Global Copper Clad Laminate Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1040

December 2024

85

About the Report

Global Copper Clad Laminate Market Overview

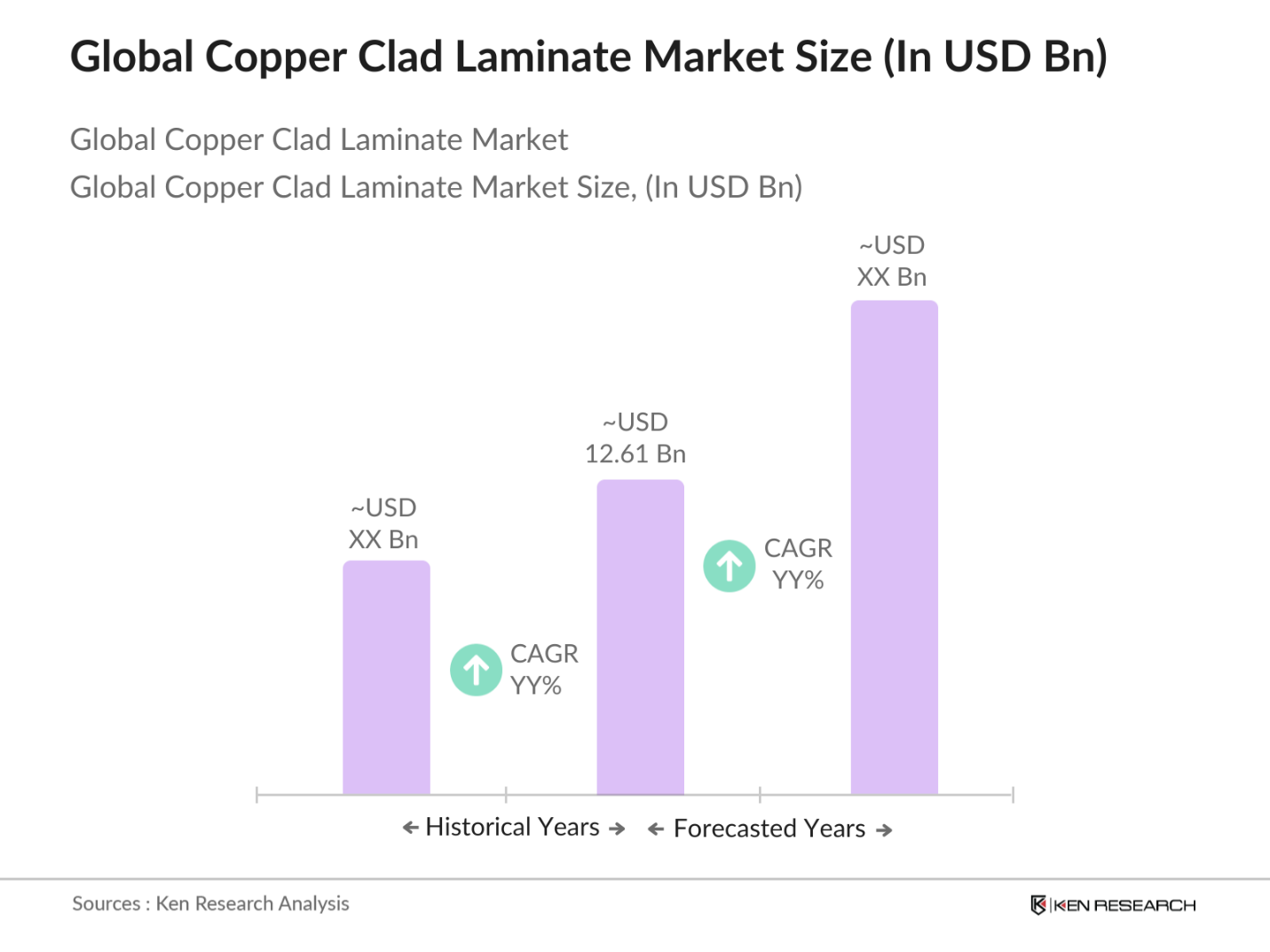

- The Copper Clad Laminate (CCL) market is valued at USD 12.61 billion, based on a five-year historical analysis. This market growth is driven by the increasing demand for printed circuit boards (PCBs) across industries such as consumer electronics, automotive, and telecommunications. The expansion of electric vehicles and the deployment of 5G infrastructure have further fueled the demand for high-performance copper-clad laminates.

