Global Furandicarboxylic Acid (FDCA) Market Outlook to 2030

Region:Global

Author(s):Shivani

Product Code:KROD10666

Region:Global

Author(s):Shivani

Product Code:KROD10666

November 2024

100

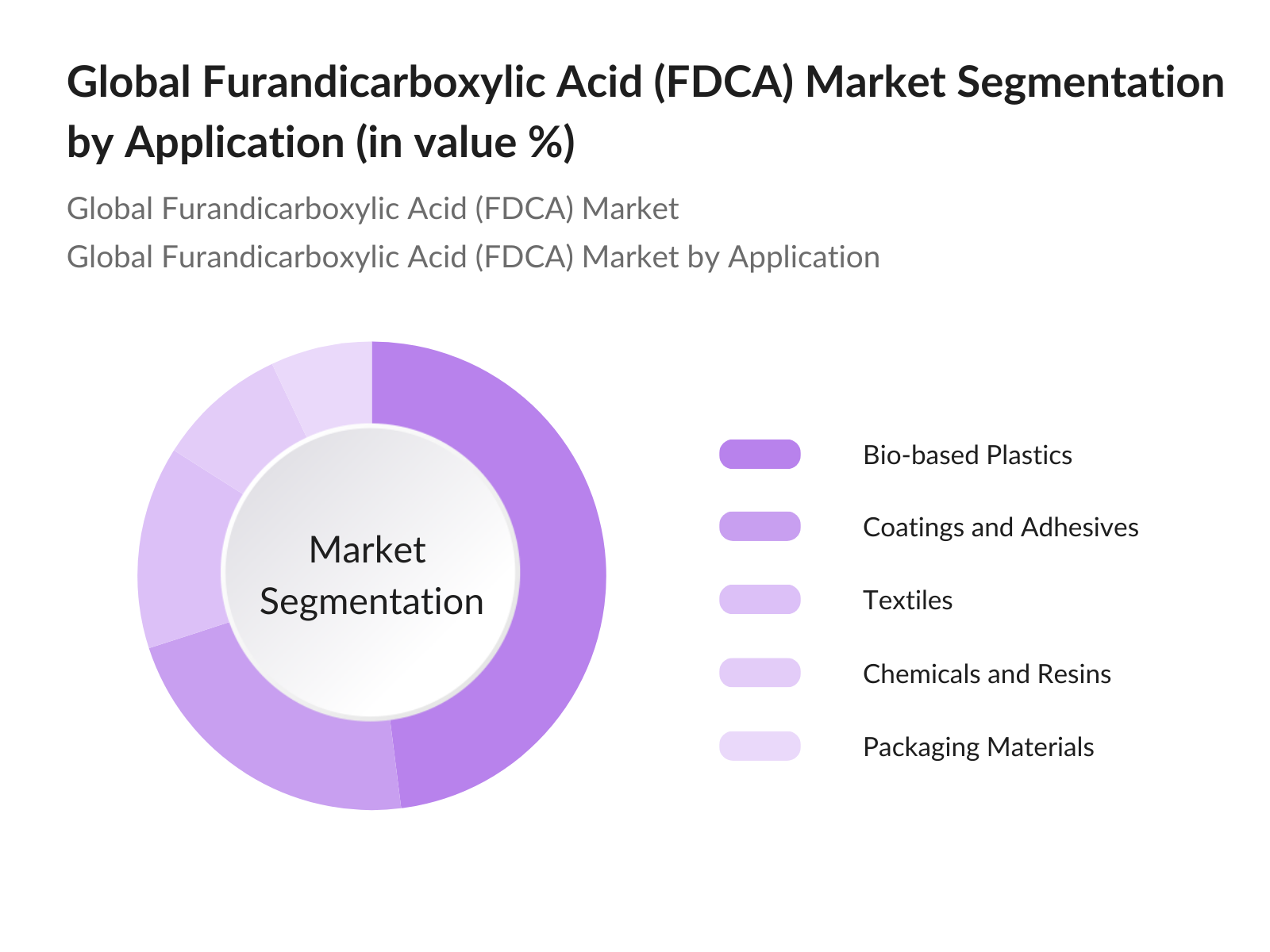

By Application: The Global Furandicarboxylic Acid Market is segmented by application into bio-based plastics, coatings and adhesives, textiles, chemicals and resins, and packaging materials. Among these, bio-based plastics hold the dominant market share. This dominance stems from the increasing global demand for sustainable packaging and the move away from petrochemical-based plastics. PEF, derived from FDCA, is a key driver in this category due to its superior performance compared to PET, especially in terms of oxygen barrier and mechanical strength, making it suitable for beverage bottles and other packaging applications.

