Global Edge Computing Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD1900

December 2024

89

About the Report

Global Edge Computing Market Overview

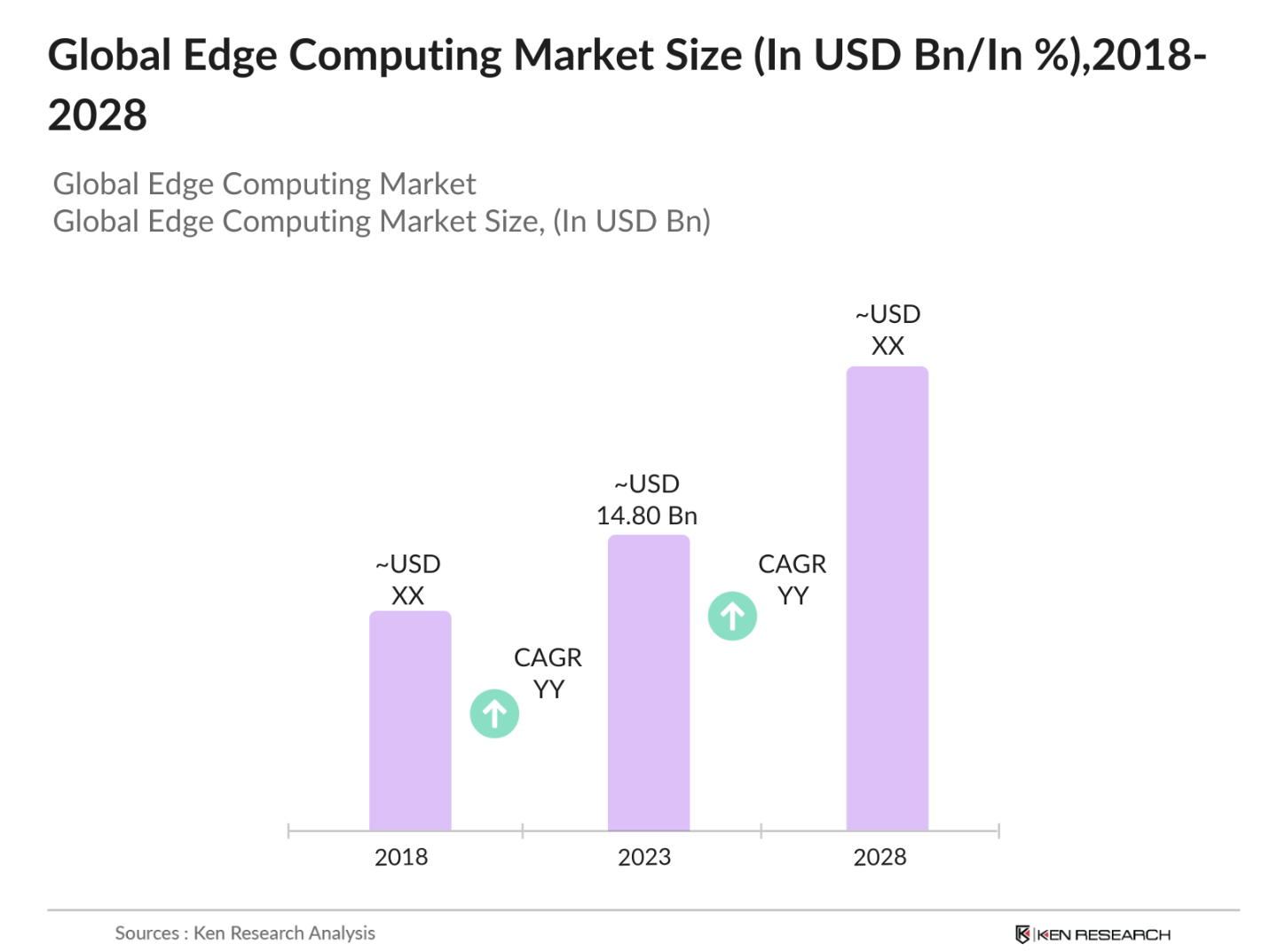

- The Global Edge Computing Market was valued at USD 14.80 billion in 2023. This growth is primarily driven by the rapid deployment of 5G networks, the rising adoption of Internet of Things (IoT) devices, and the increasing demand for low-latency processing solutions. Edge computing enables faster data processing by decentralizing computation from traditional cloud models to the networks edge, where data is generated.

