Global FDCA (Furan Dicarboxylic Acid) Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD8891

November 2024

94

About the Report

Global FDCA (Furan Dicarboxylic Acid) Market Overview

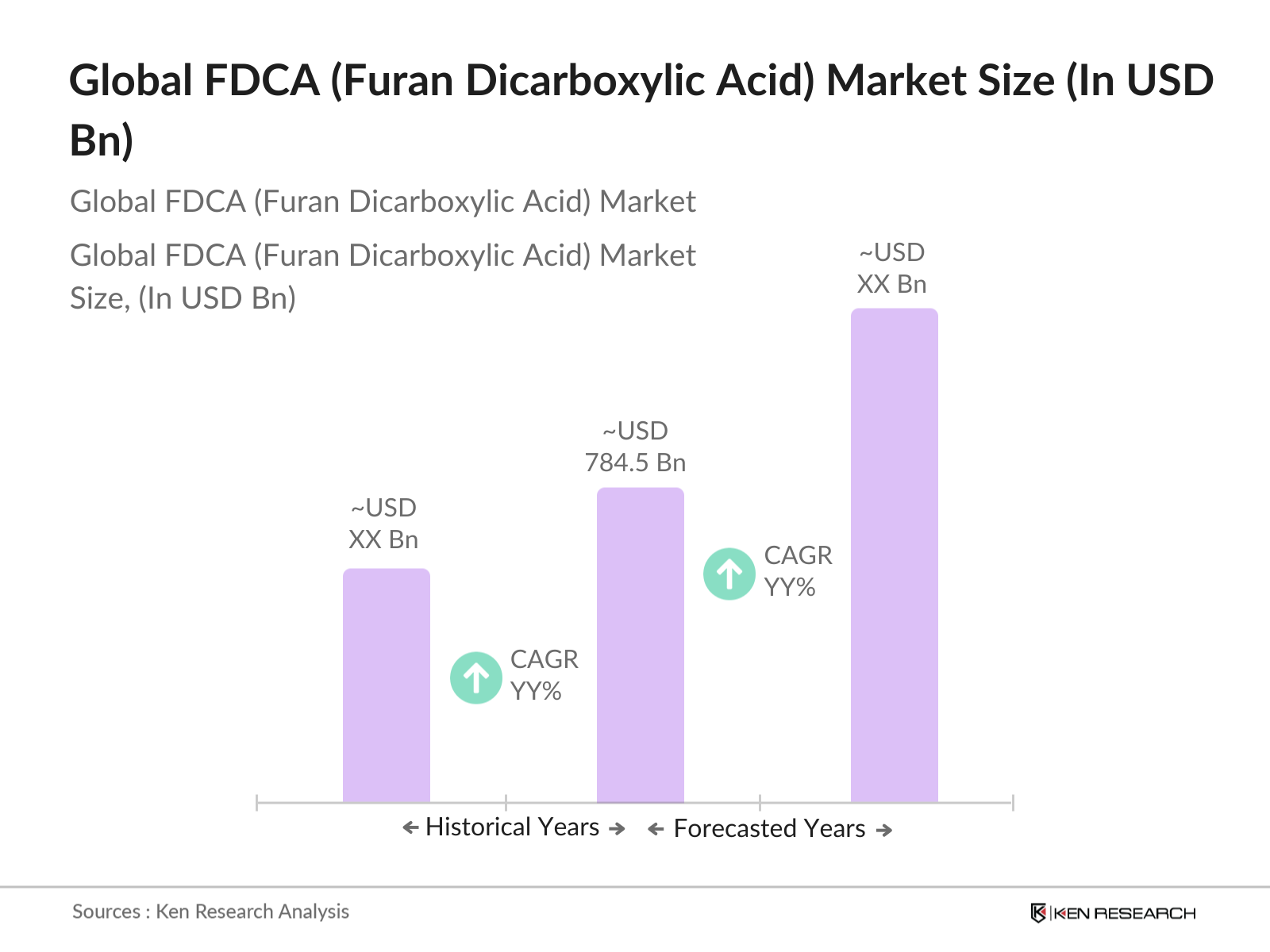

- The global FDCA (Furan Dicarboxylic Acid) market, valued at USD 784.5 billion, is driven by the increasing demand for bio-based alternatives to petroleum-based products. FDCA serves as a crucial component in the production of polyethylene furanoate (PEF), a bio-based plastic that has gained significant traction in the packaging industry due to its sustainability and superior barrier properties. The push for environmentally friendly materials is further bolstered by government regulations aimed at reducing plastic waste and carbon footprints.

