Global In-Vehicle Computer System Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD1567

December 2024

80

About the Report

Global In-Vehicle Computer System Market Overview

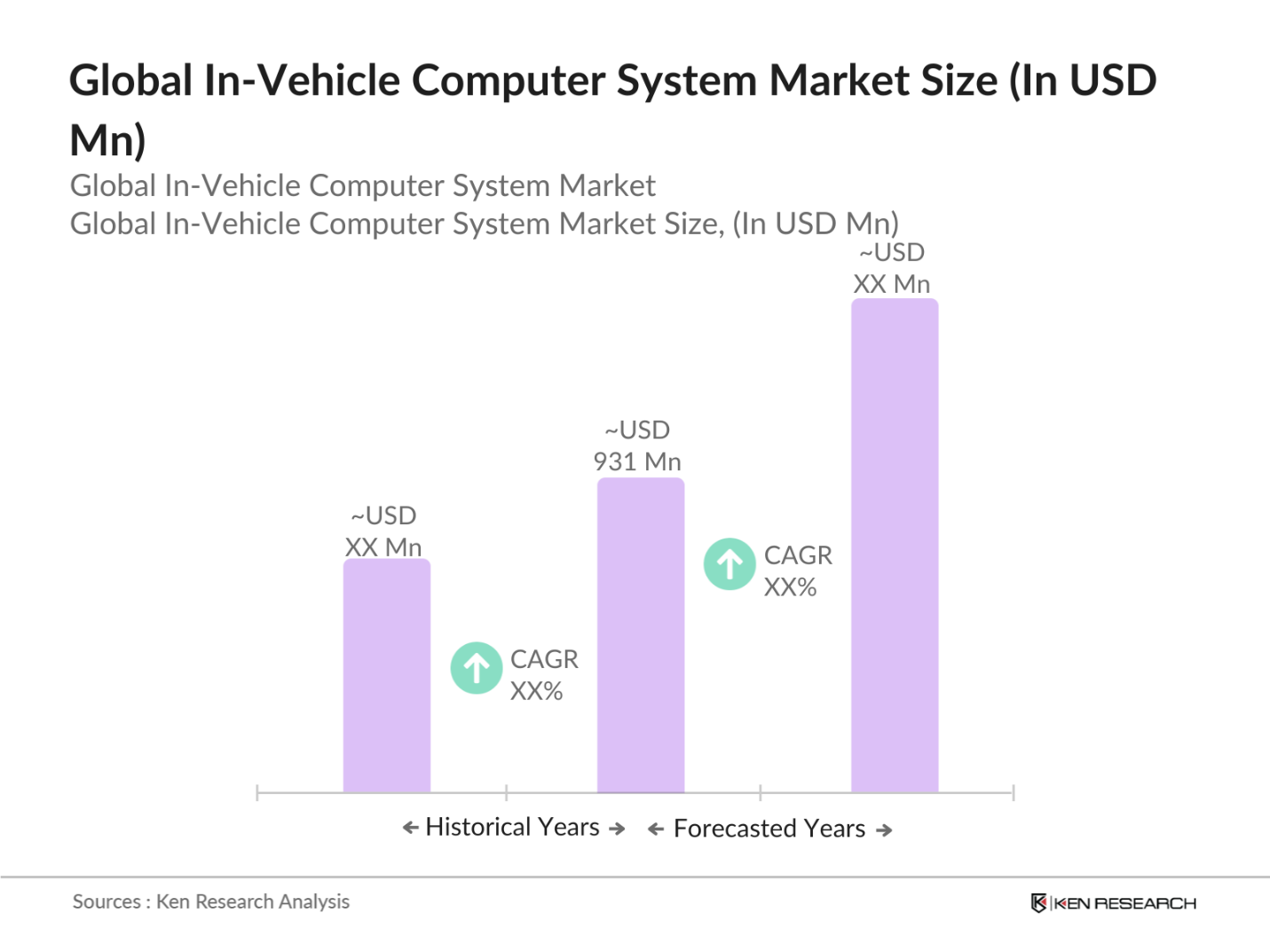

- The Global In-Vehicle Computer System market is valued at USD 931 million, based on a five-year historical analysis. This market is driven by the rapid advancement in automotive technologies and the increasing demand for connected vehicles. Automakers are continuously integrating advanced systems such as ADAS (Advanced Driver Assistance Systems), infotainment, and telematics control units, which have significantly contributed to the market size. The increased consumer preference for vehicle safety, comfort, and real-time data is another factor driving the market.

