Global Food Contract Manufacturing Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD10682

Region:Global

Author(s):Naman Rohilla

Product Code:KROD10682

December 2024

84

The food contract manufacturing market is competitive, with major players driving innovation and maintaining high standards of food quality and safety. Key players include both global and regional companies, with industry leaders setting benchmarks for quality and operational efficiency.

The global food contract manufacturing market is expected to witness substantial growth driven by the evolving consumer preference for processed and ready-to-eat food items. Increased awareness of clean-label and organic products is also anticipated to drive demand for specialized contract manufacturing services. Rising demand in emerging markets, such as Asia Pacific and Latin America, further indicates that food manufacturers will increasingly turn to contract services to meet expanding consumer bases and ensure cost-effective operations.

|

Segment |

Sub-Segments |

|

Product Type |

Bakery and Confectionery Beverages Dairy Products Meat and Seafood Snack Foods |

|

Service Type |

Packaging, Production R&D and Formulation Logistics and Warehousing |

|

Business Model |

Outsourcing Full-Service Contract Manufacturing |

|

Customer Type |

Food and Beverage Companies Retail Chains Private Label Brands |

|

Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Outsourcing Trends in Food Manufacturing

3.1.2. Demand for Cost-Effective Production

3.1.3. Expanding Food Product Portfolios

3.1.4. Rising Demand for Convenience Foods

3.2. Market Challenges

3.2.1. Quality Control and Compliance

