Global Hypercharger Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD1679

Region:Global

Author(s):Abhinav kumar

Product Code:KROD1679

December 2024

87

The Global Hypercharger Market is segmented by Region, Component, and Charging Type.

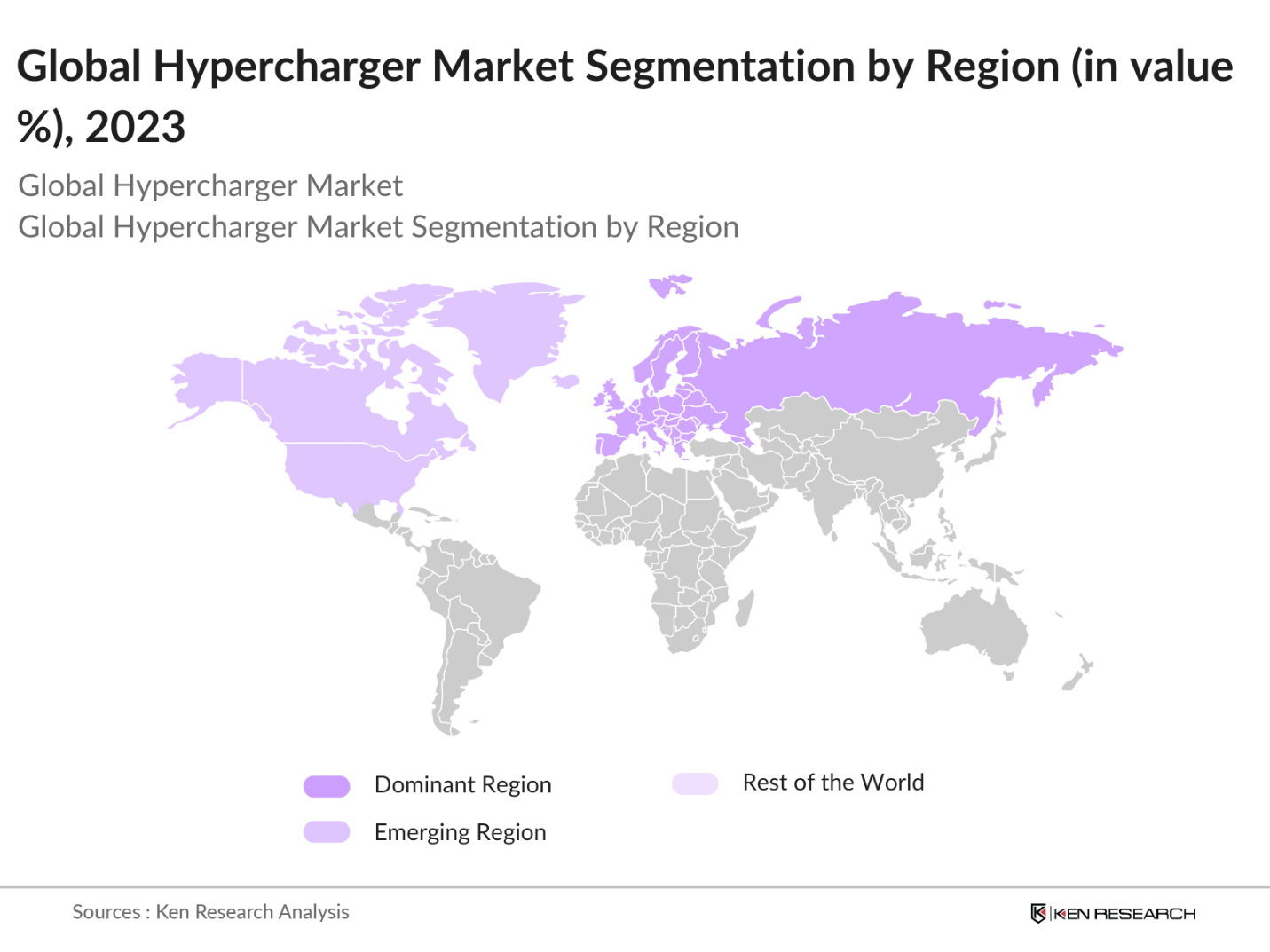

By Region: The global hypercharger market is segmented into North America, Europe, Asia-Pacific (APAC), Middle East & Africa (MEA), and Latin America. In 2023, North America held the largest market share, driven by substantial government funding for EV infrastructure, high EV adoption rates, and the presence of leading hypercharger manufacturers.

By Charging Type: The market is segmented into AC charging and DC fast charging. IN 2023, DC fast charging dominated the market, as it enables significantly faster charging speeds compared to AC charging. With automakers pushing for faster and more efficient charging solutions, the adoption of DC hyperchargers is expected to continue growing rapidly.

