Global Baby Food Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD6039

Region:Global

Author(s):Mukul

Product Code:KROD6039

November 2024

80

The Global Baby Food market is characterized by a mix of multinational corporations and local companies, with key players focusing on innovation, product diversification, and geographic expansion. The competition is intense, especially in the milk formula and organic baby food segments. Major companies such as Nestl, Abbott, and Danone dominate the market, leveraging their global presence and well-established supply chains to capture significant market share.

|

Company |

Year Established |

Headquarters |

Product Range |

Number of Employees |

Revenue (USD Bn) |

Distribution Channels |

Organic Product Offerings |

Innovation Initiatives |

Sustainability Efforts |

|

Nestl S.A. |

1867 |

Switzerland |

- |

- |

- |

- |

- |

- |

- |

|

Abbott Laboratories |

1888 |

USA |

- |

- |

- |

- |

- |

- |

- |

|

Danone S.A. |

1919 |

France |

- |

- |

- |

- |

- |

- |

- |

|

Reckitt Benckiser Group |

1823 |

UK |

- |

- |

- |

- |

- |

- |

- |

|

The Kraft Heinz Company |

2015 |

USA |

- |

- |

- |

- |

- |

- |

- |

Over the next five years, the Global Baby Food market is expected to experience steady growth, driven by increasing consumer demand for organic, clean-label, and nutrient-dense products. The market will be supported by advancements in product development, such as plant-based baby foods and customized nutrition solutions, as well as expanding e-commerce channels. Moreover, government initiatives promoting child health and nutrition are anticipated to further propel market growth.