3.2.2. Supply Chain Complexity

3.2.3. High Operational Costs

3.2.4. Limited Scalability for Customization

3.3. Opportunities

3.3.1. Growth in Organic and Specialty Foods

3.3.2. Expansion into Emerging Markets

3.3.3. Adoption of Technological Innovations

3.3.4. Partnerships with Retail Giants

3.4. Trends

3.4.1. Rise of Clean Label Manufacturing

3.4.2. Growth of Plant-Based Contract Manufacturing

3.4.3. Enhanced Focus on Sustainable Production

3.4.4. Implementation of Automation in Production Processes

3.5. Regulatory Landscape

3.5.1. Food Safety Standards (FDA, HACCP, ISO)

3.5.2. Labeling and Ingredient Disclosure Regulations

3.5.3. Environmental Compliance

3.5.4. Trade Tariffs and Export Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

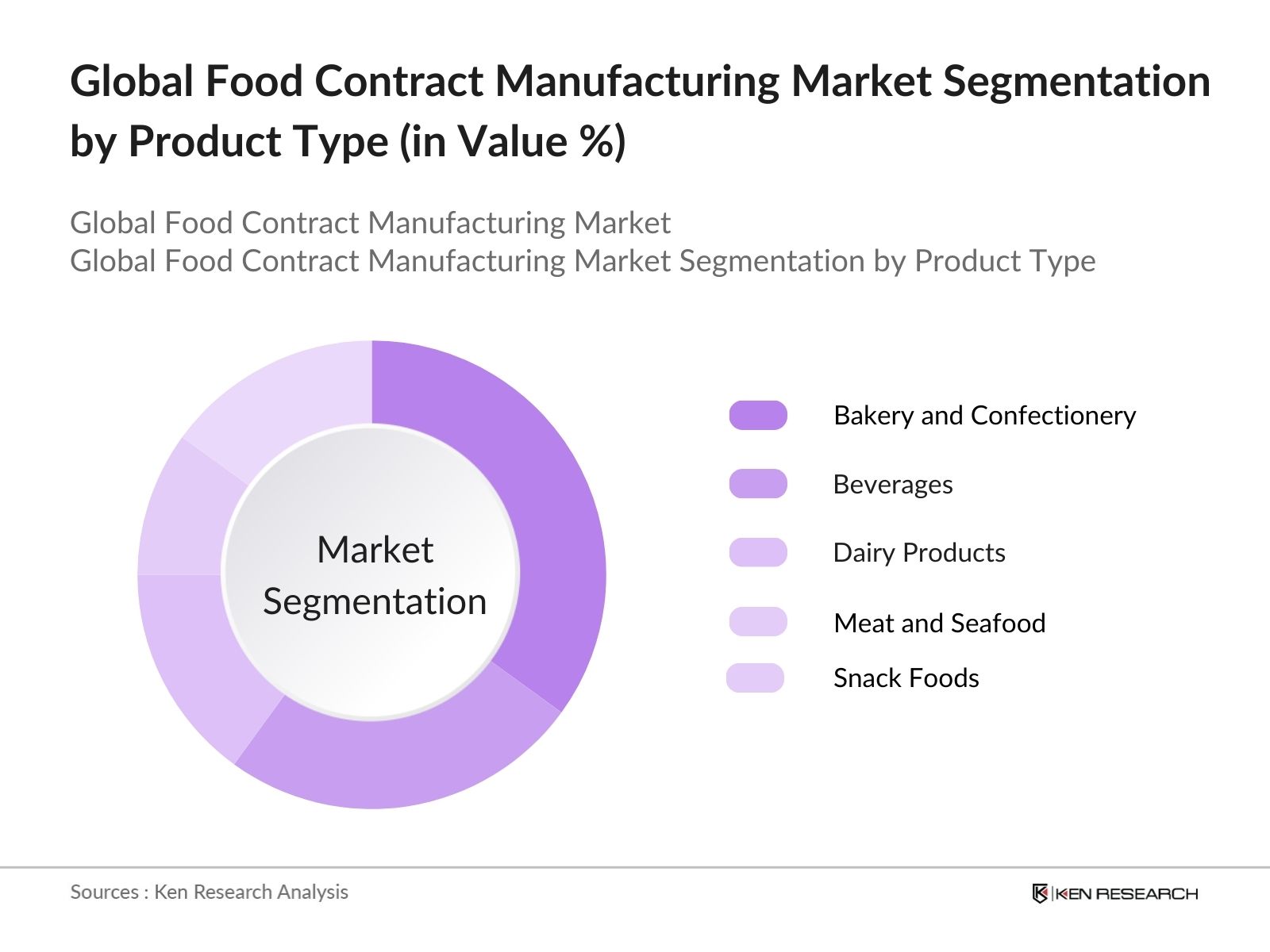

4.1. By Product Type (In Value %)

4.1.1. Bakery and Confectionery

4.1.2. Beverages

4.1.3. Dairy Products

4.1.4. Meat and Seafood

4.1.5. Snack Foods

4.2. By Service Type (In Value %)

4.2.1. Packaging

4.2.2. Production

4.2.3. R&D and Formulation

4.2.4. Logistics and Warehousing

4.3. By Business Model (In Value %)

4.3.1. Outsourcing

4.3.2. Full-Service Contract Manufacturing

4.4. By Customer Type (In Value %)

4.4.1. Food and Beverage Companies

4.4.2. Retail Chains

4.4.3. Private Label Brands

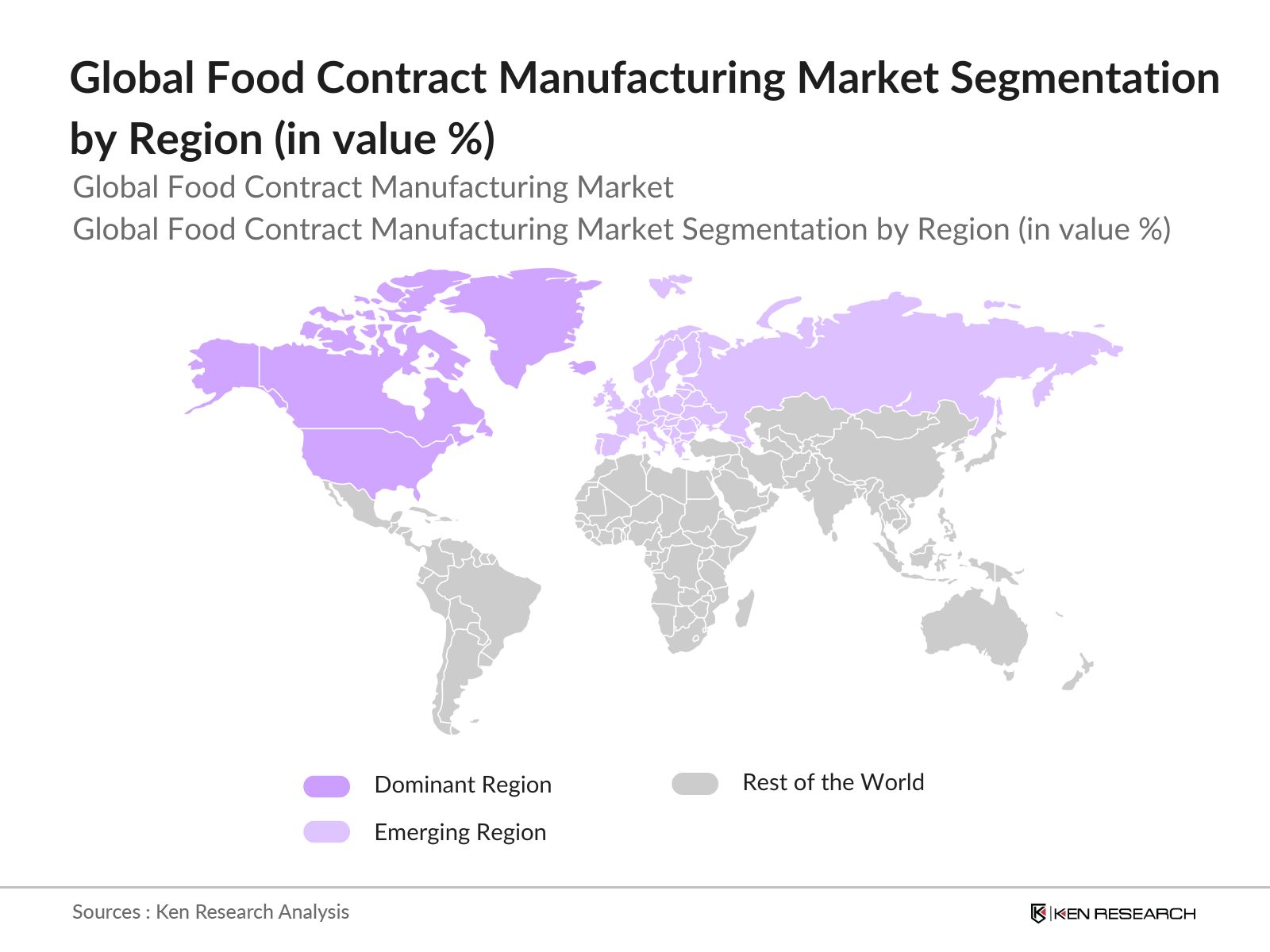

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Kerry Group

5.1.2. Archer Daniels Midland

5.1.3. Cargill Inc.

5.1.4. TreeHouse Foods Inc.

5.1.5. Gehl Foods

5.1.6. SunOpta Inc.

5.1.7. Hearthside Food Solutions LLC

5.1.8. SK Food Group

5.1.9. Crest Foods Co., Inc.

5.1.10. Reily Foods Company