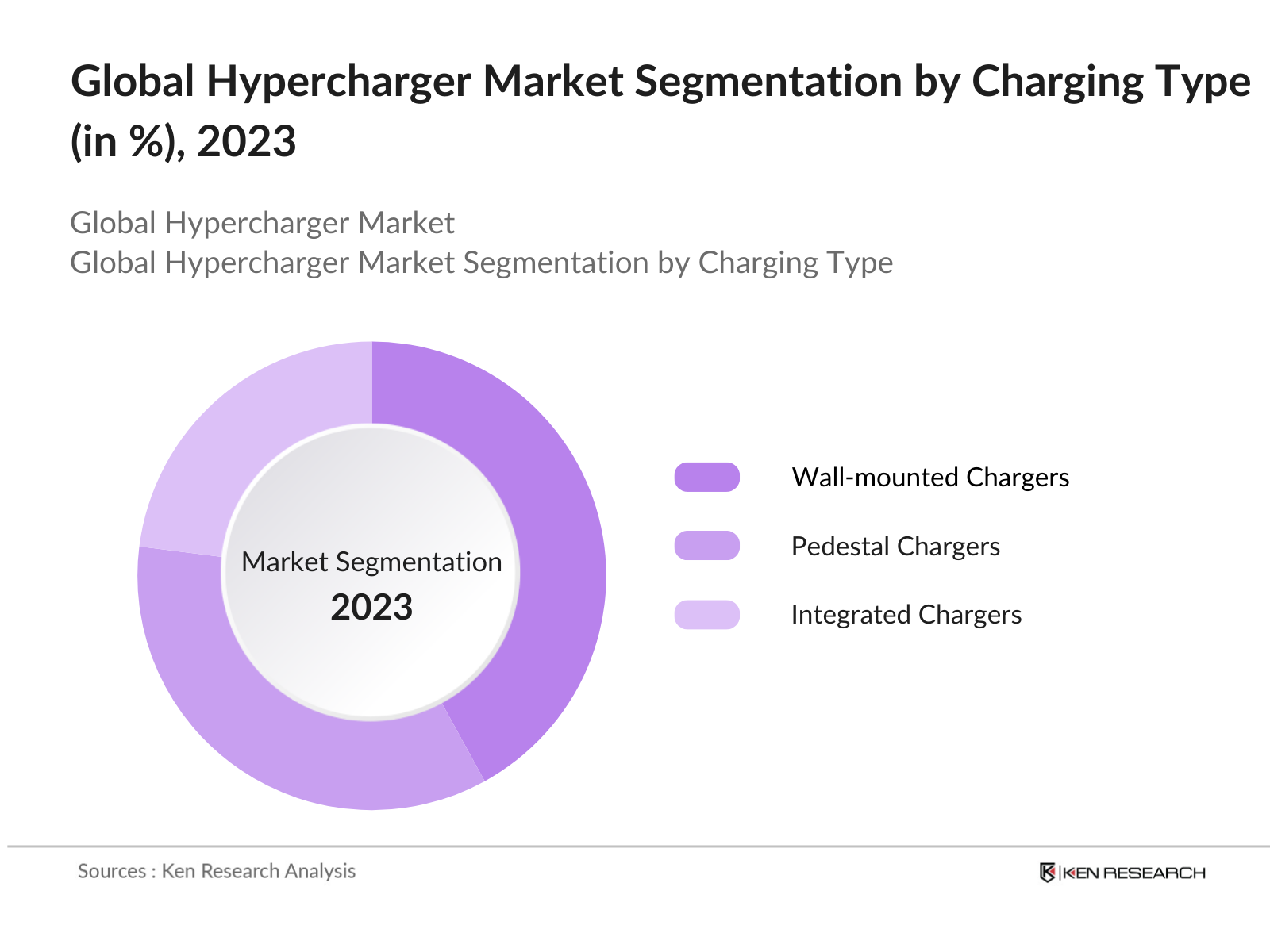

By Component: The market is segmented into hardware, software, and services. In 2023, hardware held the largest market share due to the high cost and complexity of charging station equipment. The growing demand for high-output charging stations across urban areas and highways has driven significant investments in hypercharger hardware.

|

Company |

Established Year |

Headquarters |

|

ABB |

1883 |

Zurich, Switzerland |

|

Tesla |

2003 |

Palo Alto, USA |

|

Siemens |

1847 |

Munich, Germany |

|

ChargePoint |

2007 |

Campbell, USA |

|

EVBox |

2010 |

Amsterdam, Netherlands |

ABB: In 2023, ABB announced the launch of its latest Terra HP chargers, capable of delivering 350 kW of power. These chargers have been deployed across Europe as part of the EUs efforts to increase hypercharger coverage on key highways. This initiative aligns with the European Union's efforts to expand the network of high-power electric vehicle (EV) chargers across major highways.

