Global Marine Electronics Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD983

Region:Global

Author(s):Shivani Mehra

Product Code:KROD983

December 2024

91

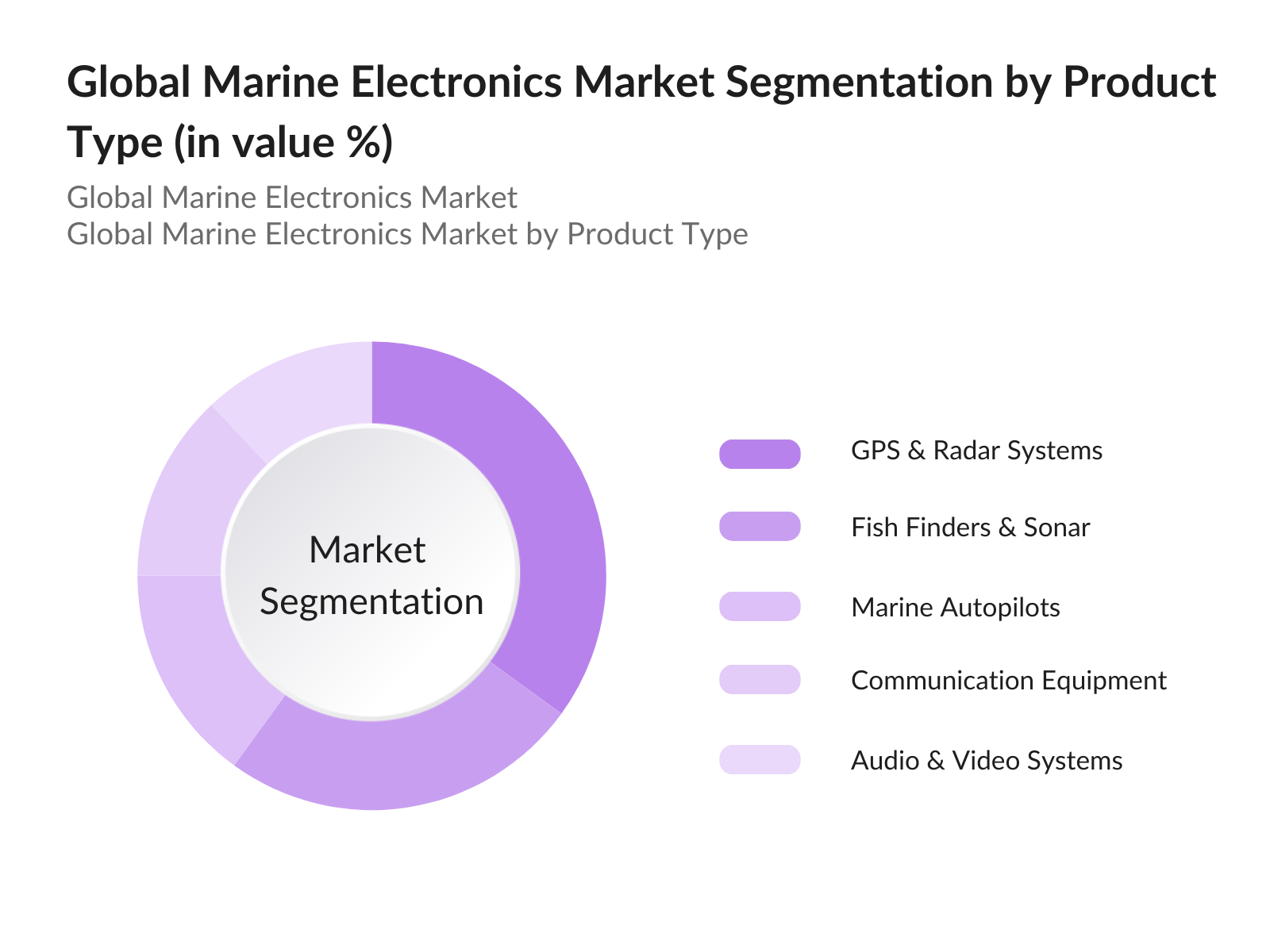

By Product Type: The marine electronics market is segmented by product type into GPS & Radar Systems, Fish Finders & Sonar, Marine Autopilots, Communication Equipment, and Audio & Video Systems. Currently, GPS & Radar Systems dominate, especially in commercial and military segments, due to their critical role in safety and route optimization. The continuous advancements in GPS technology enable more precise navigation, which is essential in busy marine routes and hazardous waters, further bolstering demand.

