Global Digital Signature Providers Market Outlook to 2030

Region:Global

Author(s):Ananya Singh

Product Code:KROD8854

November 2024

96

About the Report

Global Digital Signature Providers Market Overview

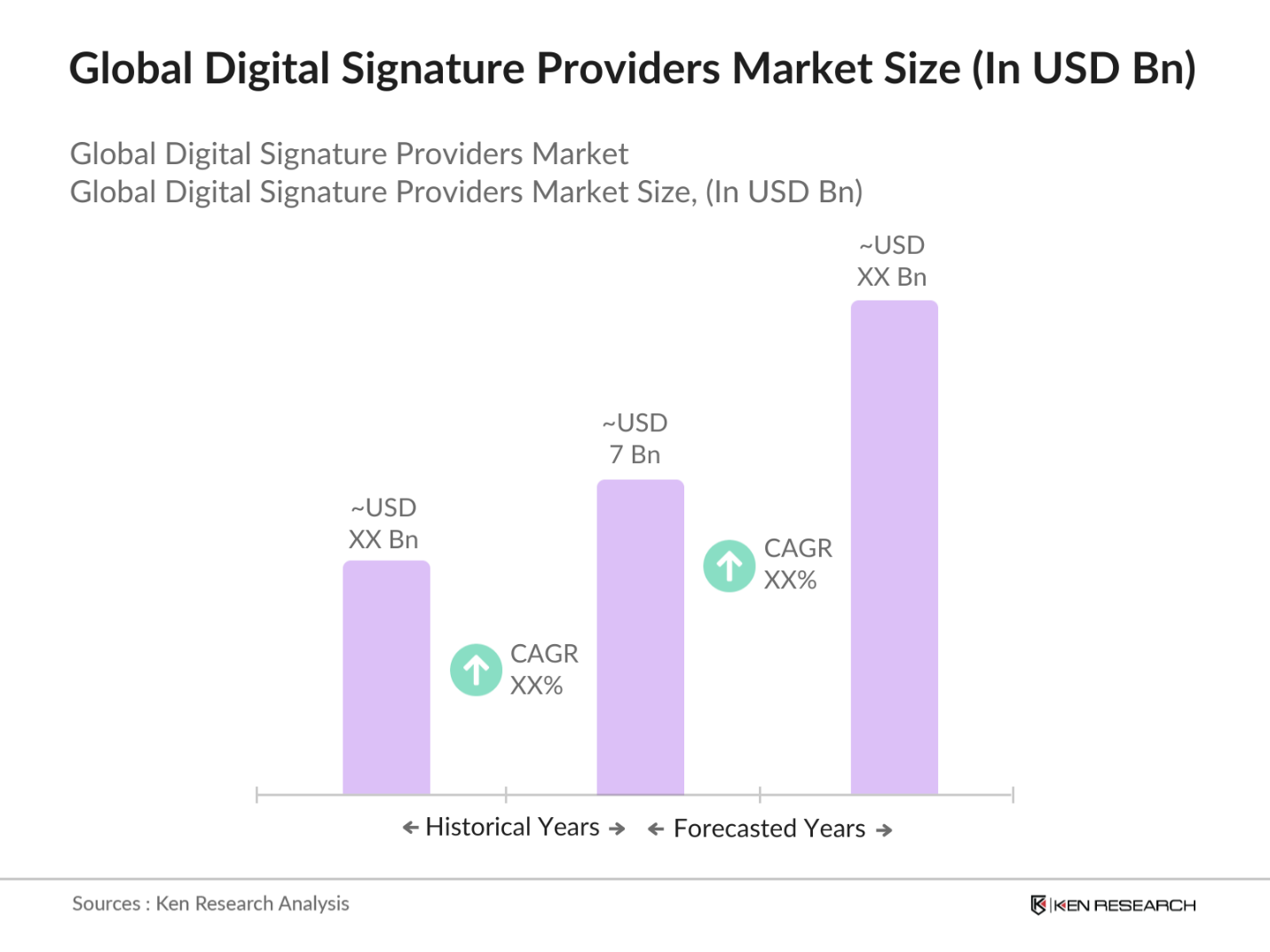

- The global digital signature providers market, valued at USD 7 billion, is primarily driven by the need for secure, convenient, and legally binding authentication solutions across various sectors, including banking, finance, healthcare, and government. Increasing regulatory demands and the need to reduce paper-based processes are major driving factors. Companies are increasingly transitioning to cloud-based digital solutions, leveraging digital signatures to streamline workflows and enhance security in document transactions.