- Major players in the global edge computing market include Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, and Cisco Systems. These companies are leading the development of edge solutions by integrating AI, machine learning, and 5G technologies. Their edge computing offerings enable organizations to reduce latency, optimize data management, and deploy real-time applications across various sectors.

- In 2023, AWS announced plans to expand its Local Zones, which are part of its edge computing strategy, by deploying infrastructure in 32 new cities globally, building upon the existing 16 Local Zones in the United States.This expansion aims to support low-latency applications across various industries, including healthcare, financial services, and government

- North America dominated the global edge computing market in 2023, supported by a robust IT infrastructure, high adoption rates of IoT devices, and substantial investments from major technology companies. The region's leadership is further bolstered by ongoing developments in 5G and AI-driven edge solutions.

Global Edge Computing Market Segmentation

The global edge computing market is segmented by region, component, and application.

- By Region: The global edge computing market is segmented into North America, Europe, Asia-Pacific (APAC), Middle East & Africa (MEA), and Latin America. In 2023, North America held the largest market share, owing to technological advancements, high IoT adoption rates, and significant investments from major tech companies. The presence of leading cloud and edge providers in the region further solidifies its position.

- By Component: The market is segmented into hardware, software, and services. In 2023, the hardware segment held the largest market share due to the increasing deployment of edge devices such as routers, gateways, and edge servers. These devices play a crucial role in enabling real-time data processing at the network's edge, especially in industries like manufacturing and transportation.

- By Application: The market is segmented into manufacturing, telecom, healthcare, retail, and transportation. In 2023, the manufacturing segment dominated the market, driven by the adoption of edge computing for real-time monitoring, predictive maintenance, and automation in smart factories. Industries are increasingly leveraging edge solutions to improve efficiency and reduce downtime.

Global Edge Computing Market Competitive Landscape

|

Company |

Year of Establishment |

Headquarters |

|

Amazon Web Services |

2006 |

Seattle, Washington, USA |

|

Microsoft Azure |

2010 |

Redmond, Washington, USA |

|

Google Cloud |

2008 |

Mountain View, California, USA |

|

IBM |

1911 |

Armonk, New York, USA |

|

Cisco Systems |

1984 |

San Jose, California, USA |

- Microsoft Azure: In 2023, Microsoft launched its Azure Edge Zones, targeting 5G-enabled IoT devices. These zones provide low-latency edge solutions for smart cities and autonomous driving. Microsoft continues to expand its edge ecosystem by partnering with telecom companies to deliver edge-enabled applications across various sectors.

- Google Cloud: In 2023, Google Cloud introduced a new AI-driven edge platform designed for healthcare and retail sectors. The platform enables businesses to deploy AI models at the edge, offering enhanced decision-making capabilities and real-time analytics for customer engagement and operational efficiency.

Global Edge Computing Market Analysis

Global Edge Computing Market Growth Drivers

- Rising Adoption of IoT Devices: In 2023, the increasing number of IoT devices, estimated to exceed 14 billion globally, has driven demand for edge computing solutions. IoT devices generate vast amounts of data that require real-time processing, particularly in sectors like healthcare, manufacturing, and smart cities. Edge computing enables these devices to operate with reduced latency, improving efficiency and decision-making capabilities.

- Deployment of 5G Networks

The global rollout of 5G networks in 2023 significantly impacted the growth of the edge computing market. With approximately 1.76 billion 5G connections worldwide, industries like telecom, automotive, and manufacturing are leveraging the high-speed, low-latency capabilities of 5G to deploy edge computing solutions. These networks enable real-time data processing in areas such as autonomous vehicles and smart infrastructure. - Integration of AI and Machine Learning: In 2023, AI-driven edge computing solutions gained traction across industries. The integration of AI and machine learning at the edge allows businesses to perform predictive analytics and automate processes without relying on centralized cloud systems. AI-based edge solutions have been particularly beneficial for industries such as retail and manufacturing, where real-time decision-making is critical.

