Global Medical Monitoring Devices Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD3149

Region:Global

Author(s):Shivani Mehra

Product Code:KROD3149

December 2024

98

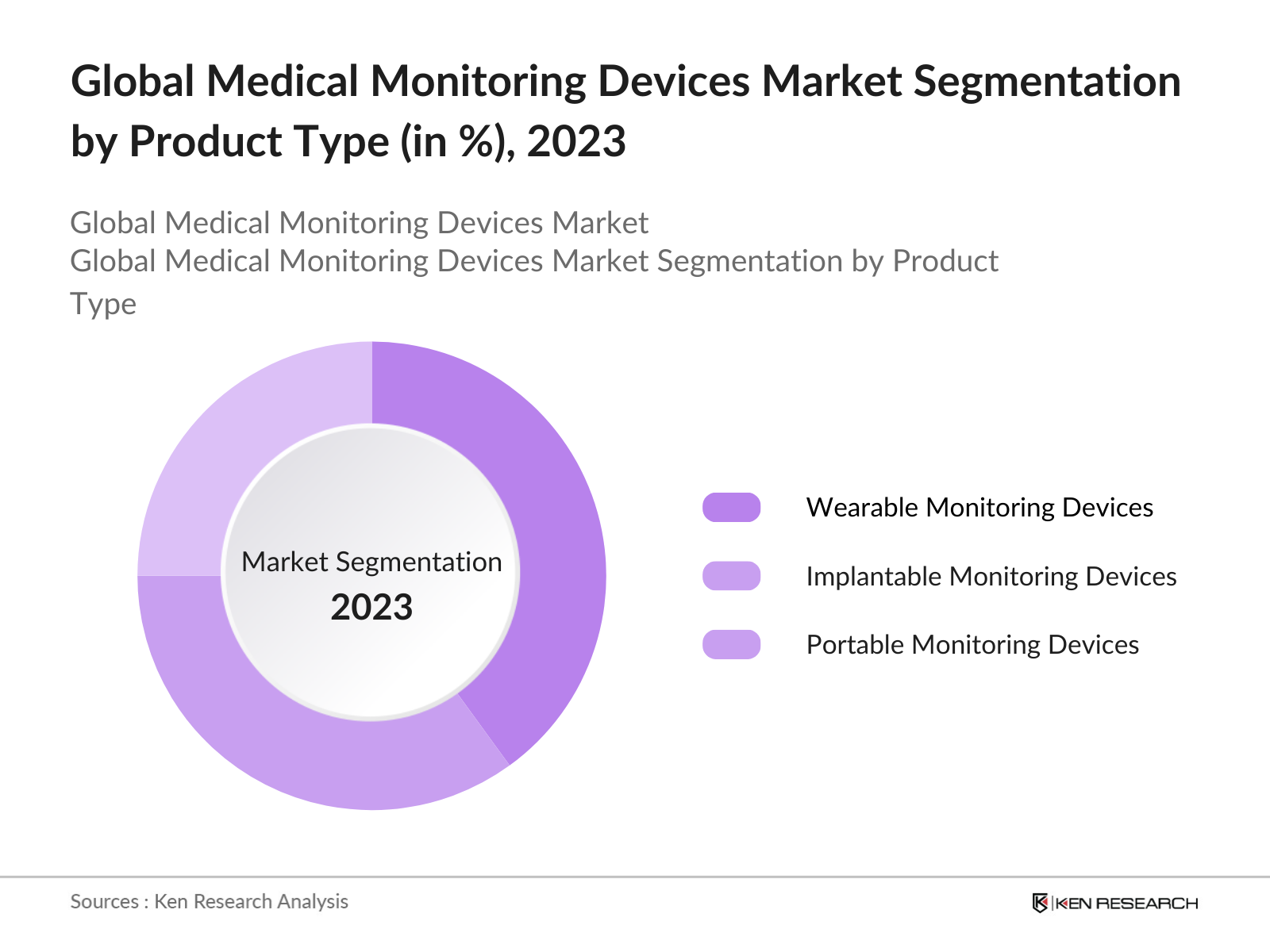

By Product Type: The global medical monitoring devices market is segmented by product type into wearable monitoring devices, implantable monitoring devices, and portable monitoring devices. In 2023, wearable devices such as continuous glucose monitors and fitness trackers captured a significant market share due to their ease of use and growing demand for real-time health data. Companies like Fitbit and Dexcom dominate this segment, driven by advancements in sensor technologies and the increasing adoption of telehealth.