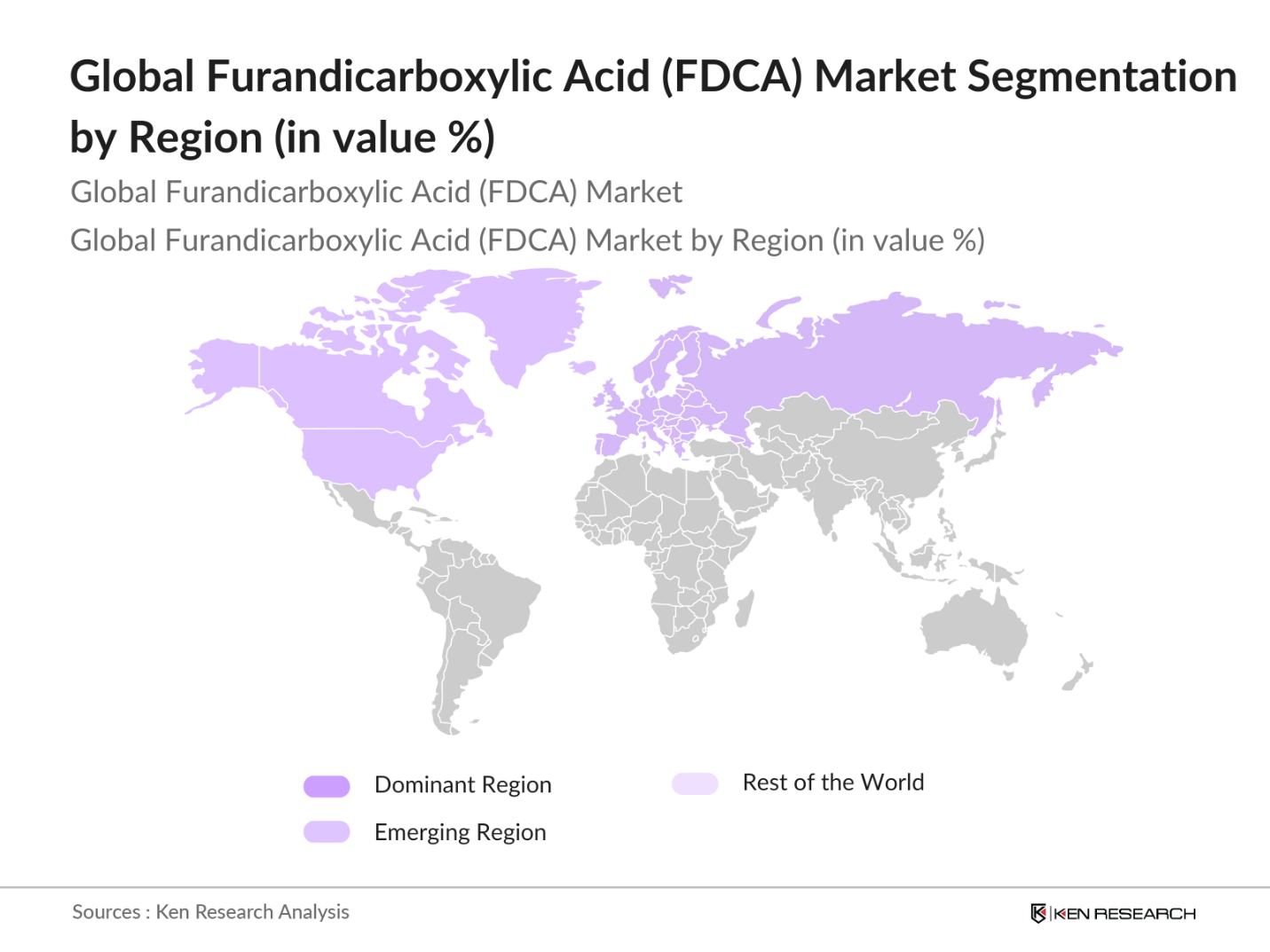

By Region: The Global Furandicarboxylic Acid Market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Europe holds the largest market share, driven bys regulatory frameworks that promote the use of bio-based plastics and a strong emphasis on sustainability in packaging and consumer goods. Countries such as the Netherlands and Germany lead the European market, supported by significant government initiatives and investments in green chemistry.

The FDCA market is dominated by a select group of companies that play a pivotal role in shaping market trends. These firms are characterized by strong R&D investments and a focus on expanding FDCA applications across various industries, particularly in bio-based plastics. The market's competitive landscape is highly concentrated, with a few players holding significant shares in terms of production capacity and market influence.

|

Company Name |

Establishment Year |

Headquarters |

Manufacturing Capacity |

Key Product Lines |

Patents Filed |

Revenue (2023) |

Market Expansion Focus |

R&D Investment (%) |

Partnerships |

|

Avantium N.V. |

2000 |

Netherlands |

High |

- |

- |

- |

- |

- |

- |

|

Corbion |

1919 |

Netherlands |

Medium |

- |

- |

- |

- |

- |

- |

|

BASF SE |

1865 |

Germany |

High |

- |

- |

- |

- |

- |

- |

|

DuPont de Nemours, Inc. |

1802 |

USA |

High |

- |

- |

- |

- |

- |

- |

|

Mitsubishi Chemical Corp |

1933 |

Japan |

Medium |

- |

- |

- |

- |

- |

- |

Over the next five years, the Global Furandicarboxylic Acid market is expected to show significant growth driven by the increasing shift towards bio-based materials and government regulations promoting sustainable products. The growing application of FDCA in packaging, automotive, and consumer goods sectors is anticipated to play a major role in driving market expansion. Moreover, advancements in FDCA production technologies, particularly fermentation-based processes, will help reduce production costs and boost the commercialization of FDCA-derived products.

