Global Law Enforcement Software Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD7214

November 2024

95

About the Report

Global Law Enforcement Software Market Overview

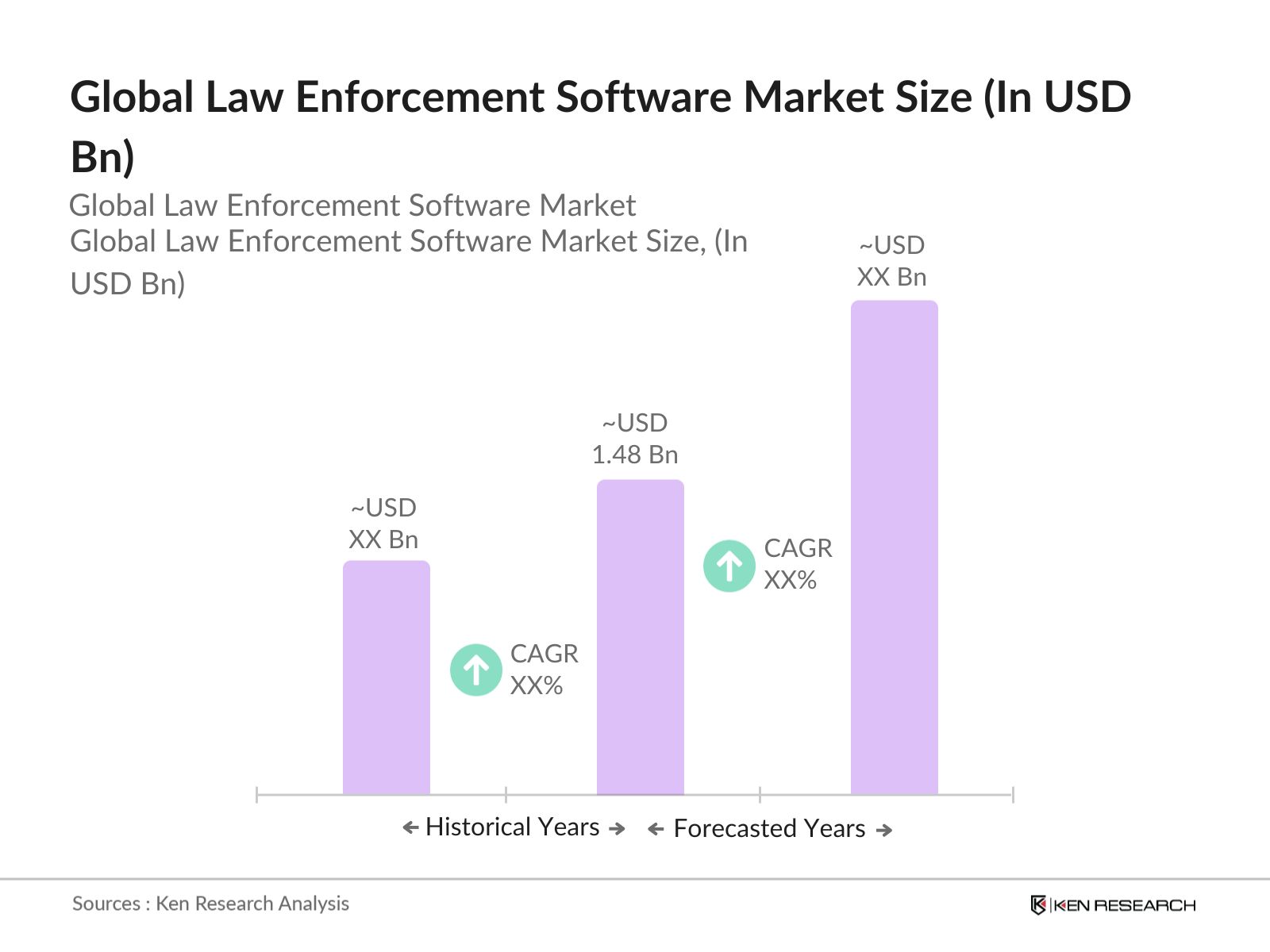

- The global law enforcement software market is valued at USD 1.48 billion, driven by the increasing need for effective digital policing solutions, advanced crime analytics, and real-time data sharing systems. The market has seen significant growth due to technological advancements in artificial intelligence (AI) and cloud computing, enabling more efficient crime detection and prevention. Additionally, the rise in cybercrime and the need for secure law enforcement systems to handle sensitive data further drive the demand for law enforcement software.

