Global Bifacial Solar Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD7970

October 2024

93

About the Report

Global Bifacial Solar Market Overview

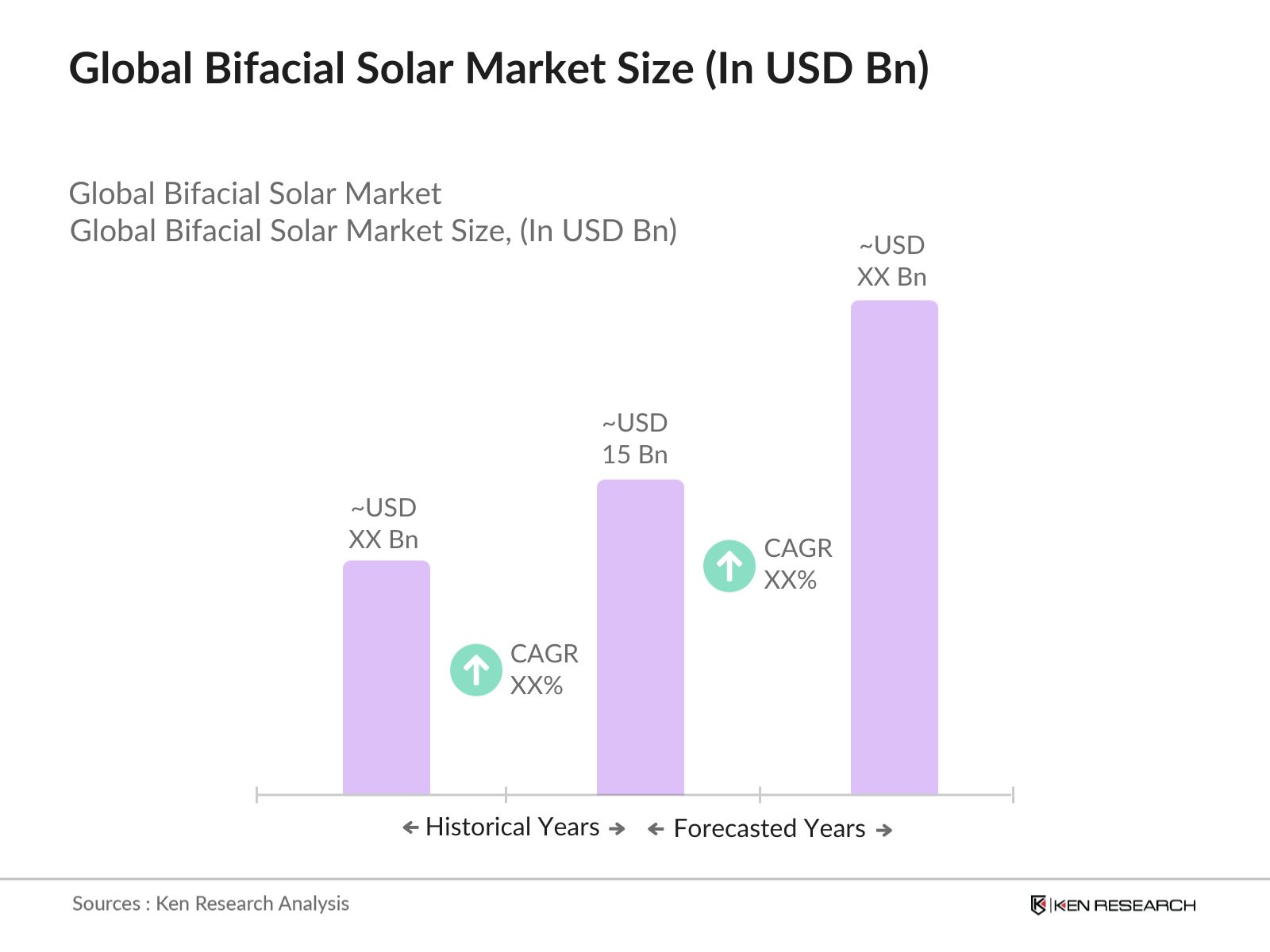

- The global bifacial solar panel market reached a valuation of USD 15 billion based on a five-year historical analysis. This growth is largely driven by the increasing adoption of bifacial technology in utility-scale projects, owing to its higher energy yield compared to traditional monofacial panels. The significant cost reduction in solar components, coupled with government incentives and the need for efficient renewable energy solutions, has further propelled market demand. The advanced efficiency of bifacial panels, which can capture sunlight on both sides, contributes to lower Levelized Cost of Energy (LCOE), making these panels highly competitive.

