Global Electronics Components Market Outlook to 2030

Region:Global

Author(s):Vijay Kumar

Product Code:KROD5627

Region:Global

Author(s):Vijay Kumar

Product Code:KROD5627

December 2024

94

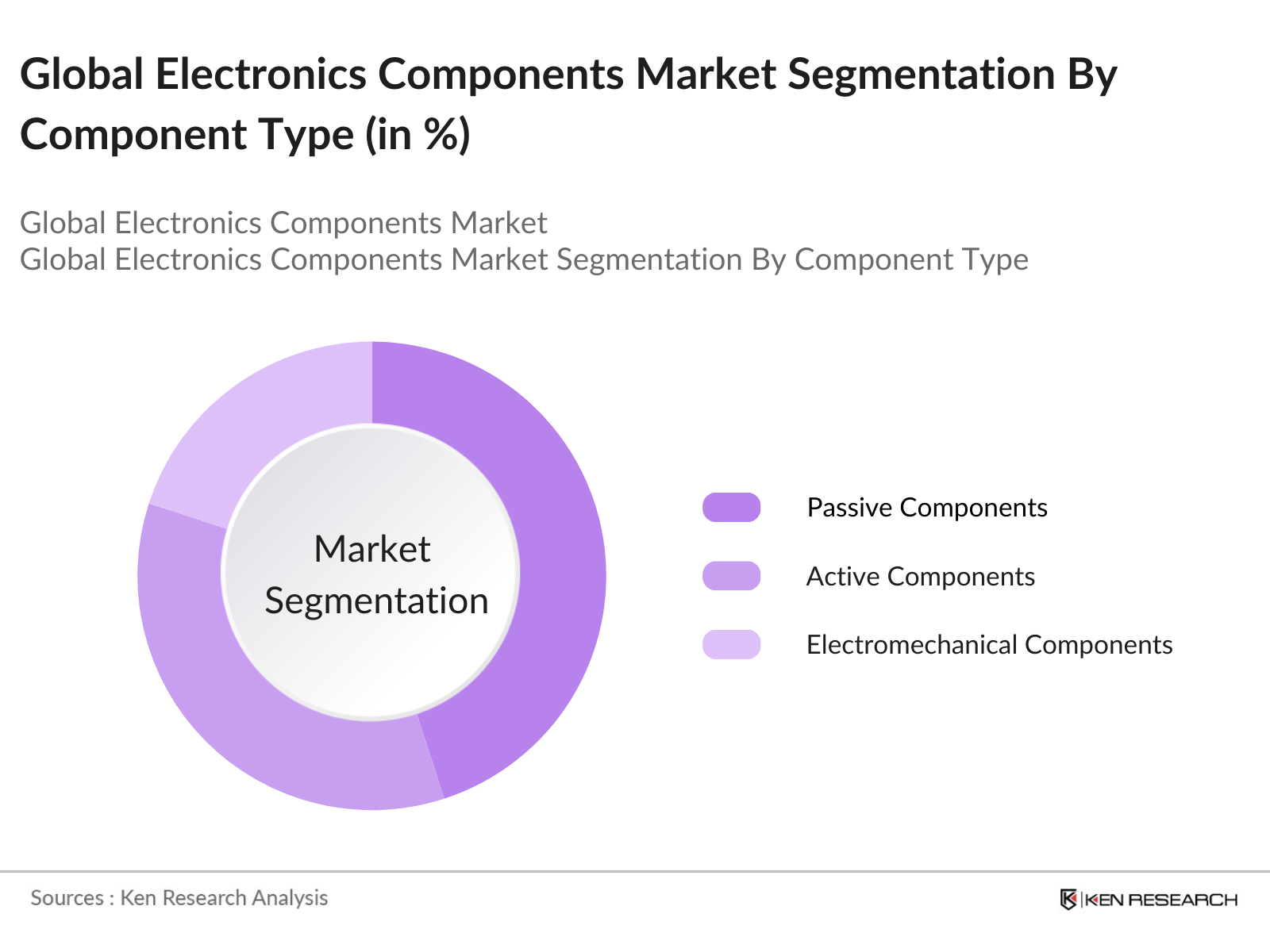

By Component Type: The market is segmented by component type into passive components, active components, and electromechanical components. Passive components, including resistors, capacitors, and inductors, dominate the market share due to their widespread use across various industries, especially in consumer electronics and telecommunications.

By Application: The market is segmented by application into automotive electronics, consumer electronics, telecommunications, industrial electronics, and medical devices. Consumer electronics hold the largest share of the market due to the continuous demand for smartphones, tablets, laptops, and wearables. The integration of advanced technologies such as artificial intelligence, IoT, and cloud computing into these devices has further fueled their demand, driving the market for electronic components.