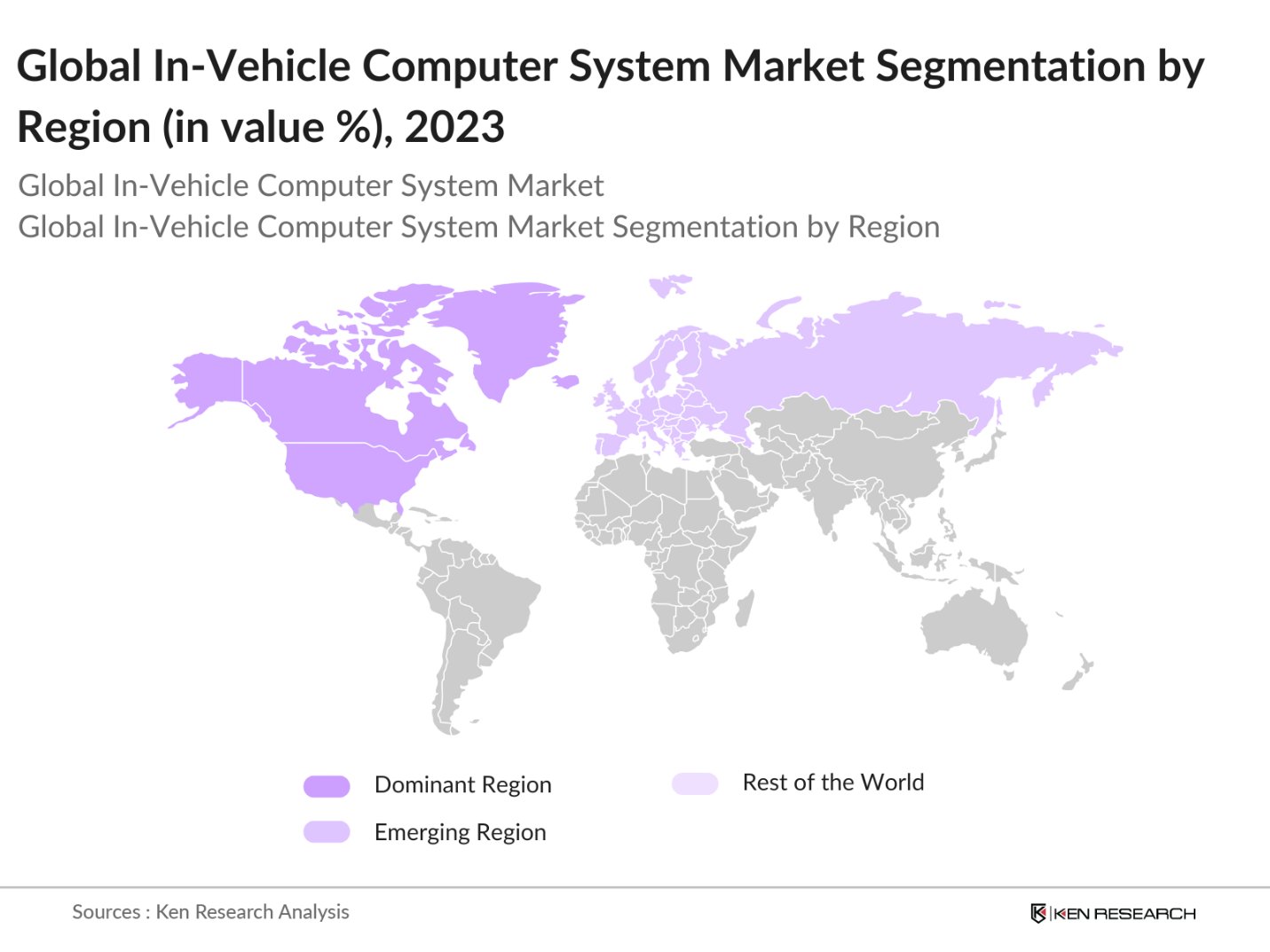

- Countries such as the United States, Germany, and China dominate the market due to their well-established automotive industries, technological advancements, and heavy investments in electric vehicles and autonomous driving. These countries host major automotive manufacturers and technology providers, which gives them an edge in innovation and large-scale production. Moreover, supportive government policies and significant R&D spending have enabled these regions to maintain their dominant position in the global market.