- Countries like China, Taiwan, and South Korea dominate the copper clad laminate market. China, being the global hub for electronics manufacturing, holds a significant portion of the market. The high demand for copper clad laminates in this region is fueled by the presence of large-scale PCB manufacturing units and government policies that support local manufacturing. Taiwan and South Korea, with their advanced electronics industries and established manufacturers of high-frequency PCBs, also play key roles in driving the market forward.

- The European Union has enacted stringent environmental regulations focused on electronic waste management, which impact copper-clad laminate production. The EUs Waste Electrical and Electronic Equipment (WEEE) Directive requires manufacturers to handle end-of-life electronic products responsibly. In 2023, the EU allocated $900 million to improve recycling technology for electronic waste, which includes extracting copper and other materials from discarded electronics. These regulations aim to reduce environmental harm and promote a circular economy, thus influencing the demand for recyclable and sustainable CCLs.

Global Copper Clad Laminate Market Segmentation

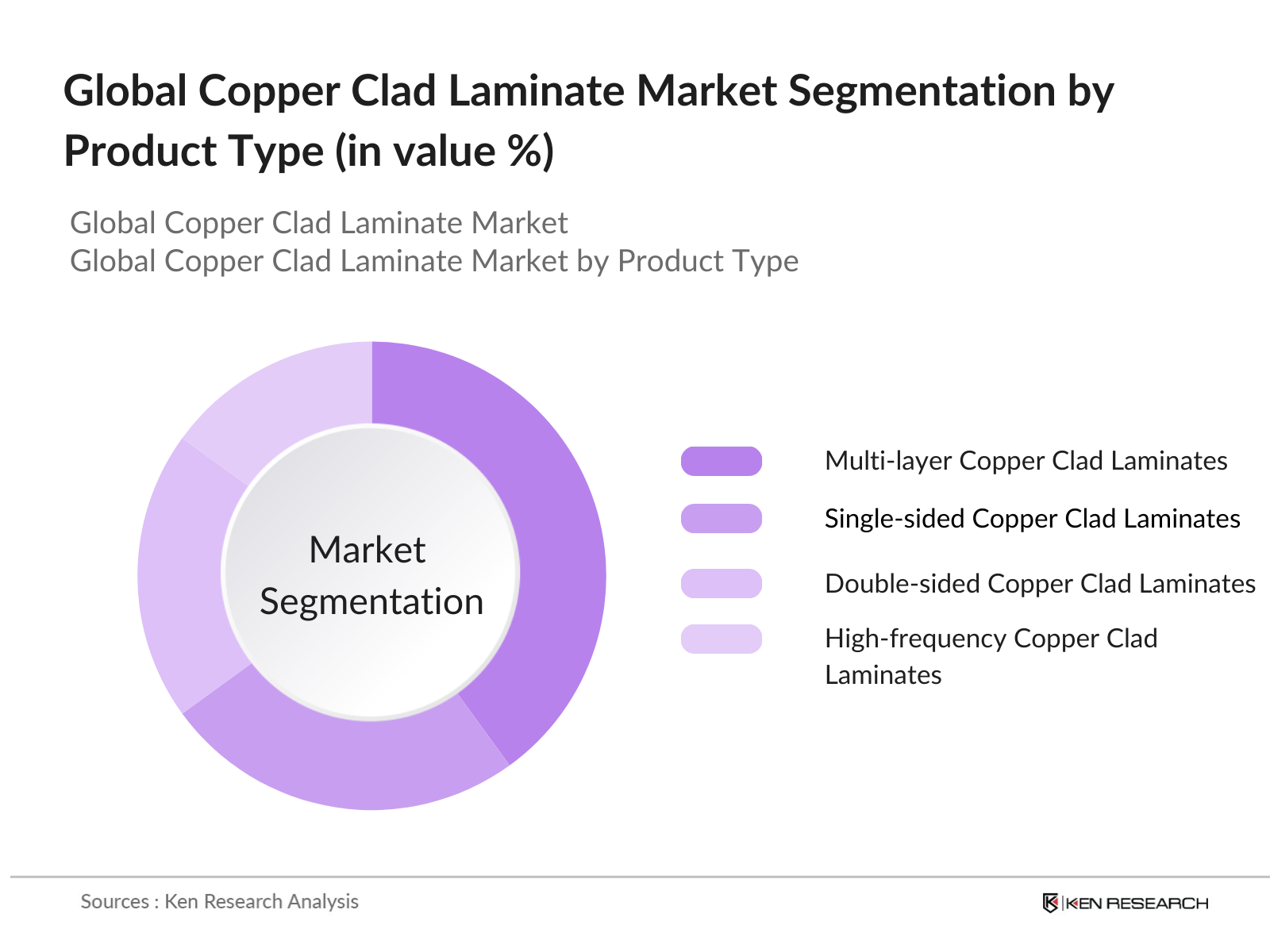

By Product Type: The Copper Clad Laminate market is segmented by product type into single-sided, double-sided, multi-layer, and high-frequency copper clad laminates. Among these, multi-layer copper clad laminates hold a dominant market share. This dominance is due to their widespread use in high-performance PCBs, which are integral to advanced telecommunications devices, automotive electronics, and industrial applications. Multi-layer laminates provide better thermal and electrical performance, making them ideal for applications requiring high reliability and precision.