- Countries such as China, the United States, and Germany dominate the global bifacial solar panel market due to their well-established renewable energy infrastructure and government policies supporting solar energy. China leads the market, driven by large-scale solar farms and the country's focus on renewable energy goals. The U.S. benefits from significant investments in solar technology and an expanding market for large-scale solar farms. Meanwhile, Germanys early adoption of bifacial technology and aggressive carbon reduction targets have cemented its position as a key market player.

- International renewable energy directives are catalyzing the growth of bifacial solar technology. The European Unions Renewable Energy Directive mandates a 40% share of energy from renewables by 2030, encouraging the use of high-efficiency technologies such as bifacial solar. Meanwhile, countries like Japan and South Korea have set binding renewable targets that require substantial solar contributions, with bifacial panels expected to play a key role in meeting these goals.

Global Bifacial Solar Market Segmentation

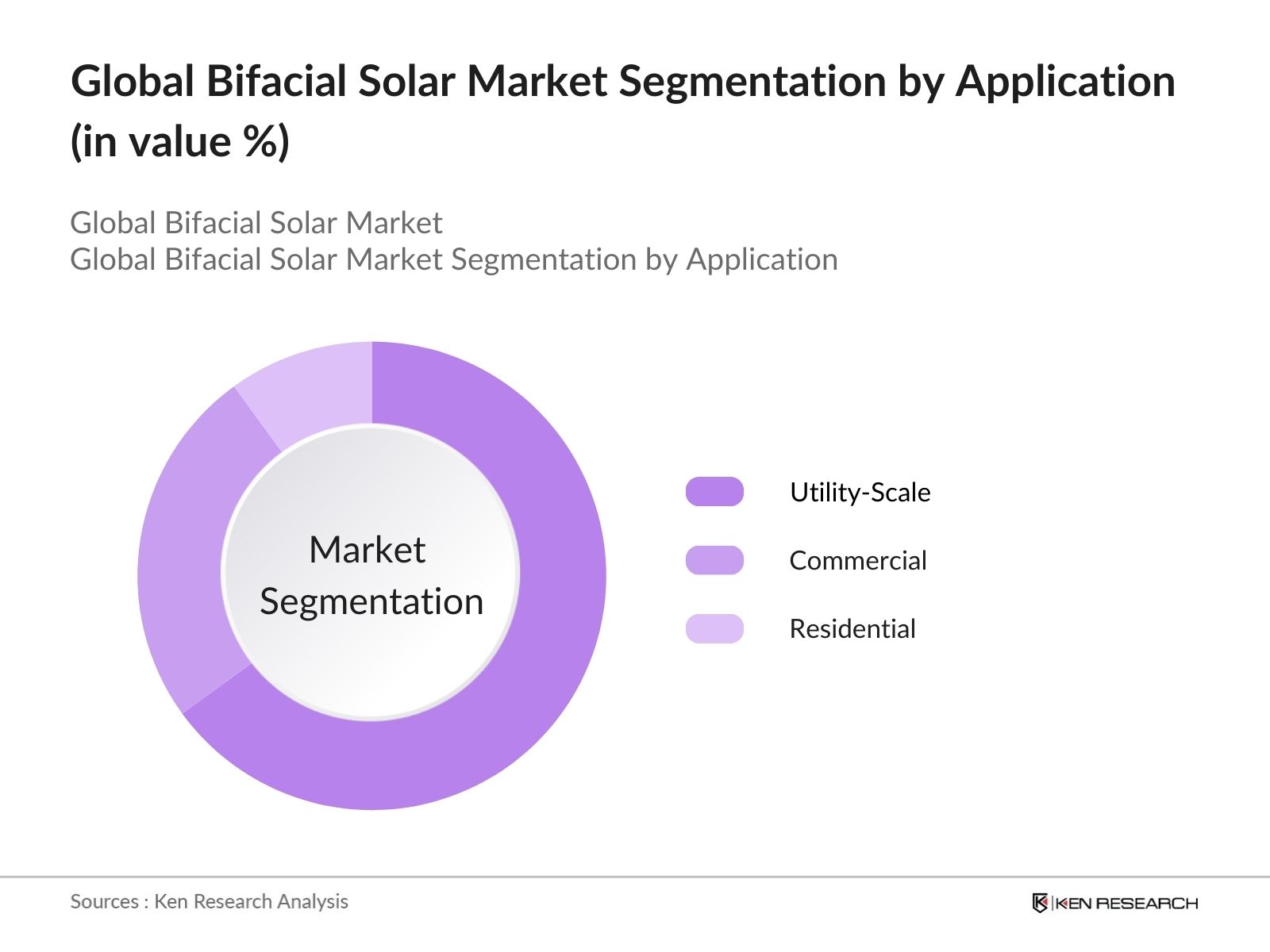

- By Application: The bifacial solar panel market is segmented into residential, commercial, and utility-scale. Utility-scale applications hold the largest market share, driven by large-scale solar projects in regions like China, the U.S., and India. The utility-scale sector benefits from the high energy output of bifacial panels, which makes them suitable for large solar farms aiming to maximize energy production and minimize costs.