- Governments worldwide have implemented stringent vehicle safety mandates, requiring automakers to integrate advanced safety technologies into their vehicles. In 2024, over 50 countries, including the United States, the EU, and Japan, have mandated the use of specific safety features such as automatic emergency braking (AEB) and lane-keeping assistance in all new vehicles. These regulations have spurred the development and adoption of in-vehicle computer systems that support these safety features, driving market growth. The widespread adoption of these systems is particularly evident in Europe, where compliance with the European New Car Assessment Programme (Euro NCAP) standards is mandatory.

Global In-Vehicle Computer System Market Segmentation

By Region: The market is segmented by region into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. North America holds the largest share of the global in-vehicle computer system market. The region's dominance is primarily due to its leading position in the automotive and technology industries. North America is home to major automotive manufacturers and tech giants that are at the forefront of developing autonomous and connected vehicle technologies. In addition, the strong presence of tech-focused start-ups and innovation hubs, especially in the United States, further propels market growth in this region.

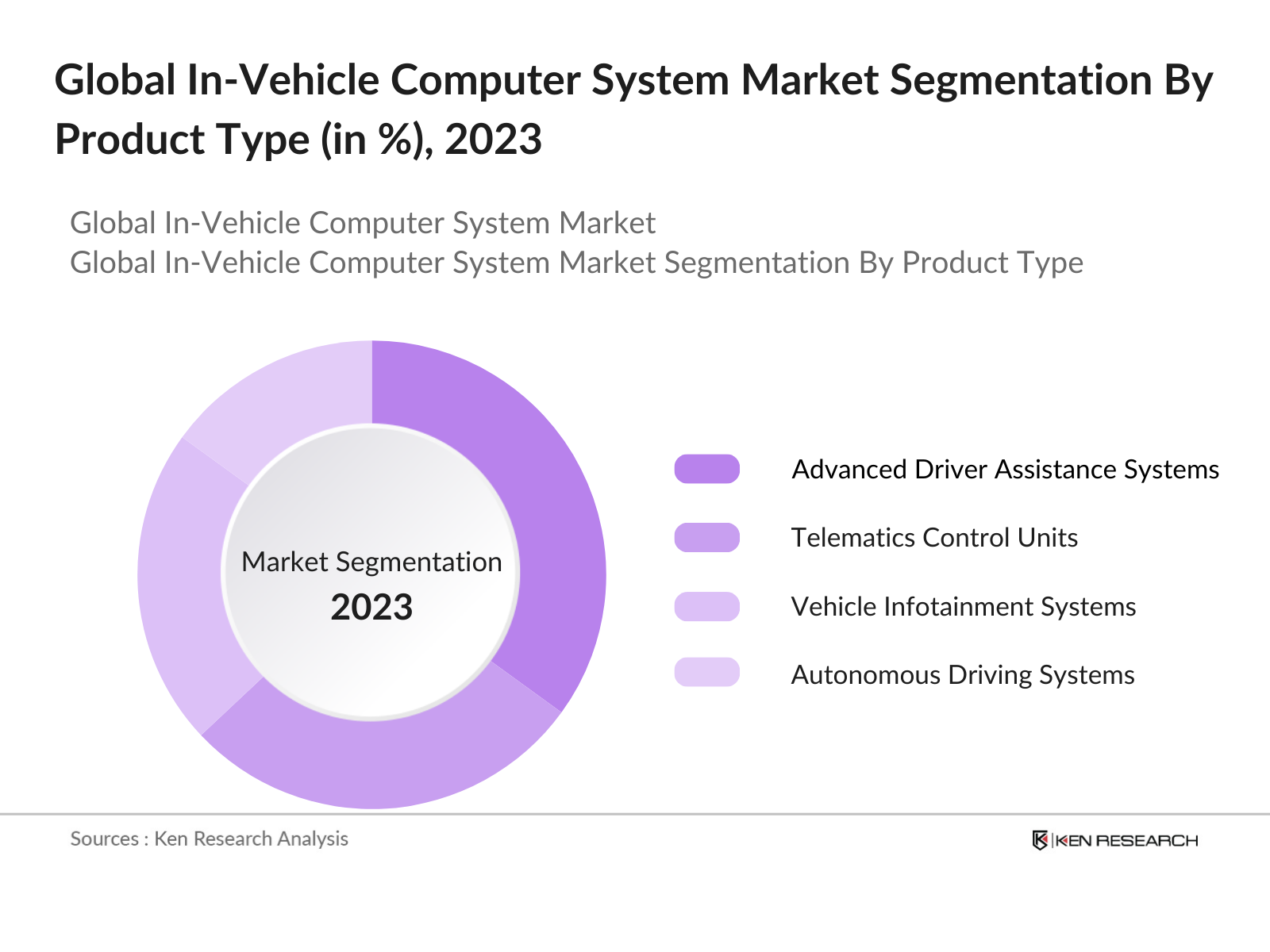

By Product Type: The global in-vehicle computer system market is segmented by product type into vehicle infotainment systems, advanced driver assistance systems (ADAS), telematics control units, autonomous driving systems, and vehicle surveillance systems. Recently, ADAS has gained the largest market share under the product type segmentation. This dominance is attributed to the increasing emphasis on vehicle safety features, stringent government regulations related to road safety, and the growing consumer awareness of the benefits of autonomous driving technologies. ADAS systems, which include features like lane-keeping assistance, adaptive cruise control, and collision avoidance systems, have seen widespread adoption, especially in premium vehicles.

By Application: The market is segmented by application into passenger vehicles, commercial vehicles, electric vehicles, and fleet management. Electric vehicles hold a significant market share under the application category. The rapid growth of the electric vehicle (EV) industry globally, especially in regions like North America and Europe, is driving the adoption of in-vehicle computer systems. EVs, with their advanced electronic architecture, demand highly sophisticated computing systems to manage battery performance, driving efficiency, and infotainment. This growing reliance on in-vehicle computers has positioned electric vehicles as a dominant sub-segment in the market.

Global In-Vehicle Computer System Market Competitive Landscape