5.1.11. PacMoore Products, Inc.

5.1.12. Oak State Products, Inc.

5.1.13. J&J Snack Foods Corp.

5.1.14. The Greenery B.V.

5.1.15. KanPak LLC

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Customer Base, Market Reach, Manufacturing Facilities, Certifications, Strategic Partnerships, R&D Investment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Incentives

5.9. Private Equity Investments

6.1. Compliance Standards

6.2. Certification Processes

6.3. Environmental Standards

6.4. Import and Export Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Service Type (In Value %)

8.3. By Business Model (In Value %)

8.4. By Customer Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

The first stage involved mapping out the global food contract manufacturing ecosystem. Comprehensive desk research was conducted using proprietary databases to identify essential market drivers, competitive structures, and trends.

This phase encompassed an in-depth analysis of historical data related to the global food contract manufacturing market. Key metrics, such as production volumes, consumer demographics, and revenue generation, were analyzed to establish accurate projections.

To validate market hypotheses, expert consultations were conducted with representatives from top contract manufacturing firms. Insights from these experts provided a clearer understanding of operational and financial dynamics within the industry.

The final stage entailed synthesizing data from both quantitative and qualitative sources, ensuring that the report is grounded in accurate, validated insights. This comprehensive approach enabled a detailed examination of current and future market conditions.

