Global Contract Research Organization (CRO) Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD5077

November 2024

86

About the Report

Global Contract Research Organization (CRO) Market Overview

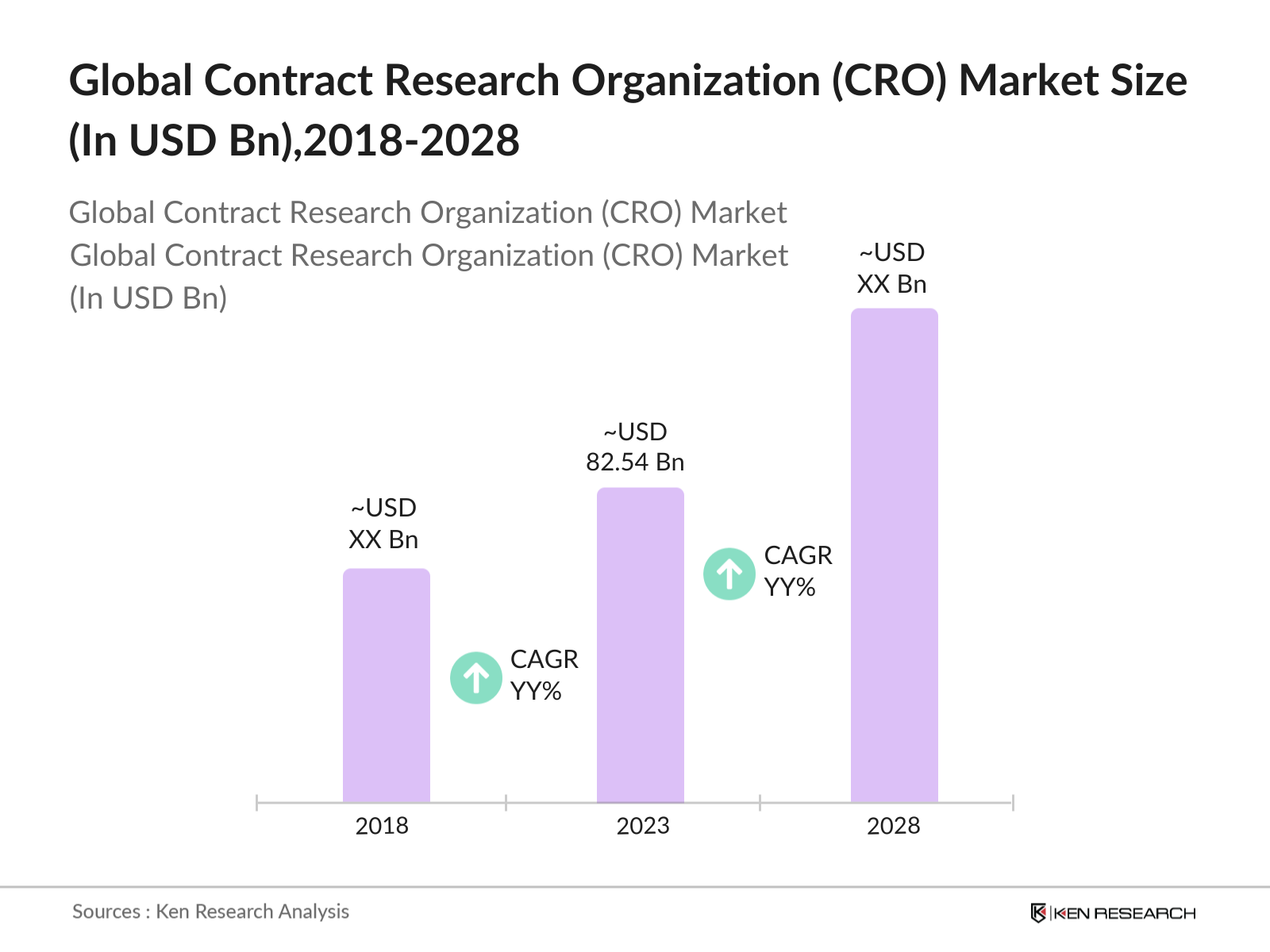

- The global contract research organization (CRO) market was valued at approximately USD 82.54 billion in 2023. This market growth is primarily driven by the increasing R&D investments by pharmaceutical and biotechnology companies. The demand for outsourcing clinical trials has surged due to the rising number of drug approvals and complex clinical studies. Furthermore, the rise of precision medicine and biologics contributes to the expansion of the CRO market.