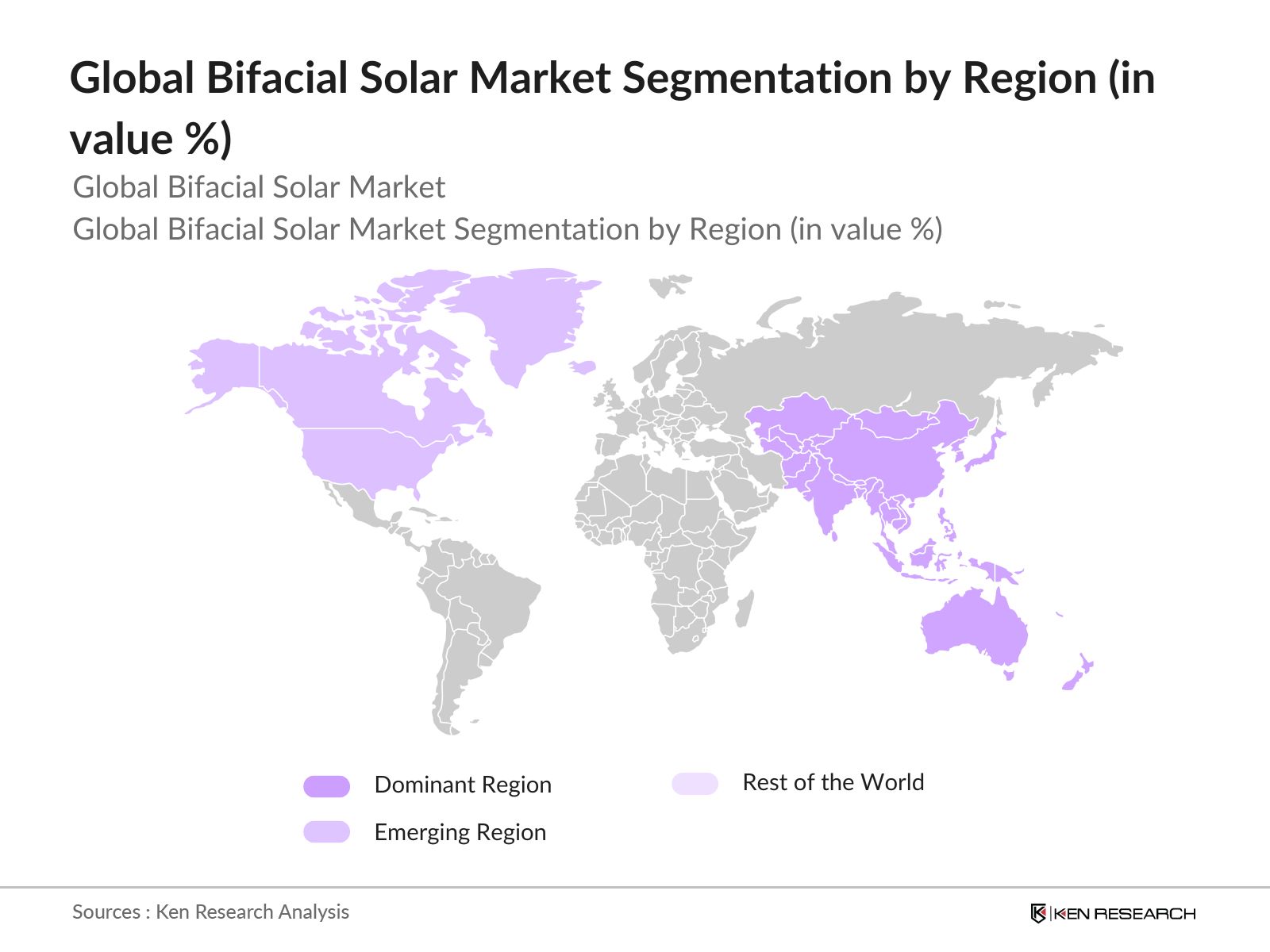

- By Region: Regionally, the bifacial solar panel market is divided into North America, Europe, Asia-Pacific, the Middle East & Africa, and Latin America. Asia-Pacific leads the market, largely due to Chinas large solar energy initiatives. The region is expected to continue its dominance as governments push for energy diversification. North America, particularly the U.S., is the second-largest market due to increased investments in renewable energy infrastructure. Europe follows closely, with countries like Germany and Spain implementing extensive solar energy policies.

Global Bifacial Solar Market Competitive Landscape

The bifacial solar panel market is dominated by a mix of global and regional players. Key companies have been focusing on expanding production capacities, improving panel efficiency, and forming strategic partnerships to maintain their market position. The market remains highly competitive, with leading manufacturers continuously innovating to reduce costs and improve energy yield.

|

Company |

Establishment Year |

Headquarters |

Global Production Capacity |

R&D Investments |

Annual Output (GW) |

Bifacial Panel Efficiency (%) |

Warranty (Years) |

Degradation Rate (% per year) |

|

Longi Solar |

2000 |

Xi'an, China |

||||||

|

JinkoSolar |

2006 |

Shanghai, China |

||||||

|

Trina Solar |

1997 |

Changzhou, China |

||||||

|

Canadian Solar |

2001 |

Guelph, Canada |

||||||

|

SunPower Corporation |

1985 |

San Jose, USA |

Global Bifacial Solar Industry Analysis

Growth Drivers

- Technological Advancements in Solar PV Efficiency: Bifacial solar panels have become a breakthrough in solar technology by utilizing both sides of the panel to generate power. In 2023, global energy output from bifacial panels saw a 20% increase in performance compared to monofacial modules. The development of advanced solar cell technologies, such as passivated emitter rear contact (PERC) and heterojunction cells, are key drivers behind this growth. For instance, countries like China, which manufactured 43 GW of bifacial modules in 2022, are setting the benchmark for innovation and efficiency improvements, according to the International Renewable Energy Agency (IRENA).