- Countries such as the Netherlands, Germany, and the U.S. dominate the FDCA market. The Netherlands has emerged as a major hub due to investments in bioplastic innovations, with companies like Avantium leading the production of bio-based FDCA. Germany and the U.S. also hold significant market positions, driven by robust demand from the packaging and automotive industries, along with strong governmental support for bio-based solutions.

- In 2023, the U.S. Department of Energy provided substantial financial backing for the development of bio-based chemicals, including FDCA. Over $500 million was allocated to research and development initiatives aimed at boosting domestic production of bio-based materials and reducing dependency on petrochemical-based plastics. This financial support encourages companies to explore FDCA production and develop innovative bio-based solutions to meet sustainability goals.

Global FDCA (Furan Dicarboxylic Acid) Market Segmentation

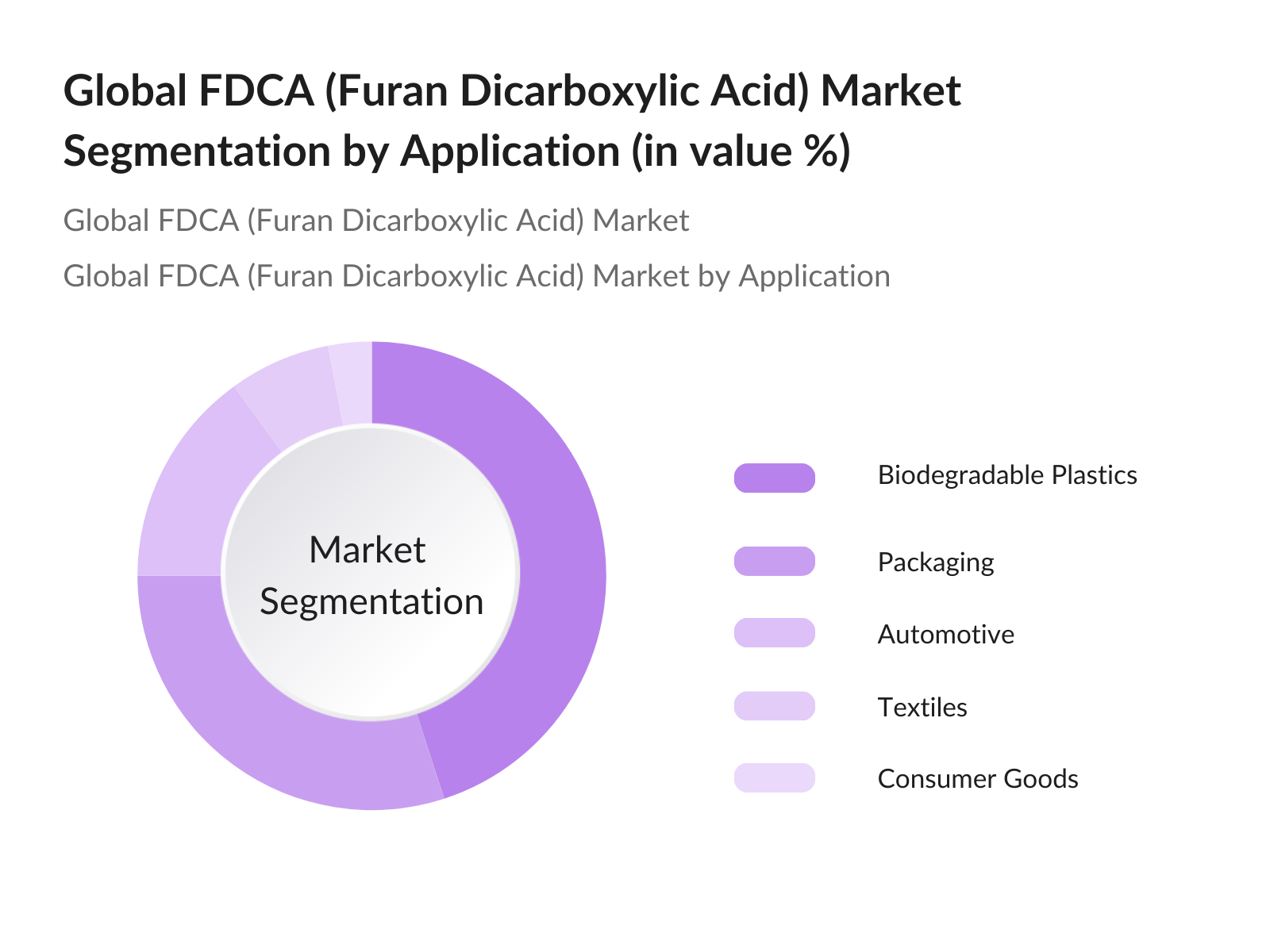

By Application: The FDCA market is segmented by application into biodegradable plastics, textiles, packaging, automotive, and consumer goods. Biodegradable plastics hold a dominant share in the market due to increasing consumer preference for eco-friendly alternatives. The use of FDCA in the production of PEF has further propelled demand, particularly in food packaging, where its superior barrier properties to gases and moisture have made it a preferred material. The automotive sector is also seeing growing adoption of FDCA due to its application in lightweight, sustainable materials.