|

By Application |

Bio-based Plastics Coatings & Adhesives Textiles Chemicals & Resins Packaging Materials |

|

By Product Type |

Dimethyl Furandicarboxylate (DMFDC) Polyethylene Furanoate (PEF) Others |

|

By Technology |

Catalytic Oxidation Fermentation-Based Processes |

|

By End-Use Industry |

Packaging Automotive Pharmaceuticals Consumer Goods Electronics |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Adoption in Bio-based Plastics

3.1.2. Rising Environmental Regulations (Furandicarboxylic Acid as Biodegradable Polymer)

3.1.3. Increasing Demand for Sustainable Packaging

3.1.4. Technological Innovations in FDCA Production (Catalyst Efficiency, Fermentation Technology)

3.2. Market Challenges

3.2.1. High Production Costs Compared to Petrochemical Derivatives

3.2.2. Limited Commercial Scale of Production

3.2.3. Lack of Awareness in End-Use Industries

3.3. Opportunities

3.3.1. Expansion into High-Performance Materials (Polyesters, Polyamides)

3.3.2. Collaboration with Major Beverage Brands for Bioplastic Bottles

3.3.3. Advancements in Green Chemistry and Sustainable Manufacturing

3.4. Trends

3.4.1. Shift towards Circular Economy and Closed-Loop Systems (Recycling FDCA-based Polymers)

3.4.2. Increasing R&D Investments in Biobased Polymers

3.4.3. Growing Consumer Preference for Eco-friendly Products

3.5. Government Regulations

3.5.1. EU Single-Use Plastic Directive and Circular Economy Action Plan

3.5.2. U.S. Bioplastics Regulations and Federal Funding for Biodegradable Materials

3.5.3. Asia-Pacific Environmental Packaging Norms

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape (Manufacturing Capacity, Patents Filed, Pricing Strategies)

