Global Hunter Syndrome Treatment Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD6276

Region:Global

Author(s):Abhinav kumar

Product Code:KROD6276

November 2024

97

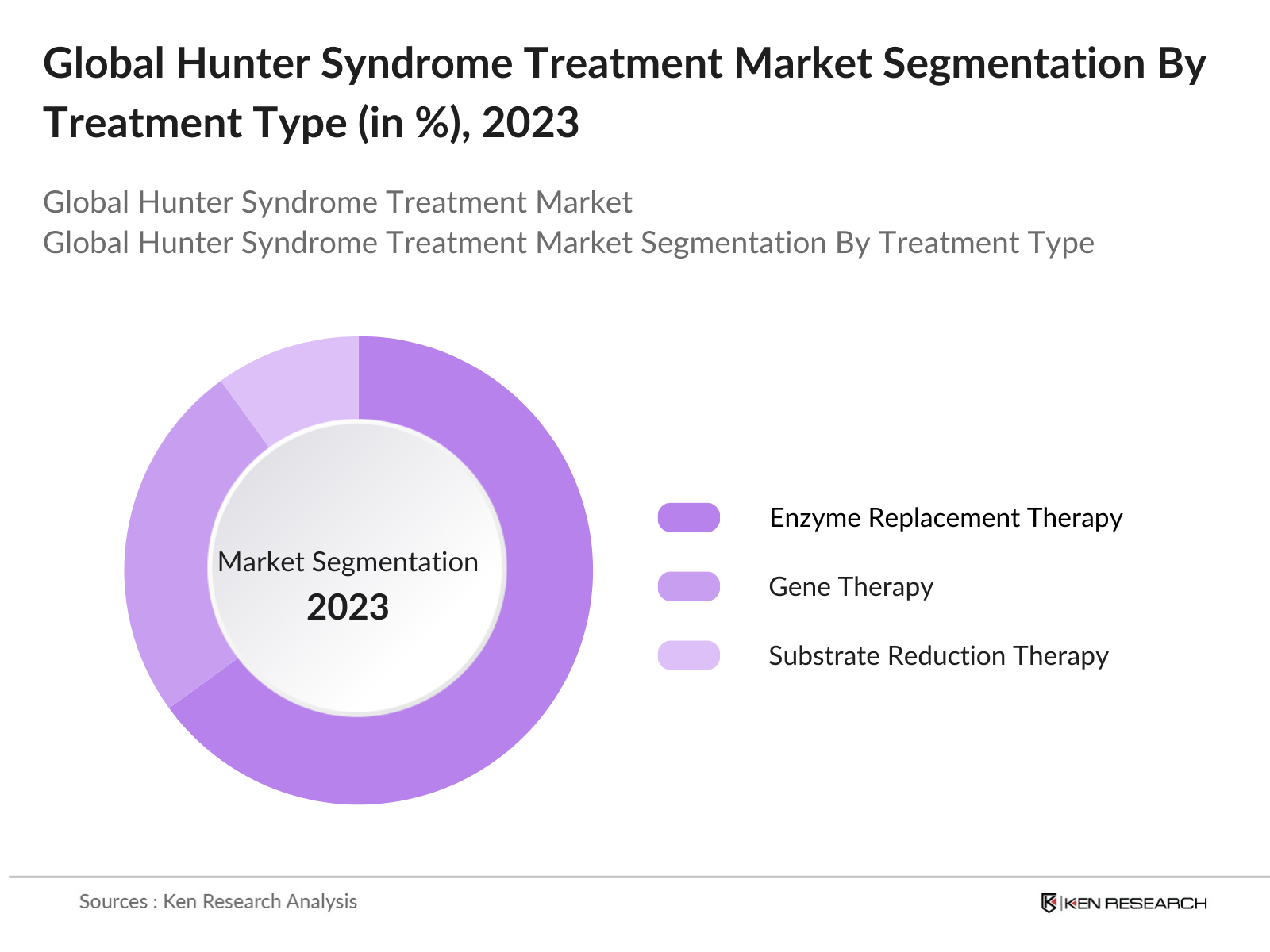

By Treatment Type: The global Hunter Syndrome market is segmented by treatment type into Enzyme Replacement Therapy (ERT), Gene Therapy, and Substrate Reduction Therapy. ERT has the dominant market share due to its early development and acceptance as the primary treatment option. Shires Elaprase, an enzyme replacement therapy, has remained the most widely prescribed solution for managing the condition. Its dominance is attributed to its efficacy in slowing the progression of the disease and its extensive approval in various regions, especially in North America and Europe.

