Global Carbon Capture and Storage (CCS) Market Outlook to 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2448

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2448

November 2024

89

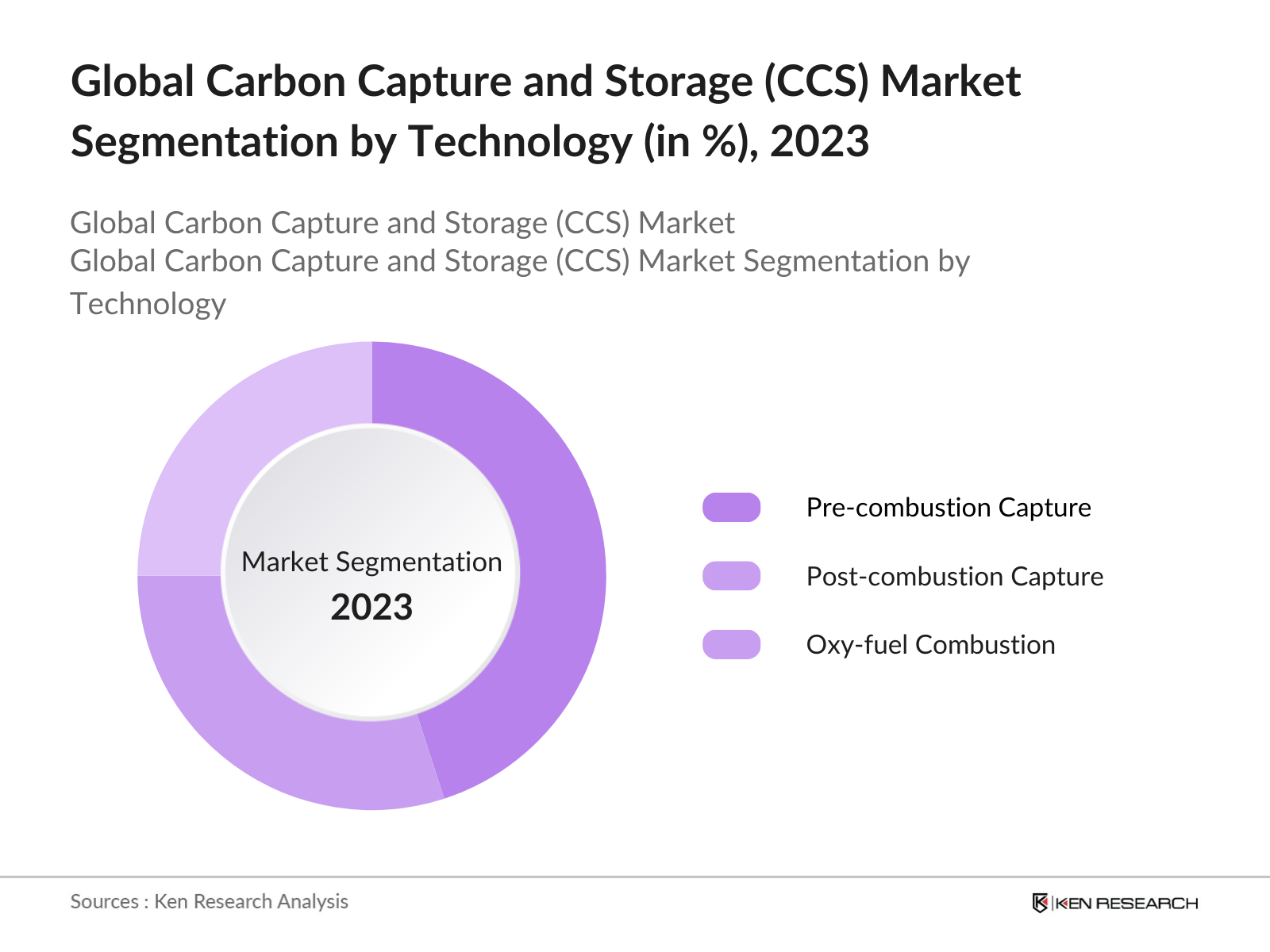

By Technology: The global CCS market is segmented by technology into pre-combustion capture, post-combustion capture, and oxy-fuel combustion. In 2023, pre-combustion capture has been noted to dominate the CCS market due to its effectiveness in capturing large volumes of CO2 at lower costs compared to post-combustion methods. This cost-effectiveness and efficiency make it a preferred choice for power plants and industrial applications.