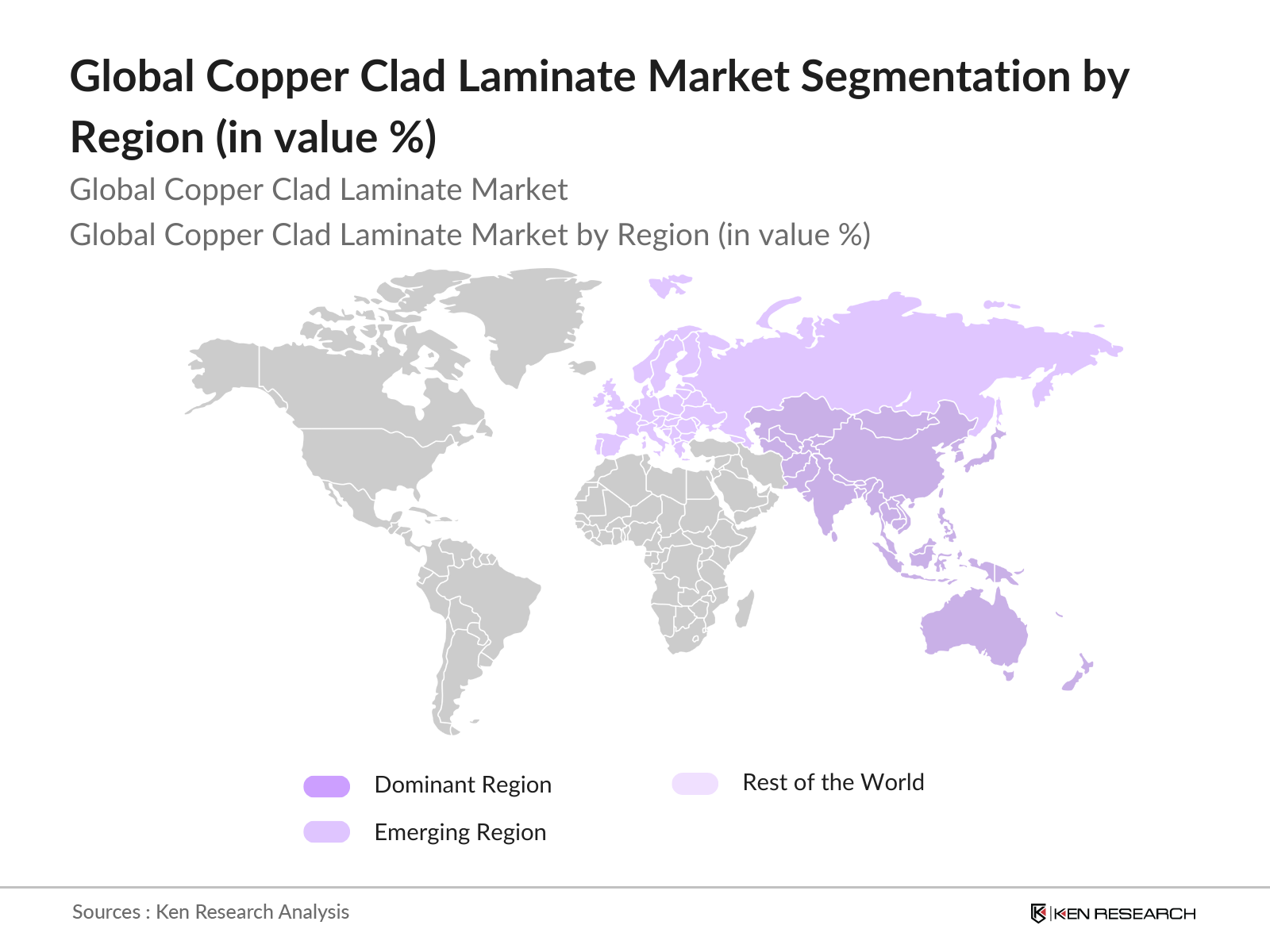

By Region: The Copper Clad Laminate market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the global market, with China being the largest contributor. The high concentration of electronics manufacturing in this region, coupled with the increasing demand for PCBs in sectors like automotive and telecommunications, drives the dominance of Asia-Pacific. The region benefits from a combination of low manufacturing costs, a skilled workforce, and strong government support for the electronics industry.

Global Copper Clad Laminate Market Competitive Landscape

The Copper Clad Laminate market is dominated by key players that have established their presence through innovation, large-scale production, and strategic investments in R&D. Companies like Kingboard Laminates Holdings and Shengyi Technology Co., Ltd. lead the market, leveraging their extensive product portfolios and long-standing expertise.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Manufacturing Facilities |

Revenue (USD Bn) |

R&D Investment |

Global Presence |

|

Kingboard Laminates Holdings |

1988 |

Hong Kong |

|||||

|

Shengyi Technology Co., Ltd. |

1985 |

Dongguan, China |

|||||

|

Mitsubishi Gas Chemical Company, Inc. |

1918 |

Tokyo, Japan |

|||||

|

Isola Group |

1912 |

Chandler, Arizona, USA |

|||||

|

Rogers Corporation |

1832 |

Chandler, Arizona, USA |

Global Copper Clad Laminate Market Analysis

Global Drivers

- Rising Demand for Electronic Devices (Smartphones, Laptops): The Copper Clad Laminate (CCL) market is seeing significant growth due to the increasing demand for electronic devices like smartphones and laptops. In 2022, the global smartphone production reached over 1.3 billion units, with Asia being the primary manufacturing hub. This surge in electronic device production has escalated the need for high-quality PCBs, where CCL plays a critical role. According to the International Monetary Fund (IMF), the electronics sector contributed $2.4 trillion to global GDP in 2022, creating a strong demand for CCL.