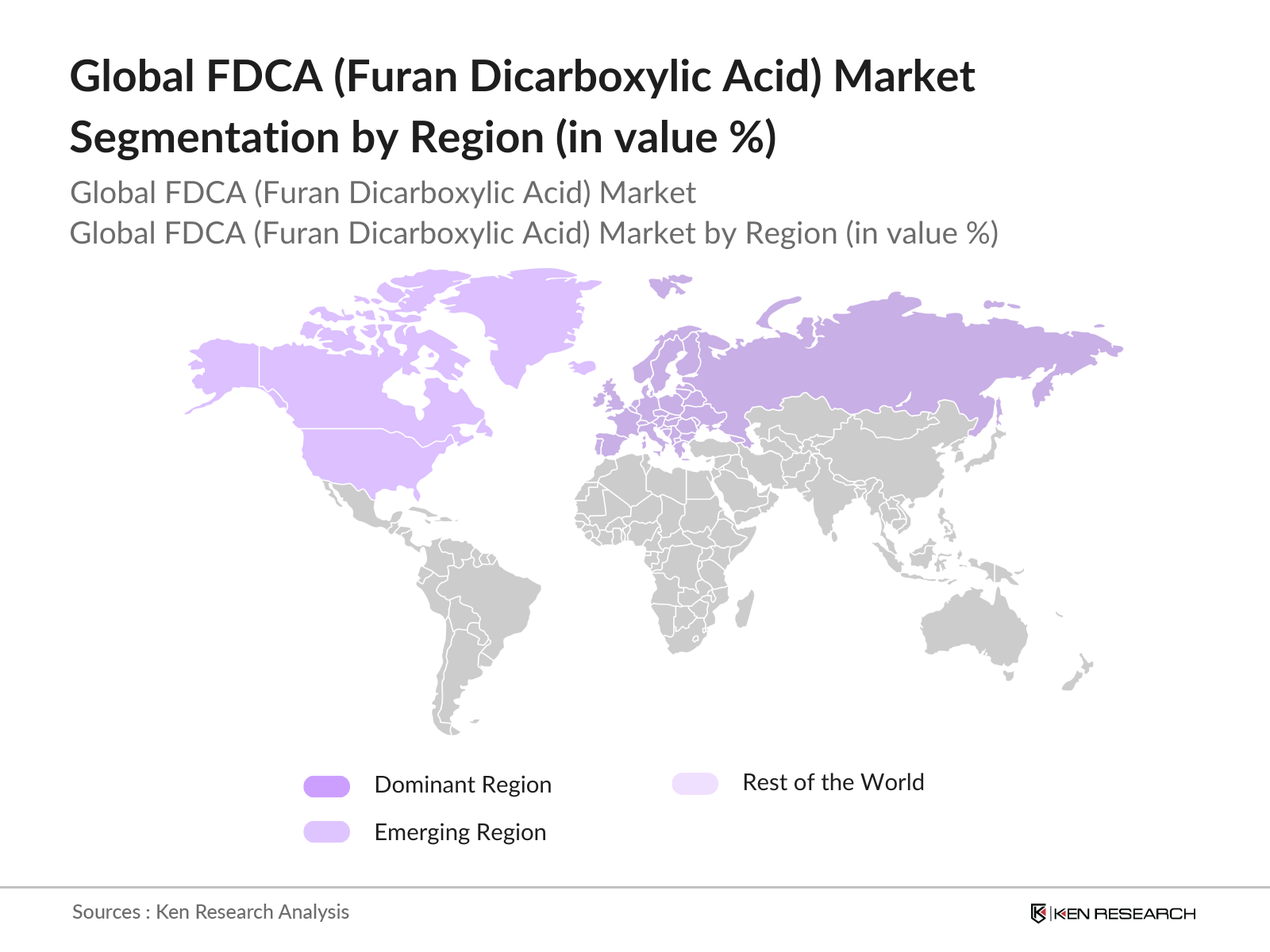

By Region: The Europe dominates the FDCA market, accounting for a significant share, driven by the region's strong environmental regulations and emphasis on sustainable materials. The European Union has set ambitious targets for reducing plastic waste, encouraging the adoption of bio-based plastics like PEF. North America follows closely, with the U.S. leading the market due to its substantial investments in bioplastic R&D and the automotive industry's shift toward sustainable materials.

Global FDCA (Furan Dicarboxylic Acid) Market Competitive Landscape

The FDCA market is dominated by both large and medium-sized players who utilize various strategies such as mergers, acquisitions, and partnerships to maintain their market positions. Companies like Avantium have made significant strides by securing funding for FDCA production facilities, while others like Corbion and Chemsky are investing in bio-based innovations to meet growing consumer demand for sustainable alternatives.

|

Company |

Establishment Year |

Headquarters |

R&D Investment |

Number of Employees |

Revenue (USD Mn) |

Key Product Lines |

Geographical Presence |

Key Partnerships |

|

Avantium |

2000 |

Amsterdam, Netherlands |

High |

- |

- |

- |

- |

- |

|

V & V Pharma Industries |

1995 |

Mumbai, India |

Medium |

- |

- |

- |

- |

- |

|

Carbone Scientific |

1999 |

Shanghai, China |

Medium |

- |

- |

- |

- |

- |

|

Chemsky International |

2003 |

Shanghai, China |

High |

- |

- |

- |

- |

- |

|

Corbion |

1919 |

Amsterdam, Netherlands |

High |

- |

- |

- |

- |

- |

Global FDCA (Furan Dicarboxylic Acid) Market Analysis

Market Growth Drivers:

- Expansion in Packaging and Bioplastics Industries (Market driver: Bio-based packaging)