4.1. By Application (In Value %)

4.1.1. Bio-based Plastics

4.1.2. Coatings and Adhesives

4.1.3. Textiles

4.1.4. Chemicals and Resins

4.1.5. Packaging Materials

4.2. By Product Type (In Value %)

4.2.1. Dimethyl Furandicarboxylate (DMFDC)

4.2.2. Polyethylene Furanoate (PEF)

4.2.3. Others

4.3. By Technology (In Value %)

4.3.1. Catalytic Oxidation

4.3.2. Fermentation-Based Processes

4.4. By End-Use Industry (In Value %)

4.4.1. Packaging

4.4.2. Automotive

4.4.3. Pharmaceuticals

4.4.4. Consumer Goods

4.4.5. Electronics

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies (Headquarters, Employees, Market Share)

5.1.1. Avantium N.V.

5.1.2. Corbion

5.1.3. Mitsubishi Chemical Holdings Corporation

5.1.4. Synvina C.V.

5.1.5. BASF SE

5.1.6. Eastman Chemical Company

5.1.7. Tokyo Chemical Industry Co., Ltd.

5.1.8. Origin Materials

5.1.9. DuPont de Nemours, Inc.

5.1.10. NatureWorks LLC

5.1.11. PTT Global Chemical Public Company Limited

5.1.12. Metabolix, Inc.

5.1.13. Danimer Scientific

5.1.14. Novamont S.p.A.

5.1.15. Futerro

5.2. Cross Comparison Parameters (Market Share, Manufacturing Capacity, Research Focus, Biopolymer Patents, Revenue, Market Expansion)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6.1. Environmental Regulations on Bioplastics (FDA, EU, EPA Certifications)

6.2. Import/Export Compliance Regulations

6.3. Certification Processes for Biodegradable Polymers

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Application (In Value %)

8.2. By Product Type (In Value %)

8.3. By Technology (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Product Innovation Strategy

9.3. White Space Opportunity Analysis

9.4. End-Use Market Penetration Strategies

In the first step, an ecosystem map was created to identify all major stakeholders in the Global Furandicarboxylic Acid market. This phase involved extensive desk research from proprietary databases and government reports, identifying key variables such as market size, product adoption rates, and geographical demand.

Next, historical data pertaining to the market was collected, focusing on key metrics like production capacity, revenue generation, and material use in various industries. Data accuracy was ensured through cross-referencing of government statistics and industry publications.

A combination of CATIs and face-to-face interviews with industry experts was used to validate the initial market hypotheses. Experts from leading chemical companies provided insight into future market trends, competitive strategies, and technological innovations.

The final phase included synthesizing data from primary and secondary research, leading to a comprehensive analysis. Direct engagement with manufacturers and industry stakeholders ensured the accuracy and reliability of market estimates.