- Expansion of 5G Infrastructure: The rapid expansion of 5G networks is bolstering demand for copper-clad laminates. As of 2024, more than 85 countries have launched commercial 5G services, requiring an estimated 8.5 million new base stations, many of which are equipped with multi-layer PCBs. Copper-clad laminates are essential for the durability and high-frequency performance needed in these applications. Government investments in 5G infrastructure, such as the U.S.'s $65 billion plan, are also pushing the demand for advanced CCL.

- Increasing Investments in PCBs for Industrial Applications: Heavy industrial applications, especially in manufacturing and energy sectors, are increasingly adopting PCBs that use copper-clad laminates. In 2023, global investment in industrial automation reached $280 billion, fueled by governments' drive toward Industry 4.0 technologies. The copper-clad laminate market is capitalizing on these investments, as it provides the high-performance PCBs needed for equipment like robotic arms and control systems. In particular, the U.S. governments $52 billion allocation to domestic manufacturing highlights the industrial use of CCL.

Market Challenges

- High Manufacturing Costs: Manufacturing copper-clad laminates is capital-intensive due to the specialized equipment and stringent quality requirements. In 2023, the cost of setting up a CCL production facility in Asia averaged $200 million, with high-end machinery and environmental control systems contributing to the price. These high initial investments, coupled with energy costs, have raised concerns about maintaining profitability in a competitive market. Moreover, labor costs have also surged, especially in regions like China and Taiwan, further driving up operational expenses.