|

By Product Type |

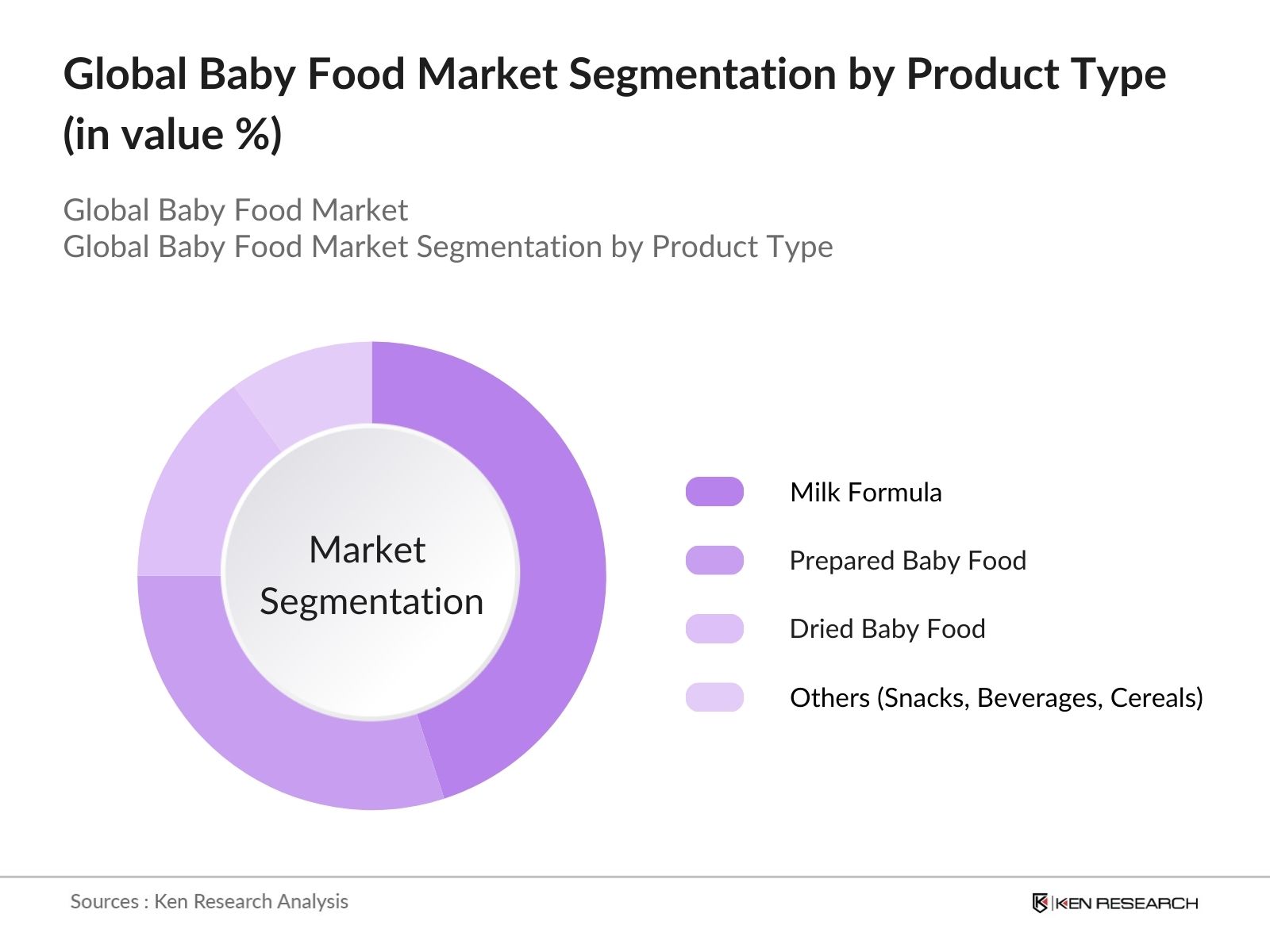

Milk Formula Prepared Baby Food Dried Baby Food Others (Snacks, Beverages, Cereals) |

|

By Age Group |

0-6 Months 6-12 Months 12-24 Months Above 24 Months |

|

By Distribution Channel |

Supermarkets and Hypermarkets Pharmacies and Drug Stores Online Channels Specialty Stores |

|

By Nature |

Organic Baby Food Non-Organic Baby Food |

|

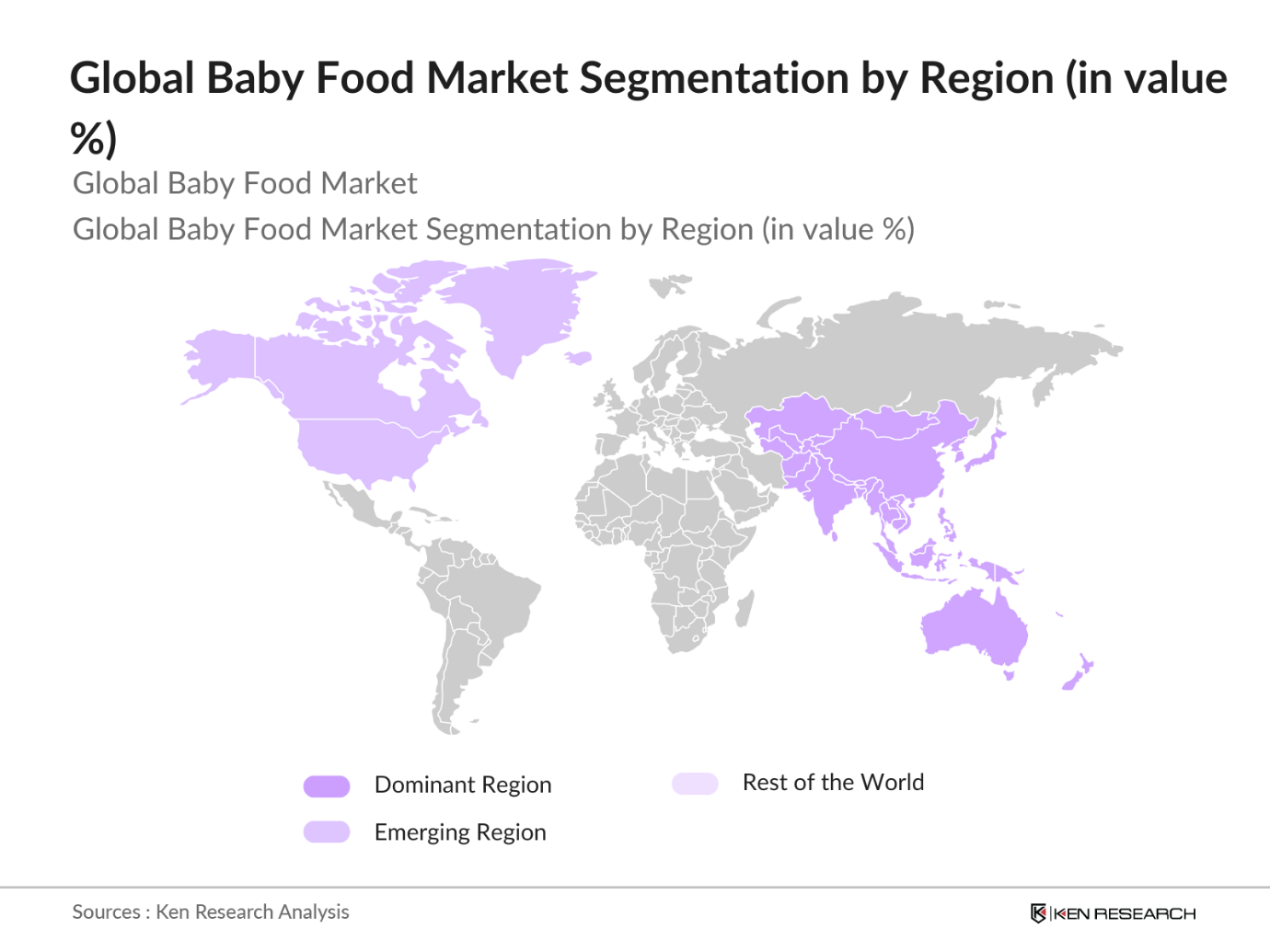

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Birth Rates (Global Birth Rate Statistics)