- Prominent players in the global CRO market include IQVIA, Syneos Health, PPD, PRA Health Sciences, and Charles River Laboratories. These companies have dominated the market by offering comprehensive clinical trial services, laboratory services, and consulting services for pharmaceutical and biotechnology companies. Their established global presence, robust expertise in regulatory compliance, and innovative clinical trial management solutions provide them with a competitive edge in the market.

- In July 2023, IQVIA announced the expansion of its global genomic testing services in collaboration with several biotech companies. This strategic expansion will enable IQVIA to offer more extensive services in precision medicine and personalized therapies, addressing the increasing demand for targeted treatments in oncology. This development enhances the company's service offerings and strengthens its position in the global CRO market.

- Cities like Boston, London, and Singapore dominate the global CRO market due to their strategic advantages and robust ecosystems. Boston is a hub for top pharmaceutical companies and research institutes, ensuring a consistent demand for CRO services. London, benefiting from its regulatory advantages post-Brexit, houses major CROs that thrive in this competitive landscape. Singapore has emerged as a key player in the Asia-Pacific region, providing strong regulatory support and a skilled workforce, making it an attractive destination for CRO services.

Global Contract Research Organization (CRO) Market Segmentation

The Global Contract Research Organization (CRO) Market is divided into the following segments:

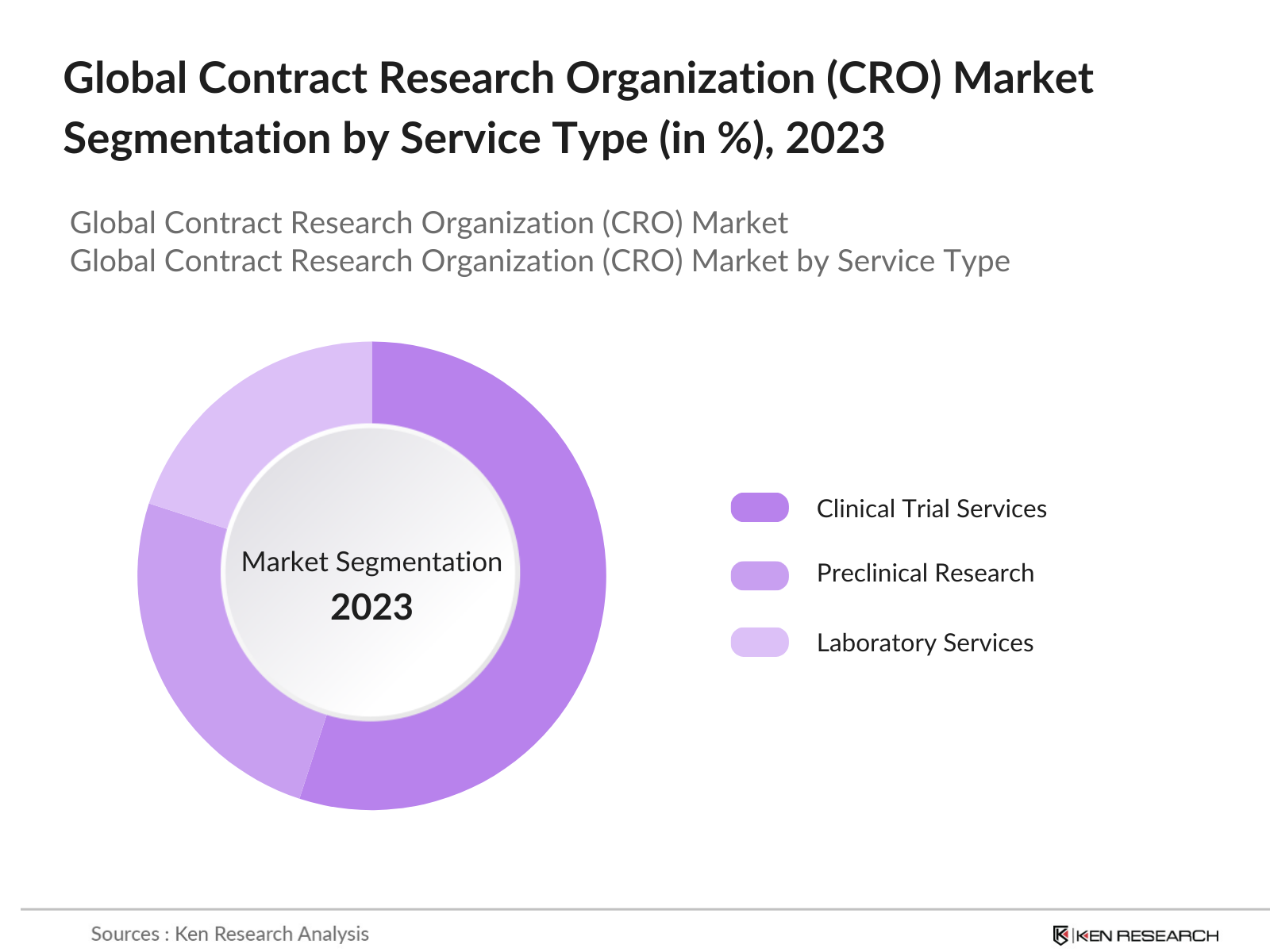

By Service Type: The global contract research organization market is segmented by service type into clinical trial services, preclinical research services, and laboratory services. In 2023, clinical trial services held the largest market share, driven by the increasing demand for Phase I-IV clinical trials globally. The rise in drug approvals and the need for global multi-center trials have led pharmaceutical companies to outsource their trials to CROs. This outsourcing trend has been strengthened by the need for CROs to manage complex regulatory frameworks and ensure patient recruitment compliance.

