Global Autonomous Bus Market Outlook to 2030

Region:Global

Author(s):Vijay Kumar

Product Code:KROD2274

Region:Global

Author(s):Vijay Kumar

Product Code:KROD2274

December 2024

82

Listen to the audio summary

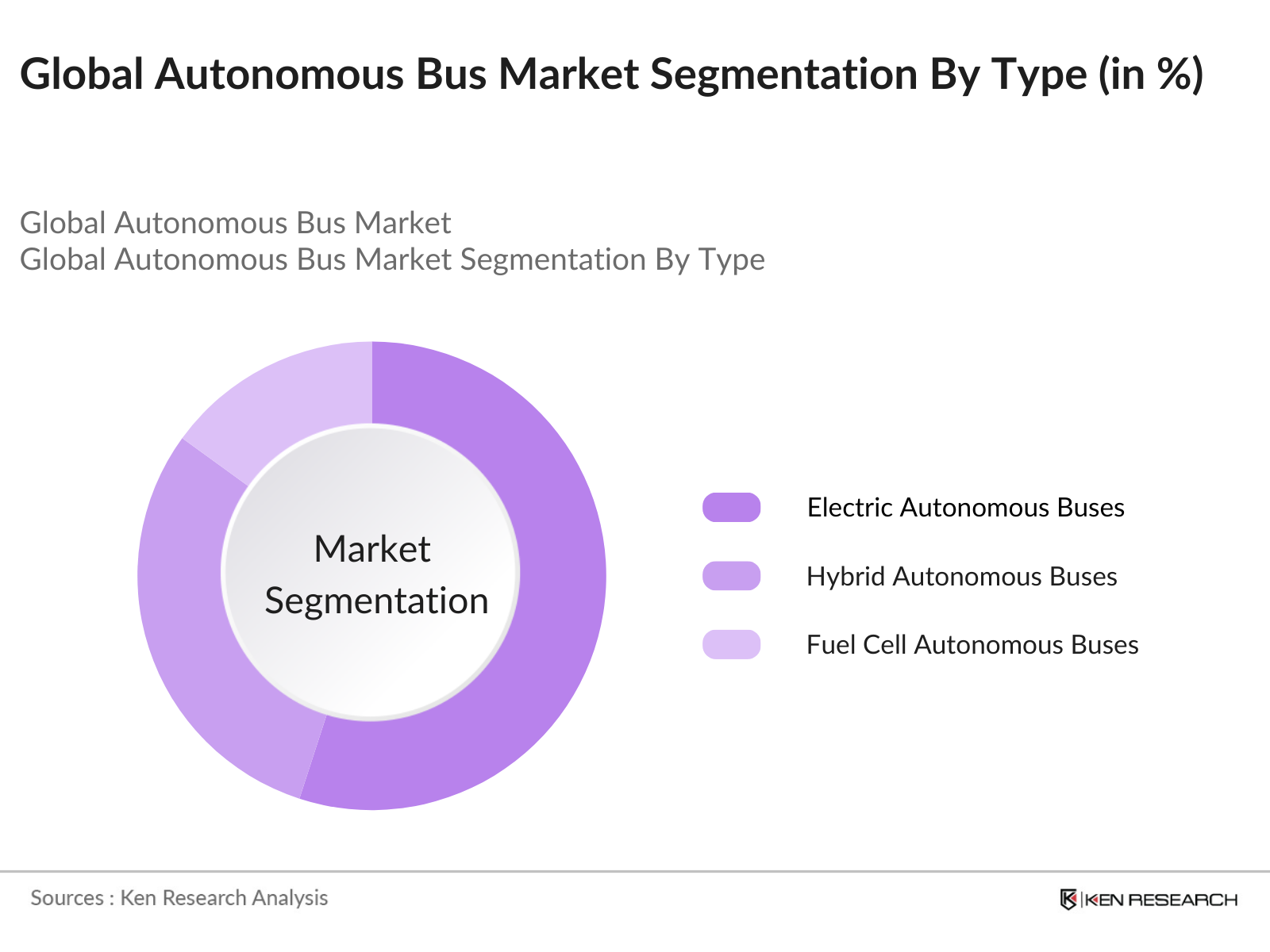

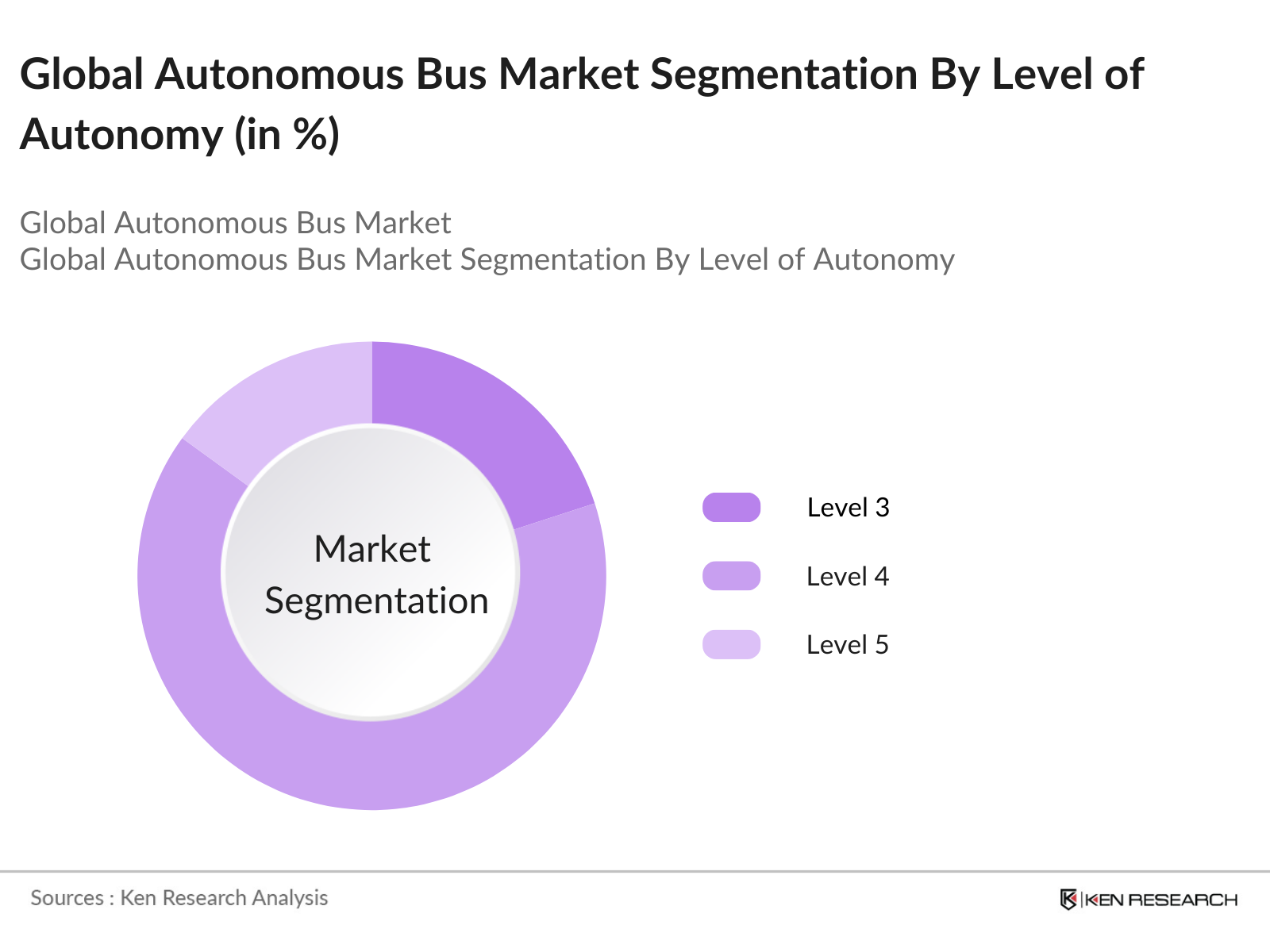

The Global Autonomous Bus Market can be segmented based on Type, Level of Autonomy, and Region.

By Type: The market is segmented by type into electric autonomous buses, hybrid autonomous buses, and fuel cell autonomous buses. In 2023, electric autonomous buses held the dominant market share due to their ability to reduce operational costs and contribute to sustainability. The increasing number of government subsidies promoting electric public transport and the rising environmental consciousness among consumers have reinforced the dominance of this segment.

By Level of Autonomy: The market is further segmented by level of autonomy into Level 3, Level 4, and Level 5. Level 4 autonomous buses dominated the market in 2023, as they are widely deployed in various pilot projects in cities across North America, Europe, and Asia. The ability to operate independently in most driving scenarios makes Level 4 buses ideal for urban public transport.

