Global Health Check-Up Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD7018

December 2024

94

About the Report

Global Health Check-Up Market Overview

- The Global Health Check-Up market is valued at USD 49 billion, based on a five-year historical analysis. This market is driven by the increasing demand for preventive healthcare services, influenced by a growing awareness of early diagnosis benefits. Technological advancements, such as AI-powered diagnostic tools and home health monitoring kits, have played a significant role in expanding the availability of comprehensive health check-ups.

- Countries such as the United States, India, and Germany dominate the health check-up market due to the presence of well-established healthcare systems, advanced diagnostic technologies, and a large population base with a high disposable income. In particular, the U.S. leads in preventive health services due to strong health insurance coverage and corporate wellness programs that incentivize regular health check-ups.

- Governments worldwide are increasing their focus on preventive healthcare. In 2023, the World Health Organization (WHO) reported that over 90 countries had implemented national strategies emphasizing preventive healthcare. These policies are aimed at reducing the burden on healthcare systems by encouraging early detection and management of diseases through regular health check-ups. Government subsidies for preventive services, particularly in high-income countries, have been a major driver of growth in this market.

Global Health Check-Up Market Segmentation

By Region: The market is segmented by region into North America, Europe, APAC, MEA, and Latin America. North America holds the dominant market share driven by robust healthcare infrastructure, technological advancements in diagnostic tools, and significant healthcare expenditure by the population. The regions focus on preventive care through corporate wellness programs and insurance coverage has contributed to its market leadership.

