Global Gas Engines Market Outlook to 2030

Region:Global

Author(s):Yogita Sahu

Product Code:KROD4933

Region:Global

Author(s):Yogita Sahu

Product Code:KROD4933

October 2024

83

By Engine Type: The market is segmented by engine type into reciprocating gas engines, gas turbines, microturbines, and Stirling engines. Reciprocating gas engines currently dominate the market, primarily due to their high efficiency in small to medium-scale applications such as distributed power generation and CHP. These engines are highly adaptable to various fuel types, including natural gas and biogas, making them a preferred choice across industries.

By Application: The market is segmented by application into power generation, cogeneration/CHP, industrial applications, and commercial buildings. Power generation holds the largest market share as gas engines are widely deployed for generating electricity in regions with grid reliability issues or for off-grid power solutions. Additionally, the industrial applications sub-segment, which includes sectors like oil & gas and manufacturing, is gaining traction due to the need for reliable and efficient power supply, particularly in areas with stringent emission regulations.

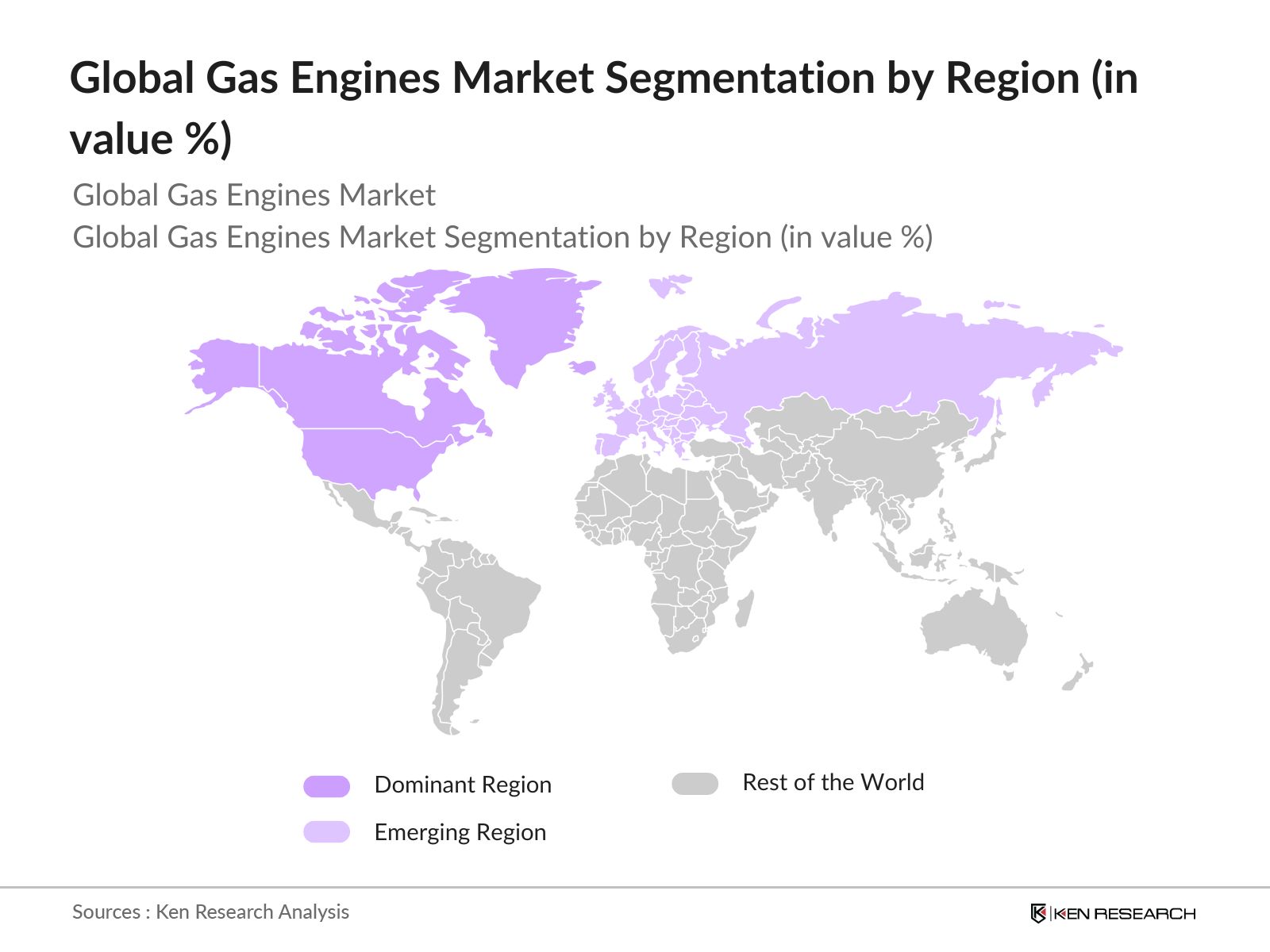

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Europe continues to dominate the market due to the region's strong focus on renewable energy and emissions reduction targets. Germany, in particular, is a leading market due to its investments in CHP systems. The Asia-Pacific region is also witnessing growth, driven by industrialization and urbanization in countries like China and India.

The market is highly consolidated, with a few major players controlling a portion of the market. Companies in this market compete based on product innovation, efficiency, and their ability to comply with stringent environmental regulations. Major players include General Electric, Caterpillar, and Wrtsil Corporation, which are known for their technological advancements and wide product portfolios.

|

Company |

Established |

Headquarters |

Fuel Type Specialization |

Product Portfolio |

Geographic Presence |

R&D Investment (%) |

Market Share (%) |

Technological Innovation |

Strategic Partnerships |

|

General Electric (GE) |

1892 |

Boston, USA |

|||||||

|

Caterpillar Inc. |

1925 |

Illinois, USA |

|||||||

|

Wrtsil Corporation |

1834 |

Helsinki, Finland |

|||||||

|

Rolls-Royce Holdings plc |

1906 |

London, UK |

|||||||

|

Cummins Inc. |

1919 |

Indiana, USA |

