Global Cloud TV Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD1130

Region:Global

Author(s):Shreya Garg

Product Code:KROD1130

November 2024

91

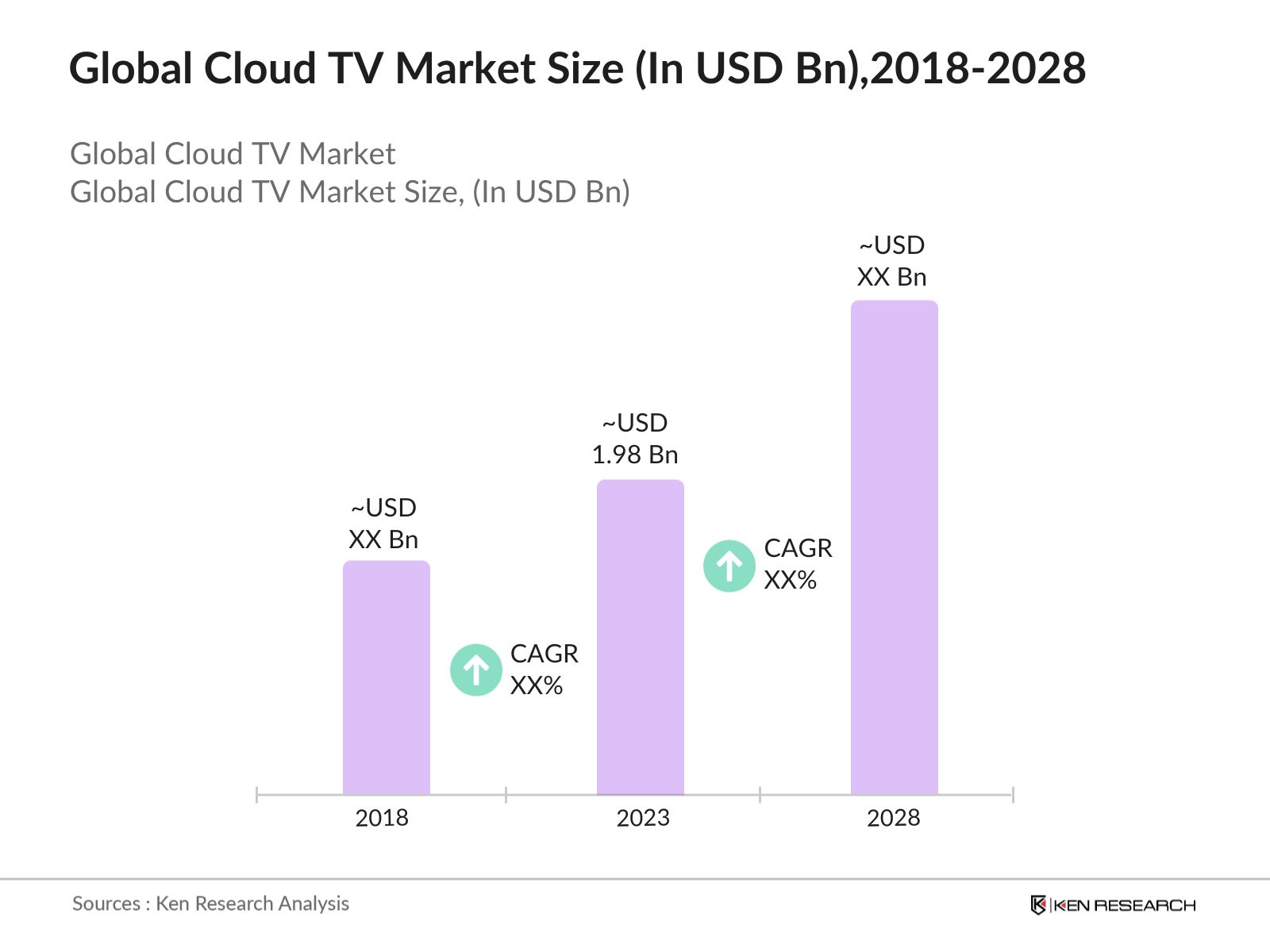

The global Cloud TV market was valued at USD 1.98 Billion in 2023, primarily driven by the growing demand for over-the-top (OTT) content and advancements in cloud computing technologies. The proliferation of smart devices, coupled with rising internet penetration, played a crucial role in accelerating the adoption of Cloud TV services. Content providers are increasingly shifting to cloud-based solutions for their scalability, cost-efficiency, and flexibility, which has further fueled the market's growth.

Several key players dominate the global Cloud TV market, leveraging cloud technologies to offer innovative solutions. Major players include Kaltura, Comcast Technology Solutions, Brightcove, Synamedia, and Ateme. These companies are continuously investing in research and development to enhance their Cloud TV platforms, offering enhanced video quality, personalization, and user experience.