- Stringent Environmental Regulations on Copper Extraction: Environmental regulations on copper extraction and processing pose a significant challenge to the CCL market. Countries such as Chile, the worlds largest copper producer, have enacted stricter mining regulations, which have increased operational costs for copper suppliers. In 2023, Chile implemented water conservation laws that added $1.5 billion in compliance costs for copper miners. These regulations directly affect the supply and price of copper, leading to higher raw material costs and impacting the overall cost structure for CCL manufacturers.

Global Copper Clad Laminate Market Future Outlook

Over the next five years, the Copper Clad Laminate market is poised to experience substantial growth driven by continuous advancements in telecommunications, the growing demand for electric vehicles (EVs), and the increasing use of high-frequency PCBs in industrial applications. Governments worldwide are also implementing policies to support the domestic production of electronic components, which will further stimulate market growth. Additionally, the trend toward miniaturization of electronic devices and the growing demand for environmentally friendly materials will create new opportunities for manufacturers of copper clad laminates.

Market Opportunities:

- Shift Toward Environmentally Friendly Laminates (Halogen-Free): A growing trend in the CCL market is the shift towards environmentally friendly laminates, particularly halogen-free options. In 2023, Europe implemented regulations that require electronics manufacturers to limit halogenated flame retardants in PCBs. As a result, the demand for halogen-free copper-clad laminates has increased, with manufacturers investing heavily in alternative materials. The European Union allocated $750 million in grants for research into green PCB technologies, further pushing this market trend toward sustainability.

- Rising Adoption of Miniaturization in Electronics: The rising trend of miniaturization in electronics is shaping the future of the CCL market. With devices like smartphones and wearables becoming smaller, the need for compact yet highly efficient PCBs is growing. In 2023, global production of miniaturized components for electronics exceeded 100 billion units, with significant investments in microelectronics. Copper-clad laminates must adapt to these changing requirements, supporting higher performance in smaller form factors. The Japanese governments $1 billion investment in miniaturization R&D is an indicator of this growing trend.

Scope of the Report

|

By Product Type |

Single-sided Copper Clad Laminates Double-sided Copper Clad Laminates Multi-layer Copper Clad Laminates High-frequency Copper Clad Laminates |

|

By Resin Type |

Epoxy Resins Phenolic Resins Polyimide Resins |

|

By Application |

Consumer Electronics Automotive Telecommunications Industrial Equipment Aerospace & Defense |

|

By End-User Industry |

Electronics Manufacturing Automotive Manufacturing Telecommunication Equipment Aerospace Component Manufacturers |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Copper Clad Laminate Manufacturers

PCB Manufacturers

Automotive Electronics Manufacturers

Telecommunication Equipment Manufacturers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Environmental Protection Agency (EPA), Ministry of Electronics and Information Technology (MeitY))

Suppliers of Raw Materials (Copper, Resins)

Industrial Equipment Manufacturers

Companies

Players Mention in the Report

Kingboard Laminates Holdings

Shengyi Technology Co., Ltd.

Mitsubishi Gas Chemical Company, Inc.

Isola Group

Rogers Corporation

Sumitomo Bakelite Co., Ltd.

Panasonic Corporation

DowDuPont Inc.

SYTECH Co., Ltd.

Taiwan Union Technology Corporation

Grace Electron Co., Ltd.

Doosan Corporation

Eternal Materials Co., Ltd.

Guangdong Chaohua Technology Co., Ltd.

Nan Ya Plastics Corporation

Table of Contents

01. Global Copper Clad Laminate Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02. Global Copper Clad Laminate Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. Global Copper Clad Laminate Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand for Electronic Devices (Smartphones, Laptops)