Global Edge Computing Market Challenges

- Data Security and Privacy Concerns: In 2023, with the growing adoption of edge computing, concerns over data security and privacy have intensified. Processing data at the edge introduces new vulnerabilities, especially in sectors such as healthcare and finance, where sensitive data is prevalent. Organizations must implement robust security measures to ensure that data is processed securely and complies with regional data protection regulations.

- High Infrastructure Costs: In 2023, the high costs associated with deploying and maintaining edge infrastructure posed a significant challenge, particularly for small and medium enterprises (SMEs). Edge devices, servers, and network infrastructure are expensive, making it difficult for smaller organizations to adopt edge computing solutions at scale. This has limited the adoption of edge computing in resource-constrained environments.

Global Edge Computing Market Government Initiatives

- European Unions Horizon Europe Program: In 2023, the European Union launched the Horizon Europe program, allocating 13.5 billion to fund edge computing initiatives, particularly in smart cities and industrial IoT applications. This initiative aims to enhance real-time data processing capabilities and drive the adoption of edge solutions in urban management and industrial automation.

- Indias National Investment and Infrastructure Fund (NIIF): In 2023, the Digital Edge company and its partnership with the National Investment and Infrastructure Fund (NIIF) and AGP InvestCo to develop a 300MW hyperscale data center in Navi Mumbai, which involves a total investment of $2 billion, not $300 million for a government program. The focus of the Digital Edge initiative is on building data center infrastructure, which is part of India's broader digital transformation strategy.

Global Edge Computing Market Future Market Outlook

The global edge computing market is expected to witness significant growth by 2028, driven by advancements in AI, 5G technology, and the increasing adoption of IoT devices. As industries across the globe prioritize real-time data processing, edge computing will play a crucial role in enabling low-latency applications and optimizing operational efficiency.

Future Market Trends

- Integration with AI and Machine Learning: By 2028, edge computing solutions will increasingly integrate AI and machine learning technologies to enhance real-time data processing capabilities. AI-driven edge solutions will dominate applications in industries like healthcare, retail, and manufacturing, enabling predictive maintenance, automated decision-making, and real-time customer engagement.

- Expansion of Distributed Edge Networks: By 2028, localized edge data centers will provide greater scalability and resilience, reducing dependence on centralized cloud systems. This trend will be driven by the need for faster data processing and improved network reliability.

Scope of the Report

|

Component |

Hardware Software Services |

|

Application |

Manufacturing Telecom Healthcare Retail Transportation |

|

Deployment Mode |

Cloud-Based On-Premise |

|

Organization Size |

Large Enterprises Small Enterprises Medium Enterprises |

|

By Region |

North America Europe Asia-Pacific (APAC) Middle East & Africa (MEA) Latin America |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

IT and Cloud Service Industries

Telecommunication Companies

IoT Device Manufacturing Industries

Data Center Companies

Automotive and Transportation Companies

Manufacturing Companies

Retail and E-Commerce Companies

Investments and Venture Capitalist Firms

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Amazon Web Services (AWS)

Microsoft Azure

Google Cloud

IBM

Cisco Systems

Huawei Technologies

Dell Technologies

Hewlett Packard Enterprise (HPE)

NVIDIA Corporation

Siemens AG

Table of Contents

1. Global Edge Computing Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Edge Computing Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Edge Computing Market Analysis

