Global Cellular Health Screening Market Outlook to 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1445

November 2024

91

About the Report

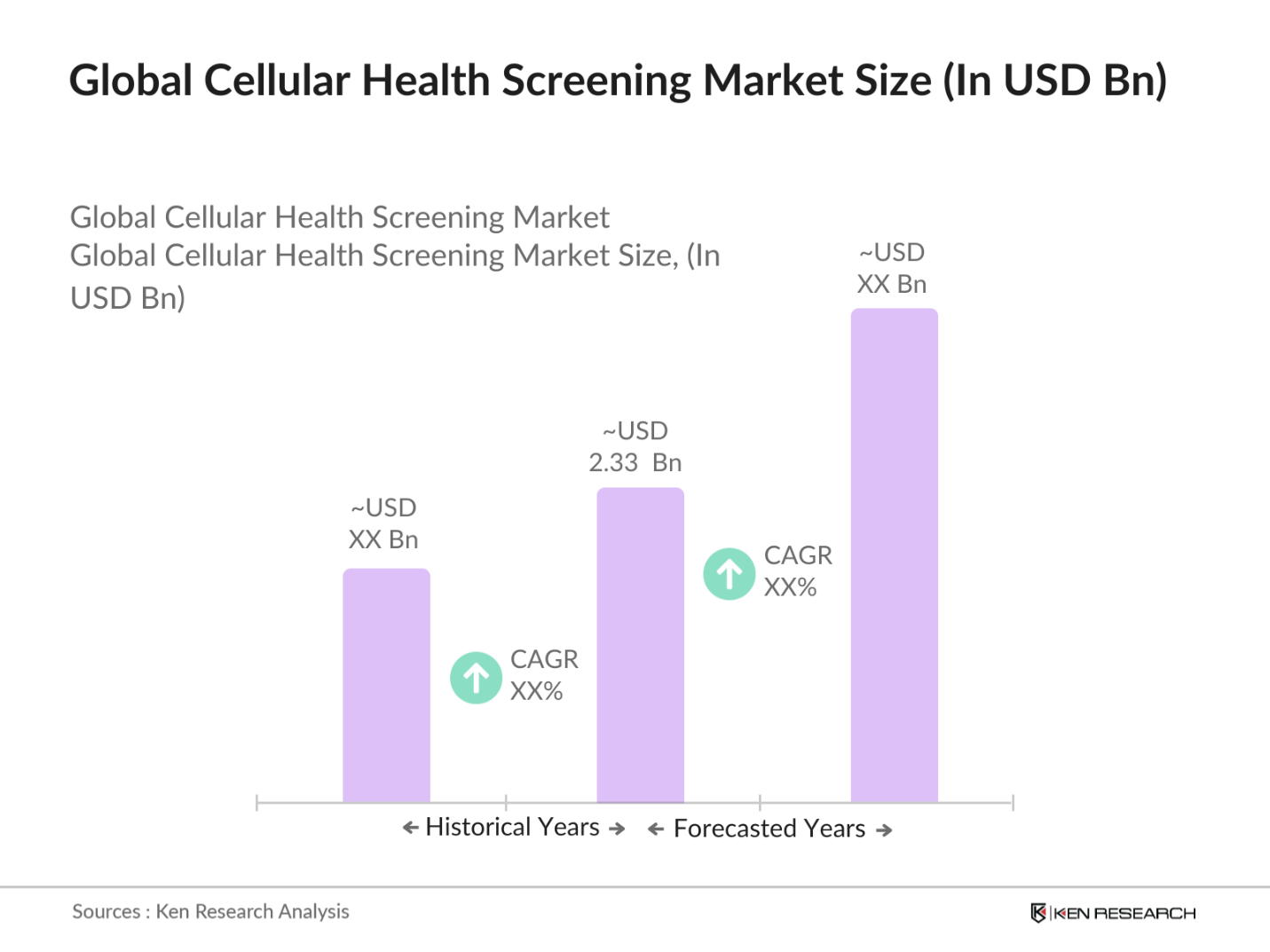

Global Cellular Health Screening Market Overview

- The global cellular health screening market is valued at approximately USD 2.33 billion. The markets growth is driven by increasing awareness of preventive healthcare and the rising incidence of chronic diseases, which has prompted the adoption of cellular health screening tests. The growing interest in personalized medicine and advancements in testing technologies like telomere length testing and oxidative stress analysis are key contributors to market expansion. Continuous investments in research and development by biotech firms are also enhancing the accuracy and accessibility of these screening tools.