By Region: The global CRO market is segmented by region into North America, Europe, Asia-Pacific (APAC), Latin America, and the Middle East & Africa (MEA). In 2023, North America held the largest market share, driven by the high concentration of pharmaceutical companies, advanced healthcare infrastructure, and strong government support for clinical trials. The U.S., in particular, dominates due to a large number of FDA-approved drug trials and the presence of key players like IQVIA and PPD. Europe follows closely, with rising investments in biopharma R&D. APAC, led by China and India, is emerging due to its lower trial costs and vast patient pool.

By End-User: The contract research organization market is segmented by end-user into pharmaceutical companies, biotechnology companies, and medical device companies. In 2023, pharmaceutical companies dominated the market, accounting for the largest share of CRO demand. This is due to the increased outsourcing of clinical trials, which allows pharmaceutical companies to focus on their core R&D activities while leveraging CROs' expertise in regulatory compliance, patient recruitment, and clinical data management. Biotechnology companies have also increased their reliance on CROs, especially for novel biologics and gene therapies.

By Region: The global CRO market is segmented by region into North America, Europe, Asia-Pacific (APAC), Latin America, and the Middle East & Africa (MEA). In 2023, North America held the largest market share, driven by the high concentration of pharmaceutical companies, advanced healthcare infrastructure, and strong government support for clinical trials. The U.S., in particular, dominates due to a large number of FDA-approved drug trials and the presence of key players like IQVIA and PPD. Europe follows closely, with rising investments in biopharma R&D. APAC, led by China and India, is emerging due to its lower trial costs and vast patient pool.