The global in-vehicle computer system market is characterized by the presence of several key players. Major companies have established strong R&D capabilities and are investing heavily in the development of advanced systems, leading to high market consolidation. Companies such as Continental AG, Robert Bosch GmbH, and Intel Corporation dominate the market, leveraging their expertise in automotive technologies and strong partnerships with vehicle manufacturers.

|

Company Name |

Established Year |

Headquarters |

Revenue (USD bn) |

Number of Employees |

Product Portfolio |

Geographic Presence |

R&D Investment |

Partnerships |

|

Continental AG |

1871 |

Hanover, Germany |

_ |

_ |

_ |

_ |

_ |

_ |

|

Robert Bosch GmbH |

1886 |

Gerlingen, Germany |

_ |

_ |

_ |

_ |

_ |

_ |

|

Intel Corporation |

1968 |

Santa Clara, USA |

_ |

_ |

_ |

_ |

_ |

_ |

|

NXP Semiconductors |

2006 |

Eindhoven, Netherlands |

_ |

_ |

_ |

_ |

_ |

_ |

|

Qualcomm Technologies Inc. |

1985 |

San Diego, USA |

_ |

_ |

_ |

_ |

_ |

_ |

Global In-Vehicle Computer System Industry Analysis

Growth Drivers

- Rising demand for connected vehicles: The demand for connected vehicles is rapidly increasing as global automotive production integrates more advanced technologies. In 2024, the total number of connected vehicles on the road is expected to exceed 500 million globally, driven by increasing internet penetration and expanding mobile networks (IMF, 2024). The global expansion of 4G and 5G networks has played a significant role in facilitating real-time vehicle-to-vehicle and vehicle-to-infrastructure communications. Countries like the United States and China have implemented policies promoting the adoption of connected vehicles to improve road safety and optimize traffic management, further pushing market demand.

- Growth in ADAS: The adoption of Advanced Driver Assistance Systems (ADAS) has been bolstered by stringent government safety regulations and consumer preference for enhanced driving experiences. By 2024, around 80 million vehicles worldwide are expected to be equipped with ADAS features such as adaptive cruise control and lane departure warning, with Europe and North America leading the charge in terms of adoption. According to World Bank reports, road safety policies have emphasized mandatory ADAS technologies in new vehicle models, particularly in the EU and Japan, driving the integration of in-vehicle computer systems that support these features.

- Increased need for vehicle safety and monitoring: The rise in global logistics and e-commerce activities has fueled the demand for fleet management systems, which rely on in-vehicle computer systems for real-time monitoring and safety compliance. As of 2023, global freight volumes reached 57.7 billion tons, emphasizing the need for efficient fleet management solutions. Countries such as the United States, with its massive logistics network, have adopted comprehensive vehicle safety monitoring systems to optimize fleet operations, reduce downtime, and ensure driver safety. This trend is also evident in India and China, where regulatory bodies have mandated fleet management technology for commercial transport.