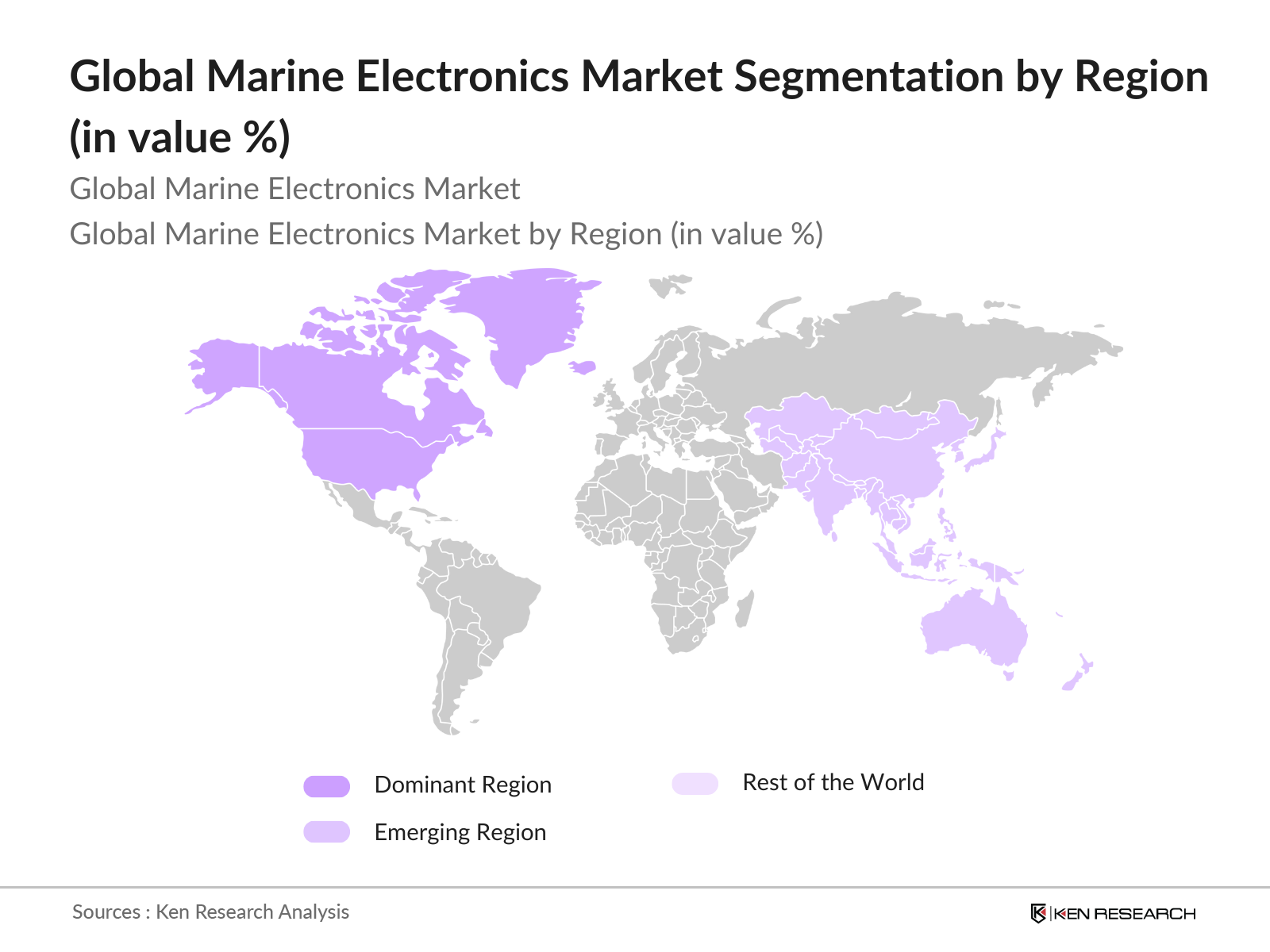

By Region: In terms of geographical segmentation, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest share, benefiting from its substantial investments in maritime infrastructure, especially within the U.S. commercial and recreational boating sectors. These regions exhibit high adoption rates of marine electronics due to the focus on safety and operational efficiency.

The Global Marine Electronics market is characterized by the presence of key players who drive technological innovation, product differentiation, and strategic partnerships to capture market share.

|

Company |

Establishment Year |

Headquarters |

Key Products |

Technology Focus |

Market Presence |

Strategic Initiatives |

Key Partnerships |

Product Innovation |

Regional Focus |

|

Garmin Ltd. |

1989 |

Schaffhausen, CH |

GPS, Radar Systems |

- |

- |

- |

- |

- |

- |

|

Furuno Electric Co., Ltd. |

1938 |

Nishinomiya, JP |

Communication Equip. |

- |

- |

- |

- |

- |

- |

|

Kongsberg Maritime |

1814 |

Kongsberg, NO |

Navigation Systems |

- |

- |

- |

- |

- |

- |

|

Teledyne FLIR LLC |

1978 |

Wilsonville, US |

Thermal Imaging |

- |

- |

- |

- |

- |

- |

|

Northrop Grumman |

1939 |

Falls Church, US |

Defense Electronics |

- |

- |

- |

- |

- |

- |

Market Growth Drivers

Market Challenges:

The marine electronics market is expected to continue its growth trajectory over the next five years, driven by the increasing need for safety, efficiency, and environmental sustainability across maritime sectors. Advancements in navigation, coupled with rising investments in marine infrastructure, especially in emerging economies, will contribute to market expansion. The market will also benefit from ongoing technological developments in autonomous marine systems, particularly in GPS, radar, and underwater sonar applications, which will be critical for various commercial and defense uses.

Market Opportunities:

|

By Product Type |

GPS & Radar Systems Fish Finders & Sonar Marine Autopilots Communication Equipment Audio & Video Systems |

|

By Application |

Merchant Marine Fishing Vessels Yachts/Recreation Military Underwater Exploration Drones |

|

By Vessel Type |

Commercial Vessels Defense & Naval Ships Leisure Boats |

|

By End-User |

Analog Digital Hybrid Systems |

|

By Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Dynamics and Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size Analysis

