Global Cell Surface Markers Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1459

November 2024

84

About the Report

Global Cell Surface Markers Market Overview

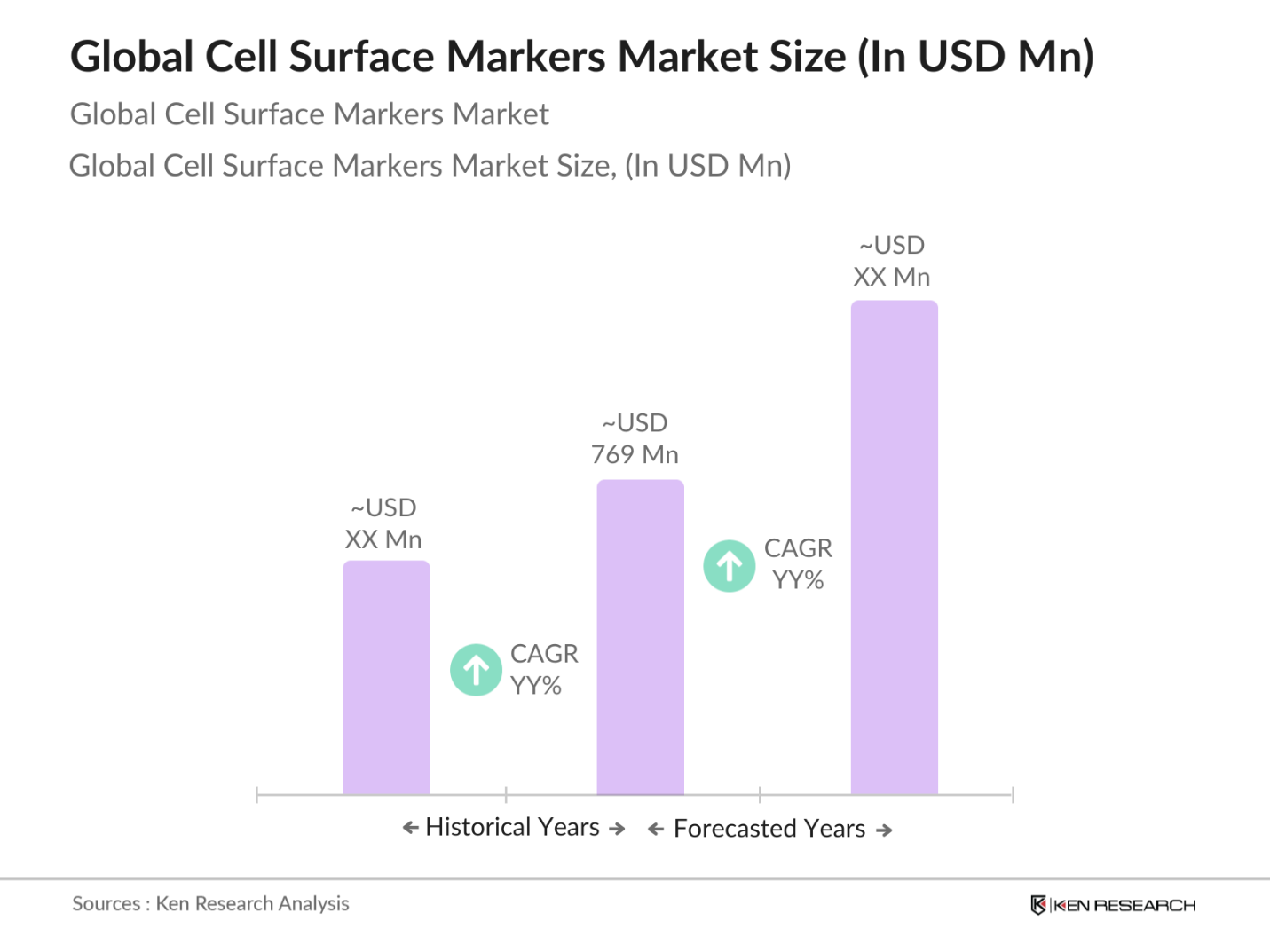

- The global cell surface markers market is valued at USD 769 million, based on a five-year historical analysis. This growth is primarily driven by the increasing use of cell surface markers in precision medicine, specifically in cancer research, HIV treatment, and stem cell therapies. Additionally, the rise in diagnostic applications, fueled by advancements in flow cytometry and PCR arrays, is further contributing to the expansion of this market. These markers are essential for identifying specific cell types, which facilitates disease diagnosis and research efforts, thus driving market demand