By Region: Geographically, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and MEA. Asia-Pacific led the market in 2023, driven by strong government initiatives and heavy investments in smart city infrastructure. Chinas focus on developing autonomous vehicle technology, along with Japans push for driverless public transportation, has made the region a global leader in this segment.

|

Company Name |

Headquarters |

Establishment Year |

|

EasyMile |

Toulouse, France |

2014 |

|

Navya |

Villeurbanne, France |

2014 |

|

Volvo |

Gothenburg, Sweden |

1927 |

|

Scania |

Sdertlje, Sweden |

1911 |

|

Daimler |

Stuttgart, Germany |

1926 |

The Global Autonomous Bus Market is poised for significant growth, driven by advancements in AI technology, the increasing focus on smart cities, and growing government support for sustainable transportation systems.

|

By Type |

Rotary Desiccant Dehumidifiers Portable Desiccant Dehumidifiers Stationary Desiccant Dehumidifiers |

|

By End-User |

Electric Autonomous Buses Hybrid Autonomous Buses Fuel Cell Autonomous Buses |

|

By Region |

North America Europe APAC Latin America MEA |

|

By Level of Autonomy |

Level 3 Level 4 Level 5 |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Urbanization and Traffic Congestion

3.1.2. Technological Advancements in AI and Sensor Technologies

3.1.3. Government Initiatives and Funding

3.1.4. Environmental Concerns and Emission Regulations

3.2. Market Challenges

3.2.1. High Development and Maintenance Costs

3.2.2. Regulatory and Legal Hurdles

3.2.3. Public Acceptance and Trust Issues

3.3. Opportunities

3.3.1. Expansion into Emerging Markets

3.3.2. Integration with Smart City Projects

3.3.3. Partnerships and Collaborations

3.4. Trends

3.4.1. Adoption of Electric and Hybrid Propulsion Systems

3.4.2. Deployment of Level 4 and Level 5 Autonomous Buses

3.4.3. Use of Advanced Driver Assistance Systems (ADAS)

3.5. Government Regulations

3.5.1. Autonomous Vehicle Testing Policies

3.5.2. Safety Standards and Compliance

3.5.3. Incentives for Electric and Autonomous Vehicles

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter's Five Forces Analysis

3.9. Competitive Landscape

4.1. By Level of Autonomy (in Value %)

4.1.1. Level 1

4.1.2. Level 2

4.1.3. Level 3

4.1.4. Level 4

4.1.5. Level 5

4.2. By Propulsion Type (in Value %)

4.2.1. Diesel

4.2.2. Electric

4.2.3. Hybrid

4.3. By Application (in Value %)

4.3.1. Intercity

4.3.2. Intracity

4.3.3. Shuttle Services

4.4. By Sensor Type (in Value %)

4.4.1. Lidar

4.4.2. Radar

4.4.3. Camera

4.4.4. Ultrasonic

4.5. By Region (in Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. AB Volvo

5.1.2. Zhengzhou Yutong Bus Co. Ltd.

5.1.3. Navya

5.1.4. Daimler AG

5.1.5. Xiamen King Long United Automotive Industry Co. Ltd.

5.1.6. EasyMile

5.1.7. Volkswagen AG

5.1.8. Toyota Motor Corporation

5.1.9. Tesla Inc.

5.1.10. Proterra Inc.

5.1.11. Local Motors

5.1.12. Waymo LLC

5.1.13. Baidu Inc.

5.1.14. Hyundai Motor Company

5.1.15. NFI Group Inc.

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Market Share, R&D Expenditure, Product Portfolio, Regional Presence)

5.3. Strategic Initiatives

5.4. Mergers and Acquisitions

5.5. Investment Analysis

5.5.1. Venture Capital Funding

5.5.2. Government Grants

5.5.3. Private Equity Investments

6.1. Autonomous Vehicle Legislation

6.2. Safety and Emission Standards

6.3. Data Privacy and Cybersecurity Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Level of Autonomy (in Value %)

8.2. By Propulsion Type (in Value %)

8.3. By Application (in Value %)

8.4. By Sensor Type (in Value %)

8.5. By Region (in Value %)

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Creating an ecosystem for all major entities within the Global Autonomous Bus Market and referencing a combination of secondary and proprietary databases to conduct desk research. This step includes gathering industry-level information, identifying market trends, regulatory frameworks, and understanding the competitive landscape to ensure a thorough analysis.

Compiling data on the Global Autonomous Bus Market over the years, including market penetration across various segments, and evaluating the performance of key market players. This involves analyzing production capacities, market shares, and sales data to compute the total revenue generated within the market. Ensuring accuracy by conducting multiple quality checks of the data points is also part of this process.

Developing market hypotheses and conducting interviews via Computer Assisted Telephone Interviews (CATIs) with industry experts and key stakeholders from prominent autonomous bus companies. These interviews help validate the collected data, refine market forecasts, and gather critical operational and financial insights directly from industry leaders.

Collaborating with key players in the autonomous bus industry to understand the dynamics of product segments, evolving customer needs, sales trends, and market challenges. A bottom-up approach is utilized to ensure the final data reflects current market conditions accurately and supports effective strategic decision-making.

