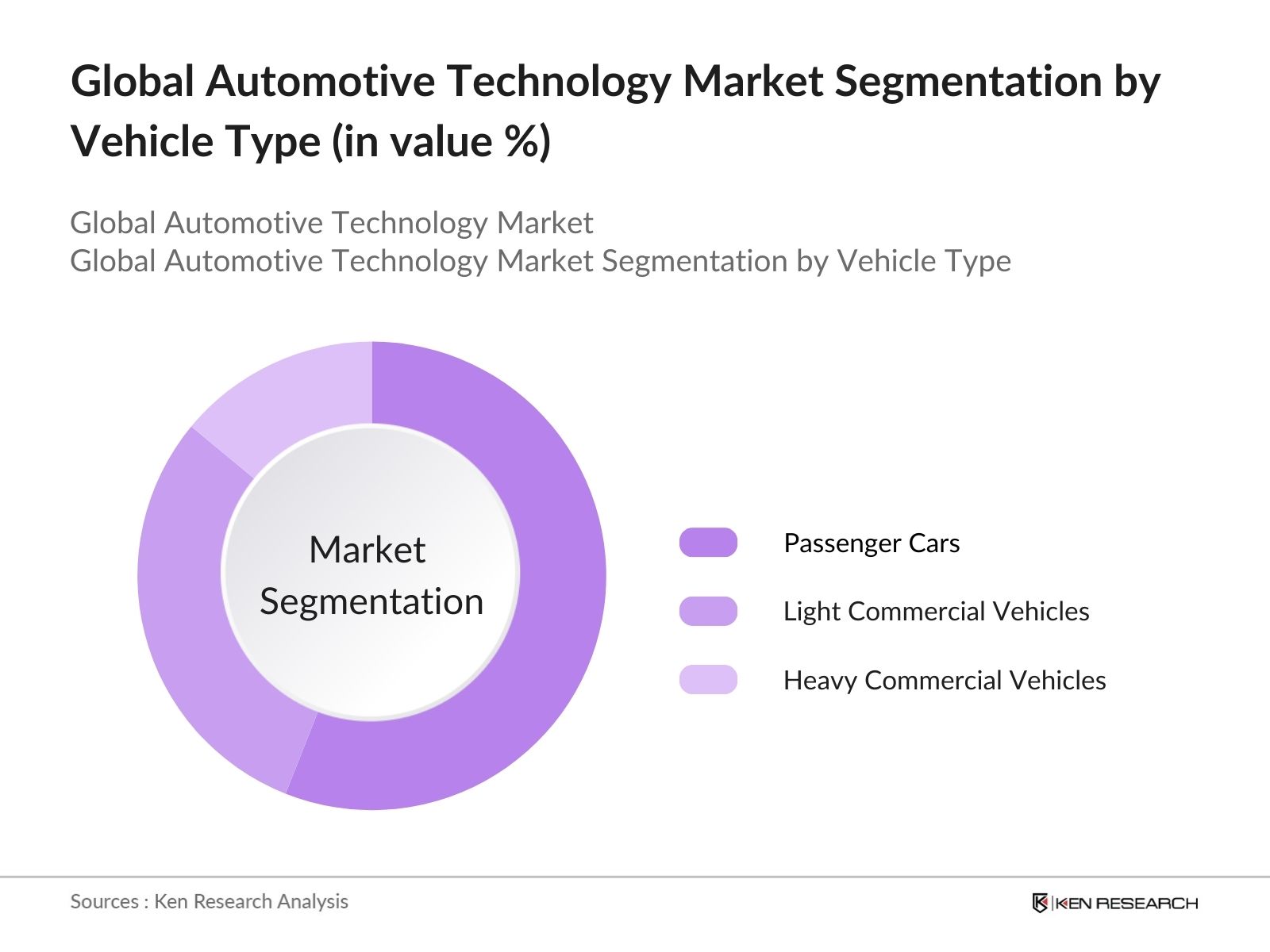

By Vehicle Type The global automotive technology market is segmented by vehicle type, including passenger cars, light commercial vehicles, and heavy commercial vehicles. Passenger cars hold a dominant market share in this segment due to the high consumer demand for comfort, convenience, and safety technologies integrated into personal vehicles. This segments strength is attributed to increased adoption of infotainment systems, ADAS, and vehicle electrification features tailored for passenger comfort and environmental sustainability.