3.1.2. Rising Parental Concerns for Infant Nutrition (Parental Buying Trends, Nutritional Awareness)

3.1.3. Urbanization and Lifestyle Changes (Urban vs Rural Baby Food Consumption)

3.1.4. Growth of E-commerce and Online Distribution (E-commerce Sales Metrics for Baby Food)

3.2. Market Challenges

3.2.1. High Production and R&D Costs (Cost Analysis of Baby Food Manufacturing)

3.2.2. Regulatory Compliance (Global and Regional Baby Food Regulations)

3.2.3. Competition from Homemade Food Solutions (Home-Based Food Trends for Infants)

3.3. Opportunities

3.3.1. Expansion into Emerging Markets (Baby Food Demand in Emerging Economies)

3.3.2. Technological Advancements in Product Formulation (Innovations in Baby Food Production)

3.3.3. Growing Focus on Organic and Clean Label Products (Growth in Organic Baby Food Segment)

3.4. Trends

3.4.1. Increasing Demand for Plant-Based Baby Food (Growth Rate of Plant-Based Baby Foods)

3.4.2. Customization and Personalized Baby Nutrition (Consumer Demand for Custom Baby Foods)

3.4.3. Packaging Innovations (Sustainability in Baby Food Packaging Solutions)

3.5. Regulatory Landscape

3.5.1. FDA Regulations for Infant Formula and Baby Food (US Baby Food Safety Guidelines)

3.5.2. European Unions Baby Food Compliance Standards (EU Regulations and Safety Protocols)

3.5.3. Global Certifications for Organic and Non-GMO Baby Food (Certification Protocols in Baby Food Industry)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Milk Formula

4.1.2. Prepared Baby Food

4.1.3. Dried Baby Food

4.1.4. Others (Snacks, Beverages, Cereals)

4.2. By Age Group (In Value %)

4.2.1. 0-6 Months

4.2.2. 6-12 Months

4.2.3. 12-24 Months

4.2.4. Above 24 Months

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets and Hypermarkets

4.3.2. Pharmacies and Drug Stores

4.3.3. Online Channels

4.3.4. Specialty Stores

4.4. By Nature (In Value %)

4.4.1. Organic Baby Food

4.4.2. Non-Organic Baby Food

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Nestl S.A.

5.1.2. Abbott Laboratories

5.1.3. Danone S.A.

5.1.4. Reckitt Benckiser Group Plc

5.1.5. The Kraft Heinz Company

5.1.6. Perrigo Company Plc

5.1.7. Hero Group

5.1.8. Campbell Soup Company

5.1.9. FrieslandCampina

5.1.10. Mead Johnson & Company, LLC

5.1.11. Bellamys Organic Pty Ltd

5.1.12. Hain Celestial Group

5.1.13. Arla Foods Amba

5.1.14. Ellas Kitchen Group Ltd

5.1.15. Hipp GmbH & Co. Vertrieb KG

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Distribution Channels, Product Diversification, Sustainability Efforts, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Nutritional Standards and Labeling Requirements

6.2. Compliance with Global Food Safety Regulations

6.3. Organic Certification and Non-GMO Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Age Group (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Nature (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

This phase involves creating a comprehensive overview of the Global Baby Food Market ecosystem, covering key stakeholders such as manufacturers, retailers, and regulatory bodies. Secondary research is conducted using proprietary databases and credible industry reports to identify market trends, growth drivers, and key variables.

Historical data related to market size, product segmentation, and geographical expansion is analyzed to assess market penetration. Revenue generation data is also compiled to ensure accuracy, and insights into production and distribution channels are gathered to evaluate market structure.

In this stage, market hypotheses are formulated and validated through consultations with industry experts and key players. This is achieved via computer-assisted telephone interviews (CATIs), providing firsthand insights into market trends and competitive strategies.

This final step involves synthesizing data collected from various stakeholders to develop a well-rounded market analysis. This includes detailed insights into consumer behavior, market dynamics, and future projections. Validation is ensured through cross-referencing with industry standards and expert opinions.