- North America, particularly the United States, dominates the global cellular health screening market. The dominance is due to the presence of major players, such as Telomere Diagnostics and SpectraCell Laboratories, and the regions advanced healthcare infrastructure. Additionally, high disposable income and a strong focus on preventive healthcare contribute to the region's leadership in this market. Europe also holds a significant market share, with countries like Germany and the UK leading due to extensive healthcare reimbursement policies and research facilities.

- The National Cancer Institutes Precision Medicine Initiative in the U.S. promotes personalized cellular health screening, particularly for cancer detection. In 2023, the initiative saw a $400 million investment aimed at expanding genomic and cellular diagnostic tools for personalized treatment plans. This program supports nationwide access to cellular health tests, contributing to early detection and personalized therapy recommendations for over 1 million patients annually.

Global Cellular Health Screening Market Segmentation

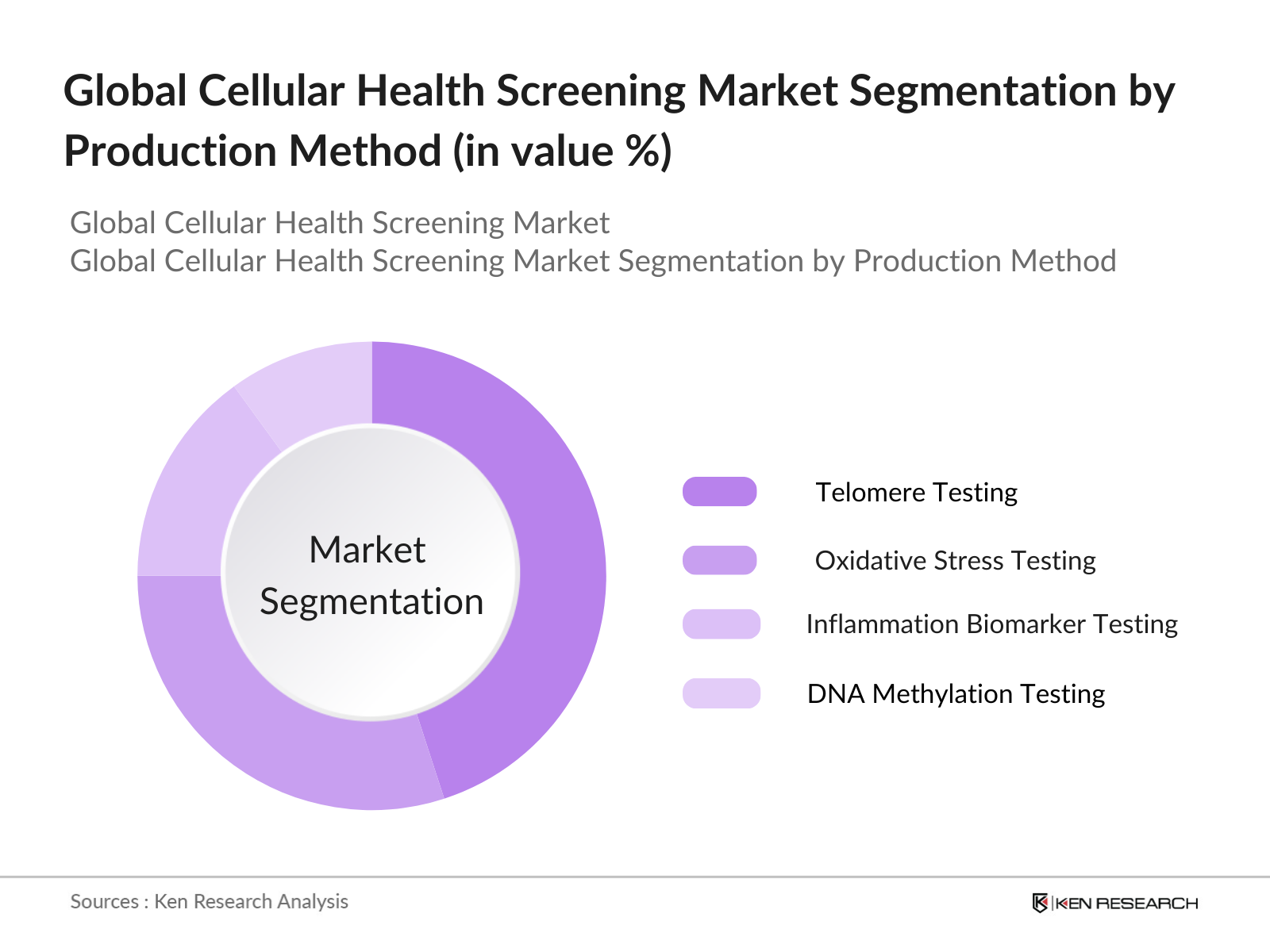

By Product Type: The cellular health screening market is segmented by product type into telomere testing, oxidative stress testing, inflammation biomarker testing, and DNA methylation testing. Telomere testing holds the largest market share due to its role in determining biological age, a key concern in preventive health and anti-aging treatments. Companies such as Life Length and Quest Diagnostics offer telomere testing, which has gained traction among individuals seeking to monitor their cellular health as part of longevity programs.

By Region: The cellular health screening market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest market share, driven by a well-established healthcare system and significant investment in advanced diagnostics. The presence of major players such as Quest Diagnostics and Labcorp further boosts the regions dominance. In Asia-Pacific, countries like Japan and South Korea are experiencing rapid growth due to rising awareness of personalized medicine and preventive healthcare.

Global Cellular Health Screening Market Competitive Landscape