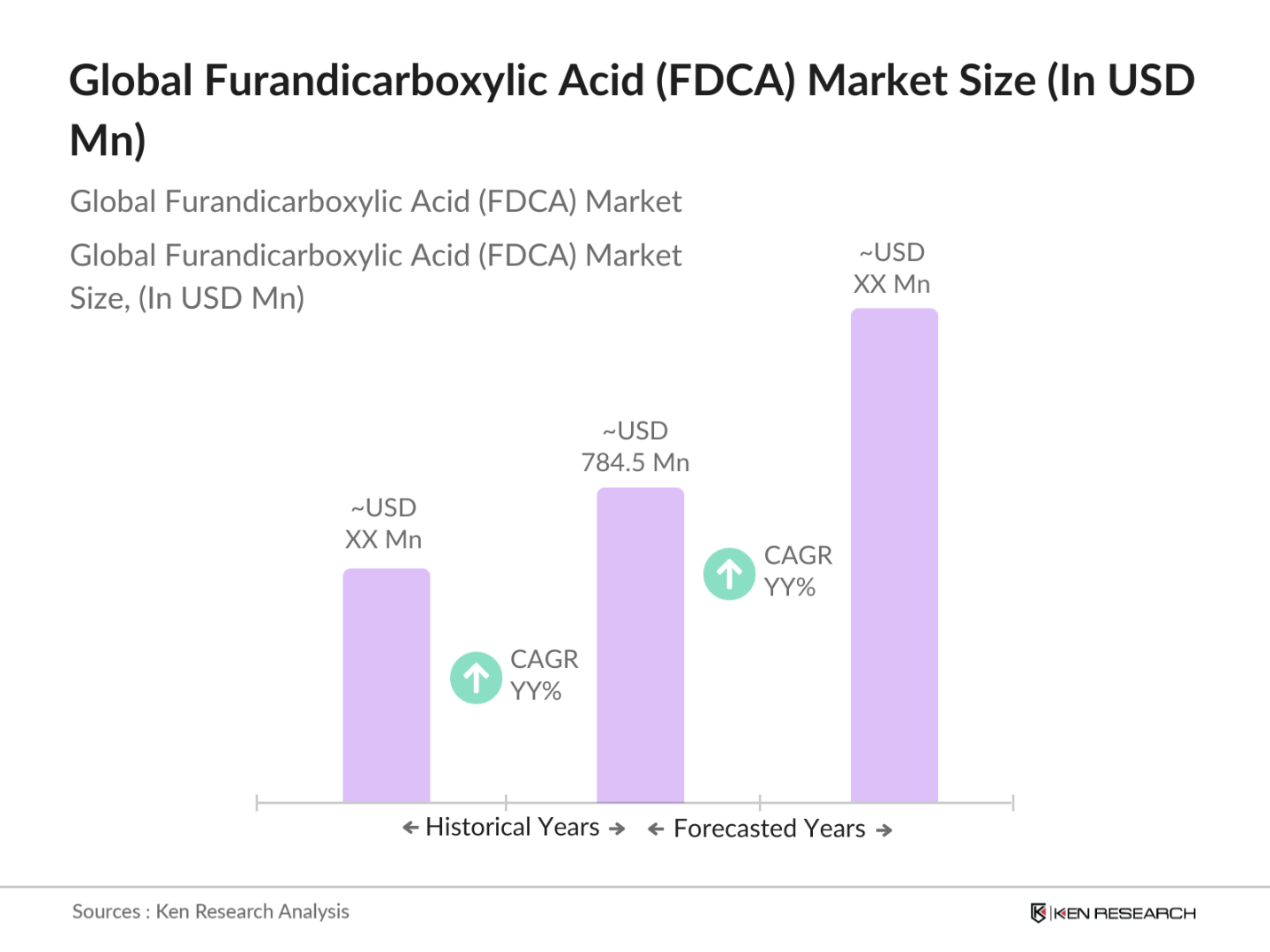

The global furandicarboxylic acid market is valued at approximately USD 784.5 million, driven by increasing demand for bio-based plastics and sustainable materials across industries.

Key challenges include high production costs compared to petrochemical alternatives and limited commercial-scale production, which could hinder broader market adoption.

Major players include Avantium, BASF SE, DuPont, Mitsubishi Chemical Corporation, and Corbion. These companies dominate the market through extensive R&D, strategic partnerships, and strong production capacities.

The market is driven by increasing regulations favoring eco-friendly materials, advancements in FDCA production technologies, and rising consumer demand for sustainable packaging solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.