Tesla: In 2023, Tesla expanded its Supercharging network at a record pace, installing over 1,270 new stations and 12,400 individual stalls globally.This represents a 6% increase in stations and 14% increase in stalls compared to the previous year. The companys V3 Superchargers are capable of delivering 250 kW, enabling Tesla vehicles to charge at unprecedented speeds.

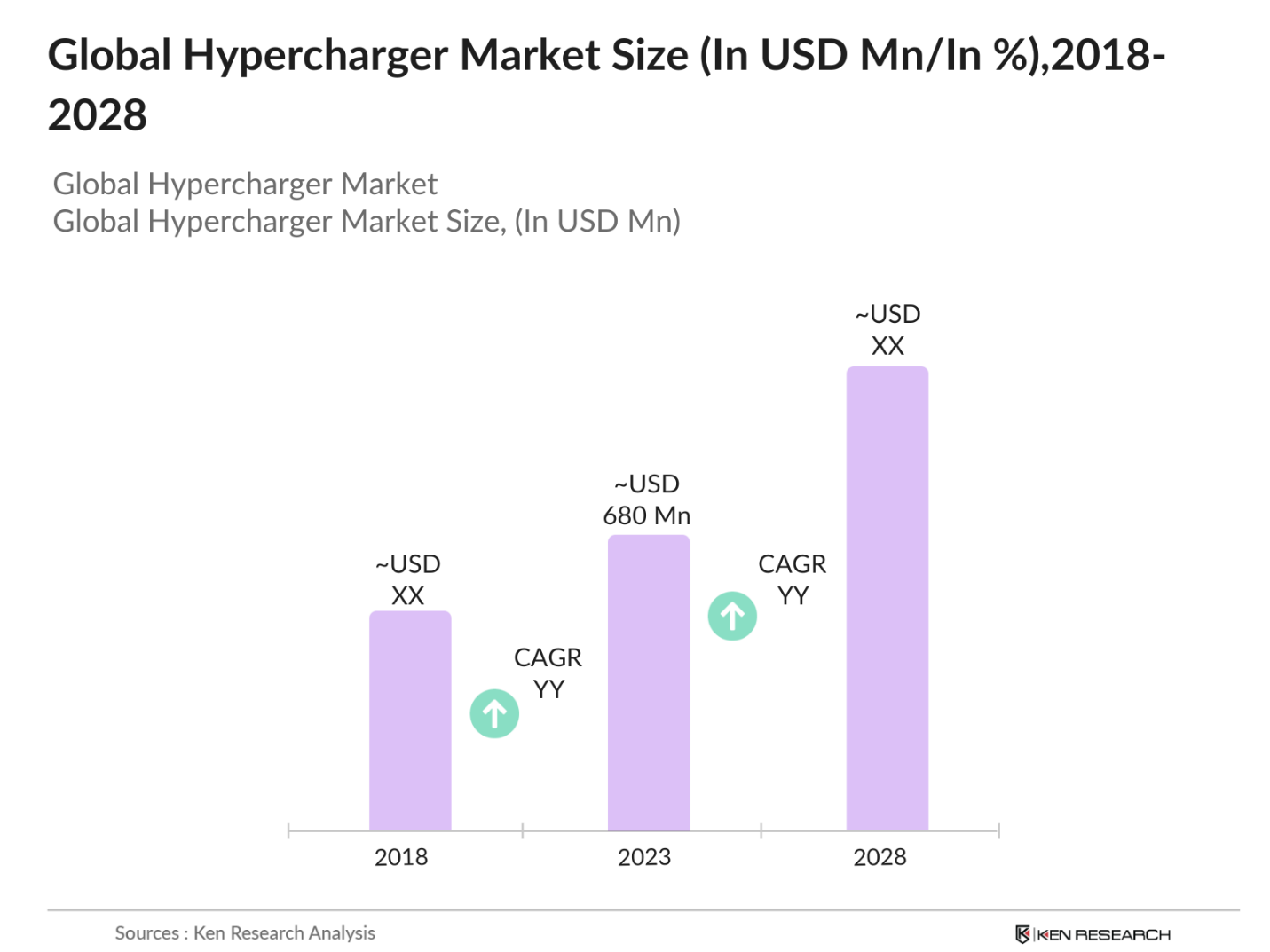

The Global Hypercharger Market is expected to experience substantial growth through 2028, driven by increasing EV adoption, government support for clean energy initiatives, and ongoing technological advancements in hypercharging infrastructure.

|

By Component |

Hardware Software Services |

|

By Charging Type |

AC Charging DC Fast Charging |

|

By End-User |

Public Charging Stations Commercial Fleets Residential Users |

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Buses |

|

By Region |

North America Europe Asia-Pacific (APAC) Middle East & Africa (MEA) Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (EV Adoption, Charging Infrastructure Expansion, Technological Advancements, Government Incentives)