In 2023, Kaltura's collaboration with Bouygues Telecom in France, where Kaltura's technology is being utilized to power a next-generation IPTV and OTT digital TV service. This partnership is expected to enhance Bouygues Telecom's offerings by migrating to a cloud-based operation, providing features like content management and improved user experiences.

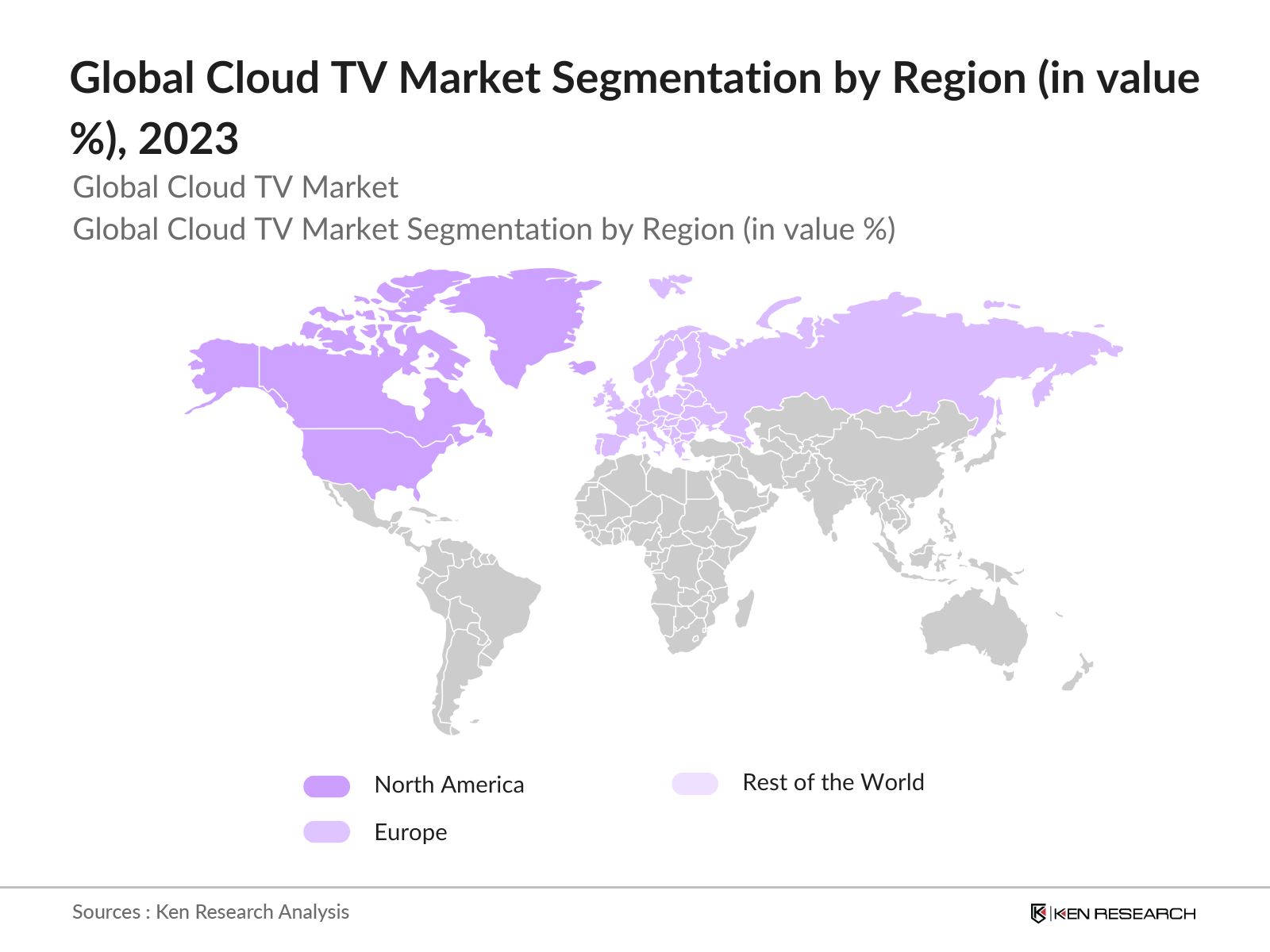

United States, dominates the global market share in 2023. This dominance is attributed to the widespread availability of high-speed internet and the strong presence of key Cloud TV players like Comcast and Kaltura. Additionally, the regions early adoption of OTT services, coupled with consumer preference for personalized content, has solidified its leadership in the market.

The Cloud TV market is segmented by various factors such as product type, deployment type, region etc.