Market Challenges

- High implementation costs: The high costs associated with implementing sophisticated in-vehicle computer systems, including hardware, software, and maintenance, remain a significant barrier to widespread adoption. For instance, the average cost of integrating ADAS and connected vehicle systems in a mid-range car is estimated at $1,500 to $3,000, a significant expense for automakers in developing markets. According to the IMF, low-income economies may struggle with adoption due to higher import taxes on technology and limited government support, particularly in Africa and Southeast Asia, where the cost-benefit ratio remains skewed against immediate implementation.

- Data security concerns: As in-vehicle computer systems become more connected, the threat of cyberattacks has risen significantly. In 2023, over 3 million cyber incidents targeting automotive systems were reported globally, with malicious hackers exploiting vulnerabilities in software and communication channels. This trend is particularly concerning in regions with high rates of connected vehicle adoption, such as the United States, where the Department of Homeland Security issued multiple warnings regarding the cybersecurity risks associated with vehicle-to-infrastructure (V2I) communications. The challenge for automakers lies in developing robust cybersecurity frameworks to mitigate these risks without increasing system complexity or cost.

Global In-Vehicle Computer System Market Future Outlook

Over the next five years, the Global In-Vehicle Computer System market is expected to experience significant growth driven by continuous advancements in automotive technology, increasing demand for connected and autonomous vehicles, and growing regulatory mandates for vehicle safety. The adoption of 5G connectivity, AI-driven systems, and edge computing will further accelerate market expansion. The integration of in-vehicle computer systems with smart city infrastructure will provide new opportunities for growth, especially in the electric and autonomous vehicle sectors. As governments across the globe push for safer, smarter, and more efficient transport systems, in-vehicle computer systems will play a pivotal role in shaping the future of mobility.

Opportunities

- Expansion of electric vehicles: The global push for reducing carbon emissions has accelerated the adoption of electric vehicles (EVs), with over 16.5 million EVs on the road by the end of 2023, according to the International Energy Agency. The increasing demand for EVs presents a significant opportunity for in-vehicle computer system providers to cater to the need for advanced battery management, real-time monitoring, and vehicle-to-grid (V2G) communications. Countries like Norway and Germany, where EV adoption is highest, have implemented favorable government policies that encourage the integration of intelligent in-vehicle systems to manage energy consumption and optimize vehicle performance.

- Growing IoT infrastructure: The rapid expansion of IoT infrastructure globally supports the proliferation of in-vehicle computer systems. By 2024, there will be an estimated 28 billion IoT-connected devices worldwide, according to the IMF, and a significant portion of these devices will be in the automotive sector. The growing IoT ecosystem facilitates real-time data exchange between vehicles and external networks, enhancing services such as predictive maintenance, fleet management, and real-time navigation. Countries like China and the United States are at the forefront of building comprehensive IoT infrastructures, which provide substantial growth opportunities for the automotive in-vehicle computer systems market.

Scope of the Report

|

Product Type |

Vehicle Infotainment Systems Advanced Driver Assistance Systems (ADAS) Telematics Control Units Autonomous Driving Systems Vehicle Surveillance Systems |

|

Application |

Passenger Vehicles Commercial Vehicles Electric Vehicles Fleet Management |

|

Technology |

Edge Computing Artificial Intelligence (AI) Cloud Computing V2X Technology (Vehicle-to-Everything) 5G Connectivity |

|

Component |

Central Processing Units (CPUs) Graphics Processing Units (GPUs) Network Interfaces Sensors and Cameras |

|

Region |

North America Europe Asia Pacific Latin America Middle East and Africa |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Automotive OEMs

Technology Companies

Electric Vehicle Companies

Fleet Management Companies

Government Agencies (National Highway Traffic Safety Administration, European Automobile Manufacturers' Association)

Investments and Venture Capitalist Firms

Smart City Infrastructure Industry

Regulatory Bodies (US Department of Transportation, European Union Road Safety Agency)

Companies

Players Mentioned in the Report:

Continental AG

Robert Bosch GmbH

Intel Corporation

NXP Semiconductors

Qualcomm Technologies Inc.

NVIDIA Corporation

Denso Corporation

Aptiv PLC

Harman International Industries Inc.

ZF Friedrichshafen AG

Veoneer Inc.

Panasonic Corporation

LG Electronics Inc.