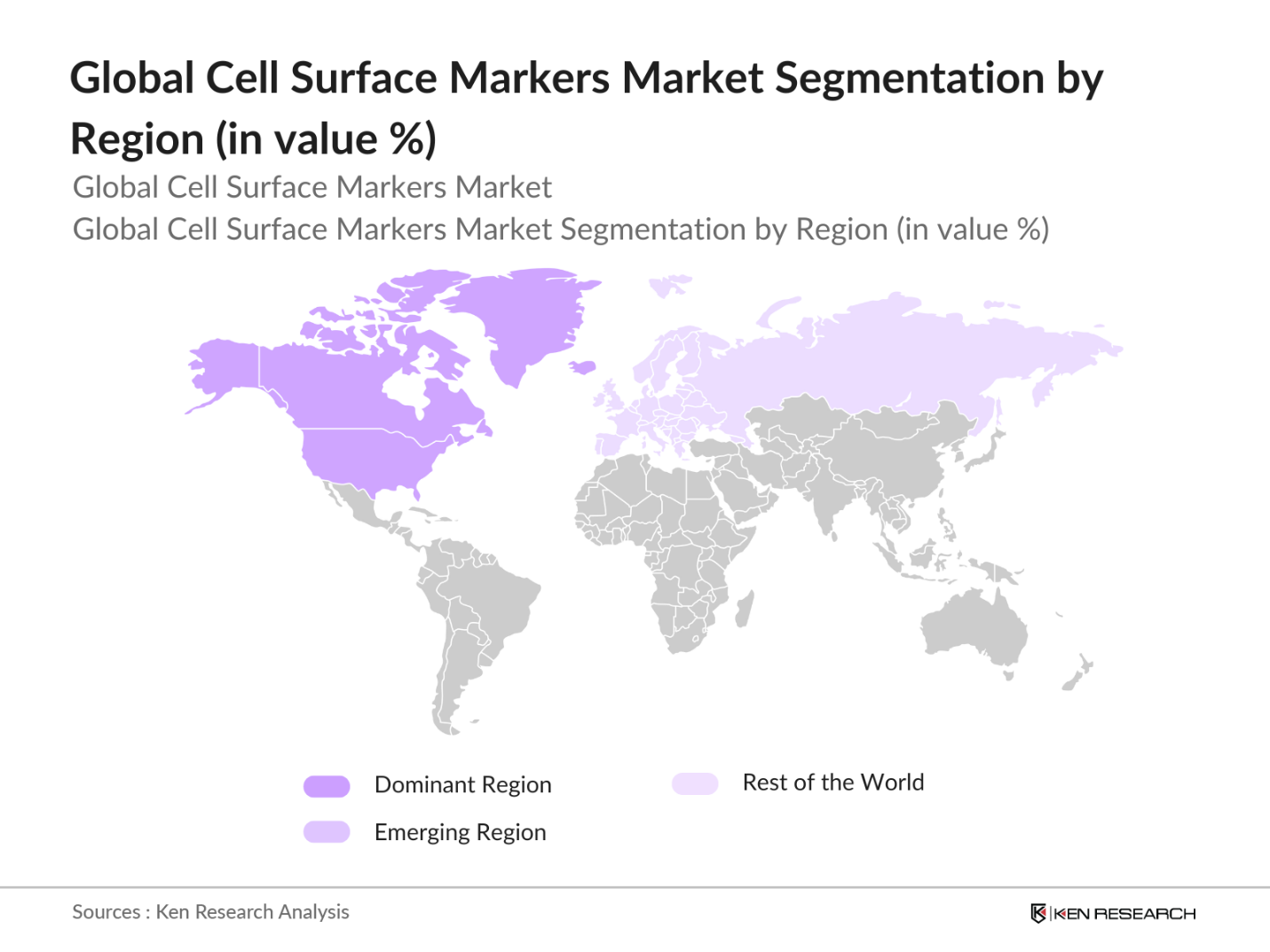

- The global market is dominated by regions such as North America and Europe, with the United States and Germany leading due to their advanced healthcare infrastructure and significant investment in biotechnology. The U.S. remains dominant because of its large pharmaceutical sector, extensive research and development in personalized medicine, and government-backed healthcare initiatives. Meanwhile, Germany leads in Europe due to its advanced diagnostic technologies and well-established pharmaceutical industry