- Decline in Manufacturing Costs (LCOE, BOS Costs): The levelized cost of energy (LCOE) for solar power projects has declined sharply, dropping to around $0.057 per kWh in 2023 due to improvements in bifacial solar manufacturing. This is a result of economies of scale, automation, and enhanced module efficiency, according to the International Energy Agency (IEA). Additionally, balance-of-system (BOS) costs, which include inverters and installation, have decreased by nearly 12% in emerging markets, driving down the total installation costs for bifacial solar projects.

- Government Renewable Energy Targets: Countries worldwide are increasing their renewable energy targets, pushing the adoption of bifacial solar panels. The European Union has set a target of 45% renewable energy by 2030, with solar power playing a crucial role. In the U.S., the Inflation Reduction Act of 2022 has reinforced investment in renewable energy, with a goal of achieving 100 GW of solar capacity by 2025. In India, the government aims to install 280 GW of solar capacity by 2030, much of which will be driven by bifacial technology due to its higher efficiency.

Market Restraints

- Lack of Standardization in Efficiency Ratings: A lack of universally accepted standards for bifacial panel efficiency poses a challenge for the industry. While front-side performance can be measured easily, back-side generation is highly dependent on location and ground reflectivity (albedo), leading to inconsistent ratings. The International Electrotechnical Commission (IEC) has made strides in developing standard protocols, but as of 2024, only about 35% of global bifacial panels are certified under a common rating system, which complicates adoption.

