Global Liquid Crystal Polymers Market Outlook to 2030

Region:Global

Author(s):Shambhavi

Product Code:KROD10457

Region:Global

Author(s):Shambhavi

Product Code:KROD10457

December 2024

91

By Product Type: The Global Liquid Crystal Polymers Market is segmented by product type into Standard LCPs and High-Performance LCPs. Recently, High-Performance LCPs have secured a dominant market share in the segmentation by product type. This dominance is attributed to their superior thermal stability, mechanical strength, and excellent electrical properties, making them ideal for demanding applications in electronics and automotive industries. Manufacturers are increasingly focusing on high-performance variants to cater to the evolving needs of high-tech applications, thereby driving the growth of this sub-segment.

By Application: The Global Liquid Crystal Polymers Market is segmented by application into Electronics, Automotive, Aerospace, and Others. The Electronics segment holds the largest market share, driven by the increasing demand for miniaturized and high-performance components in smartphones, wearable devices, and telecommunications equipment. The superior properties of LCPs, such as low dielectric constant and high thermal resistance, make them indispensable in the production of flexible printed circuits and high-frequency connectors, thereby reinforcing their dominance in this application segment.

The Global Liquid Crystal Polymers Market is dominated by a few major players, including local manufacturers and global giants such as Celanese Corporation, Mitsui Chemicals, J. Morita Corporation, Solvay S.A., and Teijin Limited. This consolidation highlights the significant influence of these key companies, which leverage their extensive research and development capabilities, broad product portfolios, and strong distribution networks to maintain a competitive edge in the market.

Over the next five years, the Global Liquid Crystal Polymers Market is expected to show significant growth driven by continuous advancements in material science, expanding applications in high-tech industries, and increasing investments in research and development. The rising demand for lightweight and high-performance materials in automotive and aerospace sectors, coupled with the proliferation of electronic devices, will further propel market expansion. Additionally, ongoing innovations aimed at enhancing the properties of LCPs will open new avenues for their application, ensuring sustained market growth.

|

Segments |

Sub-Segments |

|

Product Type |

Resins |

|

Application |

Electrical & Electronics |

|

Technology |

Injection Molding |

|

End-User |

Original Equipment Manufacturers (OEMs) |

|

Region |

North America |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Rising Demand in Electrical & Electronics Sector

3.1.2 Expansion of Automotive Industry Applications

3.1.3 Technological Advancements in Polymer Manufacturing

3.1.4 Increasing Usage in Medical Applications

3.2 Market Challenges

3.2.1 High Production Costs

3.2.2 Availability of Alternative High-Performance Polymers

3.2.3 Supply Chain Constraints in Raw Materials

3.3 Opportunities

3.3.1 Expanding Applications in 5G and Telecommunication Equipment

3.3.2 Growth in Emerging Economies

3.3.3 Technological Innovations and Patented LCP Products

3.4 Trends

3.4.1 Miniaturization of Electronic Components

3.4.2 Integration in Smart Automotive Electronics

3.4.3 Rise in LCP Recycling Efforts

3.5 Government Regulations

3.5.1 Import/Export Policies on High-Performance Polymers

3.5.2 Environmental Regulations Impacting Production

3.5.3 Standards for Medical and Automotive Applications

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape Analysis

4.1 By Product Type (in USD Bn)

4.1.1 Resins

4.1.2 Films

4.1.3 Fibers

4.2 By Application (in USD Bn)

4.2.1 Electrical & Electronics

4.2.2 Automotive

4.2.3 Medical

4.2.4 Industrial Machinery

4.2.5 Consumer Goods

4.3 By Technology (in USD Bn)

4.3.1 Injection Molding

4.3.2 Extrusion

4.3.3 Blow Molding

4.4 By End-User (in USD Bn)

4.4.1 Original Equipment Manufacturers (OEMs)

4.4.2 Suppliers and Distributors

4.4.3 R&D Organizations

4.5 By Region (in USD Bn)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1 Sumitomo Chemical Co., Ltd.

5.1.2 Celanese Corporation

5.1.3 Solvay S.A.

5.1.4 Polyplastics Co., Ltd.

5.1.5 Toray Industries, Inc.

5.1.6 Ueno Fine Chemicals Industry, Ltd.

5.1.7 RTP Company

5.1.8 Kuraray Co., Ltd.

5.1.9 SABIC

5.1.10 Shanghai PRET Composites Co., Ltd.

5.1.11 Entek International LLC

5.1.12 Murata Manufacturing Co., Ltd.

5.1.13 Nippon Steel Chemical & Material Co., Ltd.

5.1.14 DuPont de Nemours, Inc.

5.1.15 Parker Hannifin Corporation

5.2 Cross Comparison Parameters

5.2.1 Headquarters Location

5.2.2 Revenue

5.2.3 Number of Employees

5.2.4 Product Portfolio Depth

5.2.5 R&D Spending

5.2.6 International Presence

5.2.7 Vertical Integration Level

5.2.8 Patented Technologies

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Subsidies and Grants

6.1 Environmental Compliance Standards

6.2 Certification Processes

6.3 Industrial Quality Standards

7.1 Market Size Projections

7.2 Key Factors Driving Future Growth

8.1 By Product Type (in USD Bn)

8.2 By Application (in USD Bn)

8.3 By Technology (in USD Bn)

8.4 By End-User (in USD Bn)

8.5 By Region (in USD Bn)

9.1 Total Addressable Market (TAM) Analysis

9.2 Strategic Market Positioning

9.3 New Product Development Strategies

9.4 White Space Analysis

Disclaimer Contact UsThe initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Global Liquid Crystal Polymers Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

In this phase, we will compile and analyze historical data pertaining to the Global Liquid Crystal Polymers Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATI) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

The final phase involves direct engagement with multiple liquid crystal polymer manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Global Liquid Crystal Polymers Market.