- The U.S. government launched the Precision Medicine Initiative (PMI) to revolutionize disease treatment through individualized approaches. In 2023, the PMI received $1.4 billion in federal funding aimed at accelerating research in areas like cancer, rare diseases, and the application of cell surface markers. This initiative includes partnerships with leading biotech firms and academic institutions to integrate cell-based diagnostics, further driving demand for cell surface markers in personalized medicine.

Global Cell Surface Markers Market Segmentation

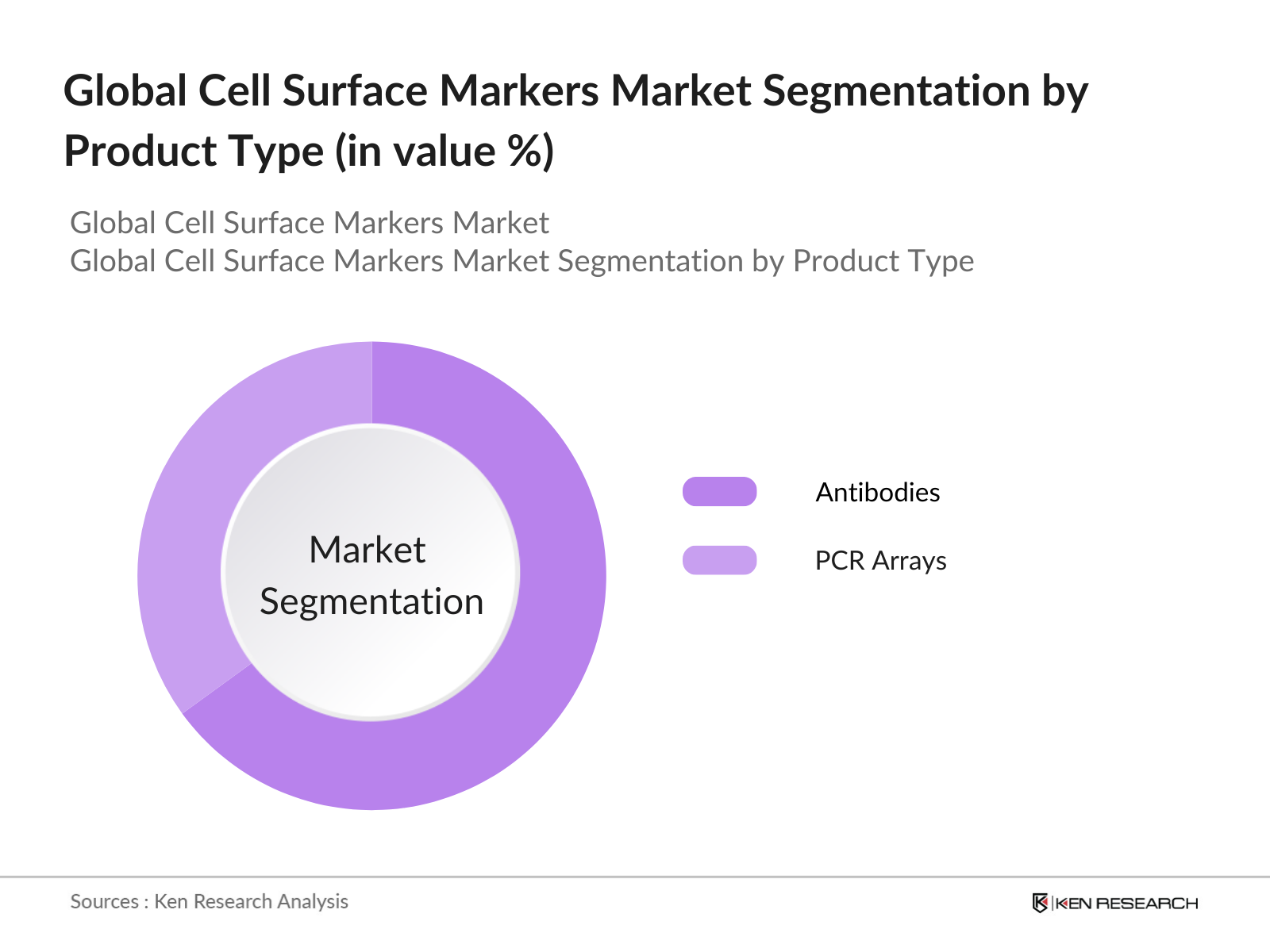

By Product Type: The global cell surface markers market is segmented by product type into antibodies and PCR arrays. Antibodies currently hold a dominant market share due to their widespread use in diagnostic and therapeutic applications. Their ability to bind specific antigens makes them invaluable in detecting diseases such as cancer. The dominance of this segment is also attributed to the extensive research being conducted in the field of immunology, which requires high volumes of antibodies for cell surface marker identification.

By Region: The cell surface markers market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. North America continues to dominate, particularly the U.S., due to high healthcare spending and extensive research facilities. The strong presence of biotech companies, a well-established pharmaceutical industry, and growing investments in personalized medicine are driving the dominance of this region.

Global Cell Surface Markers Market Competitive Landscape

The global cell surface markers market is dominated by a few key players, who leverage strategic partnerships and mergers to maintain their market positioning. Companies like Thermo Fisher Scientific and BD (Becton, Dickinson, and Company) have a strong market presence due to their advanced product offerings and extensive distribution networks. Collaborations with academic and research institutes also play a crucial role in their market dominance.

|

Company |

Established |

Headquarters |

Revenue |

Product Portfolio |

R&D Focus |

Key Partnerships |

Geographical Reach |

Market Position |

|

Thermo Fisher Scientific |

1956 |

U.S. |

- |

|||||

|

BD (Becton, Dickinson) |