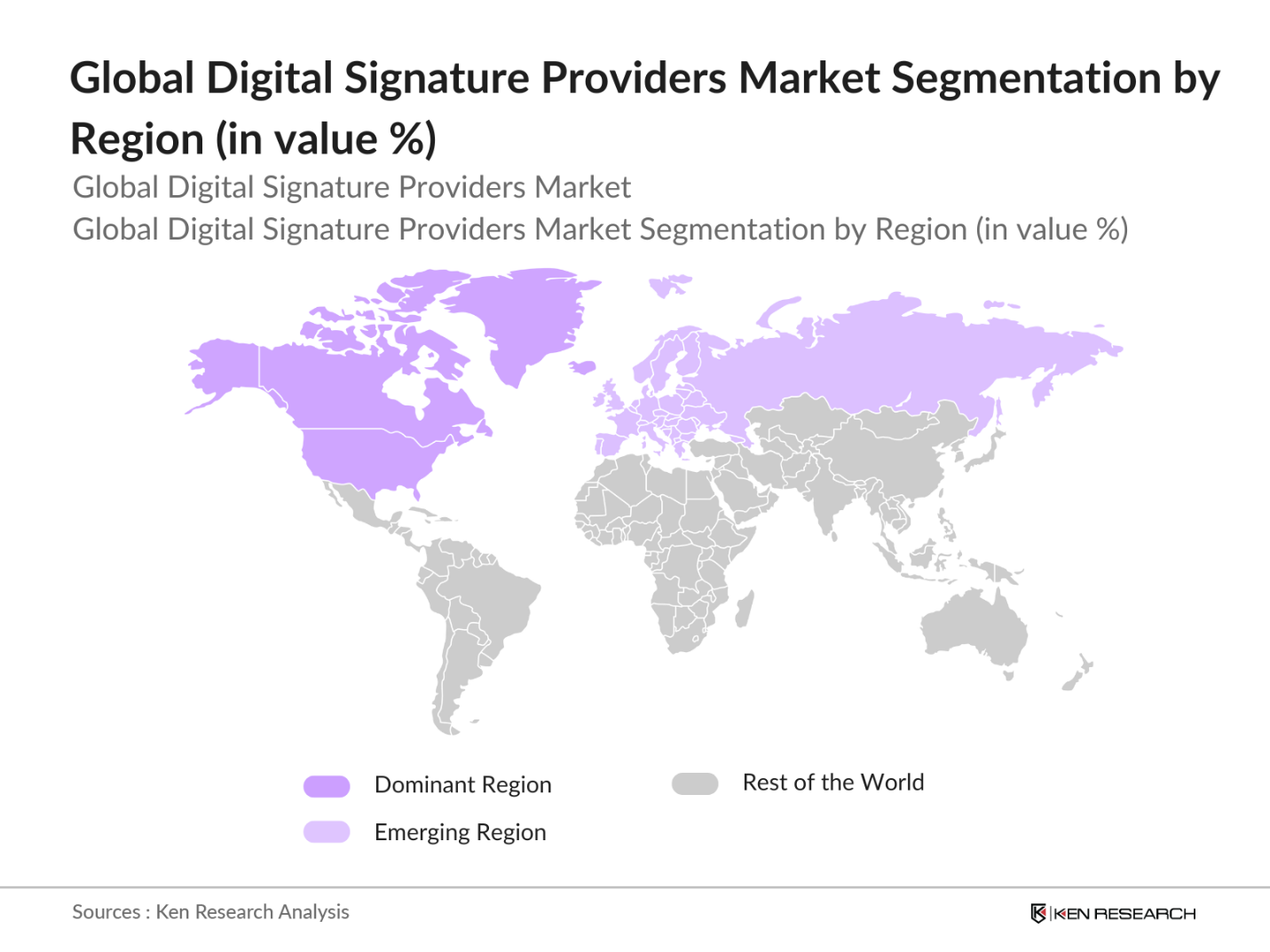

- The market is predominantly dominated by regions like North America and Europe, where the regulatory environment is highly conducive to digital transformation and cybersecurity. The U.S., with its mature IT infrastructure and widespread adoption of e-signature regulations, leads the market, while countries in Europe, such as Germany and the UK, benefit from strict data privacy regulations like GDPR, which encourage the adoption of secure digital signature solutions.

- To encourage digital transformation, several governments offer tax incentives for businesses implementing digital solutions. For instance, Canada provides tax credits for companies investing in digital signature systems, contributing to an estimated USD 300 million in tax relief for businesses in 2024. This support reduces the financial barrier, making it easier for organizations to adopt secure digital authentication tools.