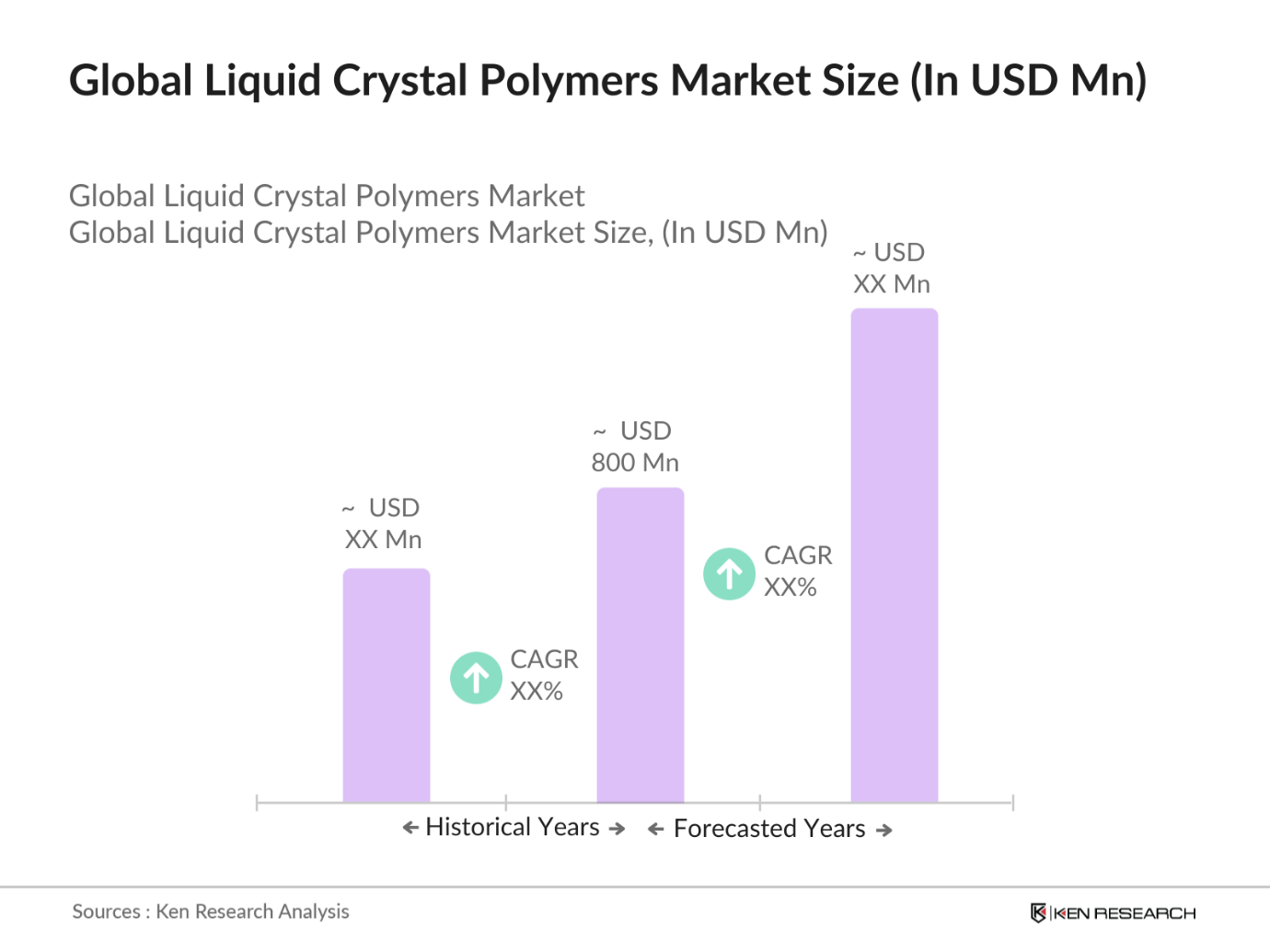

The Global Liquid Crystal Polymers Market was valued at USD 800 million in 2023, driven by increasing demand in high-performance electronic applications, automotive, and aerospace industries.

Challenges include high production costs, limited availability of raw materials, and stringent regulatory standards. Additionally, the complexity of manufacturing processes for high-performance LCPs poses a barrier to market growth.

Key players in the market include Celanese Corporation, Mitsui Chemicals, J. Morita Corporation, Solvay S.A., and Teijin Limited. These companies dominate due to their extensive research and development capabilities and strong global presence.

The market is propelled by factors such as the rising demand for miniaturized electronic components, advancements in material science, and increasing applications in automotive and aerospace industries. Additionally, the growth of the telecommunications sector significantly boosts market expansion.

East Asia dominates the Global Liquid Crystal Polymers Market, primarily due to the strong presence of key manufacturers in Japan and South Korea, advanced technological infrastructure, and significant investments in research and development.

Future trends include the development of more sustainable and eco-friendly LCPs, integration of LCPs in emerging technologies such as flexible electronics and 5G communications, and increased focus on enhancing the thermal and mechanical properties of LCPs to meet the demands of high-performance applications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.