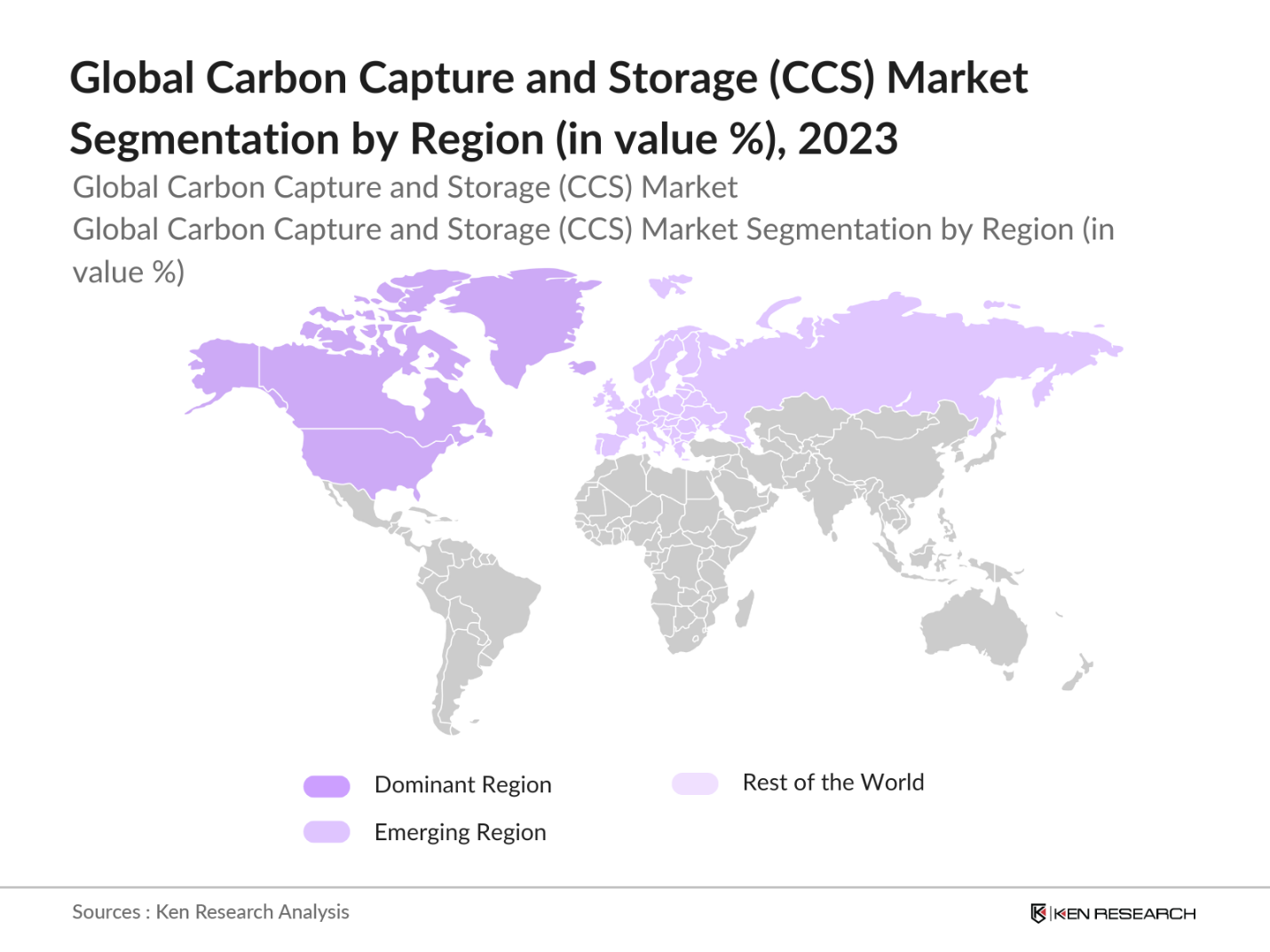

By Region: The global CCS market is segmented into North America, Europe, Asia-Pacific (APAC), Latin America, and the Middle East & Africa (MEA). North America dominates the market in 2023, driven by favorable government policies, significant investments, and the presence of major players such as ExxonMobil and Chevron. The U.S. and Canada lead the CCS space with extensive project development and large-scale storage capacities. Government initiatives, like the U.S. 45Q carbon capture credits, have further accelerated growth in this region.