The global cellular health screening market is moderately consolidated, with key players focusing on research and development to improve the accuracy and accessibility of screening tools. Major companies such as Telomere Diagnostics, SpectraCell Laboratories, and Genova Diagnostics dominate the market. The competitive landscape is further strengthened by the increasing demand for personalized medicine and preventive healthcare solutions. Collaborations with healthcare providers, government initiatives promoting preventive health, and the introduction of cost-effective screening solutions are major factors driving competition in the market.

|

Company Name |

Establishment Year |

Headquarters |

Product Portfolio |

R&D Investments |

Geographic Presence |

Partnerships |

Revenue (2023) |

Employees |

|

Telomere Diagnostics |

2010 |

Menlo Park, USA |

Telomere Testing |

- |

- |

- |

- |

- |

|

SpectraCell Laboratories |

1993 |

Houston, USA |

Nutritional Testing |

- |

- |

- |

- |

- |

|

Genova Diagnostics |

1986 |

Asheville, USA |

Biomarker Testing |

- |

- |

- |

- |

- |

|

Life Length |

2011 |

Madrid, Spain |

Telomere Testing |

- |

- |

- |

- |

- |

|

Quest Diagnostics |

1967 |

Secaucus, USA |

Comprehensive Testing |

- |

- |

- |

- |

- |

Global Cellular Health Screening Market Analysis

Global Cellular Health Screening Market Growth Drivers

- Technological Advancements: Technological advancements are reshaping cellular health screening, with breakthroughs in AI and molecular diagnostics making tests faster and more accurate. In 2024, approximately of the world's health diagnostics incorporated AI for precise results, as reported by the World Health Organization (WHO). Real-time analysis capabilities have significantly improved diagnostic workflows, reducing the time to obtain results from several days to a few hours. AI-driven diagnostics are predicted to analyze over 1.5 billion health records by the end of the year, enhancing personalized treatments based on cellular health patterns.

- Personalized Medicine Demand: Demand for personalized medicine continues to grow due to increased consumer awareness and advancements in genomics. According to the National Institutes of Health (NIH), over 4 million individuals have undergone genetic testing in the U.S. as part of personalized treatment plans as of 2024. The NIH also states that of healthcare professionals consider cellular health as a key factor in customizing patient therapies, particularly for cancer treatments and chronic conditions. This rise has been pivotal in driving the cellular health screening market.