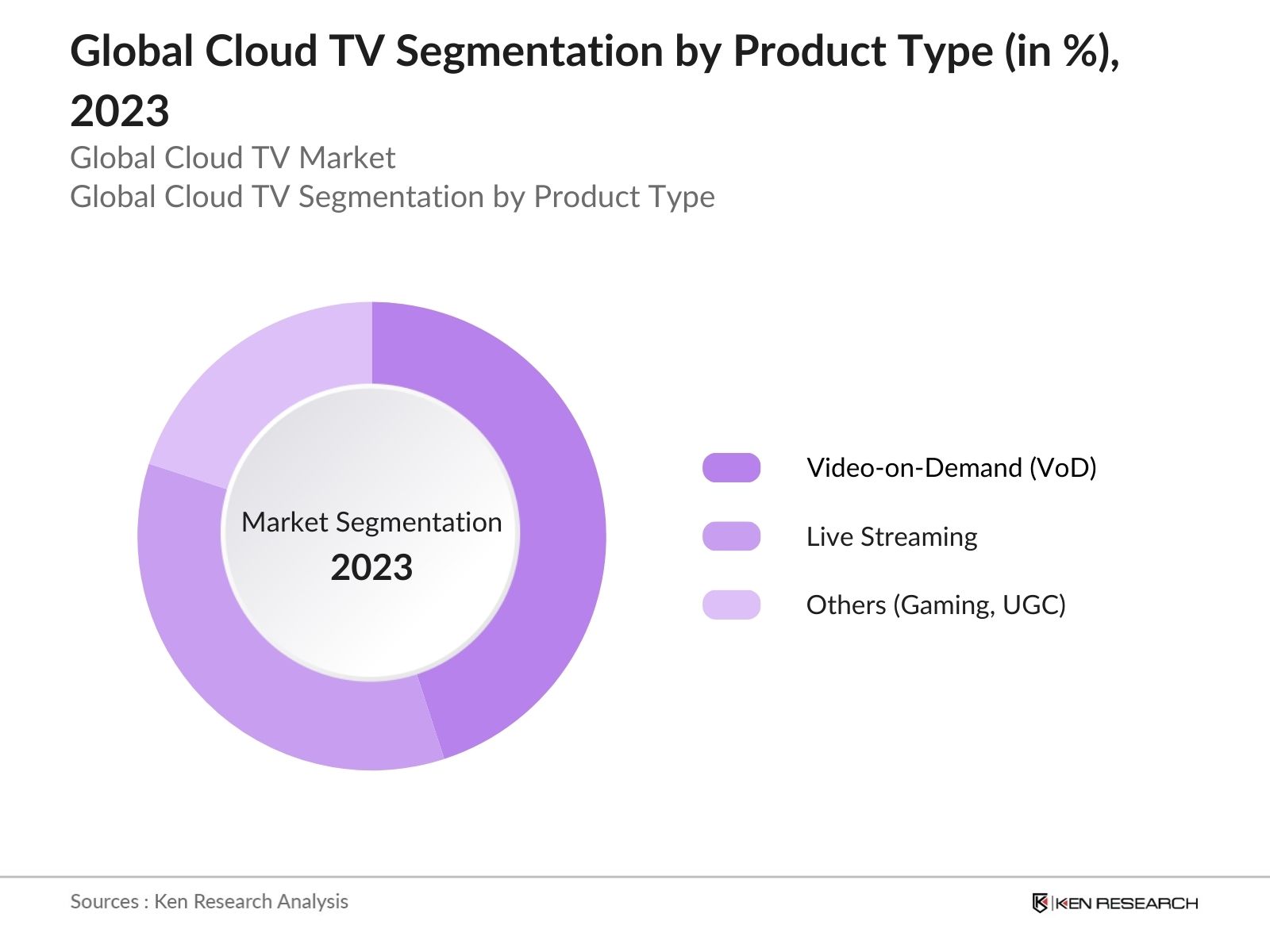

By Product Type: The market is segmented by product type into live streaming, video-on-demand (VoD), and others (gaming, user-generated content). In 2023, video-on-demand held a dominant market share, primarily due to the increasing consumer demand for flexible viewing options and the growing popularity of platforms like Netflix and Amazon Prime. VoD services allow users to watch content at their convenience, making it the most preferred segment among consumers globally.

By Deployment Mode: By deployment mode, the market is segmented into public cloud, private cloud, and hybrid cloud. In 2023, the hybrid cloud segment dominated with a market share, driven by its ability to offer the scalability of the public cloud while maintaining the security and privacy of a private cloud. Hybrid cloud solutions are particularly popular among broadcasters and OTT service providers, allowing them to manage large volumes of content efficiently while adhering to data protection regulations.