By End-Use Industry: The global CCS market is segmented by end-use industry into power generation, oil and gas, and chemicals. In 2023, power generation holds the dominant position, driven by the sector's significant carbon emissions and the urgent need for emission reduction solutions. Coal and natural gas-fired power plants are increasingly adopting CCS technologies to comply with environmental regulations. The electricity sector is a major contributor to greenhouse gas emissions, accounting for about one-third of total emissions in the U.S.

|

Company Name |

Establishment Year |

Headquarters |

|

ExxonMobil |

1870 |

Irving, Texas |

|

Shell |

1907 |

The Hague, Netherlands |

|

Chevron |

1879 |

San Ramon, California |

|

TotalEnergies |

1924 |

Paris, France |

|

Equinor |

1972 |

Stavanger, Norway |

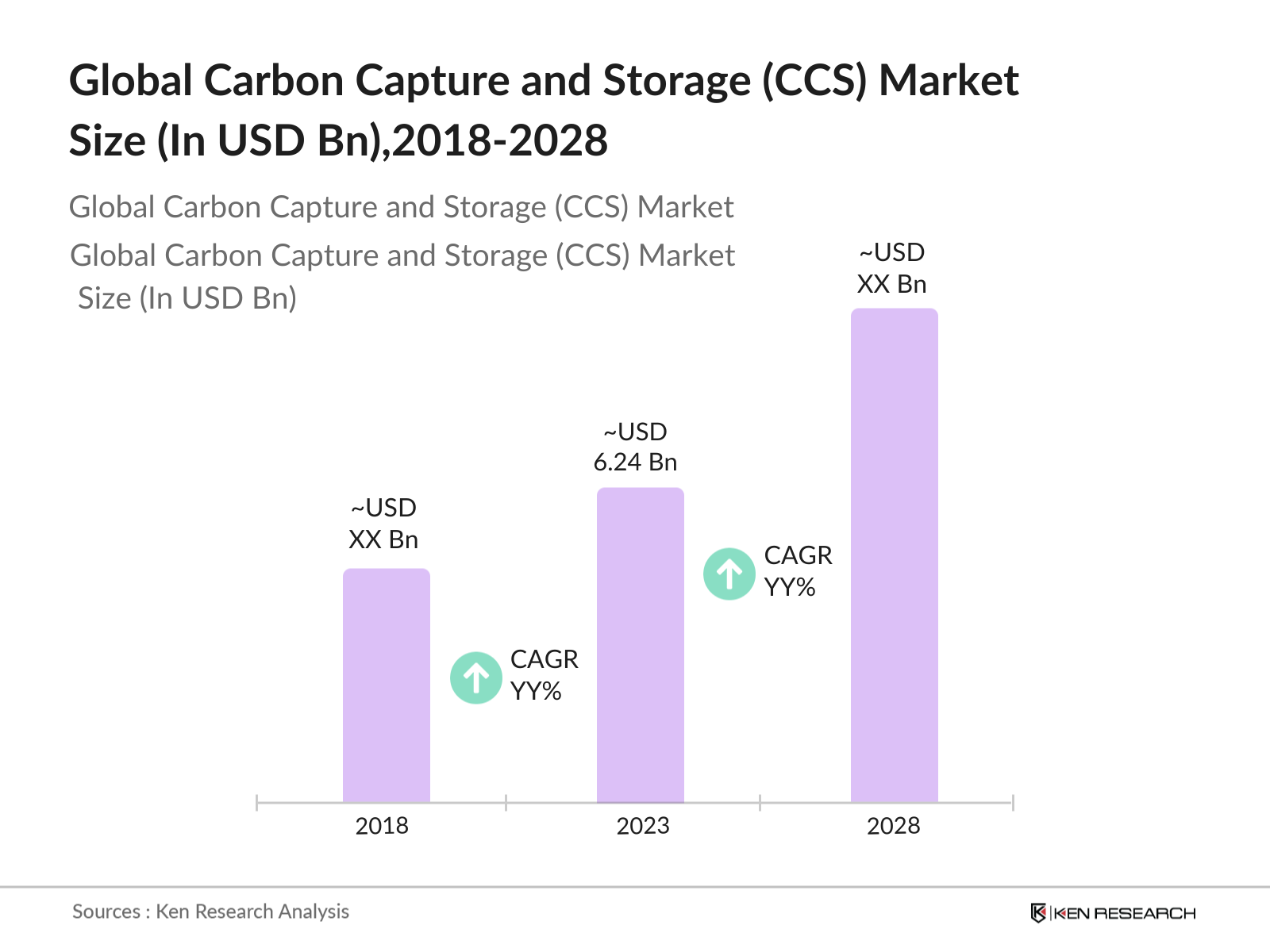

The global carbon capture and storage (CCS) market is poised for significant growth by 2028, driven by a combination of government initiatives, stricter environmental regulations, and the increasing demand for sustainable industrial practices. As countries push toward achieving net-zero carbon emissions targets, CCS will play a vital role in reducing CO2 emissions across energy-intensive sectors.