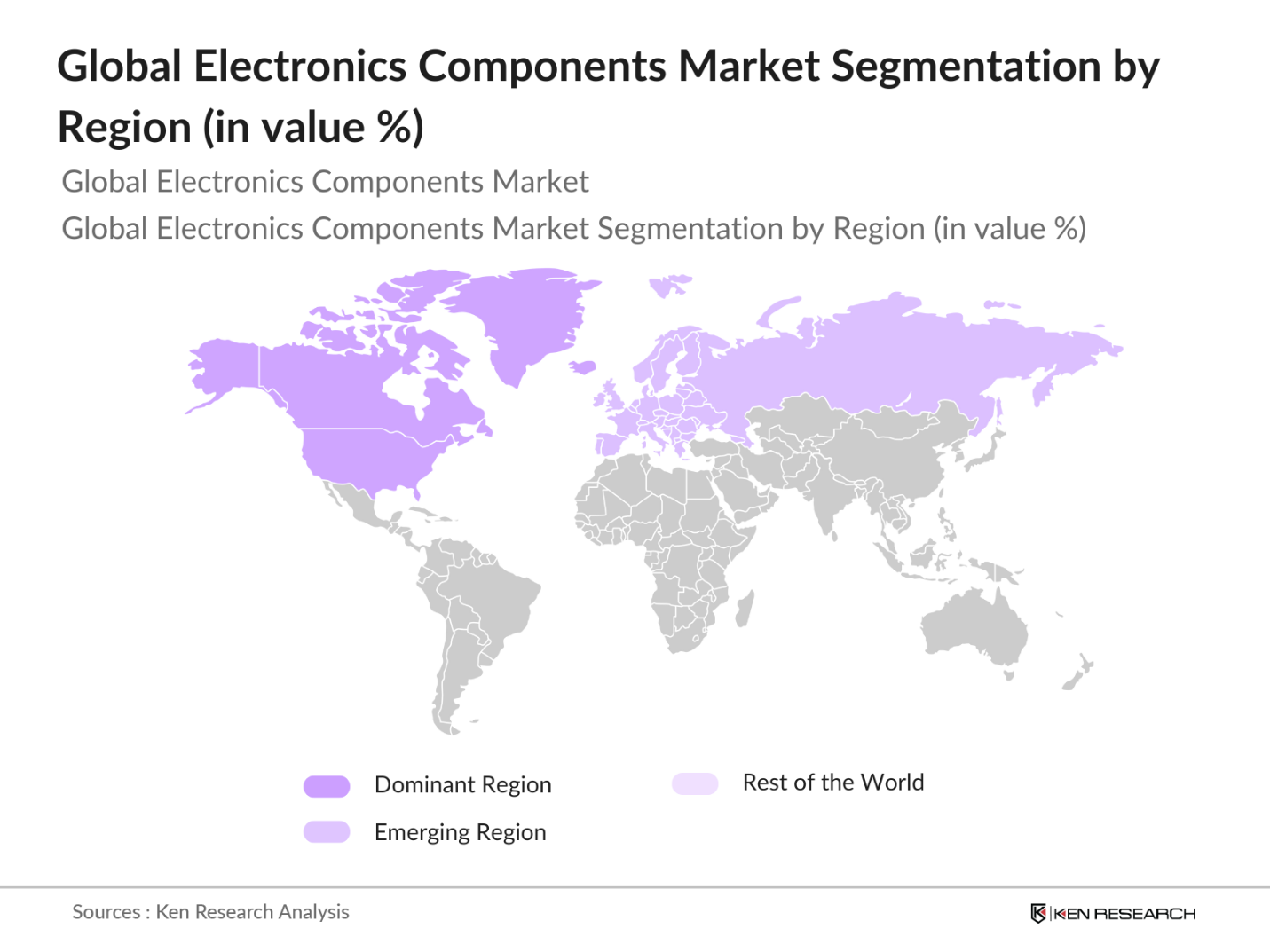

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific leads the market due to its strong manufacturing capabilities and the presence of leading electronic component manufacturers in countries like China, Japan, and South Korea. The availability of raw materials, low labor costs, and strong governmental support for the electronics industry in these countries also contribute to the region's dominance.

The global electronics components market is dominated by a mix of established global players and specialized manufacturers. Major companies leverage innovation, strategic partnerships, and heavy R&D investments to maintain their competitive advantage. For instance, companies like Intel and Samsung are focusing on developing cutting-edge semiconductor technologies for AI and quantum computing applications.