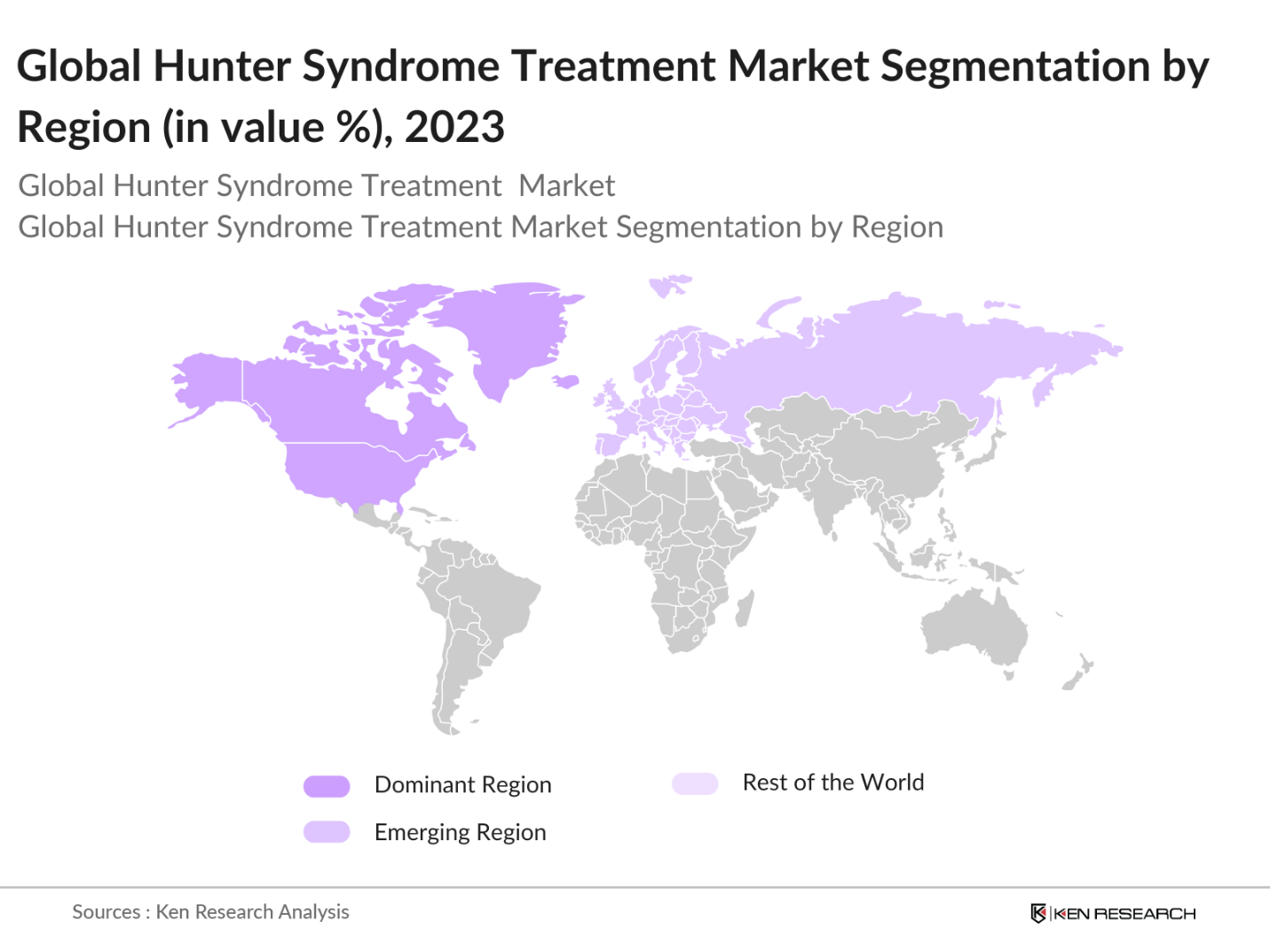

By Region: The Hunter Syndrome treatment market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America leads the global market due to its strong healthcare infrastructure and the high concentration of research facilities and pharmaceutical companies. Europe follows closely, driven by government initiatives and patient advocacy groups that support research and development. Asia Pacific is experiencing rapid growth, primarily in Japan and South Korea, where advances in healthcare and increased awareness of rare diseases are driving demand for Hunter Syndrome treatments.

By Mode of Administration: The market is also segmented by the mode of administration into Intravenous, Oral, and Subcutaneous treatments. Intravenous (IV) therapies hold the largest share of the market due to their proven effectiveness in delivering enzymes directly into the bloodstream. IV treatments, such as Elaprase, have been in use for years and are supported by extensive clinical trials, making them the most trusted option for both healthcare providers and patients.

The Hunter Syndrome treatment market is consolidated with a few major players leading in research and drug development. Companies like Takeda (Shire) and BioMarin Pharmaceutical dominate, with several other biopharmaceutical companies focusing on innovative therapies. These companies have strong research pipelines, global presence, and collaborations with academic institutions, enhancing their market positions.