2.2 Year-On-Year Growth Trends

2.3 Key Market Milestones and Developments

3.1 Market Growth Drivers

3.1.1 Rising Demand for GPS and Radar (Safety, Navigation Precision)

3.1.2 Technological Innovations (Marine Autopilots, Sonar Systems)

3.1.3 Increased Adoption in Military Applications (Passive Radar Systems, Advanced Monitoring)

3.1.4 Demand for Onboard Entertainment Systems (Enhanced Passenger Experience)

3.2 Market Challenges

3.2.1 High Costs of Advanced Sonar Systems (Research & Development Constraints)

3.2.2 Environmental Factors (Waterproofing, Corrosion Resistance)

3.2.3 Regulatory Standards and Compliance (Global and Regional Requirements)

4.1 Opportunities

4.1.1 Integration of AI in Navigation Systems

4.1.2 Expansion in Emerging Markets (APAC, Latin America)

4.1.3 Hybrid Power Systems for Environmental Efficiency

4.2 Emerging Trends

4.2.1 Passive Radar for Military and Commercial Use

4.2.2 Advanced Thermal Imaging (Night and Fog Navigation)

4.2.3 IoT-Enabled Predictive Maintenance (Operational Efficiency)

5.1 By Product Type

5.1.1 GPS & Radar Systems

5.1.2 Fish Finders & Sonar

5.1.3 Marine Autopilots

5.1.4 Communication Equipment

5.1.5 Audio & Video Systems

5.2 By Application

5.2.1 Merchant Marine

5.2.2 Fishing Vessels

5.2.3 Yachts/Recreation

5.2.4 Military Applications

5.2.5 Underwater Exploration Drones

5.3 By Vessel Type

5.3.1 Commercial Vessels

5.3.2 Defense & Naval Ships

5.3.3 Leisure Boats

5.4 By Technology

5.4.1 Analog

5.4.2 Digital

5.4.3 Hybrid Systems

5.5 By Region

5.5.1 North America

5.5.2 Europe

5.5.3 Asia Pacific

5.5.4 Latin America

5.5.5 Middle East & Africa

6.1 Major Competitors in Marine Electronics Market

6.1.1 Garmin Ltd.

6.1.2 Furuno Electric Co., Ltd.

6.1.3 Kongsberg Maritime

6.1.4 Navico Group

6.1.5 Wrtsil Corporation

6.1.6 Northrop Grumman Corporation

6.1.7 Thales Group

6.1.8 Tokyo Keiki Inc.

6.1.9 L3Harris Technologies, Inc.

6.1.10 Japan Radio Co., Ltd.

6.1.11 Teledyne FLIR LLC

6.1.12 ATLAS ELEKTRONIK GmbH

6.1.13 Johnson Outdoors Inc.

6.1.14 Neptune Sonar Ltd.

6.1.15 Sound Metrics Corp.

6.2 Cross Comparison Parameters (Revenue, Technology Focus, Geographic Presence, Innovation Rate, Product Portfolio Depth, Strategic Partnerships, Market Share, R&D Expenditure)

6.3 Market Share Analysis

6.4 Strategic Developments and Initiatives

6.5 Mergers and Acquisitions

6.6 Venture Capital Investments and Funding

7.1 Key Suppliers and Raw Material Analysis

7.2 Key Distribution Channels

7.3 Key Consumers and Demand Centers

7.4 Value Chain Optimization Opportunities

8.1 North America

8.2 Europe

8.3 Asia Pacific

8.4 Latin America

8.5 Middle East & Africa

9.1 Projections by Region

9.2 Key Growth Drivers and Restraints for Future Market

10.1 Strategic Positioning and Investment Opportunities

10.2 Customer Analysis (Cohorts and Behavior Insights)

10.3 White Space Analysis in Product and Regional Markets

Disclaimer Contact UsThe initial phase involved mapping the ecosystem of stakeholders within the Global Marine Electronics Market, utilizing secondary databases to capture extensive market-level information. This phase identified variables like product demand, regulatory influences, and supply chain dynamics.

This phase analyzed historical data covering market penetration, customer segmentation, and technological innovation rates. Data from 2018-2023 was used to build an accurate picture of market trends and drivers, such as the rise in demand for safety and navigation technology.

Through structured consultations with marine technology professionals, market assumptions were verified and refined. These interviews provided critical insights into operational and financial dynamics, bolstering the reliability of data estimates.

The synthesis stage involved direct feedback from manufacturers, covering sales performance, consumer preferences, and product technology. This collaborative input verified the data, enhancing the credibility and depth of the analysis.