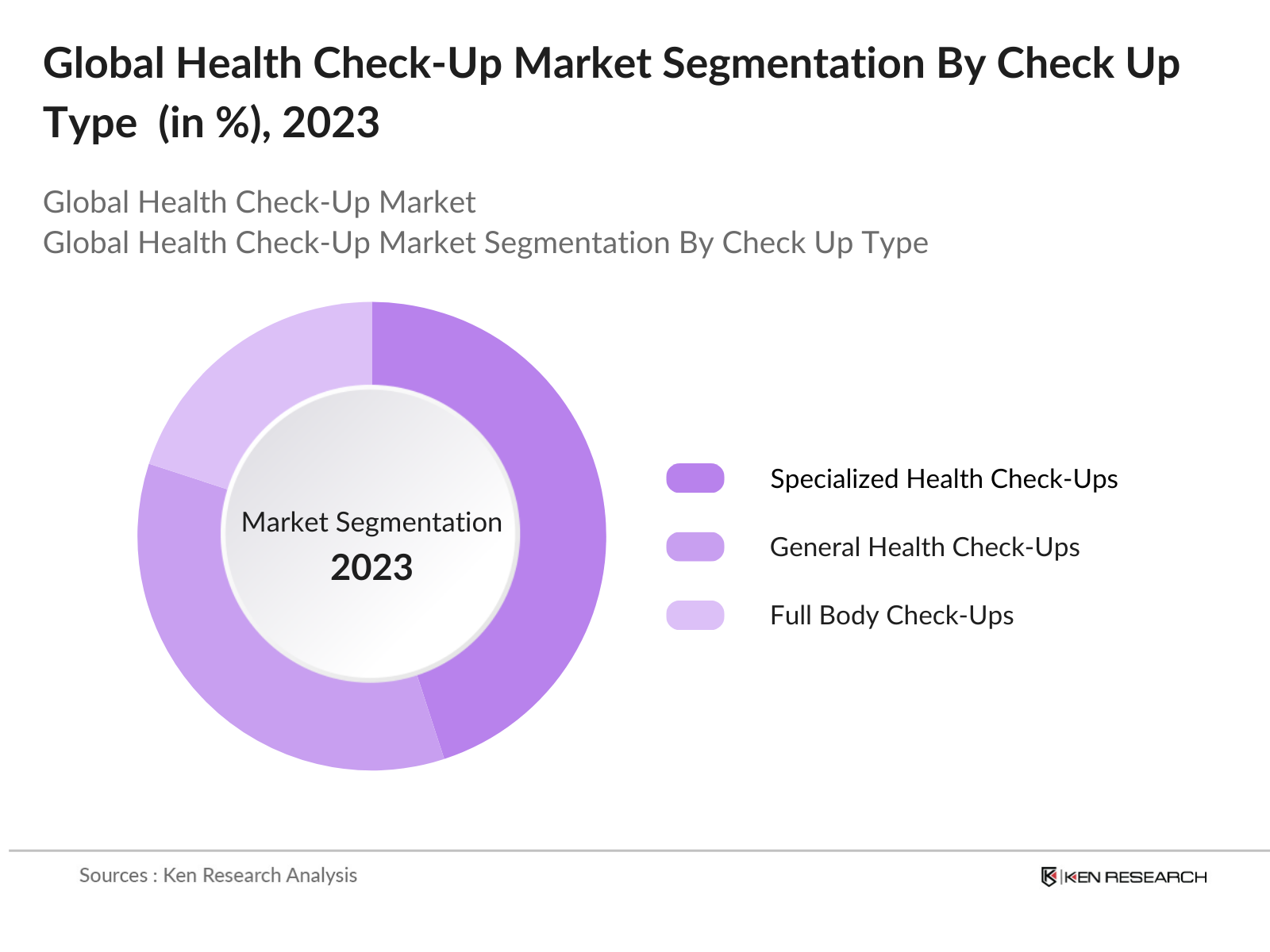

By Check-Up Type: The Global Health Check-Up market is segmented by check-up type into General Health Check-Ups, Specialized Health Check-Ups, and Full Body Check-Ups. Specialized Health Check-Ups, such as those for cardiovascular diseases and cancer, have a dominant market share due to the rising incidence of chronic diseases and the need for specific diagnostics. Health-conscious consumers are increasingly opting for such targeted diagnostics to detect diseases at an early stage.

Global Health Check-Up Market Competitive Landscape

The Global Health Check-Up market is consolidated with a few key players dominating the industry. Companies such as Quest Diagnostics, Cleveland Clinic, and Apollo Hospitals play a crucial role in the market. Their dominance is attributed to their well-established brand presence, comprehensive service offerings, and advanced diagnostic tools that attract a large customer base.

|

Company |

Establishment Year |

Headquarters |

No. of Health Centers |

Revenue (USD Bn) |

Employees |

R&D Investments (USD Mn) |

Partnerships |

Technological Advancements |

|

Quest Diagnostics |

1967 |

U.S. |

_ |

_ |

_ |

_ |

_ |

_ |

|

Cleveland Clinic |

1921 |

U.S. |

_ |

_ |

_ |

_ |

_ |

_ |

|

Apollo Hospitals |

1983 |

India |

_ |

_ |

_ |

_ |

_ |

_ |

|

Mayo Clinic |

1889 |

U.S. |

_ |

_ |

_ |

_ |

_ |

_ |

|

Life Line Screening |

1993 |

U.S. |

_ |

_ |

_ |

_ |

_ |

_ |

Global Health Check-Up Industry Analysis

Growth Drivers

- Rise in Preventive Health Care Demand: The increasing emphasis on preventive healthcare is a significant growth driver for the global health check-up market. According to the World Bank, life expectancy globally has risen from 72.8 years in 2020 to 73.4 years in 2023. This has led to a growing focus on maintaining long-term health, which has increased demand for preventive check-ups. Furthermore, the Global Health Expenditure Database shows that public health spending increased by $200 billion between 2020 and 2022, driven largely by preventive measures. This rising investment in preventive care is boosting the health check-up market.

- Increase in Health Consciousness: Health consciousness has increased globally, with more individuals actively participating in regular health check-ups. A 2023 WHO report states that 30% of global adults have adopted some form of annual or biannual health check-up. In 2022, global health awareness programs led to a $1.5 trillion expenditure on wellness, which reflects a broader shift in consumer behavior towards healthier lifestyles. Additionally, World Bank data highlights that health awareness campaigns in both developed and developing economies have contributed to this trend.

- Technological Advancements in Diagnostics: Technological advancements are revolutionizing the global health check-up market, with AI, machine learning, and high-speed diagnostics leading the charge. The integration of next-generation sequencing (NGS) and real-time PCR tests has significantly improved the accuracy of health check-ups. According to the World Health Organization (WHO), over 70 countries in 2022 upgraded their diagnostic frameworks to adopt modern technology, including digital diagnostics. These advancements have led to faster, more accurate check-ups, improving patient outcomes and encouraging greater uptake of routine health screenings.