The Hunter Syndrome treatment market is expected to see substantial growth over the next five years, driven by advancements in gene therapy and the expansion of enzyme replacement therapies. The market is anticipated to benefit from increased funding for rare disease research, the emergence of new therapies, and broader awareness among patients and healthcare providers. Companies are likely to focus on enhancing the efficacy of existing treatments, improving delivery methods, and expanding their presence in underdeveloped regions with unmet medical needs. The continued support from governments, alongside collaborations between academia and pharmaceutical firms, will be key drivers of future growth. As innovative gene therapies move toward commercialization, the treatment landscape is expected to shift, offering improved outcomes for patients.

|

Treatment Type |

Enzyme Replacement Therapy (ERT) Gene Therapy Substrate Reduction Therapy |

|

Mode of Administration |

Intravenous Oral Subcutaneous |

|

Age Group |

Pediatric Patients Adult Patients |

|

Distribution Channel |

Hospital Pharmacies Specialty Clinics Online Pharmacies |

|

Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Advancements in Enzyme Replacement Therapy (ERT)

3.1.2. Increasing Research and Development Investments

3.1.3. Rising Prevalence of Rare Genetic Disorders

3.1.4. Availability of Government Funding and Orphan Drug Incentives

3.2. Market Challenges

3.2.1. High Treatment Costs

3.2.2. Limited Patient Awareness in Developing Economies

3.2.3. Complexities in Clinical Trials

3.3. Opportunities

3.3.1. Expansion of Gene Therapy Applications

3.3.2. Increasing Collaborations Between Biopharma Companies

3.3.3. Growth of Personalized Medicine Approaches

3.4. Trends

3.4.1. Adoption of Innovative Therapeutics for Rare Diseases

3.4.2. Increased Use of Biomarkers for Treatment Efficacy

3.4.3. Advances in Gene Editing Technologies

3.5. Government Regulation

3.5.1. Orphan Drug Designation Policies

3.5.2. Regulatory Pathways for Approval of Rare Disease Treatments

3.5.3. International Guidelines for Gene Therapy and Clinical Trials

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Treatment Type (In Value %)

4.1.1. Enzyme Replacement Therapy (ERT)

4.1.2. Gene Therapy

4.1.3. Substrate Reduction Therapy

4.2. By Mode of Administration (In Value %)

4.2.1. Intravenous

4.2.2. Oral

4.2.3. Subcutaneous

4.3. By Age Group (In Value %)

4.3.1. Pediatric Patients

4.3.2. Adult Patients

4.4. By Distribution Channel (In Value %)

4.4.1. Hospital Pharmacies

4.4.2. Specialty Clinics

4.4.3. Online Pharmacies

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Shire (now Takeda)

5.1.2. BioMarin Pharmaceutical Inc.

5.1.3. Sanofi Genzyme

5.1.4. JCR Pharmaceuticals Co., Ltd.

5.1.5. Green Cross Corp.

5.1.6. RegenxBio Inc.

5.1.7. Ultragenyx Pharmaceutical Inc.

5.1.8. Orchard Therapeutics

5.1.9. Sangamo Therapeutics, Inc.

5.1.10. Abeona Therapeutics

5.1.11. Lysogene

5.1.12. Denali Therapeutics

5.1.13. ArmaGen, Inc.

5.1.14. Sarepta Therapeutics

5.1.15. Inventiva Pharma

5.2. Cross Comparison Parameters

5.2.1. Research & Development Expenditure

5.2.2. Product Portfolio Breadth

5.2.3. Strategic Collaborations

5.2.4. Market Penetration by Geography

5.2.5. Regulatory Approvals

5.2.6. Number of Patents

5.2.7. Manufacturing Capabilities

5.2.8. Market Share in Hunter Syndrome Treatment

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Global Orphan Drug Designation Policies

6.2. Compliance Requirements for Clinical Trials

6.3. Certification and Approval Processes for Gene Therapy

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Treatment Type (In Value %)

8.2. By Mode of Administration (In Value %)

8.3. By Age Group (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThis phase focuses on constructing a detailed market map of the global Hunter Syndrome treatment market. Key variables such as market drivers, patient demographics, and treatment efficacy are identified through extensive desk research and the utilization of proprietary industry databases. This lays the foundation for understanding the overall market dynamics.

Historical data and trends are analyzed to estimate market penetration and assess the current ratio of patients to treatment availability. Further, an evaluation of revenue statistics is conducted to verify the reliability of market projections, considering product uptake and market expansions.

Our initial market assumptions are tested through in-depth interviews with industry experts, including key opinion leaders and pharmaceutical executives. These consultations help refine our understanding of the market dynamics and corroborate the data gathered from secondary research.