- Grid Infrastructure Constraints (Grid Parity, Integration): Bifacial solar projects often face challenges in integrating into existing grid systems. Grid parity, where solar electricity costs are competitive with fossil fuel power, has only been achieved in a few regions. The lack of sufficient grid infrastructure, especially in emerging markets, hampers the integration of large bifacial projects. As of 2023, the International Renewable Energy Agency (IRENA) reported that grid connection costs can account for up to 30% of the total project budget in certain regions.

Global Bifacial Solar Market Future Outlook

Over the next five years, the global bifacial solar panel market is expected to experience substantial growth driven by ongoing technological innovations, reductions in manufacturing costs, and increasing demand for sustainable energy solutions. Key regions such as China, the U.S., and Germany will continue to play a major role in market expansion, while new emerging markets, especially in Latin America and Africa, are anticipated to witness increased adoption. The integration of bifacial panels with battery storage solutions and advancements in solar tracking systems will likely further boost market demand.

Market Opportunities

- Growing Demand for Clean Energy (PPA Models, Utility-Scale Projects): The global push for clean energy has created significant opportunities for bifacial solar panel adoption. Power purchase agreements (PPAs) for solar projects have surged, with 110 GW worth of utility-scale solar PPAs signed in 2022 alone, according to the U.S. Energy Information Administration (EIA). The bifacial panels' ability to generate up to 25% more energy than conventional panels makes them attractive for large-scale projects. This growth is particularly evident in the Asia-Pacific region, where over 40% of new solar capacity in 2023 is estimated to use bifacial technology.

- Favorable Policies and Incentives (Feed-In Tariffs, Net Metering): Government policies such as feed-in tariffs (FIT) and net metering are promoting the adoption of bifacial solar technology. Japan, for instance, offers FIT rates of approximately $0.14 per kWh, while China has implemented favorable net metering schemes that allow excess electricity generated by bifacial panels to be sold back to the grid. In the U.S., the Investment Tax Credit (ITC) offers a 30% tax credit for solar projects, driving investment in bifacial solar systems, with over 6 GW of bifacial panels installed in 2022.

Scope of the Report

|

Product Type |

Monocrystalline Bifacial Panels, Polycrystalline Bifacial Panels, Thin-Film Bifacial Panels |

|

Application |

Residential, Commercial, Utility-Scale |

|

Technology |

PERC, HJT, TOPCon |

|

Power Rating |

Below 150 W, 150 W to 300 W, Above 300 W |

|

Region |

North America, Europe, Asia-Pacific, Middle East & Africa, Latin America |

Products

Key Target Audience

Solar Project Developers

Solar Energy Distributors

Utility Companies

Governments and Regulatory Bodies (International Renewable Energy Agency, U.S. Department of Energy)

Renewable Energy Investors

Venture Capital and Private Equity Firms

Energy Storage Providers

Solar Technology Researchers and Manufacturers

Companies

Players Mentioned in the Report:

Longi Solar

JinkoSolar

Trina Solar

Canadian Solar

SunPower Corporation

REC Solar Holdings

First Solar

Hanwha Q Cells

Yingli Solar

GCL System Integration

Risen Energy

Seraphim Energy Group

Talesun Solar Technologies

Solaria Corporation

JA Solar

Table of Contents

1. Global Bifacial Solar Panel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Bifacial Solar Panel Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Bifacial Solar Panel Market Analysis

3.1. Growth Drivers

3.1.1. Technological Advancements in Solar PV Efficiency

3.1.2. Decline in Manufacturing Costs (LCOE, BOS Costs)

3.1.3. Government Renewable Energy Targets

3.1.4. Solar Power Adoption in Emerging Economies

3.2. Market Challenges

3.2.1. High Installation Costs

3.2.2. Lack of Standardization in Efficiency Ratings

3.2.3. Grid Infrastructure Constraints (Grid Parity, Integration)

3.3. Opportunities

3.3.1. Growing Demand for Clean Energy (PPA Models, Utility-Scale Projects)

3.3.2. Favorable Policies and Incentives (Feed-In Tariffs, Net Metering)

3.3.3. Increasing Adoption in Industrial & Commercial Segments

3.4. Trends

3.4.1. Integration of Bifacial Solar with Energy Storage

3.4.2. Floating Solar Projects using Bifacial Technology

3.4.3. Bifacial Modules in Solar Trackers

3.5. Government Regulation

3.5.1. International Renewable Energy Directives

3.5.2. Tax Incentives for Solar Energy

3.5.3. Carbon Emission Reduction Targets

3.5.4. Renewable Portfolio Standards (RPS)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.7.1. Raw Material Suppliers