Global Digital Signature Providers Market Segmentation

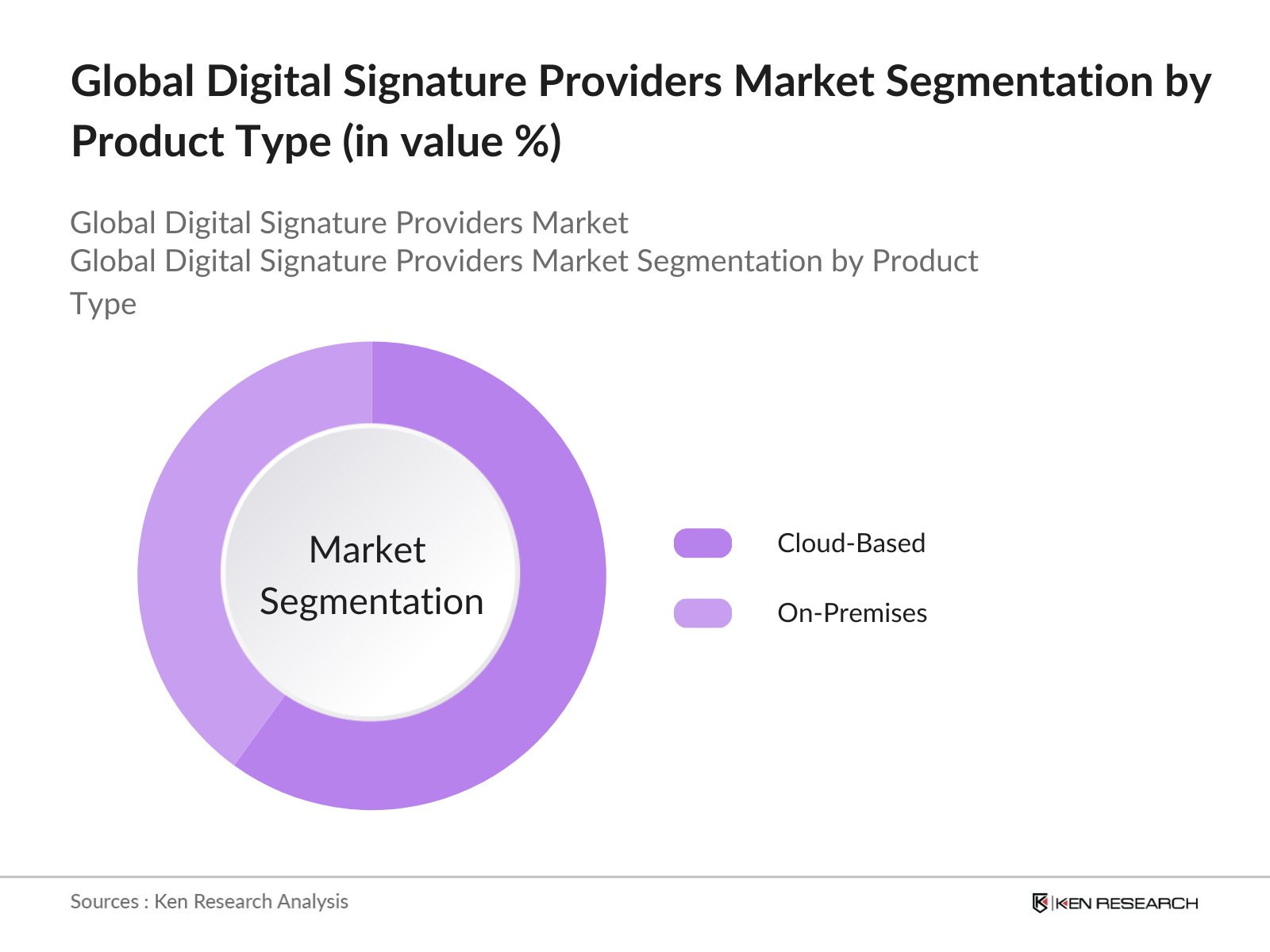

- By Solution Type: The global digital signature providers market is segmented by solution type into on-premises solutions and cloud-based solutions. Cloud-based solutions have the dominant market share under this segmentation due to their scalability, ease of implementation, and lower operational costs, which appeal to both large enterprises and SMEs. Additionally, the shift toward digital transformation and remote work models has further accelerated the adoption of cloud solutions, making them preferable for their flexibility and real-time accessibility.

- By Region: Regionally, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America has the leading market share due to its well-established infrastructure, regulatory support, and the presence of major market players. Strong investments in IT and security infrastructure, along with favorable regulatory policies, have bolstered the market position in the region.

By Authentication Type: The market is segmented by authentication type into knowledge-based authentication, biometric authentication, and multi-factor authentication. Multi-factor authentication (MFA) holds the largest market share in this segment as it offers enhanced security measures by combining multiple layers of verification, crucial for sectors like banking and healthcare. MFA reduces the risk of fraud and unauthorized access, which has become paramount with the rise in cyber-attacks.

Global Digital Signature Providers Market Competitive Landscape

The global digital signature providers market is dominated by key players such as Adobe Inc., DocuSign, and OneSpan, highlighting the consolidation in the market and the influence of these major providers. These companies lead in innovation, regulatory compliance, and have extensive global reach, contributing to their strong market positions.

Global Digital Signature Providers Market Analysis