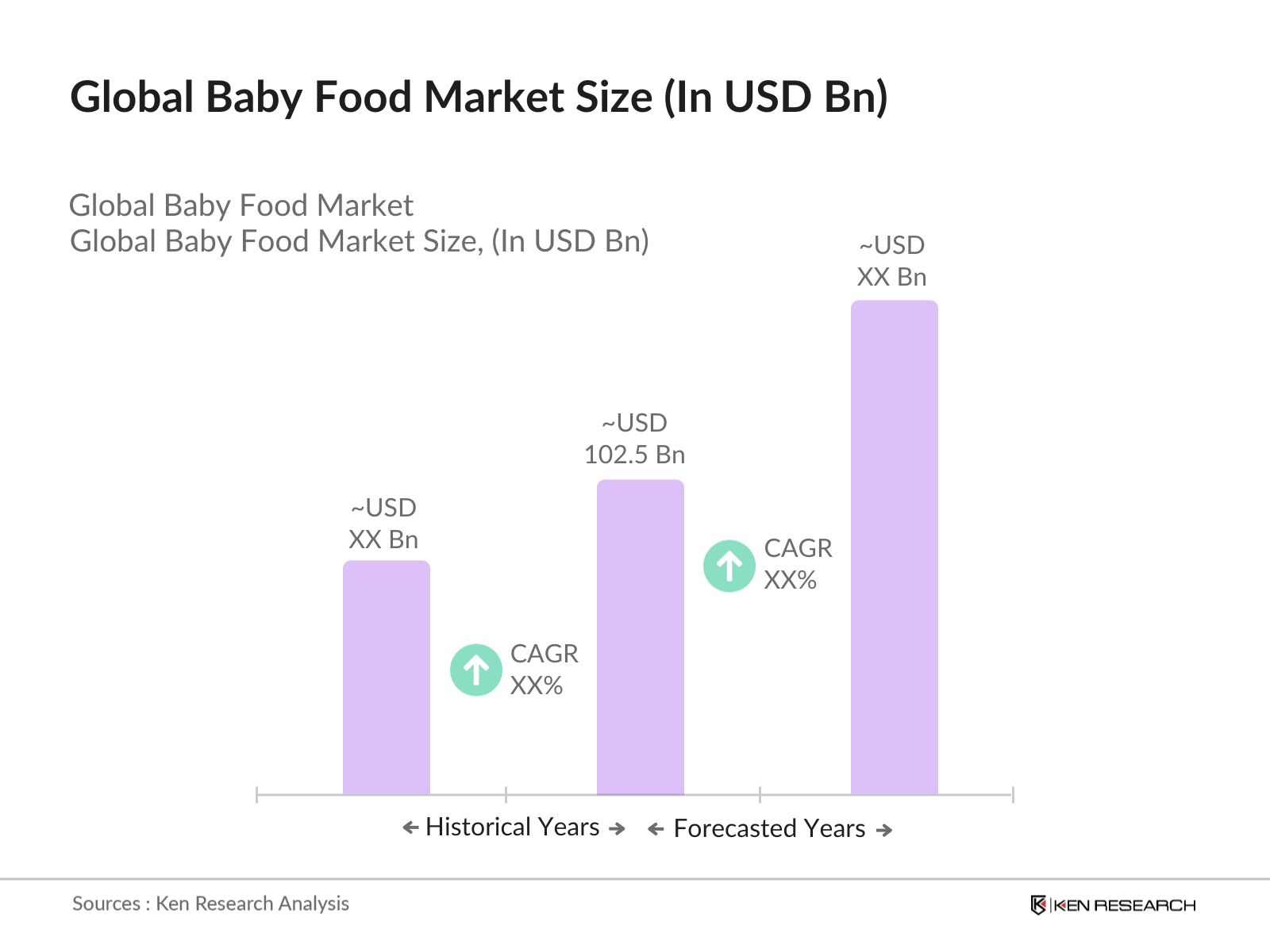

The global baby food market was valued at USD 102.5 billion, driven by increasing demand for infant nutrition, growing awareness about baby health, and expansion of e-commerce distribution.

Challenges include high production costs, stringent regulatory frameworks, and growing competition from homemade and organic baby food alternatives, making it difficult for smaller players to sustain market share.

Key players include Nestl, Abbott Laboratories, Danone, Reckitt Benckiser, and The Kraft Heinz Company. These companies lead the market due to their strong brand recognition, extensive distribution networks, and continuous product innovations.

The market is driven by rising urbanization, increasing parental focus on nutrition, growth of e-commerce, and a shift towards organic and clean-label products. Technological innovations in packaging and product formulation are also contributing to market growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.