Over the next five years, the global gas engines industry is expected to experience robust growth driven by increased demand for cleaner power generation solutions and advancements in gas engine technology. The transition towards low-carbon economies in Europe and North America will continue to push the adoption of natural gas and biogas-based engines.

|

Engine Type |

Reciprocating Gas Engines Gas Turbines Microturbines Stirling Engines |

|

Power Output |

Below 1 MW 1 MW to 5 MW 5 MW to 15 MW Above 15 MW |

|

Application |

Power Generation Cogeneration/CHP Industrial Commercial Buildings |

|

Fuel Type |

Natural Gas Biogas Hydrogen Other Synthetic Gases |

|

Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1 Definition and Scope

1.2 Market Taxonomy (Engine Types, Power Output, Applications, Fuel Type, and Regions)

1.3 Market Growth Rate (CAGR, Revenue Growth)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

4.1 By Engine Type (In Value %)

4.2 By Power Output (In Value %)

4.3 By Application (In Value %)

4.4 By Fuel Type (In Value %)

4.5 By Region (In Value %)

5.1 Detailed Profiles of Major Companies

6.1 Emission Standards and Environmental Regulations (EPA, Euro VI, IMO)

6.2 Compliance Requirements (Air Quality Standards, Noise Pollution Control)

6.3 Certification Processes (ISO 50001, CE Marking, Industry Certifications)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Engine Type (In Value %)

8.2 By Power Output (In Value %)

8.3 By Application (In Value %)

8.4 By Fuel Type (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis (End-User Insights)

9.3 Marketing Initiatives (Market Penetration, Product Positioning)

9.4 White Space Opportunity Analysis

The first phase involved mapping out the key stakeholders in the global gas engines market. This was supported by extensive desk research, using both secondary and proprietary databases to gather a comprehensive set of industry data. Critical market variables, such as fuel supply dynamics, power generation needs, and regulatory frameworks, were identified.

Historical data was collected and analyzed to assess the market penetration of gas engines, including a review of market drivers and challenges. Key performance metrics, such as revenue generation and efficiency improvements in gas engine technology, were assessed.

Market hypotheses were validated through consultations with industry experts, including engineers, product managers, and policymakers. These discussions provided valuable insights into the operational and financial dynamics shaping the gas engines market.

The final phase involved compiling the data gathered through bottom-up analysis and validating it against industry sources. This data was used to construct the market forecast and segmentation model for the gas engines market.