Market Challenges

- High Cost of Advanced Health Check-Ups: The cost of advanced diagnostic tests remains a key challenge for market growth. According to a 2023 report from the World Bank, the average global expenditure on healthcare diagnostics for an individual is around $300 annually, but advanced diagnostics can push this figure above $1,000. This pricing disparity makes preventive health check-ups less accessible to lower-income populations. Additionally, healthcare spending as a percentage of GDP varies widely, with some developing economies spending as little as 3%, limiting the reach of high-end health check-ups.

- Limited Availability of Comprehensive Services in Rural Areas: Healthcare services in rural areas lag significantly behind urban centers. In 2022, the World Health Organization (WHO) reported that over 40% of the global population lacks access to comprehensive diagnostic services due to inadequate healthcare infrastructure in rural regions. The report also found that rural healthcare centers are underfunded, with 30% of rural hospitals having obsolete diagnostic tools. This gap in service provision is a major barrier to the growth of the health check-up market in these areas.

Global Health Check-Up Market Future Outlook

Over the next five years, the Global Health Check-Up market is expected to show significant growth driven by increasing demand for preventive healthcare services, advancements in diagnostic technology, and growing consumer awareness regarding early disease detection. The rising geriatric population, particularly in developed countries, will further propel the demand for regular health check-ups. Additionally, innovations in wearable diagnostic devices and the growing popularity of telemedicine are likely to shape the future of the health check-up market.

Opportunities

- Growing Geriatric Population: The growing elderly population presents a significant opportunity for the health check-up market. According to the UN Population Division, there were 771 million people aged 65 and older in 2022, and this demographic is expected to account for 17% of the global population by 2025. The rising prevalence of age-related diseases, including cardiovascular diseases and diabetes, is driving the demand for regular health check-ups. This increase in the geriatric population highlights the need for more tailored health check-up services.

- Telemedicine Integration with Health Check-Ups: Telemedicine is revolutionizing the way health check-ups are conducted. In 2023, over 700 million telemedicine consultations were conducted globally, according to the World Bank. The ability to remotely monitor health conditions has proven effective, especially in remote and rural regions. The combination of telemedicine with preventive health check-ups is becoming a key driver of market growth, with governments worldwide supporting the expansion of telehealth services to improve healthcare access in underserved areas.

Scope of the Report

|

Check-Up Type |

General Health Check-Ups, Specialized Health Check-Ups Full Body Check-Ups |

|

Age Group |

Pediatrics Adults Geriatrics |

|

Service Provider |

Hospitals Diagnostic Centers Online Health Check-Up Platforms |

|

Technology |

Wearable Devices AI-Powered Diagnostics Traditional Diagnostics |

|

Region |

North America Europe APAC MEA Latin America |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Hospitals and Diagnostic Industries

Health Insurance Companies

Medical Device Companies

Wearable Technology Companies

Telemedicine Industries

Government and Regulatory Bodies (e.g., FDA, CDC)

Investments and Venture Capitalist Firms

Health and Wellness Companies

Companies

Players Mentioned in the Report:

Quest Diagnostics

Cleveland Clinic

Mayo Clinic

Apollo Hospitals

Life Line Screening

Nuffield Health

Health Check 360

Metropolis Healthcare

Pharmeasy

Onsite Health Diagnostics

Dasa Diagnostics

SRL Diagnostics

Abbott Laboratories

Medanta

Healthians

Table of Contents

1. Global Health Check-Up Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Health Check-Up Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Health Check-Up Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Preventive Health Care Demand