The final step involves compiling the findings from the previous stages and synthesizing them into a comprehensive analysis of the market. Insights from primary interviews and secondary research are consolidated to provide an accurate and validated report of the global Hunter Syndrome treatment market.

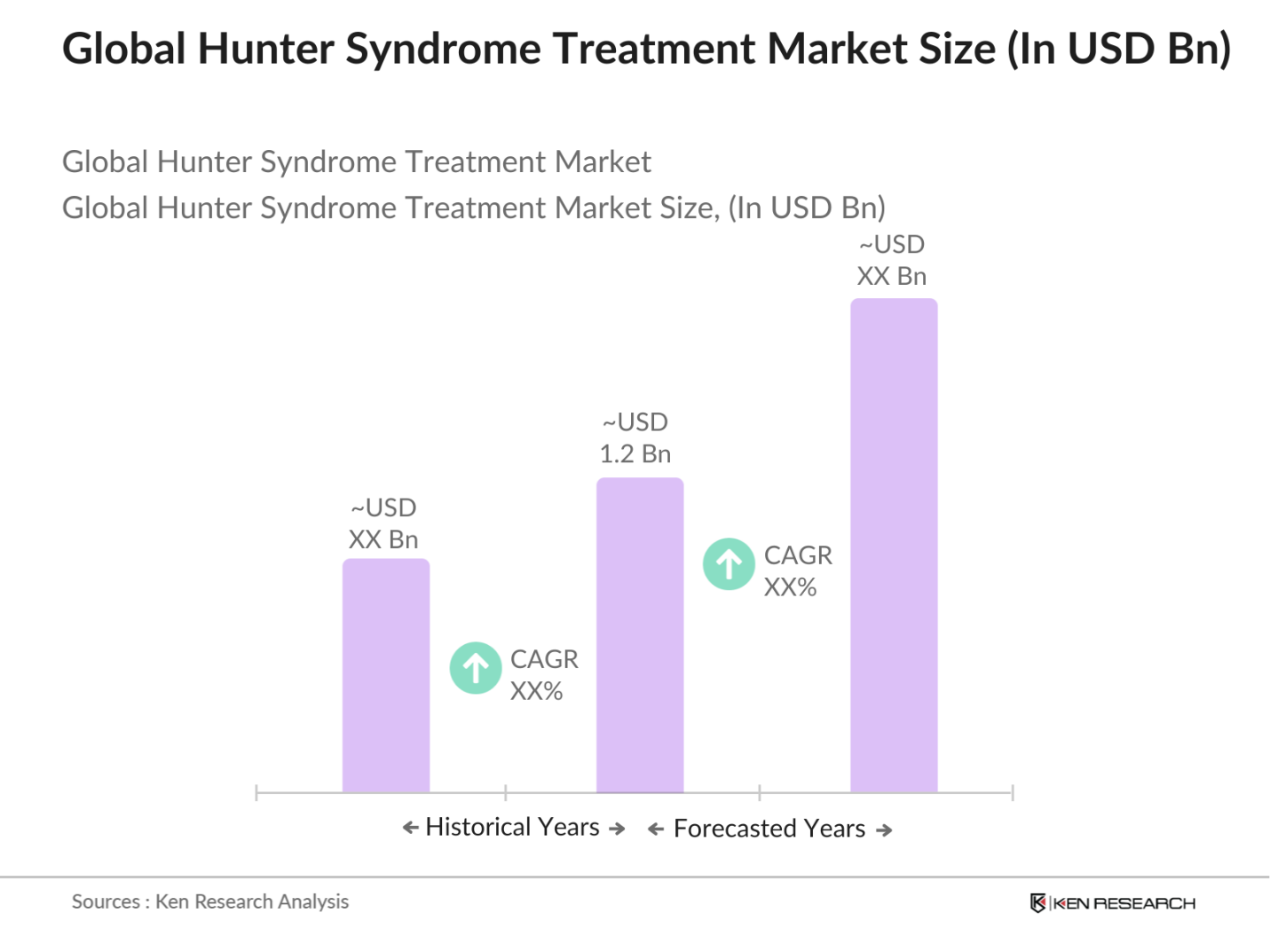

The global Hunter Syndrome treatment market is valued at approximately USD 1.2 billion, driven by growing advancements in enzyme replacement therapies and increasing awareness of rare diseases.

The challenges include high treatment costs, limited patient awareness in developing regions, and complexities in clinical trials, particularly for emerging gene therapies.

Key players include Takeda (Shire), BioMarin Pharmaceutical, Sanofi Genzyme, JCR Pharmaceuticals, and Ultragenyx Pharmaceutical, dominating the market due to their strong research pipelines and global presence.

The market is propelled by advancements in treatment technologies, increased funding for rare diseases, and government support through orphan drug incentives.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.