- Countries such as the United States and the United Kingdom dominate the law enforcement software market due to their advanced technological infrastructure, high adoption of digital policing tools, and well-established law enforcement agencies. The United States, in particular, benefits from substantial government funding and extensive research initiatives to enhance public safety and crime control. In Europe, countries like Germany and the UK lead due to strong investments in public safety and their advanced data protection regulations.

- In 2024, governments worldwide are enacting stricter cybercrime legislation to tackle the growing threat of cybercriminal activities. The European Unions ePrivacy Regulation and the United States Cybersecurity Information Sharing Act are two examples of legislative frameworks that regulate the sharing of digital evidence while ensuring data protection. Over 130 countries now have national legislation aimed at protecting citizens data, a significant increase from just 80 countries in 2018. These laws are critical in ensuring the safe deployment of law enforcement software.

Global Law Enforcement Software Market Segmentation

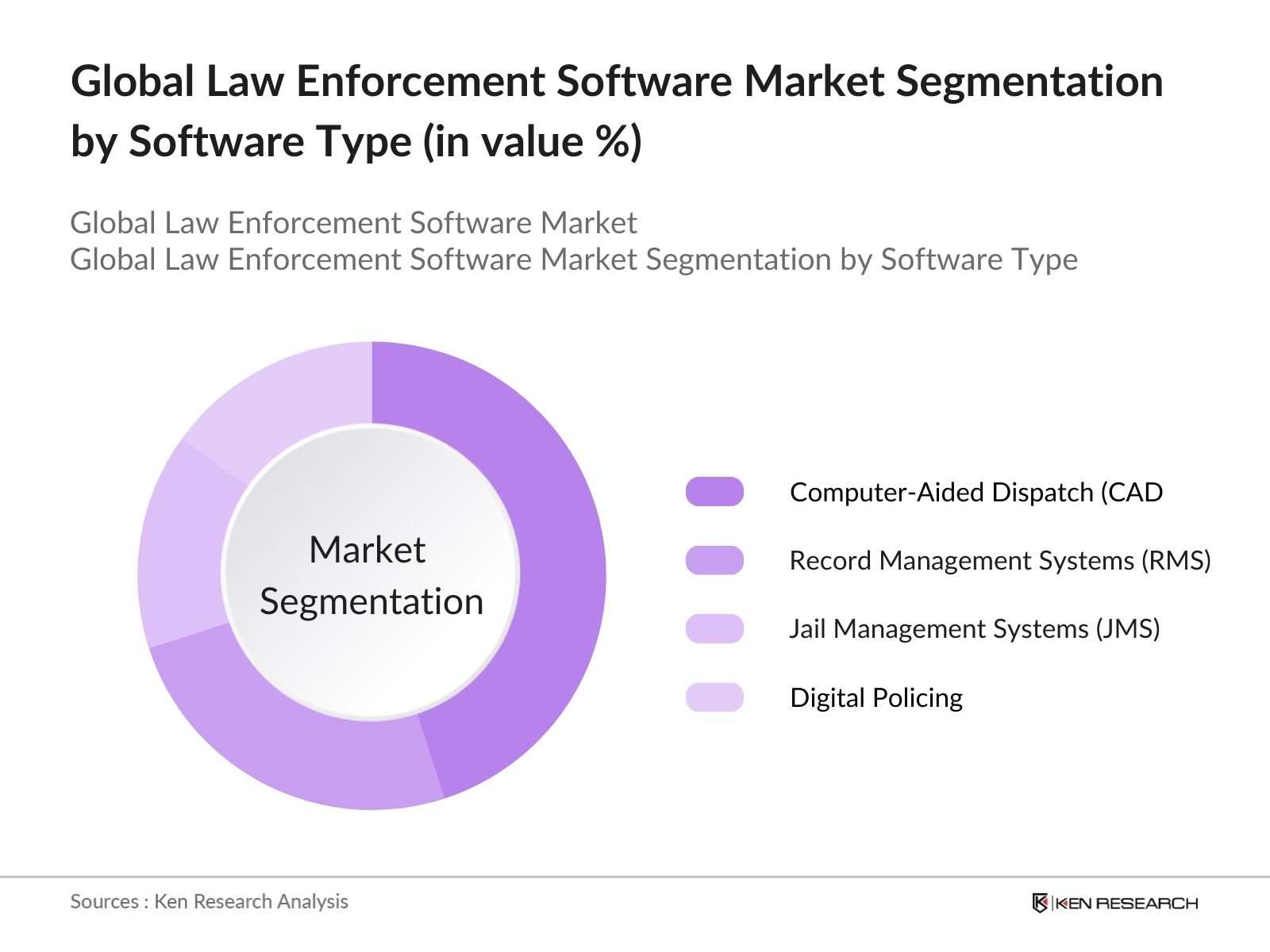

- By Software Type: The global law enforcement software market is segmented by software type into Computer-Aided Dispatch (CAD), Record Management Systems (RMS), Jail Management Systems (JMS), Digital Policing, and Crime Analytics. Computer-Aided Dispatch (CAD) has a dominant market share due to its widespread use in managing emergency response operations and optimizing dispatch efficiency. CAD systems are critical for real-time incident management, which makes them indispensable for law enforcement agencies aiming to improve response times. Additionally, the integration of CAD with GPS tracking and video surveillance systems has strengthened its position in the market.