3.1.2. Growth in Automotive Electronics (EVs, Autonomous Vehicles)

3.1.3. Expansion of 5G Infrastructure

3.1.4. Increasing Investments in PCBs for Industrial Applications

3.2. Market Challenges

3.2.1. Fluctuation in Raw Material Prices (Copper, Resins)

3.2.2. High Manufacturing Costs

3.2.3. Stringent Environmental Regulations on Copper Extraction

3.3. Opportunities

3.3.1. Technological Advancements in Multi-layer PCBs

3.3.2. Increasing Demand for High-Frequency Laminates (5G Applications)

3.3.3. Expansion into Emerging Markets (Asia-Pacific)

3.4. Trends

3.4.1. Shift Toward Environmentally Friendly Laminates (Halogen-Free)

3.4.2. Rising Adoption of Miniaturization in Electronics

3.4.3. Growth in Internet of Things (IoT) Devices

3.5. Government Regulations

3.5.1. Trade Policies on Copper Imports and Exports

3.5.2. Environmental Regulations on Electronic Waste Management

3.5.3. Incentives for Domestic Manufacturing of PCBs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

04. Global Copper Clad Laminate Market Segmentation

4.1. By Product Type (In Value %) 4.1.1. Single-sided Copper Clad Laminates

4.1.2. Double-sided Copper Clad Laminates

4.1.3. Multi-layer Copper Clad Laminates

4.1.4. High-frequency Copper Clad Laminates

4.2. By Resin Type (In Value %)

4.2.1. Epoxy Resins

4.2.2. Phenolic Resins

4.2.3. Polyimide Resins

4.3. By Application (In Value %)

4.3.1. Consumer Electronics

4.3.2. Automotive

4.3.3. Telecommunications

4.3.4. Industrial Equipment

4.3.5. Aerospace & Defense

4.4. By End-User Industry (In Value %)

4.4.1. Electronics Manufacturing

4.4.2. Automotive Manufacturing

4.4.3. Telecommunication Equipment Manufacturers

4.4.4. Aerospace Component Manufacturers

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. Global Copper Clad Laminate Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Kingboard Laminates Holdings

5.1.2. Shengyi Technology Co., Ltd.

5.1.3. Nan Ya Plastics Corporation

5.1.4. Mitsubishi Gas Chemical Company, Inc.

5.1.5. Isola Group

5.1.6. Rogers Corporation

5.1.7. DowDuPont Inc.

5.1.8. Sumitomo Bakelite Co., Ltd.

5.1.9. Panasonic Corporation

5.1.10. Guangdong Chaohua Technology Co., Ltd.

5.1.11. Taiwan Union Technology Corporation

5.1.12. Grace Electron Co., Ltd.

5.1.13. SYTECH Co., Ltd.

5.1.14. Doosan Corporation

5.1.15. Eternal Materials Co., Ltd.

5.2. Cross Comparison Parameters (Revenue, Manufacturing Facilities, Product Portfolio, R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

06. Global Copper Clad Laminate Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

07. Global Copper Clad Laminate Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08. Global Copper Clad Laminate Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Resin Type (In Value %)

8.3. By Application (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

09. Global Copper Clad Laminate Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins with a comprehensive analysis of the Copper Clad Laminate market ecosystem, identifying all relevant stakeholders. This step involves thorough secondary research from proprietary databases and industry reports to define the key market dynamics.

Step 2: Market Analysis and Construction

This phase involves gathering historical data on the Copper Clad Laminate market, including production, demand, and revenue figures. The data is used to assess the current market status and future growth prospects, considering the penetration of CCL products in different industries.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formulated based on historical data and emerging trends. These are validated through interviews with industry experts, including CCL manufacturers and electronics industry specialists, to ensure the accuracy of the data.

Step 4: Research Synthesis and Final Output

In this final stage, data from various sources is synthesized to create a detailed report on the Copper Clad Laminate market. The findings are verified through consultations with industry players to ensure the final report reflects the market's current state and future potential accurately.

Frequently Asked Questions

01. How big is the Global Copper Clad Laminate Market?

The Global Copper Clad Laminate market was valued at USD 12.61 billion, driven by the increasing demand for printed circuit boards across various industries, including telecommunications, automotive, and consumer electronics.

02. What are the challenges in the Copper Clad Laminate Market?

The market faces challenges such as fluctuating copper prices and stringent environmental regulations, particularly concerning copper extraction and electronic waste management. These factors can affect the cost structure for manufacturers.

03. Who are the major players in the Copper Clad Laminate Market?

Key players include Kingboard Laminates Holdings, Shengyi Technology Co., Ltd., Mitsubishi Gas Chemical Company, Inc., Isola Group, and Rogers Corporation. These companies dominate due to their strong production capabilities and extensive product portfolios.

04. What drives the Copper Clad Laminate Market?

The market is driven by increasing demand for high-frequency PCBs used in telecommunications, the growing adoption of electric vehicles, and advancements in PCB technologies for industrial applications.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.