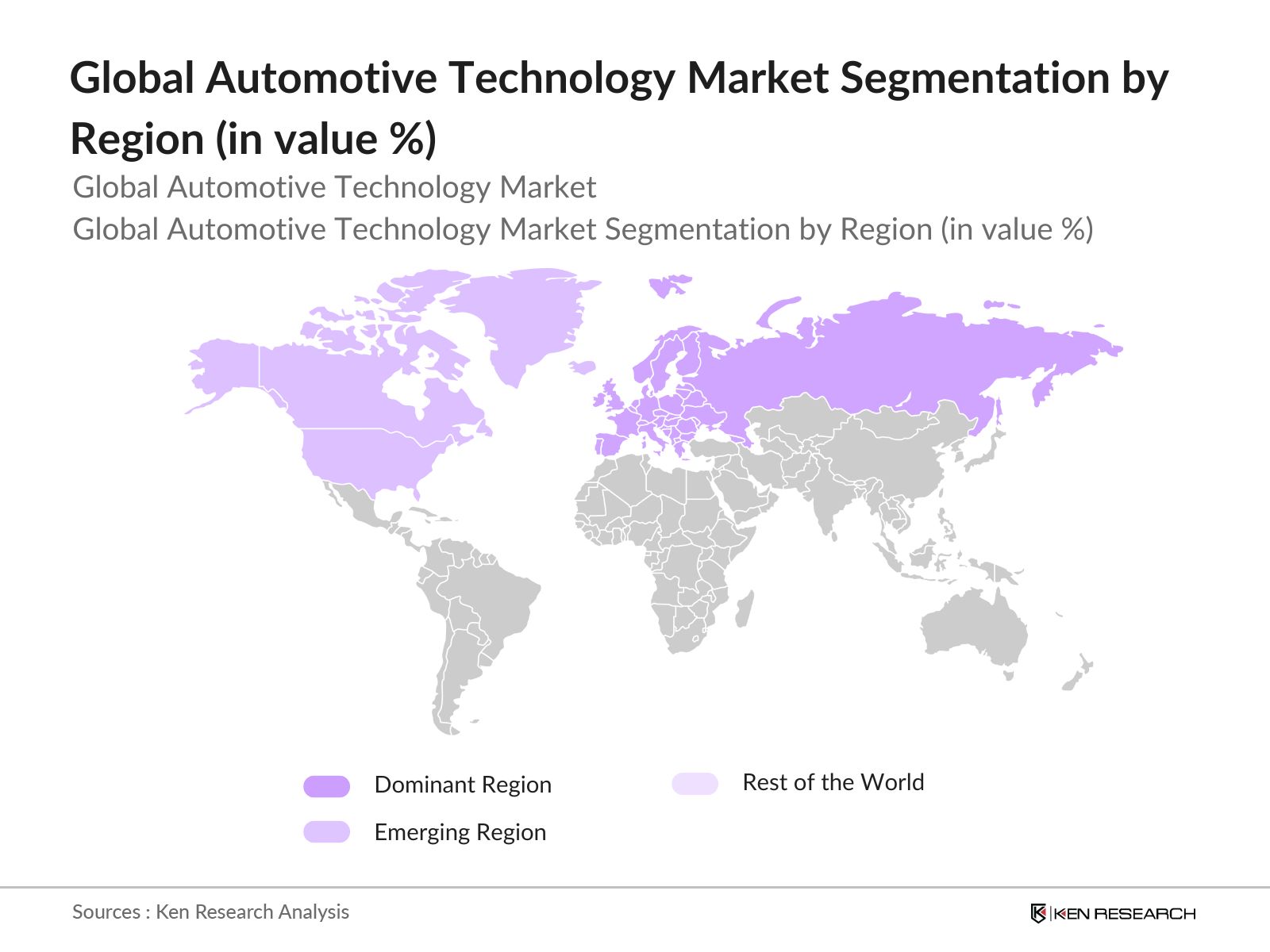

By Region The market is segmented regionally into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Europe leads in market share owing to regulatory pressure on emissions and carbon footprints, which has accelerated the adoption of EVs and advanced automotive technologies. The presence of strong automotive OEMs in the region, along with government incentives for green technology, reinforces Europes dominant position in automotive technology.

By Technology Type Automotive technology is segmented by technology type, including electrification, autonomous driving, connectivity, and ADAS. ADAS holds a significant share, with an estimated 40% dominance, driven by increasing safety regulations and consumer demand for features that enhance driver awareness and vehicle control. ADAS technologys integration is widespread in both passenger and commercial vehicles, propelled by governmental safety mandates and insurance benefits for vehicles equipped with advanced safety systems.

The global automotive technology market is dominated by a select group of players that leverage their expertise in technology integration and market presence. This concentration underscores the substantial impact and competitive strength of these industry leaders.