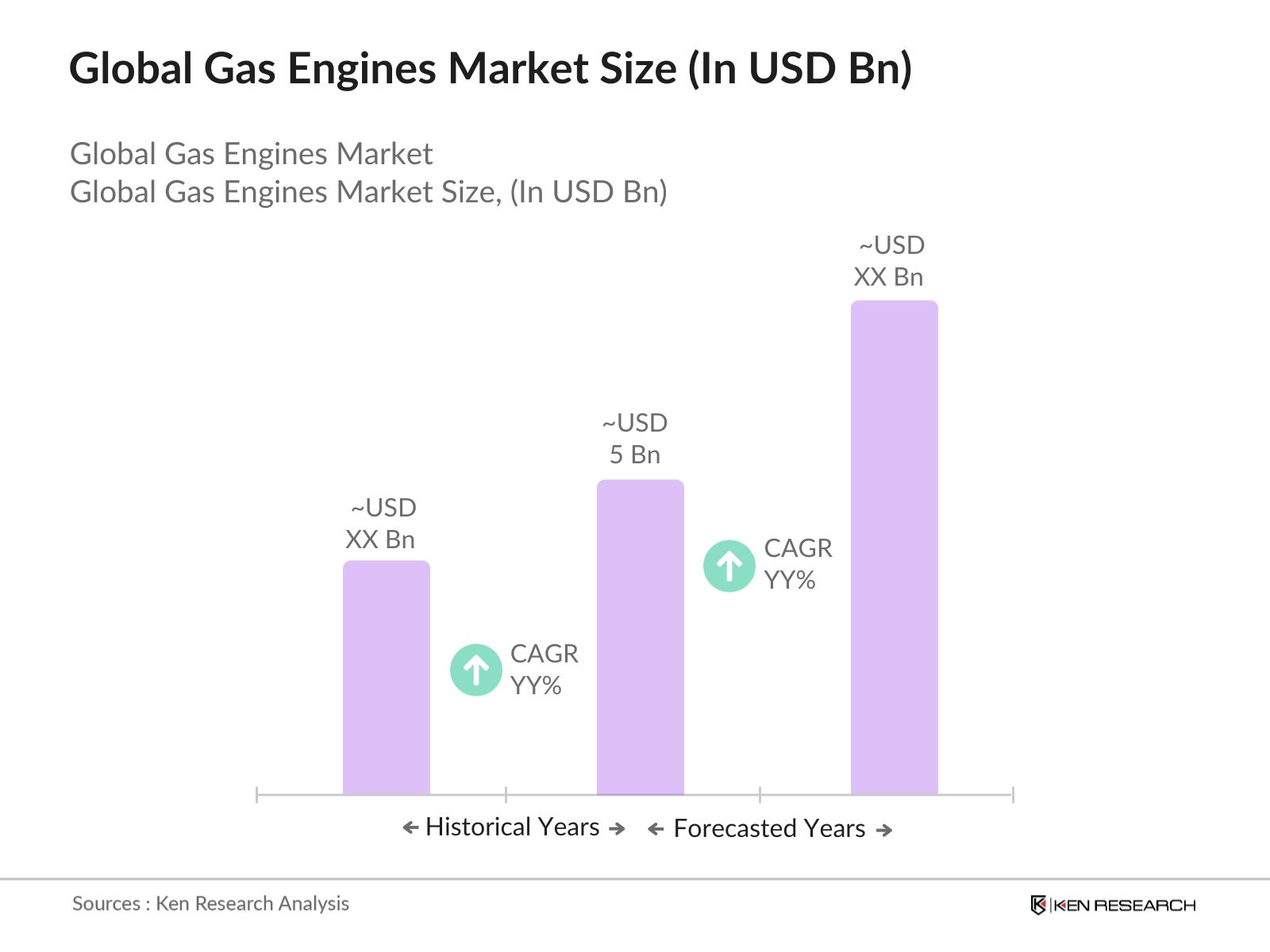

The global gas engines market is valued at USD 5 billion based on a five-year historical analysis. This growth is driven by increasing demand for distributed power solutions and a shift towards cleaner fuel alternatives.

Key challenges in the global gas engines market include high initial investment costs, volatility in natural gas prices, and competition from renewable energy sources. Additionally, gas infrastructure limitations in certain regions hamper market growth.

Major players in the global gas engines market include General Electric, Caterpillar Inc., Wrtsil Corporation, Rolls-Royce Holdings plc, and Cummins Inc. These companies dominate due to their extensive product portfolios and technological innovations.

The global gas engines market is driven by increasing demand for reliable power generation, especially in industrial and commercial sectors. The transition towards lower emissions and energy-efficient solutions also plays a significant role in market growth.

Major trends in the global gas engines market include the increasing adoption of IoT in engine monitoring, the growing use of renewable natural gas (RNG), and advancements in hybrid gas engine technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.