Growth Drivers

- Increased Adoption of Digital Transformation in Key Sectors: The demand for digital signatures is surging as industries such as banking, financial services, and insurance (BFSI) integrate digital authentication solutions to support paperless workflows and enhance transaction security. The BFSI sector alone is set to adopt over 1 billion digital signature transactions in 2024 to streamline processes and meet compliance standards, driven by data security mandates. Government policies favoring digitalization across sectors are further driving adoption, resulting in digital signatures becoming a critical tool in sectors dealing with high-volume document handling and verification.

- Government and Regulatory Support for Digital Signatures: Governments worldwide have implemented electronic signature regulations, mandating secure digital transactions and document authentication. In 2024, electronic signature laws in over 70 countries, including the U.S., Canada, and several EU nations, legally enforce digital signatures, with the U.S. alone seeing over 400 million document authentications completed via digital signatures. Regulatory bodies like the European Unions eIDAS framework also enhance cross-border legal standards, positioning digital signatures as a required component of secure, legally binding digital transactions.

- Growing Cybersecurity Threats and Need for Data Integrity: The rise in cyber threats and data breaches has increased the need for secure authentication solutions. The financial loss from cyberattacks is projected to exceed USD 10 trillion globally in 2024, prompting businesses to adopt secure digital signatures as part of robust cybersecurity measures. These solutions are essential in high-risk industries such as finance and healthcare, where data integrity is critical to operations, making digital signatures indispensable for secure, compliant transaction verification.

