Global Computer Vision Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD5007

Region:Global

Author(s):Shivani Mehra

Product Code:KROD5007

November 2024

98

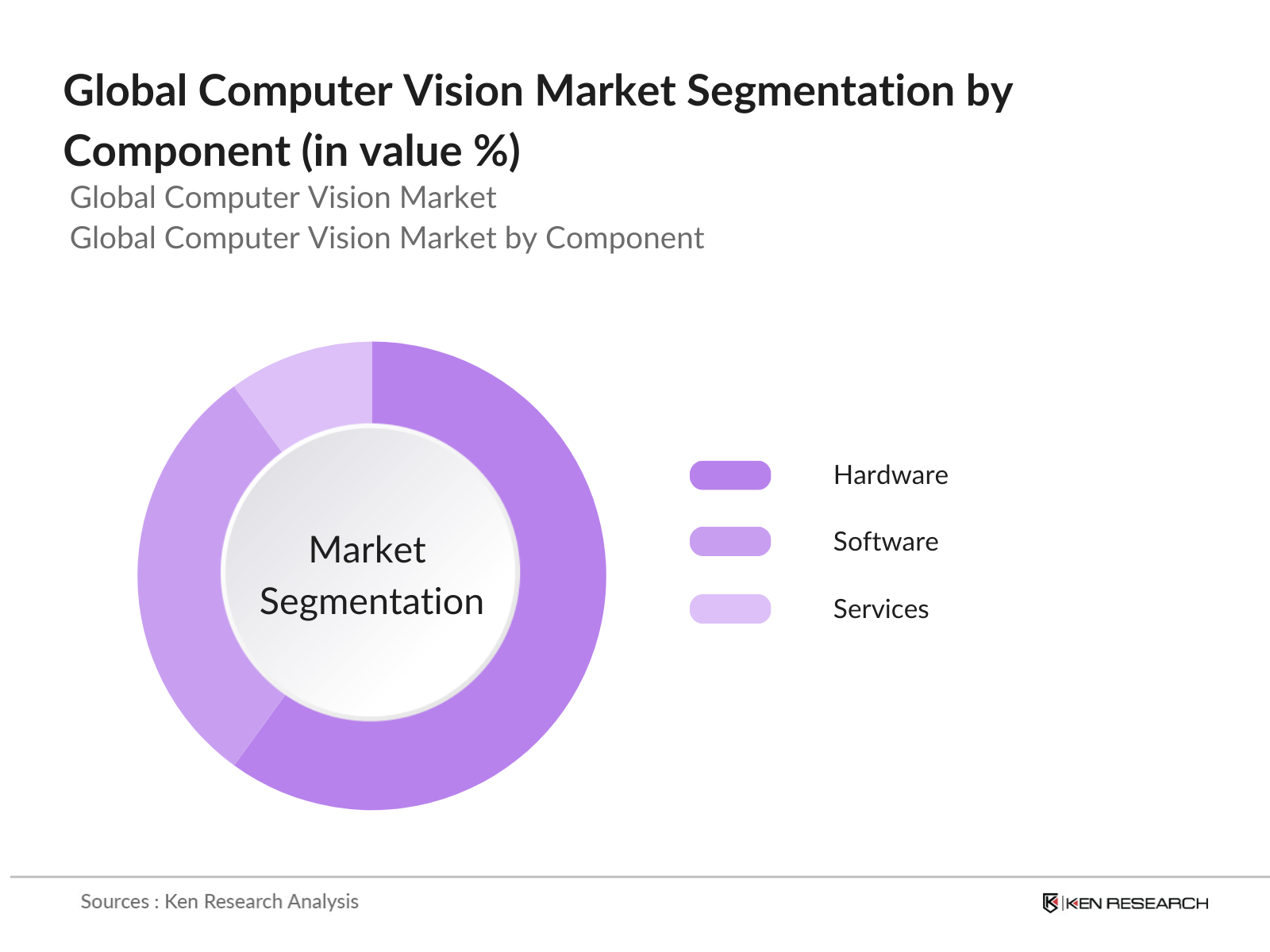

By Component: The global computer vision market is segmented by component into hardware, software, and services. Hardware dominates the market, driven by the increasing use of high-resolution cameras, sensors, and processors in applications such as quality inspection in manufacturing and autonomous driving. The demand for advanced image sensors and AI processors has grown significantly, especially in automotive and industrial automation sectors, where precision and speed are critical.