1897 |

U.S. |

- |

- |

- |

- |

- |

- |

|

Abcam |

1998 |

U.K. |

- |

- |

- |

- |

- |

- |

|

Qiagen N.V. |

1984 |

Netherlands |

- |

- |

- |

- |

- |

- |

|

F. Hoffmann-La Roche Ltd. |

1896 |

Switzerland |

- |

- |

- |

- |

- |

- |

Global Cell Surface Markers Market Analysis

Global Cell Surface Markers Market Growth Drivers

- Increasing Demand for Precision Medicine: Precision medicine, driven by advances in molecular diagnostics and personalized healthcare, is seeing significant adoption. The global push for tailored treatments is leading to a surge in cell surface marker applications. According to the World Health Organization (WHO), non-communicable diseases, particularly cancer and cardiovascular conditions, account for of deaths worldwide in 2023, intensifying the demand for precision medicine. The development of therapies based on specific genetic and phenotypic profiles further boosts the use of cell surface markers, helping to identify and target disease pathways precisely.

- Advancements in Cell-Based Research: Cell-based research, particularly in oncology, immunology, and regenerative medicine, has grown exponentially due to technological advancements. Flow cytometry and immunohistochemistry technologies now allow for more accurate detection of cellular markers. In 2023, it was reported that global research and development (R&D) investments in biotechnology reached over $250 billion, much of which is directed towards cell-based research. The National Institutes of Health (NIH) has also allocated over $50 billion for biomedical research, fueling innovation in the field of cell surface markers

- Growing Application in Disease Diagnosis (Cancer, HIV, Stem Cell Research): Cell surface markers play a critical role in diagnosing a wide range of diseases such as cancer, HIV, and facilitating stem cell research. In 2023, approximately 10 million people were diagnosed with cancer globally, highlighting the growing need for precise diagnostic tools. The global HIV population stands at 38 million as per the UNAIDS report, with surface marker-based tests crucial for monitoring disease progression. Furthermore, stem cell research is advancing rapidly, with the U.S. and China leading in government funding and clinical applications.