Market Challenges

- High Implementation and Maintenance Costs: Implementing digital signature solutions can be costly, particularly for small to medium enterprises. In 2024, the average cost of deploying and maintaining a secure, compliant digital signature system for enterprises is estimated to exceed USD 500,000, creating a significant barrier for smaller organizations. Additionally, recurring costs for system upgrades and cybersecurity enhancements add to the financial strain, limiting adoption among budget-constrained businesses.

- Interoperability Issues Across Platforms and Regions: Digital signature systems often face interoperability challenges, as variations in standards and protocols across regions create complexities for businesses operating globally. With over 50% of global businesses citing interoperability as a primary concern in 2024, integrating digital signature systems across different jurisdictions remains challenging. These compatibility issues slow adoption, as businesses require systems that operate seamlessly across platforms and comply with multiple regulatory frameworks.

Global Digital Signature Providers Market Future Outlook

The global digital signature providers market is expected to grow steadily, supported by regulatory compliance requirements, technological advancements, and the growing emphasis on secure digital transactions. The demand for digital authentication is anticipated to rise, driven by sectors such as BFSI, healthcare, and government, which prioritize data security and efficiency. Increasing investments in cloud technology and integration with emerging solutions like blockchain will further shape the market landscape, presenting substantial opportunities for growth and innovation.

Market Opportunities

- Increased Adoption of AI-Powered Authentication: Over the next five years, digital signature platforms are expected to incorporate AI for identity verification, detecting fraud, and improving security measures. The integration of AI is projected to support over 200 million transactions annually by 2029, transforming digital signature processes with real-time authentication and enhanced security protocols.

- Growth of Blockchain-Based Digital Signature Solutions: Blockchain-enabled digital signature solutions will likely become more prevalent as organizations prioritize data security and transparency. By 2029, blockchain technology is projected to support nearly 30% of digital signature implementations, especially in sectors with stringent data integrity requirements, ensuring secure, traceable document verification.

Scope of the Report

|

By Solution Type |

On-Premises Solutions, |

|

By Authentication Type |

Knowledge-Based |

|

By Deployment Mode |

Cloud |

|

By End-User Industry |

BFSI |

|

By Region |

North America |

Products

Key Target Audience

BFSI Sector

Healthcare Providers and Institutions

IT & Telecom Service Providers

Legal and Law Firms

E-commerce and Retail Companies

Large Enterprises and SMEs

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., GDPR, CCPA)

Companies

Players Mentioned in the Report

Adobe Inc.

DocuSign Inc.

OneSpan Inc.

Entrust Datacard Corporation

Gemalto NV

Thales Group

Zoho Corporation

Secured Signing Limited

SignNow

RightSignature by Citrix

Table of Contents

1. Global Digital Signature Providers Market Overview

1.1. Definition and Scope (Digital Signature, E-Signature, Authentication)

1.2. Market Taxonomy (Solutions, Services, Deployment, End-User)

1.3. Market Growth Rate (YOY)

1.4. Market Segmentation Overview

2. Global Digital Signature Providers Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Industry Partnerships, Government Initiatives)

3. Global Digital Signature Providers Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Regulatory Compliance Requirements

3.1.2. Adoption of Cloud-Based Solutions

3.1.3. Rising Digital Transformation

3.1.4. Enhanced Cybersecurity Needs

3.2. Restraints

3.2.1. High Initial Implementation Costs

3.2.2. Interoperability Issues

3.2.3. Security and Privacy Concerns

3.3. Opportunities

3.3.1. Integration with Blockchain Technology

3.3.2. Growing Adoption in SMEs

3.3.3. Increased Demand in BFSI and Healthcare Sectors

3.4. Trends

3.4.1. Integration of AI in Authentication

3.4.2. Growth in Multi-Factor Authentication

3.4.3. Expansion of Cloud-Based Digital Signature Solutions

3.5. Government Regulation

3.5.1. E-Signature Legislation

3.5.2. Data Privacy Compliance (GDPR, CCPA)

3.5.3. Cross-Border Authentication Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Vendors, Resellers, Cloud Providers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Global Digital Signature Providers Market Segmentation