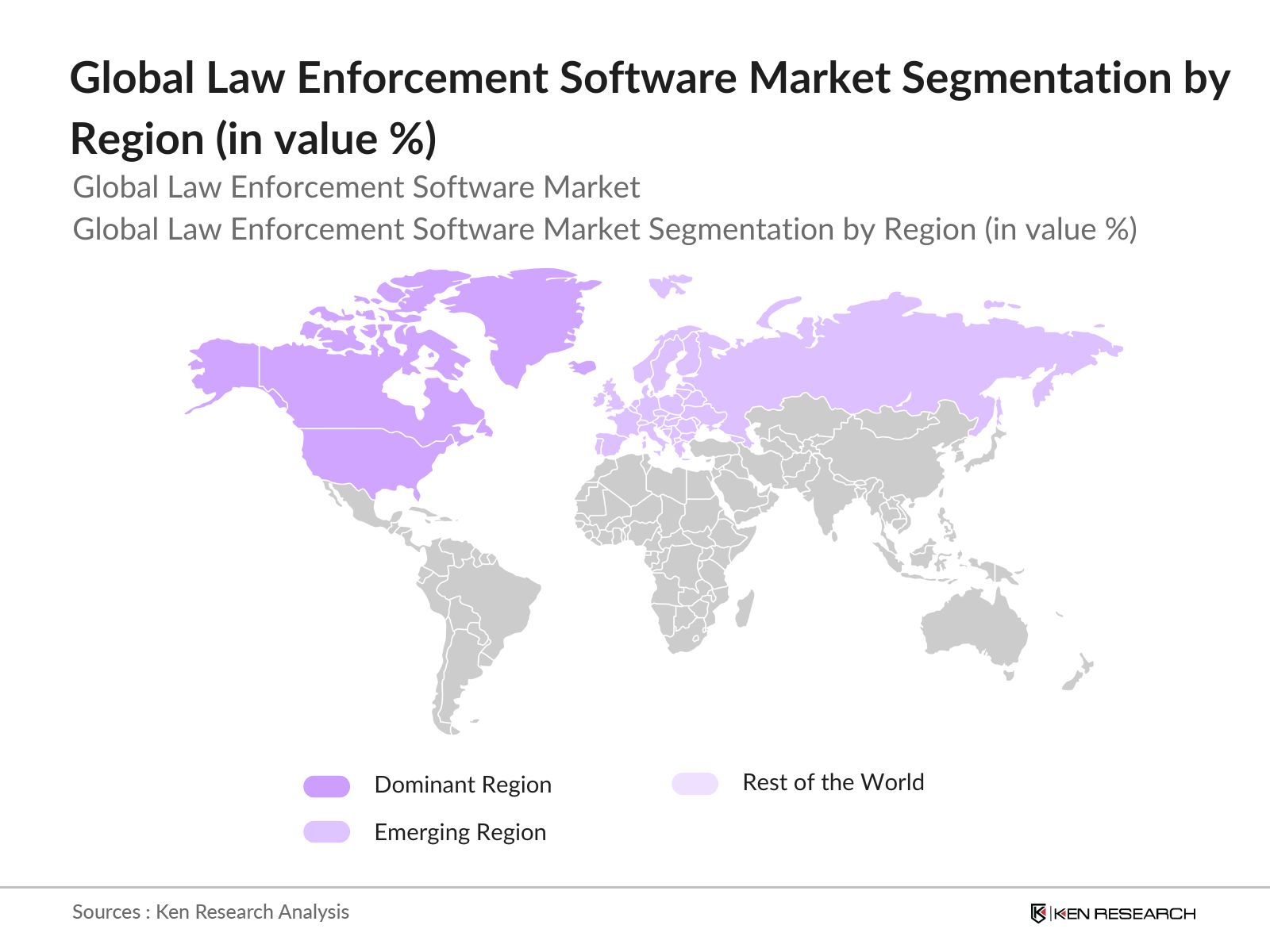

- By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America, led by the United States, dominates the market due to substantial government investments in public safety technologies, along with a high focus on cybersecurity and crime analytics. The regions advanced law enforcement infrastructure and proactive approach to adopting digital policing solutions also contribute to its leading market position. Europe follows, driven by strict regulations surrounding public safety and data privacy, particularly in countries like the UK and Germany.

- By Deployment Model: The law enforcement software market is categorized by deployment model into On-Premise and Cloud-Based.Cloud-based solutions hold a significant market share due to their scalability, flexibility, and cost-efficiency. The growing shift toward cloud-based platforms is driven by the need for real-time data access, better collaboration between agencies, and cost reduction in hardware infrastructure. Cloud solutions also enable seamless software updates and integration with AI and IoT technologies, further enhancing their popularity among law enforcement agencies.

Global Law Enforcement Software Market Competitive Landscape

The global law enforcement software market is characterized by the presence of both established global technology players and specialized providers of law enforcement solutions. Major companies focus on offering integrated software platforms that combine various tools such as CAD, RMS, and analytics into a cohesive solution. These key players dominate the market through a mix of partnerships with government agencies, innovative product launches, and expansions into new regions.

|

Company Name |

Establishment Year |

Headquarters |

Product Offerings |

Global Presence |

R&D Investments |

Revenue (USD Bn) |

Strategic Partnerships |

Employee Count |

|

Axon |

1993 |

Scottsdale, AZ, USA |

- |

- |

- |

- |

- |

- |

|

Motorola Solutions |

1928 |

Chicago, IL, USA |

- |

- |

- |

- |

- |

- |

|

NEC Corporation |

1899 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

|

IBM Corporation |

1911 |

Armonk, NY, USA |