Global Cell Surface Markers Market Challenges

- High Costs of Advanced Diagnostic Tools: The adoption of advanced diagnostic tools, such as flow cytometry and immunohistochemistry, is often hindered by high costs, particularly in low-income countries. According to the World Bank, healthcare spending per capita in low- and middle-income countries averages around $300 annually, which significantly limits the availability and accessibility of advanced diagnostic technologies. This issue is most prevalent in regions such as sub-Saharan Africa, where healthcare systems are underfunded and diagnostic infrastructures are lacking.

- Limited Access to Healthcare in Developing Regions: Limited healthcare infrastructure and resources in developing regions pose significant challenges for the market expansion of cell surface markers. According to the World Bank, of people in low-income countries still lack access to essential health services as of 2023. This lack of access hinders the adoption of advanced diagnostic tools, limiting the potential market growth for cell surface marker-based technologies in regions such as Africa, Southeast Asia, and parts of Latin America.

Global Cell Surface Markers Market Future Outlook

Over the next five years, the global cell surface markers market is expected to experience significant growth, driven by technological advancements in diagnostics, rising demand for precision medicine, and increasing investments in biotechnology. The integration of artificial intelligence and machine learning in diagnostics is also expected to play a pivotal role in expanding the market. Additionally, the ongoing demand for advanced cancer treatment and immunotherapy is likely to further propel market growth.

Market Opportunities:

- Rising Use of Flow Cytometry in Research: Flow cytometry is increasingly being adopted in research labs due to its ability to analyze multiple cell surface markers simultaneously. In 2023, the global flow cytometry equipment market reached approximately 60,000 units, with widespread usage in immunology, oncology, and microbiology. The U.S. leads in the adoption of flow cytometry technologies, with over 10,000 labs utilizing this technique for advanced research and diagnostic purposes. Additionally, China is rapidly increasing its usage of this technology, spurred by government-funded research initiatives.

- Expansion of Cell Marker-Based Diagnostic Tools: The growing demand for early and accurate diagnosis of complex diseases such as cancer and autoimmune disorders is driving the expansion of cell marker-based diagnostic tools. In 2023, approximately 19 million cancer cases were diagnosed globally, emphasizing the importance of precise diagnostic tools. The development of cell marker-based technologies, such as monoclonal antibodies and PCR arrays, has become critical in improving diagnostic accuracy and patient outcomes. Significant investments by biotechnology firms in North America and Europe are driving this expansion.

Scope of the Report

|

By Product Type |

Static Volumetric Displays Swept-Volume Displays Multi-Planar Volumetric Displays |

|

By Display Technology |

Digital Light Processing (DLP) Liquid Crystal Display (LCD) Light Emitting Diode (LED) |

|

By Application |

Medical Imaging AR/VR Advertising and Marketing Engineering and Design |

|

By End-User |

Healthcare, Automotive, Aerospace & Defense Entertainment and Media Education |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Biotechnology & Pharmaceutical Companies

Clinical Testing Laboratories

Academic & Research Institutes

Investments and Venture Capitalist Firms

Government & Regulatory Bodies (FDA, EMA, PMDA)

Diagnostic Equipment Manufacturers

Hospital Chains

R&D Organizations in Healthcare

Companies

Players Mention in the Report

Thermo Fisher Scientific

BD (Becton, Dickinson and Company)

Abcam

Qiagen N.V.

F. Hoffmann-La Roche Ltd

Bio-Rad Laboratories

Danaher Corporation (Beckman Coulter)

Genscript

Biolegend

Agilent Technologies

Siemens Healthineers

Sysmex Corporation

Nihon Kohden Corporation

Grifols SA

Merck KGaA

Table of Contents

1. Global Cell Surface Markers Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Cell Surface Markers Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Cell Surface Markers Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for Precision Medicine

3.1.2. Advancements in Cell-Based Research

3.1.3. Growing Application in Disease Diagnosis (Cancer, HIV, Stem Cell Research)

3.2. Market Challenges

3.2.1. High Costs of Advanced Diagnostic Tools

3.2.2. Complexities in Regulatory Approvals

3.2.3. Limited Access to Healthcare in Developing Regions

3.3. Opportunities

3.3.1. Expansion in Personalized Medicine

3.3.2. Integration of AI in Diagnostics

3.3.3. Increasing R&D Investments

3.4. Trends

3.4.1. Rising Use of Flow Cytometry in Research

3.4.2. Expansion of Cell Marker-Based Diagnostic Tools

3.4.3. Adoption of PCR Arrays in Drug Discovery

3.5. Regulatory Landscape

3.5.1. FDA and EMA Regulations

3.5.2. Government Funding for Biotech Research

3.5.3. Ethical Challenges in Biotechnology

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Global Cell Surface Markers Market Segmentation