3.1. Growth Drivers

3.1.1. Rising Adoption of IoT Devices

3.1.2. Deployment of 5G Networks

3.1.3. Integration of AI and Machine Learning

3.2. Market Challenges

3.2.1. Data Security and Privacy Concerns

3.2.2. High Infrastructure Costs

3.2.3. Lack of Standardized Protocols

3.3. Opportunities

3.3.1. Expansion of Distributed Edge Networks

3.3.2. AI-driven Predictive Maintenance Solutions

3.3.3. Partnerships with Telecom and Technology Providers

3.4. Trends

3.4.1. Integration of AI and Machine Learning at the Edge

3.4.2. Edge Computing in Smart Infrastructure and Autonomous Vehicles

3.4.3. Increased Adoption of Edge Computing in Retail and Healthcare

3.5. Government Regulation

3.5.1. European Union’s Horizon Europe Program

3.5.2. India’s National Investment and Infrastructure Fund (NIIF) Initiative

3.5.3. Data Privacy and Cybersecurity Regulations

3.6. SWOT Analysis

3.7. Porter’s Five Forces

3.8. Stake Ecosystem

3.9. Competition Ecosystem

4. Global Edge Computing Market Segmentation

4.1. By Region (In Value %)

4.1.1. North America

4.1.2. Europe

4.1.3. Asia-Pacific (APAC)

4.1.4. Middle East & Africa (MEA)

4.1.5. Latin America

4.2. By Component (In Value %)

4.2.1. Hardware

4.2.2. Software

4.2.3. Services

4.3. By Application (In Value %)

4.3.1. Manufacturing

4.3.2. Telecom

4.3.3. Healthcare

4.3.4. Retail

4.3.5. Transportation

4.4. By Deployment Mode (In Value %)

4.4.1. Cloud-Based

4.4.2. On-Premise

4.5. By Organization Size (In Value %)

4.5.1. Large Enterprises

4.5.2. Small Enterprises

4.5.3. Medium Enterprises

5. Global Edge Computing Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Amazon Web Services (AWS)

5.1.2. Microsoft Azure

5.1.3. Google Cloud

5.1.4. IBM

5.1.5. Cisco Systems

5.1.6. Huawei Technologies

5.1.7. Dell Technologies

5.1.8. Hewlett Packard Enterprise (HPE)

5.1.9. NVIDIA Corporation

5.1.10. Siemens AG

5.1.11. Schneider Electric

5.1.12. EdgeConneX

5.1.13. Intel Corporation

5.1.14. AT&T

5.1.15. Verizon Communications

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Partnerships, Cloud-to-Edge Integration, AI and ML Capability, Edge Infrastructure, Industry Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Edge Computing Market Regulatory Framework

6.1. Data Privacy Laws and Compliance

6.2. Cybersecurity Regulations

6.3. Certification Standards for Edge Computing

7. Global Edge Computing Market Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Edge Computing Market Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Application (In Value %)

8.3. By Deployment Mode (In Value %)

8.4. By Organization Size (In Value %)

8.5. By Region (In Value %)

9. Global Edge Computing Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Expansion Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step: 1 Identifying Key Variables

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around the Market to collate Market-level information.

Step: 2 Market Building

Collating statistics on the global edge computing market over the years, and analyzing the penetration of Marketplaces as well as the ratio of service providers to compute the revenue generated for the market. We will also review service quality statistics to understand the revenue generated which can ensure accuracy behind the data points shared.

Step: 3 Validating and Finalizing

Building Market hypotheses and conducting CATIs with Market experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step: 4 Research Output

Our team will approach multiple edge computing companies to understand the nature of service segments, consumer preferences, and other parameters. This supports validating statistics derived through a bottom-to-top approach from these edge computing companies, ensuring accuracy and reliability in the report.

Frequently Asked Questions

01 How big is the global edge computing market?

The global edge computing market was valued at USD 14.80 billion in 2023. This market is driven by the increasing demand for low-latency data processing, the rise in IoT devices, and the rapid expansion of 5G networks, enabling real-time applications across various industries.

02 What are the challenges in the global edge computing market?

Challenges in the global edge computing market include data privacy concerns, high infrastructure costs for edge devices and networks, and the lack of standardized protocols. These issues create barriers to adoption and pose difficulties in scaling edge computing solutions across different industries.

03 Who are the major players in the global edge computing market?

Key players in the global edge computing market include Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and IBM. These companies dominate the market due to their strong cloud-to-edge solutions, extensive global reach, and continuous investment in innovative edge computing technologies.

04 What are the growth drivers of the global edge computing market?

The global edge computing market is propelled by the increasing adoption of 5G networks, the rapid rise of IoT devices, and the integration of AI at the edge. These factors enhance real-time data processing and are crucial for industries like healthcare, manufacturing, and telecommunications.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.