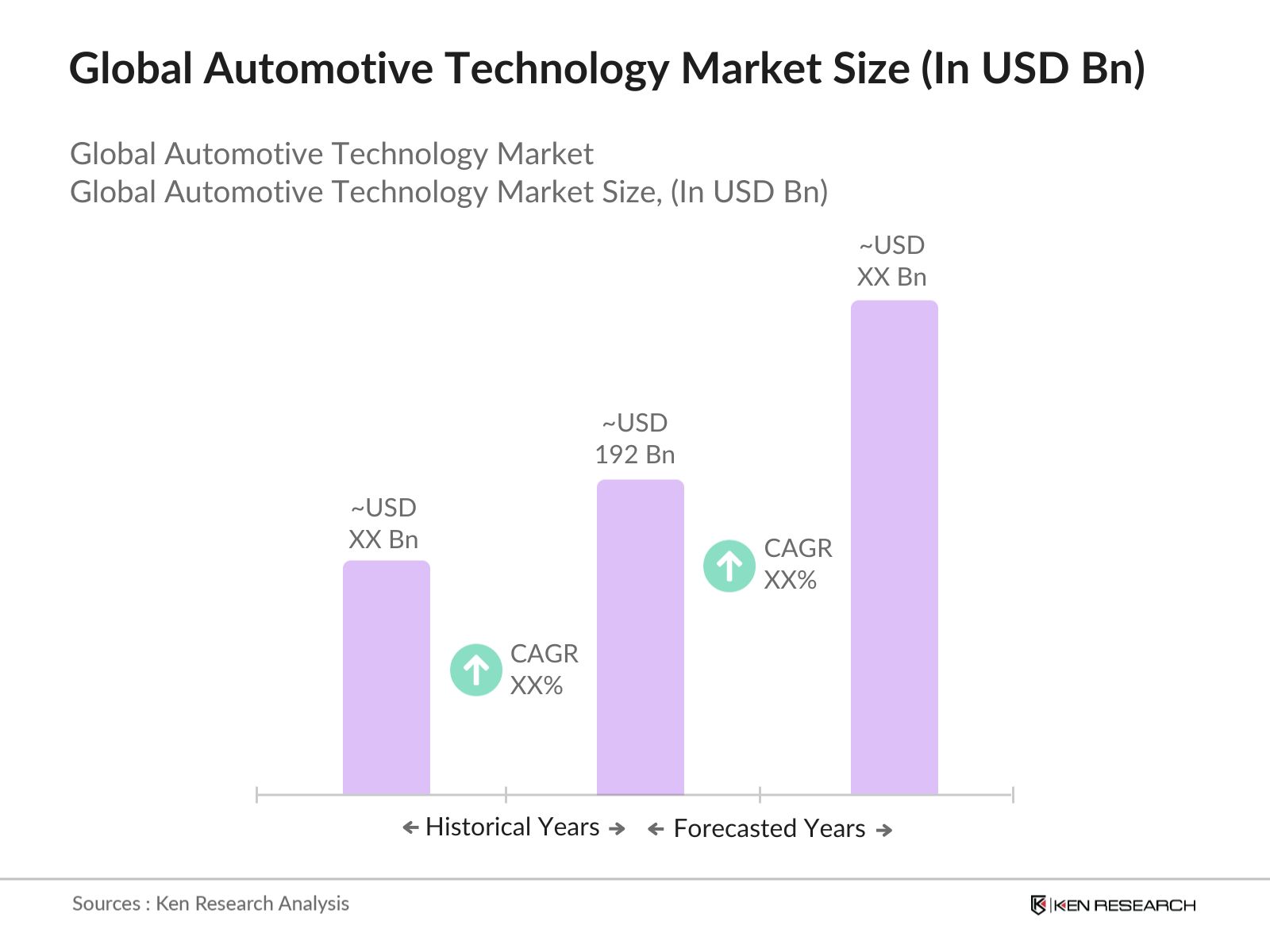

Global automotive technology market is expected to experience considerable growth due to advancements in electric and autonomous vehicles, evolving connectivity standards, and increased emphasis on sustainability. With governments worldwide providing incentives for green vehicle technology and stricter emissions regulations coming into play, the market will likely see accelerated investments in ADAS, EV charging infrastructure, and intelligent automotive solutions.