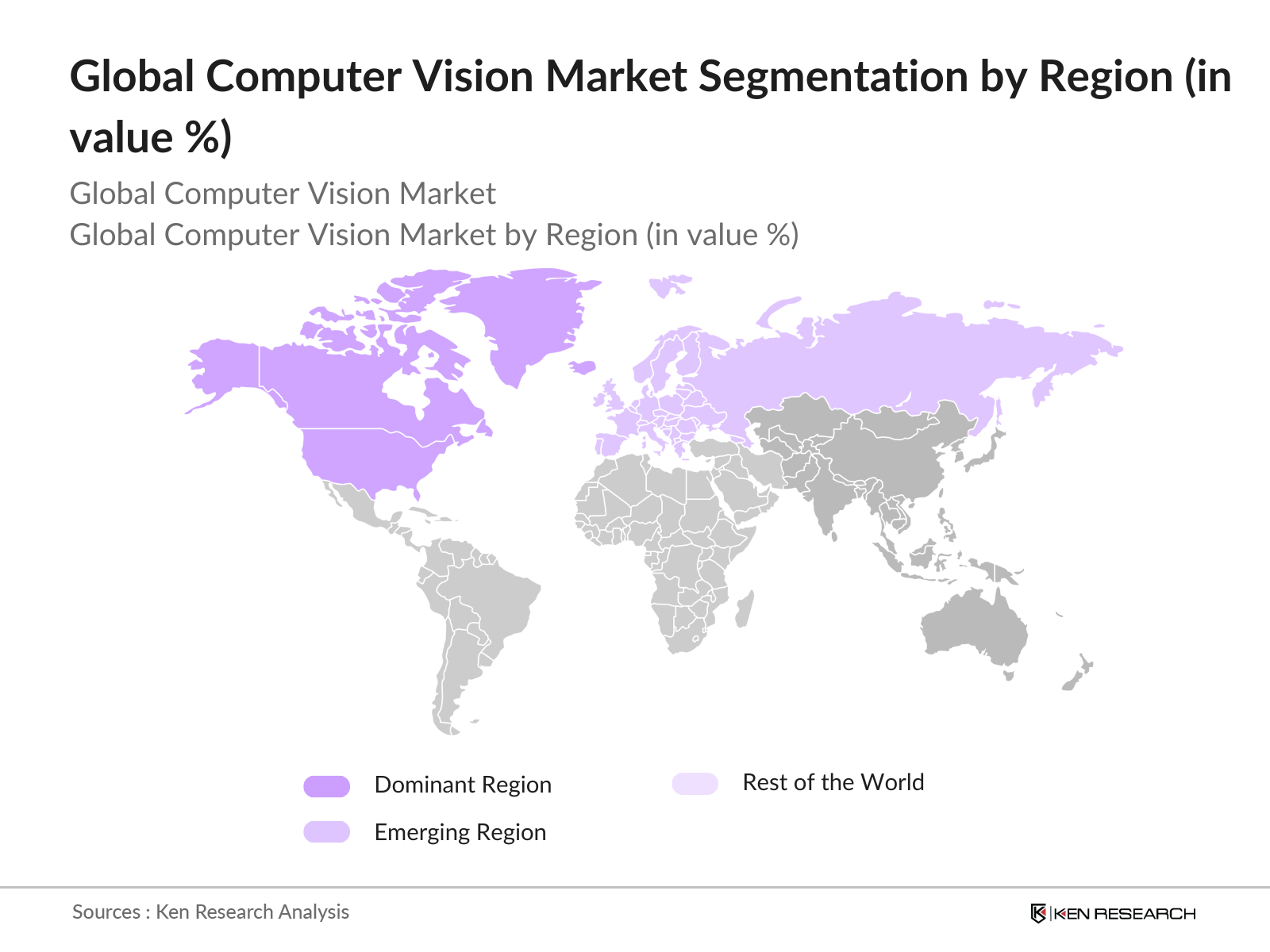

By Region: The global computer vision market is segmented by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. North America leads the market due to strong technology adoption, investments in AI, and the presence of leading market players. Asia-Pacific is the fastest-growing region, driven by rapid industrialization, especially in countries like China and Japan, where there is a significant demand for automation in manufacturing.

The global computer vision market is dominated by several major players, with companies focusing on product innovation, mergers, and acquisitions to maintain their market positions. These companies invest heavily in research and development to enhance their AI capabilities and offer better computer vision solutions for industries like healthcare, automotive, and industrial automation. The competitive landscape is also shaped by strategic partnerships and collaborations between technology firms and end-user industries.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Employees |

Product Specialization |

Regional Presence |

R&D Investment |

Innovation Index |

Strategic Partnerships |

|

Intel Corporation |

1968 |

Santa Clara, USA |

- |

- |

- |

- |

- |

- |

- |

|

Nvidia Corporation |

1993 |

Santa Clara, USA |

- |

- |

- |

- |

- |

- |

- |

|

Cognex Corporation |

1981 |

Natick, USA |

- |

- |

- |

- |

- |

- |

- |

|

Basler AG |

1988 |

Ahrensburg, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Sony Corporation |