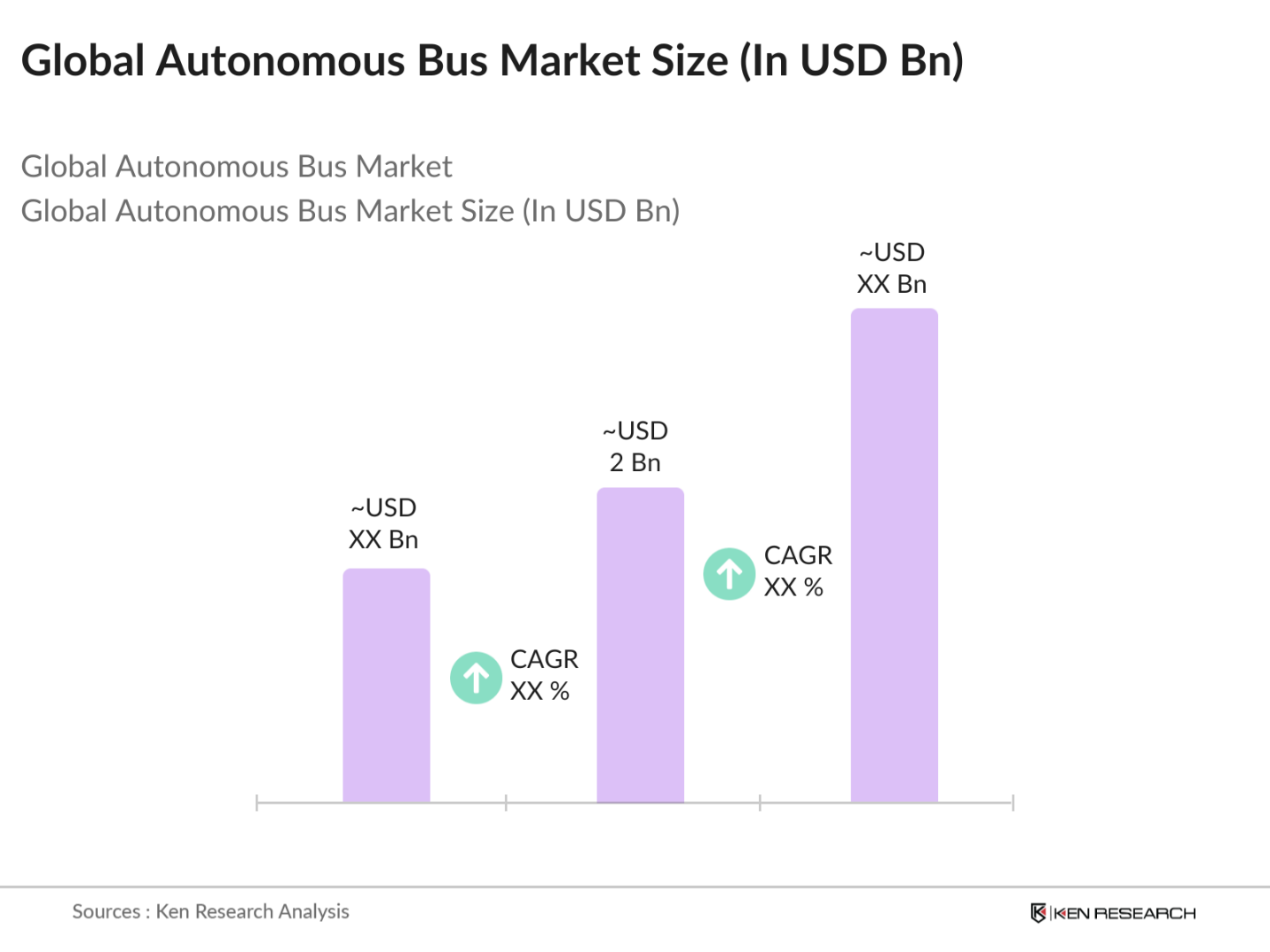

The global autonomous bus market reached a valuation of USD 2 billion in 2023, driven by the rapid adoption of AI-based technologies in public transportation and the growing demand for sustainable urban mobility.

Challenges in the global autonomous bus market include regulatory hurdles, high initial investment costs for autonomous technology, and public hesitation regarding the safety of autonomous vehicles. The lack of unified safety standards also delays large-scale deployment.

Key players in the global autonomous bus market include EasyMile, Navya, Volvo, Scania, and Daimler. These companies are leading the market through technological innovations, partnerships with governments, and extensive R&D efforts in autonomous driving technology.

The market is propelled by increased investments in smart city infrastructure, rising demand for electric vehicles, and public-private partnerships aimed at enhancing autonomous vehicle adoption. Government initiatives to reduce urban congestion also contribute to the markets expansion.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.