3.7.2. Manufacturers and Assemblers

3.7.3. Distribution Channels (EPCs, Installers)

3.7.4. End-Users (Residential, Commercial, Utility-Scale)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Global Bifacial Solar Panel Market Segmentation (In Value %)

4.1. By Product Type

4.1.1. Monocrystalline Bifacial Panels

4.1.2. Polycrystalline Bifacial Panels

4.1.3. Thin-Film Bifacial Panels

4.2. By Application

4.2.1. Residential

4.2.2. Commercial

4.2.3. Utility-Scale

4.3. By Technology

4.3.1. PERC (Passivated Emitter and Rear Contact)

4.3.2. HJT (Heterojunction)

4.3.3. TOPCon (Tunnel Oxide Passivated Contact)

4.4. By Power Rating

4.4.1. Below 150 W

4.4.2. 150 W to 300 W

4.4.3. Above 300 W

4.5. By Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5. Global Bifacial Solar Panel Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Longi Solar

5.1.2. JinkoSolar

5.1.3. Trina Solar

5.1.4. Canadian Solar

5.1.5. JA Solar

5.1.6. REC Solar Holdings

5.1.7. First Solar

5.1.8. Hanwha Q Cells

5.1.9. SunPower Corporation

5.1.10. Yingli Solar

5.1.11. GCL System Integration

5.1.12. Risen Energy

5.1.13. Seraphim Energy Group

5.1.14. Talesun Solar Technologies

5.1.15. Solaria Corporation

5.2. Cross Comparison Parameters (Panel Efficiency, Warranty, Degradation Rate, Headquarters, Global Production Capacity, Market Share, Annual Output, R&D Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. Global Bifacial Solar Panel Market Regulatory Framework

6.1. Solar PV Certification Standards

6.2. Compliance Requirements for Renewable Installations

6.3. Solar Panel Recycling Guidelines

6.4. Carbon Offsetting Programs

7. Global Bifacial Solar Panel Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Bifacial Solar Panel Future Market Segmentation (In Value %)

8.1. By Product Type

8.2. By Application

8.3. By Technology

8.4. By Power Rating

8.5. By Region

9. Global Bifacial Solar Panel Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In the initial phase, a detailed analysis of the global bifacial solar panel market's ecosystem is conducted. This includes identifying all stakeholders, such as manufacturers, raw material suppliers, and end-users. Extensive desk research and data from industry databases help define the key variables influencing market growth, such as energy efficiency and LCOE.

Step 2: Market Analysis and Construction

This step involves gathering and analyzing historical data on market trends, bifacial panel adoption rates, and manufacturing capacities. By constructing data models, we evaluate the market size and segment growth patterns. Special attention is given to emerging markets and regional adoption rates.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses are tested through consultations with industry experts, manufacturers, and distributors. These interviews are conducted using CATI methods to gather real-world insights and validate the market dynamics and projections.

Step 4: Research Synthesis and Final Output

In the final phase, a detailed report is synthesized from both top-down and bottom-up data analyses. This report includes validated figures on market size, growth drivers, challenges, and segment-specific insights, ensuring a comprehensive understanding of the global bifacial solar panel market.

Frequently Asked Questions

01. How big is the Global Bifacial Solar Panel Market?

The global bifacial solar panel market is valued at USD 15 billion based on a five-year historical analysis. with growing demand driven by utility-scale projects and technological advancements in panel efficiency.

02. What are the challenges in the Bifacial Solar Panel Market?

Key challenges include the high initial installation costs, lack of standardization in efficiency ratings, and integration issues with existing grid infrastructures, particularly in developing regions.

03. Who are the major players in the Global Bifacial Solar Panel Market?

Major players include Longi Solar, JinkoSolar, Trina Solar, Canadian Solar, and SunPower Corporation. These companies dominate the market due to their large production capacities, strong R&D focus, and global reach.

04. What are the growth drivers of the Bifacial Solar Panel Market?

The market is propelled by factors such as increased solar efficiency, declining component costs, favorable government incentives, and the global shift towards clean energy.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.