The FDCA market is witnessing significant growth due to its rising application in the packaging and bioplastics industries, driven by the shift toward sustainable packaging solutions. According to World Bank data, global packaging waste reached over 2 billion tons annually in 2023, pushing industries to adopt bio-based materials like FDCA for packaging to reduce environmental impact. Bio-based packaging materials are now supported by governmental policies across regions like the EU and North America, which has led to an increase in demand for FDCA. These policies support FDCA-based bioplastics as alternatives to traditional plastics. - Sustainable Material Demand (Government regulations promoting bioplastics): The increasing global focus on reducing carbon footprints has created high demand for sustainable materials like FDCA. As per the 2022 UN Environment Program, global waste from plastic packaging amounted to 141 million metric tons, intensifying regulatory pressure. Governments are incentivizing bio-based plastic use, which has boosted FDCA production. In 2023, over 60 countries implemented restrictions on single-use plastics, increasing demand for bio-based alternatives such as FDCA-based packaging solutions. The surge in regulations supporting the transition to sustainable bioplastics is expected to expand FDCA applications in various industries.

- Technological Advancements in FDCA Production (Market driver: Process optimization): Technological advancements in FDCA production processes have streamlined the manufacturing efficiency and reduced dependency on petrochemical-based materials. In 2023, innovations in catalytic processes for FDCA production led to a 20% increase in yield, enhancing scalability for commercial use. These advancements are supported by collaborations between research institutes and industry players. Moreover, process optimization has led to a reduction in carbon emissions, aligning with the UNs Sustainable Development Goals (SDGs), thereby boosting FDCA adoption.