4.1. By Solution Type (In Value %)

4.1.1. On-Premises Solutions

4.1.2. Cloud-Based Solutions

4.2. By Authentication Type (In Value %)

4.2.1. Knowledge-Based Authentication

4.2.2. Biometric Authentication

4.2.3. Multi-Factor Authentication

4.3. By Deployment Mode (In Value %)

4.3.1. Cloud

4.3.2. On-Premises

4.4. By End-User Industry (In Value %)

4.4.1. BFSI

4.4.2. Healthcare

4.4.3. IT & Telecom

4.4.4. Government

4.4.5. Legal

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Digital Signature Providers Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Adobe Inc.

5.1.2. DocuSign Inc.

5.1.3. OneSpan Inc.

5.1.4. Entrust Datacard Corporation

5.1.5. Gemalto NV

5.1.6. Thales Group

5.1.7. Zoho Corporation

5.1.8. Secured Signing Limited

5.1.9. SignNow

5.1.10. RightSignature by Citrix

5.2 Cross Comparison Parameters (Revenue, Headquarters, Inception Year, Market Share, Certification)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investor Analysis

5.7 Private Equity and Venture Capital Funding

5.8 Government Grants and Subsidies

6. Global Digital Signature Providers Market Regulatory Framework

6.1. E-Signature Legalization Policies (eIDAS, UETA, ESIGN Act)

6.2. Data Security Compliance (GDPR, CCPA, HIPAA)

6.3. Industry Standards and Certifications

7. Global Digital Signature Providers Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Global Digital Signature Providers Future Market Segmentation

8.1. By Solution Type (In Value %)

8.2. By Authentication Type (In Value %)

8.3. By Deployment Mode (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. Global Digital Signature Providers Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Digital Marketing Strategies

9.4. White Space Opportunity Identification

Research Methodology

Step 1: Identification of Key Variables

In this initial stage, we map the ecosystem of digital signature providers, focusing on primary stakeholders such as solution providers, end-users, and regulatory authorities. Comprehensive desk research and analysis of secondary and proprietary databases enable the identification of critical market variables influencing demand and growth.

Step 2: Market Analysis and Construction

This phase involves analyzing historical data specific to the digital signature market, assessing the adoption of various deployment models and authentication types. An evaluation of security protocols and their alignment with industry standards is also conducted to ensure reliable revenue projections.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formed and validated through in-depth interviews with industry experts, including executives from leading companies in digital security and authentication. These discussions yield essential insights into market trends and customer preferences, strengthening the validity of the market data.

Step 4: Research Synthesis and Final Output

The last phase involves synthesizing insights from primary and secondary research to create a validated and comprehensive analysis. This includes verifying segmentation data, market size, and emerging trends to ensure a thorough understanding of the global digital signature providers market.

Frequently Asked Questions

1. How big is the global digital signature providers market?

The global digital signature providers market, valued at USD 7 billion, is driven by increasing regulatory compliance needs and demand for secure digital solutions across sectors like BFSI and healthcare.

2. What are the primary drivers of growth in the global digital signature providers market?

Key growth in global digital signature providers market drivers include the rise of digital transformation, heightened data privacy regulations, and the shift towards cloud-based solutions for ease of implementation and cost savings.

3. Which regions dominate the global digital signature providers market?

North America leads the global digital signature providers market due to a robust regulatory framework and advanced IT infrastructure, followed by Europe, which benefits from GDPR and other stringent data security laws.

4. Who are the key players in the global digital signature providers market?

Major players in global digital signature providers market include Adobe Inc., DocuSign Inc., and OneSpan Inc., who dominate due to their extensive product offerings, global reach, and compliance with international standards

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.