|

By Technology |

Pre-combustion Capture Post-combustion Capture Oxy-fuel Combustion |

|

By End-Use Industry |

Power Generation Oil and Gas Chemicals |

|

By Region |

North America Europe APAC Latin America MEA |

|

By Capture Method |

Point Source Capture Industrial Carbon Capture Direct Air Capture |

01. Global Carbon Capture and Storage (CCS) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Government Investments

3.1.2. Demand from High-Emission Sectors

3.1.3. Net-Zero Emissions Push

3.2. Restraints

3.2.1. High Implementation Costs

3.2.2. Limited Storage Infrastructure

3.2.3. Policy and Regulatory Uncertainties

3.3. Opportunities

3.3.1. Carbon Capture for Industrial Applications

3.3.2. Innovation in CO2 Storage Technologies

3.3.3. Potential for Market Expansion in Emerging Economies

3.4. Trends

3.4.1. Public-Private Partnerships

3.4.2. Cluster-Based Carbon Capture Projects

3.4.3. Scaling of Pilot Projects to Full Deployment

3.5. Government Initiatives

3.5.1. U.S. Carbon Capture Program

3.5.2. European Union Innovation Fund

3.5.3. Canadas Net-Zero Accelerator Initiative

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competitive Ecosystem

4.1. By Technology (in Value %)

4.1.1. Pre-combustion Capture

4.1.2. Post-combustion Capture

4.1.3. Oxy-fuel Combustion

4.2. By End-Use Industry (in Value %)

4.2.1. Power Generation

4.2.2. Oil and Gas

4.2.3. Chemicals

4.3. By Region (in Value %)

4.3.1. North America

4.3.2. Europe

4.3.3. Asia-Pacific (APAC)

4.3.4. Latin America

4.3.5. Middle East & Africa (MEA)

4.4. By Capture Method (in Value %)

4.4.1. Point Source Capture

4.4.2. Industrial Carbon Capture

4.4.3. Direct Air Capture

4.5. By Storage Type (in Value %)

4.5.1. Geological Storage

4.5.2. Mineral Storage

4.5.3. Ocean Storage

4.6. By CO2 Source (in Value %)

4.6.1. Power Plants

4.6.2. Industrial Processes

4.6.3. Transportation

4.7. By Deployment Type (in Value %)

4.7.1. Enhanced Oil Recovery (EOR)

4.7.2. Standalone CCS Projects

4.7.3. Integrated CCS Systems

5.1. Detailed Profiles of Major Companies

5.1.1. ExxonMobil

5.1.2. Shell

5.1.3. Chevron Corporation

5.1.4. TotalEnergies

5.1.5. Equinor

5.1.6. BP

5.1.7. Schlumberger

5.1.8. Fluor Corporation

5.1.9. Linde PLC

5.1.10. Mitsubishi Heavy Industries

5.1.11. Aker Solutions

5.1.12. Air Liquide

5.1.13. Siemens Energy

5.1.14. Honeywell International Inc.

5.1.15. General Electric (GE)

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Region (in Value %)

9.2. By Technology (in Value %)

9.3. By CO2 Source (in Value %)

9.4. By Storage Type (in Value %)

9.5. By Deployment Type (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on the Global Carbon Capture and Storage (CCS) Market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Global Carbon Capture and Storage (CCS) Market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple Carbon Capture and Storage (CCS) and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from Carbon Capture and Storage (CCS).

The global carbon capture and storage (CCS) market was valued at USD 6.24 billion in 2023. It is driven by stringent environmental regulations, growing investments in sustainable technologies, and the need for large-scale carbon emissions reduction across industries like power generation and oil and gas.

Challenges in the CCS market include high operational costs, limited availability of suitable CO2 storage sites, and inadequate infrastructure for transporting captured carbon. Additionally, regulatory uncertainties in some regions hinder the smooth development of large-scale CCS projects.

Key players in the global CCS market include ExxonMobil, Shell, Chevron Corporation, TotalEnergies, and Equinor. These companies lead the market through extensive investments in infrastructure, cutting-edge CCS technologies, and strategic partnerships for CO2 capture and storage.

The growth of the CCS market is driven by increasing governmental investments in climate mitigation, the push for net-zero carbon emissions, and growing adoption of CCS technology in high-emission sectors like power generation, oil and gas, and chemicals.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.