Market Challenges:

- High Production Costs of FDCA: The high cost of FDCA production remains a significant challenge for market expansion. In 2023, the average production cost of bio-based FDCA was notably higher than conventional petrochemical-based plastics. This is due to the expensive catalytic processes and the complexities of raw material sourcing required for FDCA production. Despite various governmental incentives aimed at promoting bio-based materials, the price disparity between FDCA and traditional plastics still acts as a barrier to widespread adoption. Industry players are actively exploring new cost-reduction strategies, yet achieving price competitiveness with petrochemical alternatives remains a challenge.

- Competition from Petrochemical Alternatives: FDCA faces stiff competition from conventional petrochemical-based plastics, which dominate the market due to their cost advantages and wide availability. In 2023, petrochemical plastics remained the primary choice for plastic production globally, with a significant share of the overall market. Despite growing environmental concerns, the lower costs and well-established supply chains of petrochemical plastics present a challenge for FDCA adoption. Additionally, the strong market presence of large petrochemical companies continues to influence pricing and supply dynamics, making it difficult for bio-based alternatives like FDCA to gain widespread traction.

Global FDCA (Furan Dicarboxylic Acid) Market Future Outlook

The FDCA market is set to experience substantial growth over the next five years, fueled by rising consumer awareness of sustainability, advancements in bio-based materials, and increased government support. Key sectors like packaging, automotive, and consumer goods will continue to be primary growth drivers, as these industries transition toward more eco-friendly alternatives. Europe is expected to remain a key player, but emerging markets in Asia-Pacific will see accelerated growth due to industrial expansion and increased focus on environmental sustainability.

Market Opportunities:

- Adoption of Bio-Based Polyethylene Furanoate (PEF): One of the most prominent trends in the FDCA market is the growing adoption of bio-based polyethylene furanoate (PEF), a polymer derived from FDCA. PEF is being increasingly used as a substitute for PET due to its superior barrier properties and biodegradability. In 2023, PEF saw rising applications in the beverage packaging industry, with global production reaching 30,000 tons, supported by Europes stringent regulations on plastic waste. The adoption of PEF is being promoted by its recyclability and reduced environmental impact compared to fossil-based plastics.

- Shift Toward Green Construction Materials: FDCA is being increasingly incorporated into sustainable construction materials, especially in the development of bio-based polymers used for building insulation and interior applications. The global shift toward green building practices has spurred interest in FDCA-based resins for construction purposes. According to the International Energy Agency, green building projects gained significant momentum in 2023, creating a growing opportunity for FDCA in the construction sector.

Scope of the Report

|

By Application |

Biodegradable Plastics Packaging Textiles Automotive Consumer Goods |

|

By Type |

0.98 Purity 0.99 Purity |

|

By Production Method |

Catalytic Conversion of Sugars Biological Conversion of HMF Oxidation of Furans |

|

By End-User Industry |

Packaging Automotive Textiles Electronics Pharmaceuticals |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Government and Regulatory Bodies (e.g., European Commission, U.S. Environmental Protection Agency)

Chemical Manufacturers

Bioplastics Producers

Packaging Companies

Automotive Manufacturers

Consumer Goods Companies

Investments and Venture Capitalist Firms

Raw Material Suppliers

Companies

Players Mention in the Report

Avantium

V & V Pharma Industries

Carbone Scientific

Chemsky International

Corbion

Synbias Pharma

TCI Chemicals Pvt. Ltd.

BioAmber, Inc.

Eastman Chemical Company

AstaTech

AVA Biochem AG

Novamont SpA

Tokyo Chemical Industry Co. Ltd.

Cargill, Inc.