- Rising Geriatric Population: In 2024, the United Nations reports that there are over 1.4 billion people aged 60 years and older globally, driving demand for healthcare services including cellular health screenings. The geriatric population is expected to reach 2.1 billion by 2050, increasing the burden on health systems to deliver efficient, personalized healthcare. Age-related cellular degradation, such as the shortening of telomeres and mitochondrial dysfunction, is closely monitored through these screenings, enhancing proactive healthcare for the aging population.

Global Cellular Health Screening Market Challenges

- High Testing Costs: The cost of cellular health screening remains a barrier, particularly in lower-income countries. In 2023, the average cost for advanced molecular tests exceeds $1,500 in developed countries, according to the World Bank. This makes it inaccessible to a large portion of the population, particularly in regions like Sub-Saharan Africa, where the average annual income per capita is around $1,600. The disparity in affordability significantly hinders market growth and adoption rates in underserved areas.

- Regulatory Hurdles: Stringent regulatory frameworks and compliance requirements are challenges to market expansion. The U.S. Food and Drug Administration (FDA) has tightened regulations on cellular health screenings, with more than of submissions in 2023 being delayed due to non-compliance issues. Similarly, in the European Union, cellular health tests must comply with the In Vitro Diagnostic Regulation (IVDR), increasing the time to market for new technologies by 18 months on average.

- Data Privacy Concerns: Data privacy is a major concern, especially with the integration of AI in cellular health screenings. According to a report by the International Telecommunication Union (ITU), over 100 million health records were compromised globally in 2023. Governments have responded with stricter data protection laws; for instance, the General Data Protection Regulation (GDPR) in Europe enforces hefty penalties, with fines up to €20 million for non-compliance. Such regulatory requirements add complexity and cost for companies operating in this market.

Global Cellular Health Screening Market Future Outlook

Over the next five years, the global cellular health screening market is expected to experience significant growth, driven by increased adoption of personalized medicine and the growing emphasis on preventive healthcare. Technological advancements in testing methodologies and the integration of AI for predictive diagnostics will also propel market growth. Additionally, collaborations between biotech companies and healthcare providers will enhance the accessibility and affordability of these tests.

Market Opportunities:

- Advancements in AI-Driven Diagnostics: AI-driven diagnostics have transformed cellular health screening by improving test accuracy and efficiency. In 2023, AI systems assisted in over 600 million diagnostic tests worldwide, with predictions to double by 2025 as AI becomes more integral in laboratory settings, according to WHO. This represents a vast opportunity for companies to integrate AI tools that accelerate cellular health diagnostics, particularly in high-demand markets such as North America and Europe.

- Increased Adoption of Preventive Healthcare: Preventive healthcare is witnessing a surge globally, with governments allocating resources to promote early detection. The World Bank notes that $180 billion was invested globally in preventive health initiatives in 2024, encouraging a shift toward cellular health screening. This trend is particularly evident in Asia-Pacific, where countries like Japan and South Korea have integrated cellular health as part of national health checks, presenting lucrative opportunities for screening providers.

Scope of the Report

|

By Product Type |

Telomere Testing Oxidative Stress Testing Inflammation Biomarker Testing DNA Methylation Testing |

|

By Sample Type |

|

|

By Application |

Preventive Healthcare Chronic Disease Monitoring Personalized Medicine |

|

By Technology |

ELISA Flow Cytometry PCR Mass Spectrometry |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Cellular health screening test providers

Diagnostic laboratories

Biotechnology firms

Pharmaceutical companies

Investments and venture capitalist firms

Government and regulatory bodies (e.g., FDA, EMA)

Private health insurance companies

Research and development institutions

Companies

Players Mention in the Report

Telomere Diagnostics

SpectraCell Laboratories

Genova Diagnostics

Life Length

Quest Diagnostics

LabCorp

Cell Science Systems

OmegaQuant

InsideTracker

Everlywell

Thorne HealthTech

Immune Health Diagnostics

BiogeniQ

Chronomics

Zymo Research

Table of Contents

01. Global Cellular Health Screening Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02. Global Cellular Health Screening Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. Global Cellular Health Screening Market Analysis

3.1. Growth Drivers (Technological advancements, Personalized medicine demand, Rising geriatric population, Increasing healthcare awareness)