|

Segments |

Sub-Segments |

|

By Vehicle Type |

Passenger Cars |

|

Light Commercial Vehicles |

|

|

Heavy Commercial Vehicles |

|

|

By Technology Type |

Electrification |

|

Autonomous Driving |

|

|

Connectivity and IoT |

|

|

Advanced Driver Assistance Systems (ADAS) |

|

|

By Propulsion Type |

Internal Combustion Engine (ICE) |

|

Hybrid Electric Vehicle (HEV) |

|

|

Battery Electric Vehicle (BEV) |

|

|

Fuel Cell Electric Vehicle (FCEV) |

|

|

By Component Type |

Hardware |

|

Software |

|

|

Services |

|

|

By Region |

North America |

|

Europe |

|

|

Asia Pacific |

|

|

Latin America |

|

|

Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Summary

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Connected Vehicles

3.1.2. Increase in Electrification Trends

3.1.3. Regulatory Emissions Standards

3.1.4. Demand for Advanced Driver Assistance Systems (ADAS)

3.2. Market Challenges

3.2.1. High Cost of Technology Integration

3.2.2. Global Chip Shortage Impact

3.2.3. Skills Gap in Technology Deployment

3.3. Opportunities

3.3.1. Growth in Autonomous Vehicles

3.3.2. Software as a Service (SaaS) in Automotive

3.3.3. Infrastructure Advancements for Electric Vehicles (EVs)

3.4. Trends

3.4.1. Rise of Software-Defined Vehicles (SDVs)

3.4.2. Digitalization of Supply Chains

3.4.3. Integration of Augmented Reality in Automotive Design

3.5. Regulatory Landscape

3.5.1. Emission and Safety Standards Compliance

3.5.2. Environmental Impact Regulations

3.5.3. Automotive Data Privacy Regulations

3.6. Competitive Landscape Overview

3.6.1. Market Penetration Strategies

3.6.2. Regional and Segment-Wise Presence

3.7. Porters Five Forces Analysis

3.8. Stakeholder Ecosystem Mapping

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Light Commercial Vehicles

4.1.3. Heavy Commercial Vehicles

4.2. By Technology Type (In Value %)

4.2.1. Electrification

4.2.2. Autonomous Driving

4.2.3. Connectivity and IoT

4.2.4. Advanced Driver Assistance Systems (ADAS)

4.3. By Propulsion Type (In Value %)

4.3.1. Internal Combustion Engine (ICE)

4.3.2. Hybrid Electric Vehicle (HEV)

4.3.3. Battery Electric Vehicle (BEV)

4.3.4. Fuel Cell Electric Vehicle (FCEV)

4.4. By Component Type (In Value %)

4.4.1. Hardware

4.4.2. Software

4.4.3. Services

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Robert Bosch GmbH

5.1.2. Continental AG

5.1.3. Denso Corporation

5.1.4. Aptiv PLC

5.1.5. Valeo

5.1.6. Magna International Inc.

5.1.7. ZF Friedrichshafen AG

5.1.8. NXP Semiconductors

5.1.9. Infineon Technologies AG

5.1.10. NVIDIA Corporation

5.2. Cross-Comparison Parameters (Revenue, Technological Capabilities, Product Diversification, Geographic Reach, Research & Development Focus, Sustainability Goals, Strategic Partnerships, Employee Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives and Developments

5.5. Mergers, Acquisitions, and Partnerships

5.6. Investment and Funding Landscape

5.7. Innovation and Patents Analysis

6.1. Emission Standards

6.2. Safety Compliance Requirements

6.3. Data Privacy and Security Protocols

7.1. Market Forecast Projections

7.2. Factors Influencing Future Market Growth

8.1. TAM/SAM/SOM Analysis

8.2. Customer Acquisition and Retention Strategies

8.3. White Space Opportunity Identification

8.4. Market Expansion Strategies

The initial phase involves constructing an ecosystem map encompassing all stakeholders in the global automotive technology market. Extensive desk research is utilized to gather data from proprietary and secondary databases, identifying critical variables that influence the market.

This step includes compiling and analyzing historical data, assessing market penetration, and evaluating industry revenue statistics. Insights are gathered on service providers and technology adoption to validate the market structure.

Market hypotheses are formulated and validated through expert interviews with representatives across the automotive value chain. These consultations provide operational insights and financial data, enriching the market analysis.

The final step involves engaging directly with automotive technology providers to refine and verify the analysis. This synthesis ensures a comprehensive, accurate, and validated assessment of the global automotive technology market.

The global automotive technology market was valued at USD 192 billion, propelled by advanced integration of connected technologies, electrification, and consumer demand for enhanced safety features.

Challenges in global automotive technology market include managing high technology costs, addressing regulatory compliance, and overcoming supply chain disruptions, such as semiconductor shortages and logistics issues.

Key players in global automotive technology market include Robert Bosch GmbH, Continental AG, Denso Corporation, Aptiv PLC, and Magna International Inc., renowned for their technological expertise and global reach.

Growth in global automotive technology market is driven by rising consumer demand for safety, regulatory mandates on emissions, and increasing investment in electrification and autonomous driving technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.