Henkel

Table of Contents

01. Global FDCA Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

02. Global FDCA Market Size (In USD Million)

2.1 Historical Market Size

2.2 Key Market Developments and Milestones

2.3 Year-On-Year Growth Analysis

03. Global FDCA Market Analysis

3.1 Growth Drivers

3.1.1 Expansion in Packaging and Bioplastics Industries (Market driver: Bio-based packaging)

3.1.2 Sustainable Material Demand (Government regulations promoting bioplastics)

3.1.3 Technological Advancements in FDCA Production (Market driver: Process optimization)

3.2 Market Challenges

3.2.1 High Production Costs of FDCA

3.2.2 Limited Feedstock Availability (Raw material sourcing constraints)

3.2.3 Competition from Petrochemical Alternatives

3.3 Opportunities

3.3.1 Growing Consumer Preference for Eco-Friendly Products

3.3.2 Strategic Collaborations and Partnerships (Industry partnerships for bio-based materials)

3.3.3 Expansion into New Applications (Consumer goods, automotive sectors)

3.4 Trends

3.4.1 Adoption of Bio-Based Polyethylene Furanoate (PEF)

3.4.2 Integration of FDCA in Circular Economy Models

3.4.3 Shift Toward Green Construction Materials

3.5 Government Regulations

3.5.1 Regulations on Plastic Waste Reduction

3.5.2 Incentives for Bio-based Product Development

3.5.3 Certification Requirements for Bio-based Plastics

3.6 SWOT Analysis

3.7 Porters Five Forces

3.8 Stake Ecosystem

04. Global FDCA Market Segmentation

4.1 By Application (In Value %)

4.1.1 Biodegradable Plastics

4.1.2 Textiles

4.1.3 Packaging

4.1.4 Automotive

4.1.5 Consumer Goods

4.2 By Type (In Value %)

4.2.1 0.98 Purity

4.2.2 0.99 Purity

4.3 By Region (In Value %)

4.3.1 North America

4.3.2 Europe

4.3.3 Asia-Pacific

4.3.4 Latin America

4.3.5 Middle East & Africa

4.4 By Production Method (In Value %)

4.4.1 Catalytic Conversion of Sugars

4.4.2 Biological Conversion of HMF

4.4.3 Oxidation of Furans

05. Global FDCA Market Competitive Analysis

5.1 Detailed Profiles of Major Companies (Company Name, Headquarters, Revenue)

5.1.1 Avantium

5.1.2 V & V Pharma Industries

5.1.3 Carbone Scientific

5.1.4 Chemsky International

5.1.5 Synbias Pharma

5.1.6 TCI Chemicals Pvt. Ltd.

5.1.7 Corbion

5.1.8 Novamont SpA

5.1.9 AVA Biochem AG

5.1.10 BioAmber, Inc.

5.1.11 AstaTech

5.1.12 Eastman Chemical Company

5.1.13 Cargill, Inc.

5.1.14 Avantium Renewable Polymers

5.1.15 Tokyo Chemical Industry Co., Ltd.

5.2 Cross-Comparison Parameters (No. of Employees, Headquarters, Revenue, Application Diversity)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Collaborations, Mergers & Acquisitions)

5.5 Investment Analysis

5.6 Venture Capital Funding

5.7 Government Grants and Incentives

5.8 R&D Investments

06. Global FDCA Market Regulatory Framework

6.1 Global Environmental Standards

6.2 Compliance and Certification Processes

6.3 Government Incentives for Bio-based Materials

07. Global FDCA Future Market Size (In USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Growth

08. Global FDCA Future Market Segmentation

8.1 By Application (In Value %)

8.2 By Region (In Value %)

09. Global FDCA Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step involved mapping the FDCA market ecosystem, considering major stakeholders such as packaging companies and automotive manufacturers. A combination of proprietary databases and secondary research was used to collect data on market trends, demand, and supply dynamics.

Step 2: Market Analysis and Construction

Historical data were analyzed to identify market penetration across different industries. Factors such as adoption of bio-based materials and regional market size were evaluated, leading to an accurate estimation of FDCA market revenue.

Step 3: Hypothesis Validation and Expert Consultation

The hypothesis regarding the future of bio-based materials in packaging was validated through interviews with experts from companies like Avantium and Corbion. Their insights provided valuable information on R&D investments and strategic directions.

Step 4: Research Synthesis and Final Output

The research was finalized by triangulating data from manufacturers, industry reports, and expert opinions. This ensured the accuracy and comprehensiveness of the market analysis, ultimately forming the foundation of the FDCA market report.

Frequently Asked Questions

01. How big is the Global FDCA market?

The global FDCA market is valued at USD 784.5 billion, driven by the growing demand for bio-based materials across industries like packaging and automotive.

02. What are the challenges in the FDCA market?

Challenges include the high cost of production and the limited availability of biomass feedstock required for FDCA production, creating barriers for mass adoption.

03. Who are the major players in the FDCA market?

Key players include Avantium, V & V Pharma Industries, Carbone Scientific, Chemsky International, and Corbion. These companies dominate the market through innovation and strategic partnerships.

04. What is driving the growth of the FDCA market?

The primary growth drivers are the increasing demand for bio-based alternatives to petroleum-based plastics, advancements in FDCA production technologies, and regulatory support for sustainable materials.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.