Over the next five years, the global electronics components market is expected to witness significant growth, driven by the continuous advancements in 5G technology, growing demand for electric vehicles, and the rising integration of AI in consumer and industrial electronics. Increasing investment in renewable energy infrastructure and smart cities will also spur demand for electronic components, particularly in the power electronics and sensor segments.

|

By Component Type |

Passive Components Active Components Electromechanical Components |

|

By Application |

Automotive Electronics Consumer Electronics Telecommunications Industrial Electronics Medical Devices |

|

By Material Type |

Silicon-based Components Gallium Nitride (GaN) Components Silicon Carbide (SiC) Components |

|

By End User |

Original Equipment Manufacturers (OEMs) Aftermarket/Replacement Components |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (influenced by miniaturization trends, automation, and consumer electronics demand)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increased Demand for IoT Devices

3.1.2. Expansion of 5G Technology

3.1.3. Rising Adoption of Electric Vehicles (EVs)

3.1.4. Technological Advancements in AI and Machine Learning

3.2. Market Challenges

3.2.1. Semiconductor Shortage

3.2.2. Complex Supply Chain Dependencies

3.2.3. Environmental and Regulatory Compliance (RoHS, WEEE)

3.3. Opportunities

3.3.1. Growth in Renewable Energy Applications

3.3.2. Expanding Smart Cities Initiatives

3.3.3. Global Expansion of Data Centers

3.4. Trends

3.4.1. Rising Demand for Miniaturized Components

3.4.2. Advanced Packaging Solutions

3.4.3. Increasing Investment in R&D for Quantum Computing

3.5. Government Regulation

3.5.1. Regional Trade Agreements (impacting tariffs and component sourcing)

3.5.2. Environmental Regulations (RoHS, REACH, conflict minerals compliance)

3.5.3. Standards for Electronic Components (IPC, JEDEC)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Suppliers, OEMs, Distributors)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Component Type (In Value %)

4.1.1. Passive Components (Resistors, Capacitors, Inductors)

4.1.2. Active Components (Semiconductors, Diodes, Transistors)

4.1.3. Electromechanical Components (Relays, Switches, Connectors)

4.2. By Application (In Value %)

4.2.1. Automotive Electronics

4.2.2. Consumer Electronics

4.2.3. Telecommunications

4.2.4. Industrial Electronics

4.2.5. Medical Devices

4.3. By Material Type (In Value %)

4.3.1. Silicon-based Components

4.3.2. Gallium Nitride (GaN) Components

4.3.3. Silicon Carbide (SiC) Components

4.4. By End User (In Value %)

4.4.1. Original Equipment Manufacturers (OEMs)

4.4.2. Aftermarket/Replacement Components

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1. Intel Corporation

5.1.2. Samsung Electronics

5.1.3. Qualcomm Technologies

5.1.4. Texas Instruments

5.1.5. Murata Manufacturing Co. Ltd.

5.1.6. NXP Semiconductors

5.1.7. Vishay Intertechnology

5.1.8. Infineon Technologies AG

5.1.9. STMicroelectronics

5.1.10. TDK Corporation

5.1.11. Analog Devices, Inc.

5.1.12. Broadcom Inc.

5.1.13. Rohm Semiconductor

5.1.14. Kyocera Corporation

5.1.15. Yageo Corporation

5.2 Cross Comparison Parameters (Revenue, Component Types, Technology Focus, Market Share, R&D Investments, No. of Employees, Global Reach, Product Portfolio)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards (RoHS, WEEE, REACH)

6.2. Compliance Requirements (Conflict Minerals, Trade Regulations)

6.3. Certification Processes (ISO 9001, ISO/TS 16949)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Component Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material Type (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In the initial phase, we identified key variables influencing the global electronics components market through extensive desk research. This included mapping the ecosystem with stakeholders such as manufacturers, suppliers, and OEMs, leveraging secondary databases and proprietary information to understand market dynamics.

During this phase, historical data on market performance was compiled and analyzed. The analysis included evaluating market penetration rates, demand trends across industries, and revenue patterns, ensuring the accuracy of estimates.

The market hypotheses were validated through consultations with industry experts. These experts provided first-hand insights into market trends, operational challenges, and financial performance, which helped refine the market projections.

The final step involved synthesizing the research findings into a comprehensive market analysis. This included acquiring detailed insights from manufacturers and comparing the results with the data obtained through a bottom-up approach to ensure the final output was robust and credible.