3.2. Market Challenges (High testing costs, Regulatory hurdles, Data privacy concerns)

3.3. Opportunities (Advancements in AI-driven diagnostics, Increased adoption of preventive healthcare, Government health initiatives)

3.4. Trends (Integration of AI and IoT, Expansion of telemedicine, Rising preference for at-home health screening)

3.5. Government Regulations (FDA approvals, International cellular health standards, Data compliance)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Diagnostic labs, Healthcare providers, Tech enablers, Test kit manufacturers)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

04. Global Cellular Health Screening Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Telomere Testing

4.1.2. Oxidative Stress Testing

4.1.3. Inflammation Biomarker Testing

4.1.4. DNA Methylation Testing

4.2. By Sample Type (In Value %)

4.2.1. Blood Samples

4.2.2. Saliva Samples

4.2.3. Urine Samples

4.3. By Application (In Value %)

4.3.1. Preventive Healthcare

4.3.2. Chronic Disease Monitoring

4.3.3. Personalized Medicine

4.4. By Technology (In Value %)

4.4.1. ELISA

4.4.2. Flow Cytometry

4.4.3. PCR

4.4.4. Mass Spectrometry

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. Global Cellular Health Screening Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Telomere Diagnostics

5.1.2. SpectraCell Laboratories

5.1.3. Genova Diagnostics

5.1.4. Life Length

5.1.5. Quest Diagnostics

5.1.6. LabCorp

5.1.7. Cell Science Systems

5.1.8. OmegaQuant

5.1.9. InsideTracker

5.1.10. Everlywell

5.1.11. Thorne HealthTech

5.1.12. Immune Health Diagnostics

5.1.13. BiogeniQ

5.1.14. Chronomics

5.1.15. Zymo Research

5.2. Cross Comparison Parameters (Market Revenue, Product Portfolio, Technological Expertise, Geographic Footprint, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

06. Global Cellular Health Screening Market Regulatory Framework

6.1. International Testing Standards

6.2. Data Privacy and Compliance (HIPAA, GDPR)

6.3. FDA and EU Regulations

6.4. Certifications and Quality Control

07. Global Cellular Health Screening Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08. Global Cellular Health Screening Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Sample Type (In Value %)

8.3. By Application (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

09. Global Cellular Health Screening Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing and Distribution Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping the entire cellular health screening market ecosystem. This includes identifying the key stakeholders such as diagnostic labs, healthcare providers, and biotech firms. Extensive secondary research is conducted using proprietary databases, government health reports, and industry publications to outline critical market drivers and challenges.

Step 2: Market Analysis and Construction

In this phase, historical data on market size, revenue generation, and market penetration are compiled and analyzed. The market analysis includes an assessment of testing adoption rates and geographical analysis, which serves as the foundation for future market projections.

Step 3: Hypothesis Validation and Expert Consultation

The hypotheses developed in the previous steps are validated through interviews with industry experts, cellular health test manufacturers, and healthcare providers. The insights collected are used to refine the market estimates and forecasts.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all the collected data and insights into a comprehensive market analysis. This includes validation from key cellular health screening providers, ensuring the accuracy of market projections and key findings.

Frequently Asked Questions

01. How big is the Global Cellular Health Screening Market?

The global cellular health screening market is valued at USD 2.5 billion. This growth is attributed to the rising demand for preventive healthcare and advancements in cellular testing technologies.

02. What are the challenges in the Global Cellular Health Screening Market?

The primary challenges include the high cost of tests, regulatory hurdles surrounding medical testing, and concerns about data privacy, particularly with the increasing use of AI-driven diagnostics.

03. Who are the major players in the Global Cellular Health Screening Market?

Key players in the market include Telomere Diagnostics, SpectraCell Laboratories, Genova Diagnostics, Life Length, and Quest Diagnostics. These companies dominate the market due to their extensive testing portfolios and geographic reach.

04. What are the growth drivers of the Global Cellular Health Screening Market?

The market is driven by increasing consumer awareness of preventive healthcare, the rise in chronic disease incidences, and advancements in cellular health testing technologies. The growing interest in personalized medicine also contributes to market expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.