- |

- |

- |

- |

- |

- |

|

Oracle Corporation |

1977 |

Redwood City, CA, USA |

- |

- |

- |

- |

- |

- |

Global Law Enforcement Software Industry Analysis

Growth Drivers

- Increased Adoption of Digital Policing Solutions: The global law enforcement sector has witnessed a significant shift towards digital policing tools due to the rising complexity of criminal activities and the need for efficient response mechanisms. In 2024, governments worldwide allocated approximately $93 billion toward digital transformation initiatives in the public safety sector, including investments in digital policing solutions. These platforms improve data collection, evidence management, and operational efficiency, leading to faster response times. The World Bank reports that this shift is critical in enhancing the efficiency of police forces, particularly in urban areas facing high crime rates.

- Rising Cybercrime and Need for Advanced Tools: Cybercrime is projected to cost the global economy $8.2 trillion in 2024, according to the IMF. This has escalated the demand for advanced software solutions in law enforcement to monitor, track, and prosecute cybercriminals. Law enforcement agencies are increasingly adopting tools like forensic software and blockchain for tracking illicit activities across cyberspace. As cybersecurity threats grow in complexity, countries like the United States and the European Union have significantly ramped up investments in digital forensics and cybersecurity training programs for law enforcement officers.

- Government Initiatives for Law Enforcement Modernization: Governments across the globe are driving modernization efforts to strengthen law enforcement agencies. In 2024, the US government set aside $1.4 billion in federal funds to upgrade digital infrastructures for police departments, focusing on the adoption of body-worn cameras and mobile data terminals. Similarly, European Union member states invested approximately 760 million in enhancing their digital capabilities for law enforcement. These initiatives aim to modernize outdated systems, improve communication, and increase transparency in policing operations.