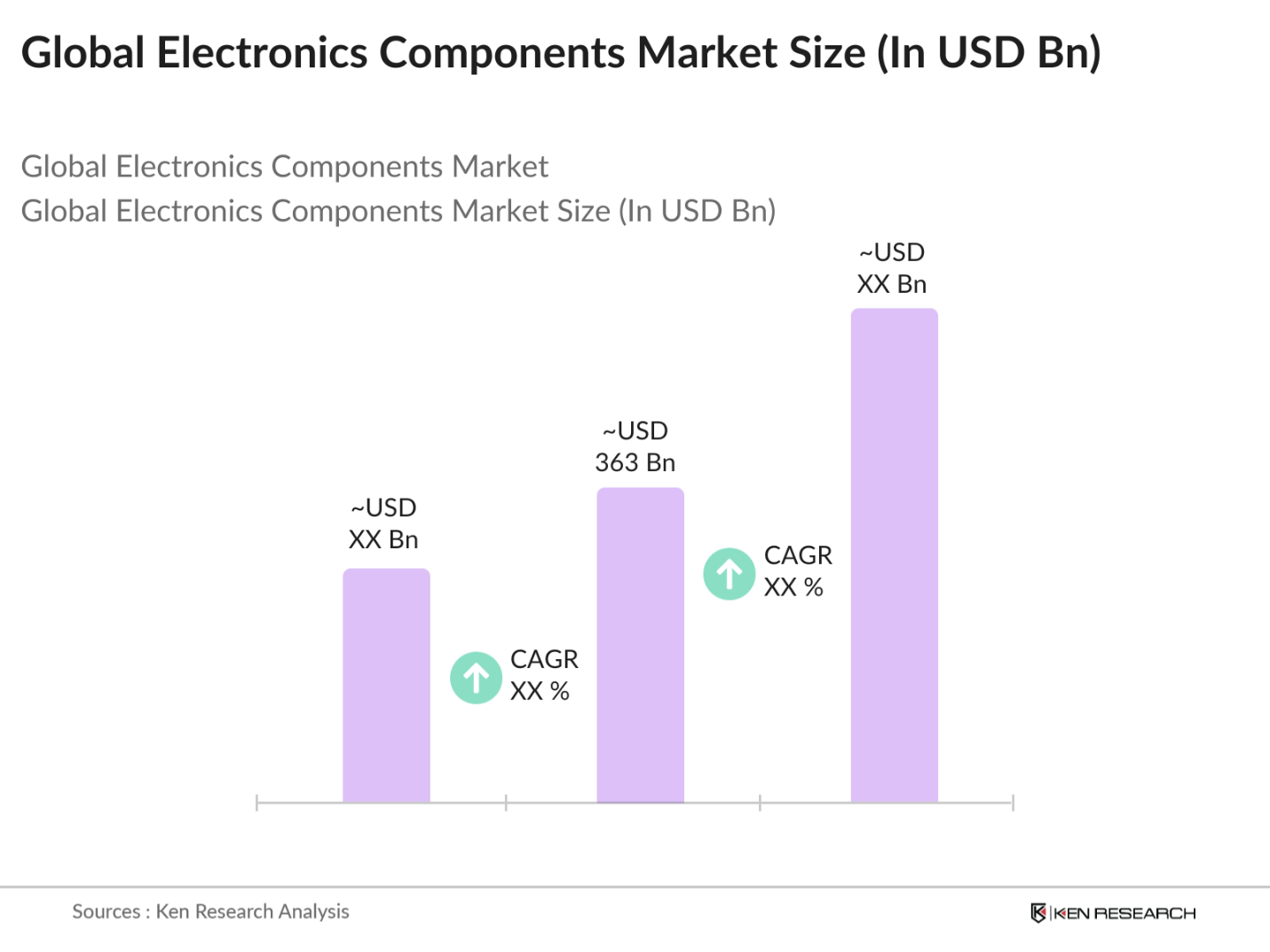

The Global Electronics Components Market is valued at USD 363 billion, based on a five-year historical analysis. This market's growth is driven by the increased demand for miniaturized, efficient components across industries like consumer electronics, automotive, and telecommunications.

Challenges in the market include supply chain disruptions, the ongoing semiconductor shortage, and regulatory compliance requirements like RoHS and REACH. Additionally, the high cost of raw materials has also affected the profitability of key players.

Key players include Intel Corporation, Samsung Electronics, Qualcomm Technologies, Murata Manufacturing, and Infineon Technologies. These companies dominate due to their innovation, global presence, and extensive product portfolios.

The market is driven by rising demand for consumer electronics, the rapid adoption of electric vehicles, the deployment of 5G networks, and increasing investments in renewable energy solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.