4.1. By Product (In Value %)

4.1.1. Antibodies

4.1.2. PCR Arrays

4.2. By Application (In Value %)

4.2.1. Disease Diagnosis (Cancer, HIV, etc.)

4.2.2. Research Applications

4.2.3. Drug Discovery

4.3. By Cell Type (In Value %)

4.3.1. T Cell Surface Markers

4.3.2. NK Cell Surface Markers

4.3.3. B Cell Surface Markers

4.3.4. Monocyte Cell Surface Markers

4.4. By End User (In Value %)

4.4.1. Hospitals & Clinical Testing Laboratories

4.4.2. Academic & Research Institutes

4.4.3. Biotechnology & Pharmaceutical Companies

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Cell Surface Markers Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Thermo Fisher Scientific

5.1.2. Becton, Dickinson and Company

5.1.3. Abcam

5.1.4. Qiagen N.V.

5.1.5. Bio-Rad Laboratories

5.1.6. F. Hoffmann-La Roche Ltd.

5.1.7. Danaher Corporation (Beckman Coulter)

5.1.8. Genscript

5.1.9. Biolegend

5.1.10. Agilent Technologies

5.1.11. Siemens Healthineers

5.1.12. Sysmex Corporation

5.1.13. Nihon Kohden Corporation

5.1.14. Grifols SA

5.1.15. Merck KGaA

5.2. Cross Comparison Parameters (Revenue, Headquarters, Market Share, R&D Focus, Product Launches)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Collaborations, Partnerships, Product Innovations)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Venture Capital, Government Funding)

6. Global Cell Surface Markers Market Regulatory Framework

6.1. Global Regulatory Standards

6.2. Compliance Requirements for New Diagnostic Tools

6.3. Ethical Concerns in Cell Surface Marker Research

7. Global Cell Surface Markers Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8. Global Cell Surface Markers Future Market Segmentation

8.1. By Product (Antibodies, PCR Arrays)

8.2. By Application (Research, Disease Diagnosis, Drug Discovery)

8.3. By Cell Type (T, NK, B, Monocyte Cell Markers)

8.4. By End User (Academic Institutes, Clinical Labs, Pharma Companies)

8.5. By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa)

9. Global Cell Surface Markers Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunities

9.4. Market Entry Strategies

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying major variables affecting the global cell surface markers market. A comprehensive review of key stakeholders is conducted, using a mix of proprietary and secondary databases to ensure accurate information.

Step 2: Market Analysis and Construction

We analyze historical data, focusing on the penetration of diagnostic tools, the demand for precision medicine, and the revenue generated by key product categories such as antibodies and PCR arrays. Market quality and size estimates are verified through multiple sources.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are tested through direct interactions with industry experts via telephonic interviews, surveys, and consultations. These insights provide operational and market-level clarity, ensuring accurate validation of data points.

Step 4: Research Synthesis and Final Output

Finally, data gathered is synthesized into a structured report. Key performance indicators (KPIs) are analyzed, and this is corroborated through cross-validation with major industry stakeholders to ensure accuracy and relevance.

Frequently Asked Questions

01. How big is the global cell surface markers market?

The global cell surface markers market is valued at USD 769 million, driven by advancements in diagnostics and growing applications in precision medicine.

02. What are the challenges in the global cell surface markers market?

Challenges include high costs of advanced diagnostic tools, complex regulatory requirements, and limited access to these technologies in developing countries.

03. Who are the major players in the global cell surface markers market?

Key players include Thermo Fisher Scientific, BD, Abcam, Qiagen N.V., and F. Hoffmann-La Roche Ltd, known for their extensive product offerings and R&D capabilities.

04. What are the growth drivers of the global cell surface markers market?

Growth is driven by increasing use of cell surface markers in cancer research, HIV treatment, and precision medicine, alongside advancements in diagnostic technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.