Market Restraints

- High Implementation Costs: Implementing advanced law enforcement software requires significant investment, particularly in developing economies. In 2023, the average cost of deploying digital policing systems, including software and hardware integration, ranged from $400,000 to $1.2 million per police department, depending on the scale and requirements. This creates a financial barrier for law enforcement agencies with limited budgets. According to the World Bank, the high costs have slowed the adoption of digital policing solutions in countries with GDP per capita below $10,000.

- Data Privacy and Security Concerns: As law enforcement agencies handle sensitive personal information, data privacy and security concerns remain paramount. In 2024, cyberattacks on law enforcement agencies resulted in the exposure of over 12 million confidential records globally. Governments are under pressure to enforce stricter regulations to safeguard personal data. The European Unions General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) mandate stringent data protection measures, but compliance remains a challenge for many agencies.

Global Law Enforcement Software Market Future Outlook

Over the next five years, the global law enforcement software market is expected to experience strong growth driven by increasing investments in public safety technologies, growing concerns about cybercrime, and advancements in digital policing solutions. The rapid adoption of AI, machine learning, and predictive analytics in crime prevention and investigation will continue to fuel market demand. Additionally, the shift toward cloud-based platforms, which offer scalable and cost-efficient solutions for law enforcement agencies, will be a key growth driver.

Market Opportunities

- Growth of Cloud-Based Solutions: The adoption of cloud-based law enforcement solutions has been growing rapidly, as these platforms provide scalable storage and analytics capabilities. In 2024, approximately 70,000 police departments globally are expected to use cloud-based solutions for case management and data storage. Cloud technology helps reduce the need for physical infrastructure, lowering operational costs and improving accessibility for agencies with limited resources. Governments in regions like North America and Europe have set aside funds to accelerate the shift towards cloud-based law enforcement tools.

- Increasing Demand for Predictive Policing Technologies: The growing use of artificial intelligence (AI) and machine learning (ML) in predictive policing is transforming law enforcement practices. In 2023, more than 12,000 police departments worldwide deployed AI-based tools to analyze crime patterns and predict criminal behavior. This has led to a reduction in crime rates in urban centers, particularly in cities like London and New York, where predictive policing technologies have helped law enforcement agencies anticipate and prevent incidents more effectively.

Scope of the Report

|

Segment |

Sub-Segment |

|

Software Type |

Computer-Aided Dispatch (CAD) |

|

Record Management System (RMS) |

|

|

Jail Management System (JMS) |

|

|

Digital Policing |

|

|

Crime Analytics |

|

|

Deployment Model |

On-Premise |

|

Cloud-Based |

|

|

Application |

Crime Management |

|

Incident Management |

|

|

Mobile Policing |

|

|

Forensic Investigation |

|

|

End-User |

Police Departments |

|

Federal Law Enforcement Agencies |

|

|

Private Security Organizations |

|

|

Judicial Departments |

|

|

Region |

North America |

|

Europe |

|

|

Asia-Pacific |

|

|

Latin America |

|

|

Middle East & Africa |

Products

Key Target Audience

Law Enforcement Agencies

Federal Law Enforcement Agencies

Public Safety and Crime Prevention Organizations

Police Departments

Government and Regulatory Bodies (US Department of Justice, European Commission)

Private Security Organizations

Investor and Venture Capitalist Firms

Judicial Departments

Companies

Players Mentioned in the Report:

Axon

Motorola Solutions, Inc.

NEC Corporation

IBM Corporation

Oracle Corporation

Palantir Technologies

Tyler Technologies, Inc.

Hexagon Safety & Infrastructure

CentralSquare Technologies

NICE Public Safety

SAS Institute

Fujitsu Limited

Esri

ShotSpotter, Inc.

PublicEngines

Table of Contents

1. Global Law Enforcement Software Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Law Enforcement Software Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Law Enforcement Software Market Analysis