1946 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

- |

Over the next five years, the global computer vision market is expected to show significant growth, driven by continuous advancements in artificial intelligence, rising demand for automation across various industries, and the increasing application of computer vision in sectors such as healthcare, automotive, and retail. The integration of computer vision with emerging technologies such as IoT and edge computing will further accelerate the market's growth trajectory.

|

By Component |

Hardware (Cameras, Sensors, Processors) Software (Machine Learning, AI Algorithms) Services (Integration, Maintenance) |

|

By Application |

Industrial Healthcare Retail Automotive Consumer Electronics |

|

By Technology |

2D Computer Vision 3D Computer Vision Deep Learning Edge Computing |

|

By End-User |

Automotive Healthcare Retail Manufacturing Security & Surveillance |

|

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increase in AI and Deep Learning Adoption (Technology Adoption)

3.1.2. Surge in Demand for Automation Across Industries (Industrial Demand)

3.1.3. Advancements in Image Sensors and Processor Technologies (Hardware Innovation)

3.1.4. Rising Demand in Consumer Electronics (End-User Market Growth)

3.2. Market Challenges

3.2.1. High Initial Investment Costs (Cost Barriers)

3.2.2. Data Privacy and Security Concerns (Regulatory Challenges)

3.2.3. Complex Implementation in Dynamic Environments (Technical Challenges)

3.3. Opportunities

3.3.1. Integration with IoT and Edge Computing (Technology Convergence)

3.3.2. Emerging Markets in Asia-Pacific and Latin America (Geographical Opportunities)

3.3.3. Growth in Autonomous Vehicles and Robotics (Application Segments Expansion)

3.4. Trends

3.4.1. Growth in 3D Computer Vision and AR/VR Applications (Emerging Technologies)

3.4.2. Expansion of Cloud-Based Solutions (Cloud Computing Integration)

3.4.3. Adoption in Healthcare for Diagnostic Imaging (Sector-Specific Trend)

3.5. Government Regulation

3.5.1. Data Protection Laws for Image and Video Data (Data Protection Compliance)

3.5.2. Standardization of AI and Vision Algorithms (Industry Standardization)

3.5.3. Government-Funded Research Initiatives (R&D Incentives)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Component (In Value %)

4.1.1. Hardware (Cameras, Sensors, Processors)

4.1.2. Software (Machine Learning, AI Algorithms, Imaging Tools)

4.1.3. Services (Integration, Maintenance, Consulting)

4.2. By Application (In Value %)

4.2.1. Industrial (Manufacturing, Automation, Quality Control)

4.2.2. Healthcare (Medical Imaging, Diagnostics, Surgery Assistance)

4.2.3. Retail (Customer Insights, Surveillance, Inventory Management)

4.2.4. Automotive (ADAS, Autonomous Vehicles, Traffic Monitoring)

4.2.5. Consumer Electronics (Smartphones, Drones, Gaming)

4.3. By Technology (In Value %)

4.3.1. 2D Computer Vision

4.3.2. 3D Computer Vision

4.3.3. Deep Learning

4.3.4. Edge Computing

4.4. By End-User (In Value %)

4.4.1. Automotive

4.4.2. Healthcare

4.4.3. Retail

4.4.4. Manufacturing

4.4.5. Security & Surveillance

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. Intel Corporation

5.1.2. Nvidia Corporation

5.1.3. Cognex Corporation

5.1.4. Basler AG

5.1.5. Teledyne Technologies Incorporated

5.1.6. Sony Corporation

5.1.7. Keyence Corporation

5.1.8. National Instruments Corporation

5.1.9. Omron Corporation

5.1.10. Qualcomm Technologies, Inc.

5.1.11. Microsoft Corporation

5.1.12. Xilinx, Inc.

5.1.13. Hikvision Digital Technology Co., Ltd.

5.1.14. Zebra Technologies Corporation

5.1.15. FLIR Systems, Inc.

5.2. Cross Comparison Parameters (Revenue, Number of Employees, Technology Specialization, R&D Investment, Regional Presence, Market Share, Innovation Index, Product Portfolio Diversity)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6.1. AI and Vision Systems Compliance Requirements

6.2. Data Privacy and Security Regulations

6.3. Certification and Industry Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Component (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Key Customer Cohorts and Behavioral Insights

9.3. Future Investment Areas

9.4. White Space Opportunity Analysis

The initial phase involves identifying major stakeholders in the global computer vision market. This is done through extensive desk research using proprietary databases and secondary sources. The objective is to define the key variables affecting market dynamics, including technological advancements and industry adoption.

Historical data is analyzed to understand market growth trends. This includes evaluating the penetration of computer vision in various industries and its adoption rates. Service quality statistics and product sales data are incorporated to estimate market revenues.

To validate the data, interviews are conducted with industry experts from key companies. This provides insights into operational challenges, financial performance, and emerging trends. These consultations help refine and verify the market hypotheses.