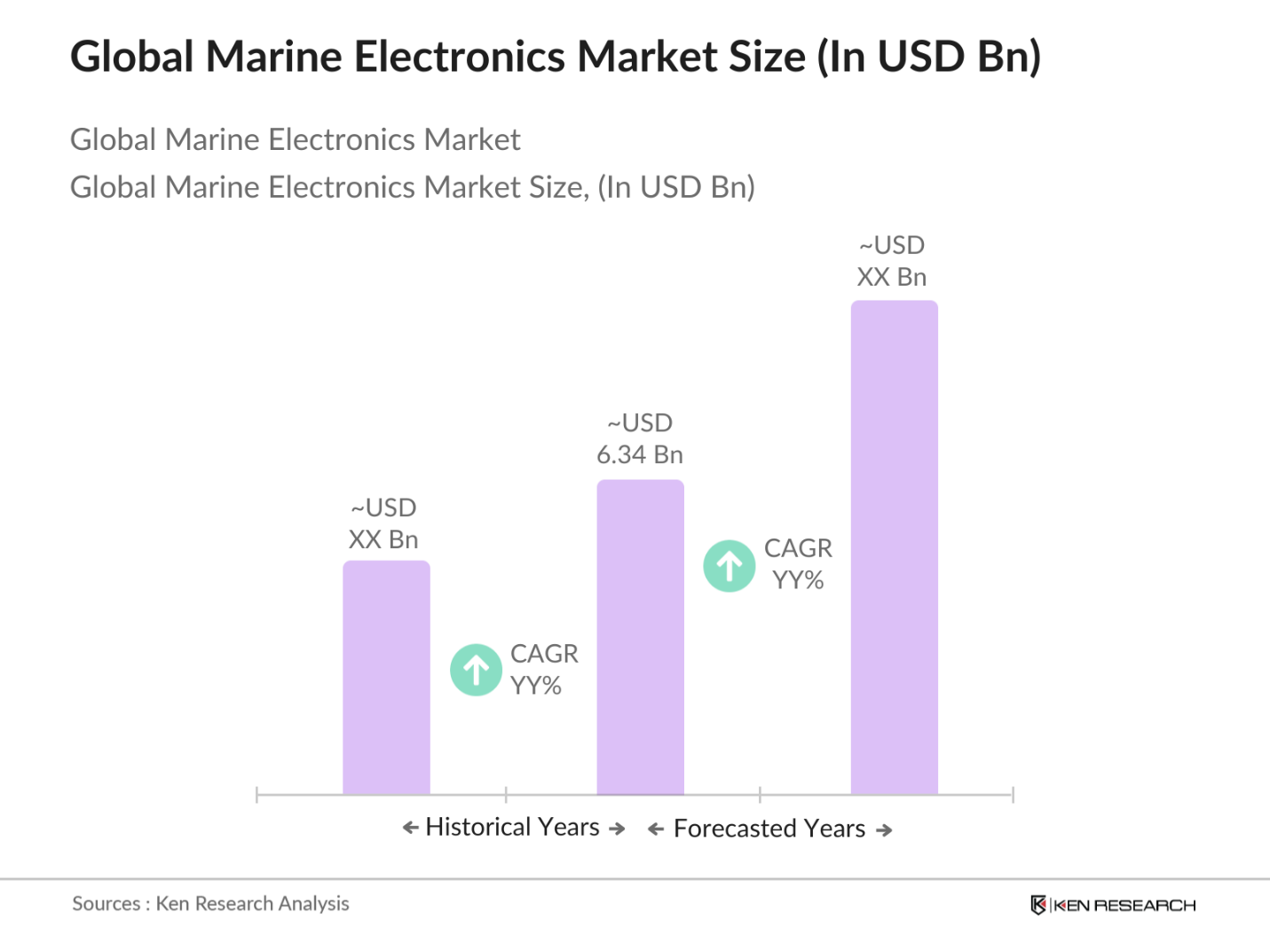

The global marine electronics market is valued at approximately USD 6.34 billion, driven by advancements in navigation systems and increasing adoption in commercial shipping and defense sectors.

Challenges include high costs associated with advanced sonar systems and the need for compliance with strict environmental and safety regulations.

Key players include Garmin Ltd., Furuno Electric Co., Ltd., Kongsberg Maritime, Teledyne FLIR LLC, and Northrop Grumman, each focusing on specific innovations in navigation and communication technologies.

The market is propelled by the growing importance of safety and precision in maritime navigation, particularly in GPS, radar, and thermal imaging technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.