TomTom NV

Visteon Corporation

Table of Contents

1. Global In-Vehicle Computer System Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global In-Vehicle Computer System Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global In-Vehicle Computer System Market Analysis

3.1. Growth Drivers

3.1.1. Increased Demand for Telematics Solutions

3.1.2. Growth in Electric and Autonomous Vehicles

3.1.3. Rising Focus on Driver Safety and Connectivity

3.1.4. Expansion of 5G Network Infrastructure

3.2. Market Challenges

3.2.1. High Costs of Implementation

3.2.2. Cybersecurity Concerns in Vehicle Systems

3.2.3. Complexity in System Integration

3.3. Opportunities

3.3.1. Advancements in AI and Machine Learning Applications

3.3.2. Growing Fleet Management Adoption in Emerging Markets

3.3.3. Partnerships with OEMs and Aftermarket Solution Providers

3.4. Trends

3.4.1. Adoption of Edge Computing in Vehicles

3.4.2. Integration of Advanced Driver Assistance Systems (ADAS)

3.4.3. Development of High-Performance Computing Units

3.5. Government Regulation

3.5.1. Vehicle Safety Standards

3.5.2. Mandates on Connected Vehicle Technology

3.5.3. Data Privacy and Cybersecurity Compliance

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porter’s Five Forces

3.9. Competition Ecosystem

4. Global In-Vehicle Computer System Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Commercial Vehicles

4.1.3. Electric Vehicles

4.2. By Offering Type (In Value %)

4.2.1. Hardware

4.2.2. Software

4.2.3. Services

4.3. By Application (In Value %)

4.3.1. Infotainment and Multimedia

4.3.2. Telematics Control Units

4.3.3. Vehicle Diagnostics

4.4. By Connectivity (In Value %)

4.4.1. 4G LTE

4.4.2. 5G

4.4.3. Satellite Connectivity

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5. Global In-Vehicle Computer System Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Intel Corporation

5.1.2. NXP Semiconductors

5.1.3. NVIDIA Corporation

5.1.4. Bosch Group

5.1.5. Continental AG

5.1.6. Qualcomm Technologies Inc.

5.1.7. Harman International

5.1.8. Garmin Ltd.

5.1.9. Panasonic Corporation

5.1.10. Advantech Co. Ltd.

5.1.11. APTIV PLC

5.1.12. LG Electronics

5.1.13. Valeo S.A.

5.1.14. Fujitsu Limited

5.1.15. Renesas Electronics

5.2. Cross Comparison Parameters (Revenue, Headquarters, Employee Count, Product Offering, Connectivity Type, Market Share, Patents, R&D Investment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global In-Vehicle Computer System Market Regulatory Framework

6.1. Vehicle Connectivity Standards

6.2. Cybersecurity Standards

6.3. Certification Requirements

7. Global In-Vehicle Computer System Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global In-Vehicle Computer System Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Offering Type (In Value %)

8.3. By Application (In Value %)

8.4. By Connectivity (In Value %)

8.5. By Region (In Value %)

9. Global In-Vehicle Computer System Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase of research involves creating an ecosystem map of the global in-vehicle computer system market. Key variables, including market drivers, competitive landscape, and product categories, are identified using extensive desk research.

Step 2: Market Analysis and Construction

This phase includes historical data analysis of product penetration, revenue generation, and market trends. In-vehicle computer systems' adoption rate across various vehicle segments is evaluated to estimate market size and forecast future growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with industry experts, including representatives from automotive manufacturers and technology providers. These consultations ensure the accuracy and reliability of data.

Step 4: Research Synthesis and Final Output

In the final phase, comprehensive data is compiled and analyzed to produce the final report. The findings are cross-verified through engagement with multiple stakeholders, ensuring a robust and precise market analysis.

Frequently Asked Questions

01. How big is the Global In-Vehicle Computer System Market?

The global in-vehicle computer system market is valued at USD 931 million, driven by rapid advancements in automotive technologies and growing demand for connected and autonomous vehicles.

02. What are the challenges in the Global In-Vehicle Computer System Market?

Challenges include high implementation costs, data security concerns, and integration complexities due to diverse automotive systems.

03. Who are the major players in the Global In-Vehicle Computer System Market?

Key players in the market include Continental AG, Robert Bosch GmbH, Intel Corporation, NXP Semiconductors, and Qualcomm Technologies Inc.

04. What are the growth drivers of the Global In-Vehicle Computer System Market?

Growth drivers include the increasing demand for vehicle safety and monitoring systems, advancements in AI and 5G, and the expansion of electric and autonomous vehicles.

05. What trends are shaping the Global In-Vehicle Computer System Market?

Trends include the adoption of edge computing, AI-driven predictive maintenance, V2X communication technologies, and integration with smart city infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.