In the final step, data from manufacturers is combined with insights from industry experts. This ensures that the bottom-up analysis is comprehensive and accurate, covering all relevant aspects of the global computer vision market.

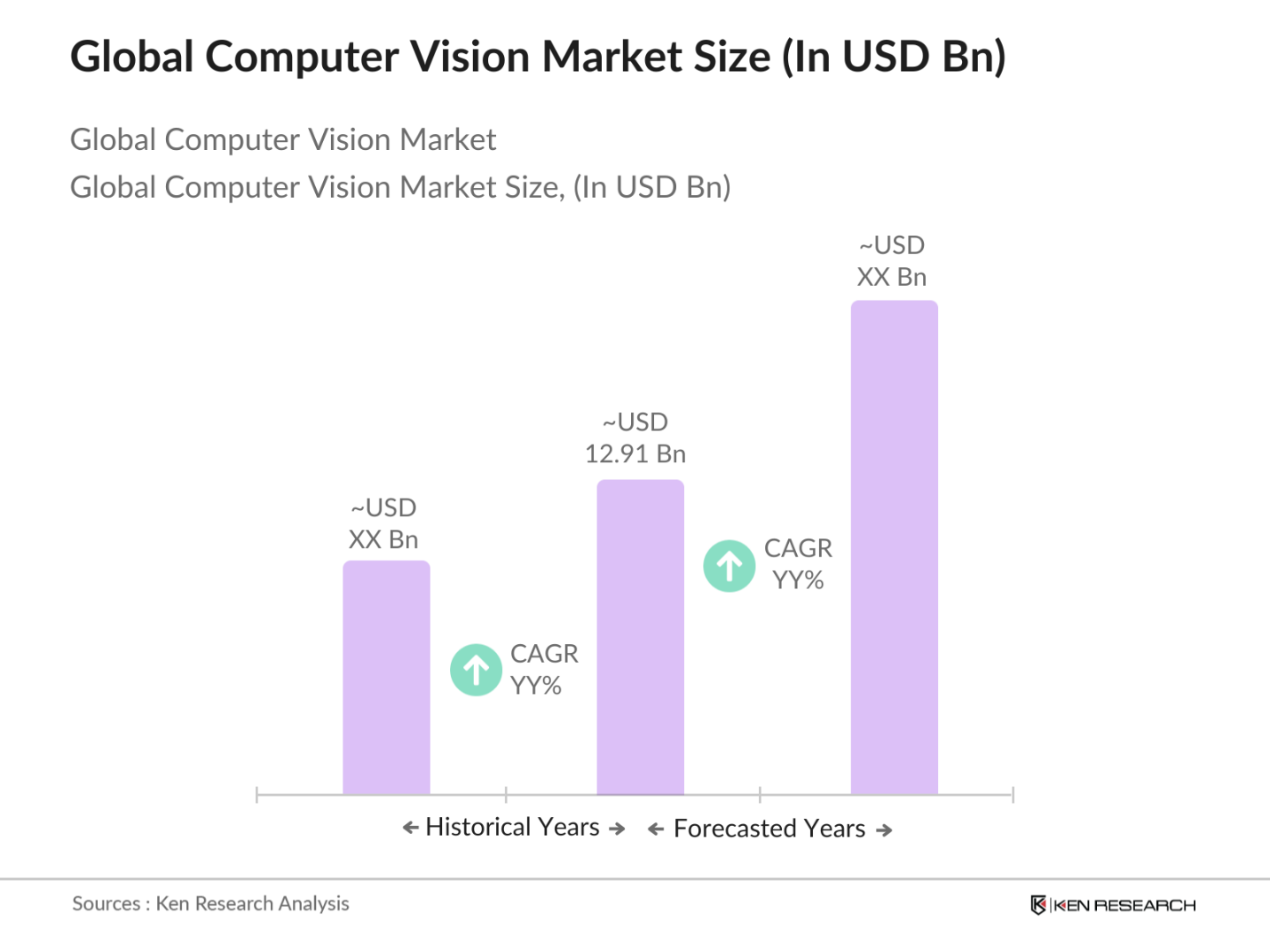

The global computer vision market is valued at USD 12.91 billion, driven by the growing adoption of AI and machine learning technologies across industries such as manufacturing, healthcare, and automotive.

Challenges include high initial investment costs, data privacy concerns, and technical issues related to implementing computer vision systems in dynamic environments, especially in sectors like healthcare and automotive.

Key players in the market include Intel Corporation, Nvidia Corporation, Cognex Corporation, Basler AG, and Sony Corporation. These companies dominate the market due to their technological advancements, strong R&D investments, and global presence.

Growth drivers include the increasing demand for automation, advancements in AI and deep learning technologies, and the rise of autonomous vehicles and healthcare imaging applications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.