Global Contract Research Organization (CRO) Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|

IQVIA |

1982 |

Durham, North Carolina, USA |

|

Syneos Health |

2017 |

Morrisville, North Carolina, USA |

|

PPD |

1985 |

Wilmington, North Carolina, USA |

|

PRA Health Sciences |

1976 |

Raleigh, North Carolina, USA |

|

Charles River Laboratories |

1947 |

Wilmington, Massachusetts, USA |

- IQVIA Recent Development: In 2023, IQVIA launched an AI-powered platform for clinical trial management that leverages machine learning to improve patient recruitment and streamline data collection. This new platform enhances efficiency in clinical trials and is expected to boost its service demand globally, positioning IQVIA at the forefront of clinical research innovation.

- Syneos Health Recent Development: In 2023, Syneos Health is recognized for its extensive experience in oncology and hematology, offering a wide range of services that include clinical development, regulatory support, and patient recruitment. They emphasize their ability to manage various types of clinical trials, including innovative designs like master trials and platform trials, which are particularly relevant in oncology research.

Global Contract Research Organization (CRO) Market Growth Drivers

- Increase in Pharmaceutical R&D Expenditure: The pharmaceutical industry's R&D spending has seen significant growth over the years, driving the demand for CRO services. According to a 2024 report by the U.S. FDA, pharmaceutical companies invested over $200 billion globally in R&D for drug development. This increase is primarily due to the rise in biologics and biosimilars, which require more complex and extensive clinical trials. With the need to streamline operations and manage costs, pharmaceutical companies are increasingly outsourcing trials to CROs, enabling them to focus on innovation.

- Rising Demand for Clinical Trials in Emerging Markets: Emerging markets such as India, China, and Brazil are seeing an increase in clinical trials due to their large patient pools, cost advantages, and improving regulatory frameworks. The Indian Ministry of Health reported that the number of clinical trials in India increased by 40% in 2023, primarily due to the countrys streamlined approval processes and the lower cost of conducting trials. These regions are becoming preferred destinations for CROs looking to expand their global footprint and take advantage of the cost savings and availability of diverse patient populations.

- Shift Toward Precision Medicine and Personalized Therapies: The growing focus on precision medicine and personalized therapies has significantly increased the need for specialized clinical trials. In 2023, the European Medicines Agency (EMA) announced that a substantial number of drugs in the pipeline were focused on targeted therapies, particularly in oncology. CROs are capitalizing on this shift by offering specialized services that include genomic testing, biomarker identification, and adaptive trial designs, which are essential for the development of these therapies. This trend is set to drive the demand for niche clinical research services globally.

Global Contract Research Organization (CRO) Market Challenges

- Stringent Regulatory Requirements: Navigating the regulatory landscape is a significant challenge for CROs, especially with varying guidelines across regions. For example, the U.S. FDA introduced new regulations in 2023 that required more extensive documentation and compliance measures for clinical trials involving biologics. Similarly, the China National Medical Products Administration has increased its oversight of CRO operations, requiring stricter adherence to patient safety and trial data transparency. These regulatory hurdles increase the complexity and cost of clinical trials, putting pressure on CROs to maintain compliance.

- Rising Operational Costs: CROs are facing rising operational costs due to inflation, increased labor costs, and the growing complexity of clinical trials. The average cost of conducting a Phase III clinical trial has significantly increased, driven by the need for more advanced trial designs and data collection methods. This rise in costs is making it challenging for smaller CROs to remain competitive, particularly in highly regulated markets such as the U.S. and Europe.

Global Contract Research Organization (CRO) Market Government Initiatives

- U.S. FDAs Expanded Breakthrough Therapy Designation: In 2023, the U.S. FDA expanded its Breakthrough Therapy Designation (BTD) program to include more therapeutic areas, such as rare diseases and complex biologics. This initiative fast-tracks the drug approval process, reducing the time it takes to bring a drug to market. As a result, pharmaceutical companies are increasingly partnering with CROs to expedite clinical trials, thereby benefiting from this regulatory support. The FDA reported that over 100 drugs received BTD in 2023, many of which were managed by CROs specializing in rapid trial management.