3.1. Growth Drivers

3.1.1. Increased Adoption of Digital Policing Solutions

3.1.2. Rising Cybercrime and Need for Advanced Tools

3.1.3. Government Initiatives for Law Enforcement Modernization

3.1.4. Integration with Public Safety and Crime Analytics

3.2. Market Challenges

3.2.1. High Implementation Costs

3.2.2. Data Privacy and Security Concerns

3.2.3. Limited Adoption in Developing Economies

3.2.4. Interoperability of Systems and Legacy Infrastructure

3.3. Opportunities

3.3.1. Growth of Cloud-Based Solutions

3.3.2. Increasing Demand for Predictive Policing Technologies

3.3.3. Emerging AI and Machine Learning Applications

3.3.4. Collaborations Between Public and Private Sectors

3.4. Trends

3.4.1. Use of Real-Time Data Sharing Platforms

3.4.2. Growth in Video Surveillance Analytics

3.4.3. Rise in Mobile Law Enforcement Solutions

3.4.4. Deployment of IoT-Enabled Law Enforcement Tools

3.5. Government Regulations

3.5.1. Cybercrime Legislation and Data Protection Laws

3.5.2. Mandates on Digital Evidence Management

3.5.3. Standards for Body-Worn Cameras (BWC)

3.5.4. National Public Safety Frameworks

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Global Law Enforcement Software Market Segmentation

4.1. By Software Type (In Value %) 4.1.1. Computer-Aided Dispatch (CAD)

4.1.2. Record Management System (RMS)

4.1.3. Jail Management System (JMS)

4.1.4. Digital Policing

4.1.5. Crime Analytics

4.2. By Deployment Model (In Value %) 4.2.1. On-Premise

4.2.2. Cloud-Based

4.3. By Application (In Value %) 4.3.1. Crime Management

4.3.2. Incident Management

4.3.3. Mobile Policing

4.3.4. Forensic Investigation

4.4. By End-User (In Value %) 4.4.1. Police Departments

4.4.2. Federal Law Enforcement Agencies

4.4.3. Private Security Organizations

4.4.4. Judicial Departments

4.5. By Region (In Value %) 4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Law Enforcement Software Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Axon

5.1.2. Motorola Solutions, Inc.

5.1.3. NEC Corporation

5.1.4. IBM Corporation

5.1.5. Oracle Corporation

5.1.6. Palantir Technologies

5.1.7. Tyler Technologies, Inc.

5.1.8. Hexagon Safety & Infrastructure

5.1.9. CentralSquare Technologies

5.1.10. NICE Public Safety

5.1.11. SAS Institute

5.1.12. Fujitsu Limited

5.1.13. Esri

5.1.14. ShotSpotter, Inc.

5.1.15. PublicEngines

5.2. Cross Comparison Parameters (Market Share, Revenue, Global Presence, Number of Employees, Product Portfolio, R&D Investments, Regional Focus, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Law Enforcement Software Market Regulatory Framework

6.1. Criminal Justice Standards

6.2. Data Privacy and Protection Guidelines

6.3. International Crime Data Sharing Protocols

6.4. Body Camera Data Storage Regulations

7. Global Law Enforcement Software Market Future Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Law Enforcement Software Future Market Segmentation

8.1. By Software Type (In Value %)

8.2. By Deployment Model (In Value %)

8.3. By Application (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. Global Law Enforcement Software Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing a comprehensive ecosystem map of the global law enforcement software market. This is achieved through extensive desk research utilizing a combination of proprietary and publicly available databases. Key variables such as market growth drivers, competitive dynamics, and technological trends are identified at this stage.

Step 2: Market Analysis and Construction

In this phase, historical data is gathered and analyzed to assess the market's trajectory, including product penetration rates and the distribution of software types across regions. Data on the number of law enforcement agencies using specific software solutions is also compiled.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed based on the collected data and are validated through consultations with industry experts via computer-assisted telephone interviews (CATI). These interviews provide critical insights into operational challenges and opportunities, further refining the market data.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing the collected data with insights from major law enforcement software vendors. The result is a comprehensive market analysis that accurately captures key market trends, competitive dynamics, and growth projections.

Frequently Asked Questions

01. How big is the Global Law Enforcement Software Market?

The global law enforcement software market is valued at USD 1.48 billion, driven by the increasing need for digital policing solutions and advancements in crime analytics.

02. What are the challenges in the Global Law Enforcement Software Market?

Key challenges include high implementation costs, data security concerns, and the complexity of integrating new systems with legacy infrastructure.

03. Who are the major players in the Global Law Enforcement Software Market?

Major players include Axon, Motorola Solutions, IBM Corporation, NEC Corporation, and Oracle Corporation, known for their robust software solutions and strong partnerships with law enforcement agencies.

04. What are the growth drivers of the Global Law Enforcement Software Market?

Growth drivers include rising cybercrime, advancements in AI and machine learning, government support for digital policing, and the growing adoption of cloud-based solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.