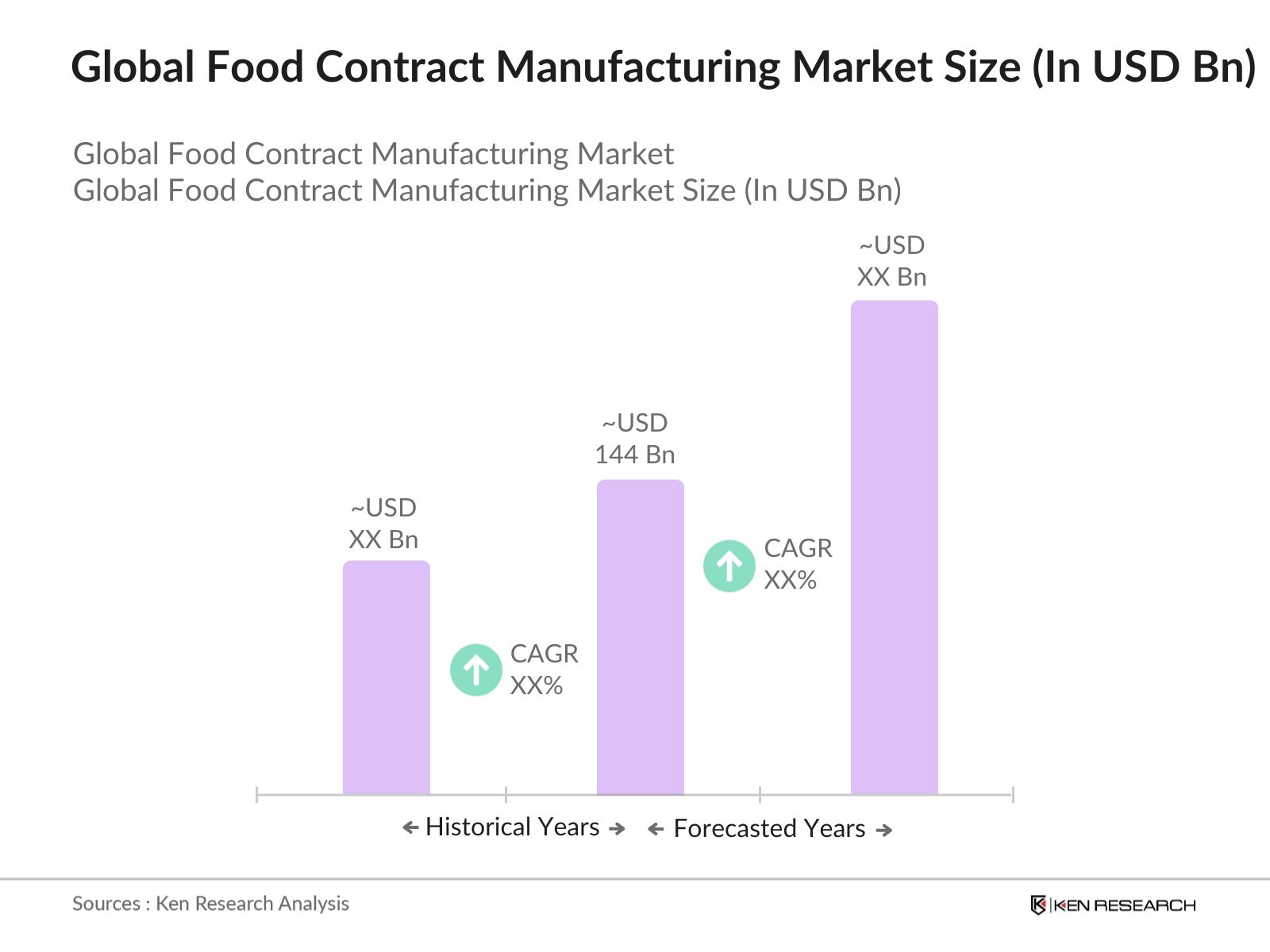

The global food contract manufacturing market was valued at USD 144 billion, driven by outsourcing trends and rising demand for specialty food products.

The market is propelled by the need for cost-efficient production, increased demand for clean-label products, and outsourcing by major food brands to optimize operations.

Key players include Kerry Group, Archer Daniels Midland, Cargill Inc., TreeHouse Foods, and Hearthside Food Solutions, who dominate due to their extensive production capabilities and strategic partnerships.

Key challenges include compliance with food safety standards, supply chain complexity, and the need for high scalability without compromising quality.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.