3.1.2. Increase in Health Consciousness

3.1.3. Technological Advancements in Diagnostics

3.1.4. Integration of AI in Health Check-Ups

3.2. Market Challenges

3.2.1. High Cost of Advanced Health Check-Ups

3.2.2. Limited Availability of Comprehensive Services in Rural Areas

3.2.3. Privacy and Data Security Concerns

3.3. Opportunities

3.3.1. Growing Geriatric Population

3.3.2. Telemedicine Integration with Health Check-Ups

3.3.3. Expansion in Emerging Markets

3.4. Trends

3.4.1. Home Health Check-Up Kits

3.4.2. Personalized Health Reports

3.4.3. Subscription-Based Health Plans

3.5. Government Regulations

3.5.1. Healthcare Policies for Preventive Care

3.5.2. Data Privacy Regulations (HIPAA, GDPR)

3.5.3. Public Health Initiatives

3.6. SWOT Analysis (Specific to health check-up providers)

3.7. Stakeholder Ecosystem (Health service providers, tech companies, insurance companies)

3.8. Porters Five Forces

3.8.1. Bargaining Power of Buyers

3.8.2. Bargaining Power of Suppliers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem

4. Global Health Check-Up Market Segmentation

4.1. By Check-Up Type (In Value %)

4.1.1. General Health Check-Ups

4.1.2. Specialized Health Check-Ups (Cardiovascular, Oncology, etc.)

4.1.3. Full Body Check-Ups

4.2. By Age Group (In Value %)

4.2.1. Pediatrics

4.2.2. Adults

4.2.3. Geriatrics

4.3. By Service Provider (In Value %)

4.3.1. Hospitals

4.3.2. Diagnostic Centers

4.3.3. Online Health Check-Up Platforms

4.4. By Technology (In Value %)

4.4.1. Wearable Devices

4.4.2. AI-Powered Diagnostics

4.4.3. Traditional Diagnostics

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. APAC

4.5.4. MEA

4.5.5. Latin America

5. Global Health Check-Up Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Cleveland Clinic

5.1.2. Mayo Clinic

5.1.3. Quest Diagnostics

5.1.4. Apollo Hospitals

5.1.5. Abbott Laboratories

5.1.6. Health Check 360

5.1.7. Life Line Screening

5.1.8. Nuffield Health

5.1.9. MediBuddy

5.1.10. Metropolis Healthcare

5.1.11. Pharmeasy

5.1.12. Onsite Health Diagnostics

5.1.13. Practo

5.1.14. Dasa Diagnostics

5.1.15. SRL Diagnostics

5.2 Cross Comparison Parameters (Revenue, No. of Clinics, Services Offered, Partnerships, R&D Investments, Market Share, Online vs Offline Operations, Growth Strategies)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Health Check-Up Market Regulatory Framework

6.1. Health Check-Up Protocols

6.2. Insurance Coverage Guidelines

6.3. Certification and Accreditation Requirements

7. Global Health Check-Up Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Health Check-Up Future Market Segmentation

8.1. By Check-Up Type (In Value %)

8.2. By Age Group (In Value %)

8.3. By Service Provider (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Global Health Check-Up Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research process began with the identification of critical variables that influence the Global Health Check-Up market. These variables were identified through extensive desk research, including market reports, government publications, and proprietary databases, to develop a comprehensive understanding of the market landscape.

Step 2: Market Analysis and Construction

In this step, historical data of the health check-up market was analyzed to assess trends in service providers and regional growth. We evaluated the penetration of diagnostic services and analyzed how technological innovations like AI-powered diagnostics have shaped the market.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses were developed and validated through consultations with key players in the health check-up market. These consultations, conducted through interviews with senior management, helped confirm our projections regarding the markets growth trajectory.

Step 4: Research Synthesis and Final Output

The final phase of the research included synthesizing data from both top-down and bottom-up approaches. Detailed insights were gathered from market players to ensure the accuracy of projections. This was followed by a review of market statistics, refining the research output to ensure it reflects the true state of the health check-up market.

Frequently Asked Questions

1. How big is the Global Health Check-Up market?

The Global Health Check-Up market is valued at USD 49 billion, driven by increasing awareness of preventive care and advancements in diagnostic technologies.

2. What are the challenges in the Global Health Check-Up market?

Challenges include high costs associated with specialized diagnostic services, lack of accessibility in rural areas, and privacy concerns surrounding patient health data.

3. Who are the major players in the Global Health Check-Up market?

Key players in the market include Quest Diagnostics, Cleveland Clinic, Apollo Hospitals, and Mayo Clinic, which dominate the market due to their established infrastructure and comprehensive health services.

4. What are the growth drivers of the Global Health Check-Up market?

The market is propelled by the increasing geriatric population, rising consumer awareness for preventive healthcare, and technological advancements like AI-based diagnostic tools and telemedicine integration.

5. Which regions dominate the Global Health Check-Up market?

North America dominates the market due to advanced healthcare infrastructure and strong insurance coverage for preventive health services. Europe and APAC follow due to their growing health-conscious populations and emerging telemedicine adoption.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.