3.1.1. Surge in Electric Vehicle Sales

3.1.2. Investments in Public Charging Infrastructure

3.1.3. Technological Innovations in Charging Speed and Efficiency

3.1.4. Government Subsidies and Emission Reduction Initiatives

3.2. Market Challenges (High Installation Costs, Infrastructure Complexity, Regional Disparities, Power Grid Limitations)

3.2.1. High Initial Capital Investment

3.2.2. Challenges in Power Distribution Networks

3.2.3. Regional Variability in Charging Demand

3.2.4. Technical Integration with Existing Grid

3.3. Opportunities (Expansion in Emerging Markets, Partnerships with Automakers, Wireless Charging Solutions, Smart Grid Integration)

3.3.1. Growing EV Markets in Asia-Pacific and Latin America

3.3.2. Collaboration with OEMs for Integrated Charging Solutions

3.3.3. Advancements in Wireless Charging Technologies

3.3.4. Smart Charging Networks for Energy Optimization

3.4. Trends (Ultra-Fast Charging Technology, Charging-as-a-Service, Energy Storage Integration, AI-Powered Charging Stations)

3.4.1. Adoption of 350kW+ Hyperchargers

3.4.2. Subscription-based Charging Models

3.4.3. Integration of Battery Storage for Load Balancing

3.4.4. AI-driven Predictive Maintenance for Charging Stations

3.5. Government Regulations (Emission Control Policies, Incentives for EV Charging Infrastructure, Renewable Energy Mandates, Cybersecurity Standards)

3.5.1. Emission Control Standards by Region

3.5.2. Government Grants for Public Charging Stations

3.5.3. Renewable Energy Requirements in Charging Networks

3.5.4. Cybersecurity Protocols for EV Charging Systems

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Charger Type (In Value %)

4.1.1. Ultra-fast Chargers (350 kW+)

4.1.2. Fast Chargers (100 kW - 350 kW)

4.1.3. Standard Chargers (Below 100 kW)

4.2. By Installation Type (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Public

4.3. By Connector Type (In Value %)

4.3.1. CCS

4.3.2. CHAdeMO

4.3.3. Tesla Supercharger

4.3.4. Type 2 (Mennekes)

4.4. By Application (In Value %)

4.4.1. Highway Charging

4.4.2. Urban Charging

4.4.3. Fleet Charging

4.4.4. Destination Charging

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Tesla Inc.

5.1.2. ABB Ltd.

5.1.3. Siemens AG

5.1.4. Schneider Electric SE

5.1.5. ChargePoint, Inc.

5.1.6. EVBox

5.1.7. Blink Charging Co.

5.1.8. Alfen N.V.

5.1.9. Tritium Pty Ltd

5.1.10. Efacec Power Solutions

5.1.11. Delta Electronics, Inc.

5.1.12. Shell Recharge Solutions

5.1.13. BP Pulse

5.1.14. Ionity GmbH

5.1.15. Enel X Way

5.2. Cross Comparison Parameters (Charger Capacity, Global Presence, Charging Network Size, Market Share, Partnerships, Research & Development, Revenue, Number of Employees)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Incentives

5.8. Venture Capital and Private Equity Investments

6.1. Industry Standards for Charging Stations

6.2. Government Policies on EV Adoption

6.3. Certification and Compliance Requirements

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Charger Type (In Value %)

8.2. By Installation Type (In Value %)

8.3. By Connector Type (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Segmentation and Target Market

9.3. Marketing Initiatives and Growth Strategies

9.4. White Space Opportunities

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around the Market to collate Market-level information.

Collating statistics on the global hypercharger market over the years, and analyzing the penetration of Marketplaces as well as the ratio of service providers to compute the revenue generated for the market. We will also review service quality statistics to understand the revenue generated which can ensure accuracy behind the data points shared.

Building Market hypotheses and conducting CATIs with Market experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple hypercharger companies to understand the nature of service segments, consumer preferences, and other parameters. This supports validating statistics derived through a bottom-to-top approach from these hypercharger companies, ensuring accuracy and reliability in the report.

The global hypercharger market was valued at $680 million in 2023, driven by the increasing adoption of electric vehicles (EVs), growing infrastructure investments, and advancements in fast-charging technology. This market is expected to grow as countries invest in reducing EV charging times.

Key challenges include the high installation costs of hypercharging stations, limited grid infrastructure in certain regions, and slow EV adoption in emerging markets. These factors present barriers to widespread deployment, particularly in developing areas.

Prominent players in the hypercharger market include ABB, Tesla, Siemens, ChargePoint, and EVBox. These companies are leading the market through technological innovation, strategic partnerships, and extensive charging networks worldwide.

Growth drivers include increasing global EV sales, government investments in charging infrastructure, and the automotive industrys shift towards electric vehicles. The demand for ultra-fast charging solutions to reduce EV downtime is a critical factor pushing market expansion.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.