- Indias New Clinical Trial Rules: In 2023, the Indian Ministry of Health introduced new rules aimed at streamlining the approval process for clinical trials, reducing the timeline for trial approvals from 6 months to 3 months. This initiative has led to a significant increase in the number of trials conducted in India, particularly for Phase II and Phase III trials. The governments goal is to make India a global hub for clinical research, attracting both global pharmaceutical companies and CROs. By 2024, the number of trials conducted in India is expected to increase by 30%, driven by these regulatory improvements.

Global Contract Research Organization (CRO) Market Outlook

The contract research organization (CRO) market is expected to experience significant growth over the next five years, driven by a combination of factors including advancements in biologics and precision medicine, increasing adoption of decentralized clinical trials, and the expansion of clinical research activities in emerging markets.

Future Trends

- Market Outlook 2028 Driven by Increasing Demand for Biologics and Precision Medicine: The contract research organization market will see strong growth over the next five years, driven by the increasing demand for biologics, biosimilars, and precision medicine. The demand for biologics and personalized therapies requires more complex and lengthy clinical trials. CROs will continue to play a critical role in managing these trials, leveraging their expertise in genomic testing, biomarker identification, and adaptive trial designs. This shift will drive sustained demand for specialized CRO services.

- Increased Adoption of Decentralized Clinical Trials: Over the next five years, decentralized clinical trials (DCTs) are expected to become the norm, particularly in the U.S. and Europe. The incorporation of decentralization will reduce the need for physical site visits and enable more efficient patient recruitment and retention. The growth of telemedicine, wearable devices, and remote monitoring technologies will further accelerate this trend, making clinical trials more accessible to diverse patient populations. This shift will enhance patient engagement and reduce dropout rates, benefiting both CROs and pharmaceutical companies.

Scope of the Report

|

By Service Type |

Clinical Trial Services Preclinical Research Laboratory Services |

|

By End-User |

Pharmaceutical Companies Biotechnology Companies Medical Device Companies |

|

By Region |

North America Europe Asia-Pacific (APAC) Latin America Middle East & Africa (MEA) |

|

By Therapeutic Area |

Oncology Cardiology Central Nervous System Infectious Diseases Other Therapeutic Areas |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Pharmaceutical companies

Biotechnology companies

Medical device manufacturers

Government and regulatory bodies (FDA)

Venture capital and private equity firms

Contract manufacturing organizations (CMOs)

Hospital and healthcare systems

Companies

Players Mentioned in the Report:

IQVIA

Syneos Health

PPD

PRA Health Sciences

Charles River Laboratories

Medpace

Labcorp Drug Development

Parexel International

Covance

ICON Plc

WuXi AppTec

KCR

PRA Health Sciences

Certara

Rho Inc.

Table of Contents

01. Global Contract Research Organization (CRO) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02. Global Contract Research Organization (CRO) Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. Global Contract Research Organization (CRO) Market Analysis