By Region: The market is segmented into North America, South America, Europe, APAC, and MEA. In 2023, North America led the dominant market share, driven by high internet penetration rates and early adoption of Cloud TV solutions. The region is home to several major Cloud TV service providers, such as Comcast and Brightcove, which further contributes to its market dominance.

|

Company Name |

Establishment Year |

Headquarters |

|---|---|---|

|

Kaltura |

2006 |

New York, USA |

|

Comcast Technology Solutions |

1963 |

Philadelphia, USA |

|

Brightcove |

2004 |

Boston, USA |

|

Synamedia |

2018 |

London, UK |

|

Ateme |

1991 |

Vlizy-Villacoublay, France |

The global Cloud TV market is projected to grow exponentially by 2028, driven by the growing demand for video streaming services, advancements in AI-powered content recommendation engines, and increased focus on delivering personalized content experiences. The rise in smart home adoption and 5G technology rollouts will further enhance streaming quality and reduce latency, fostering market growth.

|

By Product Type |

Live Streaming Video-On-Demand (Vod) Others (Gaming, User-Generated Content) |

|

By Deployment Mode |

Public Cloud Private Cloud Hybrid Cloud |

|

By Region |

North America South America Europe APAC MEA |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Demand for Streaming Services

3.1.2. Expansion of High-Speed Internet Networks

3.1.3. Shift Towards Personalized Viewing

3.1.4. Increase in Digital Content Production

3.2. Restraints

3.2.1. Data Privacy and Security Concerns

3.2.2. High Operational Costs

3.2.3. Infrastructure Gaps in Emerging Markets

3.2.4. Content Licensing Challenges

3.3. Opportunities

3.3.1. AI-Powered Content Recommendation

3.3.2. Expansion into Emerging Markets

3.3.3. Partnerships with Content Creators

3.3.4. Growth in 8K Streaming Adoption

3.4. Trends

3.4.1. Rise in Hybrid Cloud Deployments

3.4.2. Use of Machine Learning for Content Optimization

3.4.3. Integration with Smart TV Technology

3.4.4. Increasing Focus on Localized Content

3.5. Government Initiatives

3.5.1. 5G Infrastructure Investments

3.5.2. EU Digital Strategy for Cloud Adoption

3.5.3. Chinas National Digital Infrastructure Plan

3.5.4. Indias BharatNet Connectivity Initiative

3.6. SWOT Analysis

3.7. Ecosystem Stakeholders

3.8. Competitive Ecosystem

4.1. By Product Type (in Value %)

4.1.1. Video-on-Demand (VoD)

4.1.2. Live Streaming

4.1.3. Gaming and User-Generated Content

4.2. By Deployment Mode (in Value %)

4.2.1. Public Cloud

4.2.2. Private Cloud

4.2.3. Hybrid Cloud

4.3. By Region (in Value %)

4.3.1. North America

4.3.2. Europe

4.3.3. APAC

4.3.4. South America

4.3.5. Middle East & Africa (MEA)

5.1. Detailed Profiles of Major Companies

5.1.1. Kaltura

5.1.2. Comcast Technology Solutions

5.1.3. Brightcove

5.1.4. Synamedia

5.1.5. Ateme

5.2. Cross-Comparison of Key Players

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. Year of Establishment

5.2.4. Revenue

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.4.1. Mergers and Acquisitions

5.4.2. Partnerships and Collaborations

5.5. Investment Analysis

5.5.1. Venture Capital Funding

5.5.2. Government Grants

5.5.3. Private Equity Investments

6.1. Data Privacy and Compliance

6.2. Certification Standards

6.3. Cybersecurity Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (in Value %)

8.2. By Deployment Mode (in Value %)

8.3. By Region (in Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing and Positioning Initiatives

9.4. White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Global Cloud TV industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different Cloud TV companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple Cloud TV companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such Cloud TV companies.

The Global Cloud TV market was valued at USD 1.98 billion in 2023, driven by increasing demand for streaming services, rising internet penetration, and the growing adoption of cloud-based technologies.

Challenges in the global Cloud TV Market include data privacy and security concerns, high operational costs, infrastructure gaps in emerging markets, and content licensing and distribution issues that limit global reach.

Key players in the global Cloud TV market include Kaltura, Comcast Technology Solutions, Brightcove, Synamedia, and Ateme. These companies dominate due to their innovative cloud TV solutions, strategic partnerships, and strong presence in both developed and emerging markets.

The market is driven by the rising demand for streaming services across multiple devices, the expansion of high-speed internet networks globally, a shift toward personalized content viewing, and the increased production of digital content for cloud platforms.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.