3.1. Growth Drivers

3.1.1. Pharmaceutical R&D Expenditure Increase

3.1.2. Growing Demand for Clinical Trials in Emerging Markets

3.1.3. Precision Medicine and Personalized Therapies Demand

3.2. Restraints

3.2.1. Regulatory Complexities

3.2.2. Talent Shortage in Clinical Research

3.3. Opportunities

3.3.1. AI Integration in Clinical Trials

3.3.2. Expansion of Decentralized Clinical Trials

3.4. Trends

3.4.1. Growing Role of Genomics in Trials

3.4.2. Focus on Oncology Trials

3.5. Government Initiatives

3.5.1. U.S. FDA Expanded Breakthrough Therapy Designation

3.5.2. European Unions Horizon Europe Program

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competitive Ecosystem

04. Global Contract Research Organization (CRO) Market Segmentation, 2023

4.1. By Service Type (in Value %)

4.1.1. Clinical Trial Services

4.1.2. Preclinical Research

4.1.3. Laboratory Services

4.2. By End-User (in Value %)

4.2.1. Pharmaceutical Companies

4.2.2. Biotechnology Companies

4.2.3. Medical Device Companies

4.3. By Region (in Value %)

4.3.1. North America

4.3.2. Europe

4.3.3. Asia-Pacific (APAC)

4.3.4. Latin America

4.3.5. Middle East & Africa (MEA)

4.4. By Therapeutic Area (in Value %)

4.4.1. Oncology

4.4.2. Cardiovascular Diseases

4.4.3. Neurology

4.4.4. Infectious Diseases

4.5. By Clinical Phase (in Value %)

4.5.1. Phase I

4.5.2. Phase II

4.5.3. Phase III

4.5.4. Phase IV

05. Global Contract Research Organization (CRO) Competitive Landscape

5.1. Detailed Profiles of Major Companies

5.1.1. IQVIA

5.1.2. Syneos Health

5.1.3. PPD

5.1.4. PRA Health Sciences

5.1.5. Charles River Laboratories

5.1.6. Medpace

5.1.7. Labcorp Drug Development

5.1.8. Parexel International

5.1.9. Covance

5.1.10. ICON Plc

5.1.11. WuXi AppTec

5.1.12. KCR

5.1.13. Certara

5.1.14. Rho Inc.

5.1.15. Pharmaceutical Product Development (PPD)

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

06. Global Contract Research Organization (CRO) Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

07. Global Contract Research Organization (CRO) Market Regulatory Framework

7.1. Compliance Requirements

7.2. Certification Processes

08. Global Contract Research Organization (CRO) Market Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

09. Global Contract Research Organization (CRO) Market Future Market Segmentation, 2028

9.1. By Region (in Value %)

9.2. By Service Type (in Value %)

9.3. By End-User (in Value %)

9.4. By Therapeutic Area (in Value %)

9.5. By Clinical Phase (in Value %)

10. Global Contract Research Organization (CRO) Analysts Recommendations

10.1. Market Entry Strategies

10.2. Customer Targeting Strategies

10.3. Strategic Partnerships

10.4. Growth Opportunities Analysis

Disclaimer

Contact Us

Research Methodology

Step: 1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step: 2 Market Building:

Collating statistics on the Global Contract Research Organization (CRO) Market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Global Contract Research Organization (CRO) Market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step: 3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step: 4 Research Output:

Our team will approach multiple Contract Research Organization (CRO) Market and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from Contract Research Organization (CRO) Market.

Frequently Asked Questions

01. How big is the Global Contract Research Organization (CRO) market?

The global contract research organization (CRO) market was valued at USD 82.54 billion in 2023, driven by the rising R&D investments by pharmaceutical and biotechnology companies, increasing demand for clinical trials, and advancements in biologics and precision medicine.

02. What are the challenges in the Global Contract Research Organization (CRO) market?

Challenges in the global CRO market include stringent regulatory requirements across different regions, a shortage of qualified professionals in clinical research, and rising operational costs driven by inflation and the complexity of clinical trials.

03. Who are the major players in the Global Contract Research Organization (CRO) market?

Key players in the global CRO market include IQVIA, Syneos Health, PPD, PRA Health Sciences, and Charles River Laboratories. These companies dominate the market due to their extensive service offerings, global reach, and expertise in managing complex clinical trials.

04. What are the growth drivers of the Global Contract Research Organization (CRO) market?

The market is driven by the increasing R&D expenditures in the pharmaceutical and biotechnology sectors, rising demand for clinical trials in emerging markets, and the growing focus on precision medicine and biologics, which require specialized trial designs.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.