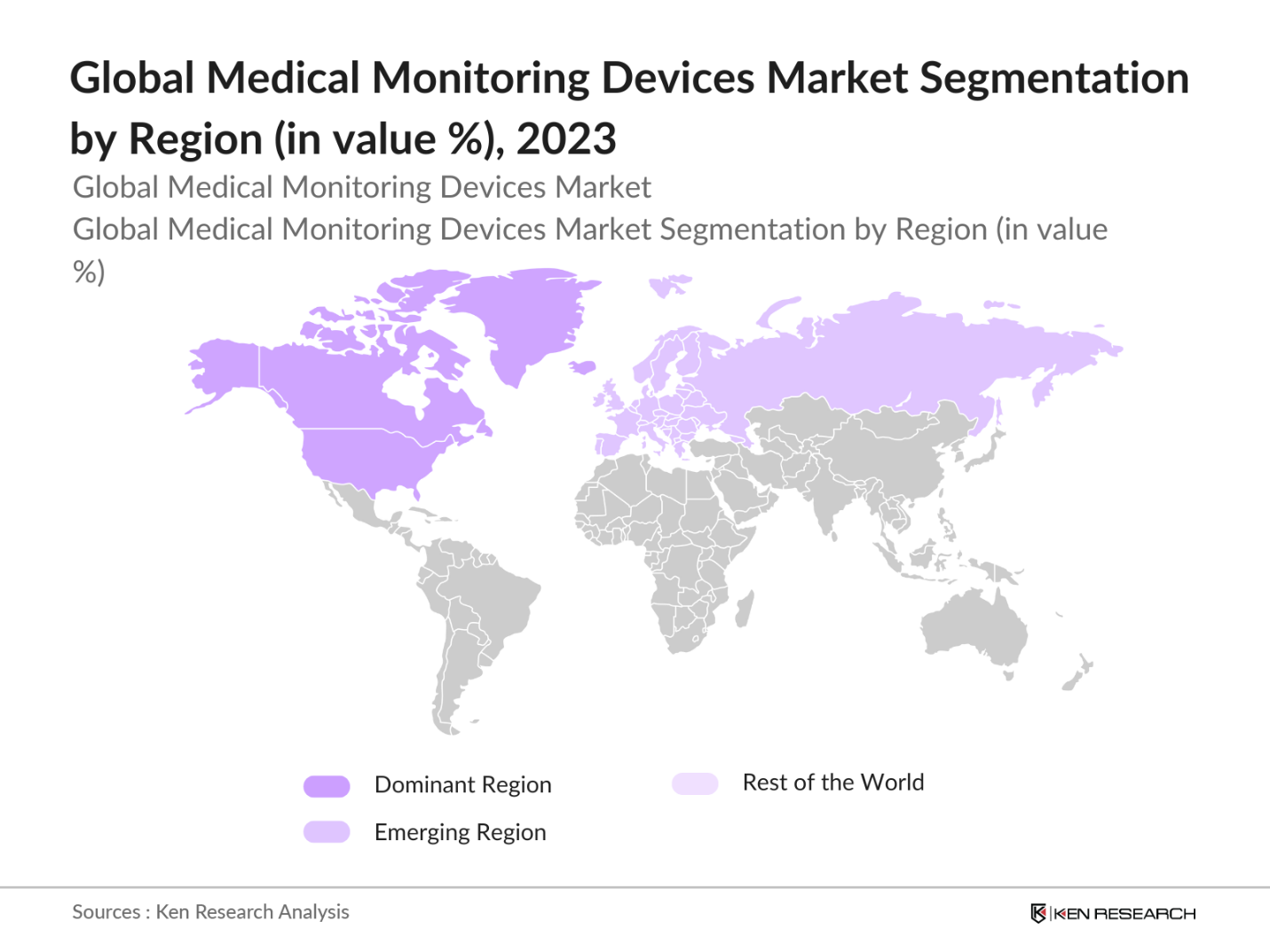

By Region: The global medical monitoring devices market is segmented regionally into North America, Europe, Asia-Pacific (APAC), Latin America, and the Middle East & Africa (MEA). In 2023, North America dominated the market due to its well-established healthcare infrastructure, high adoption of advanced technologies, and strong government support for digital health initiatives. The presence of major market players and a growing aging population further reinforce the regions leading position.

By End-User: The medical monitoring devices market is segmented by end-users into hospitals, home care settings, and ambulatory surgical centers (ASCs). In 2023, home care settings emerged as a dominant end-user, accounting for a major share of the market. This shift is driven by the increasing preference for remote monitoring technologies that reduce the need for hospital visits and offer real-time health tracking from home. The widespread adoption of wearable health devices and the growing focus on patient convenience have significantly contributed to this trend.

|

Company |

Year of Establishment |

Headquarters |

|

Medtronic PLC |

1949 |

Dublin, Ireland |

|

GE Healthcare |

1994 |

Chicago, USA |

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

|

Abbott Laboratories |

1888 |

Illinois, USA |

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

By 2028, the global medical monitoring devices market is poised for significant advancements driven by emerging technologies and evolving healthcare needs. The expanded use of biosensors for real-time health tracking, the transformative impact of 5G connectivity on remote monitoring, and increased focus on regulatory compliance will shape the market's growth trajectory.

|

By Product Type |

Wearable Monitoring Devices Implantable Monitoring Devices Portable Monitoring Devices |

|

By End-User |

Hospitals Home Care Settings Ambulatory Surgical Centers |

|

By Region |

North America Europe Asia-Pacific (APAC) Latin America Middle East & Africa (MEA) |

|

By Technology Type |

Wireless Monitoring Devices Bluetooth-Enabled Devices Standalone Devices |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

1.5. Key Market Developments

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Prevalence of Chronic Diseases

3.1.2. Increased Adoption of Remote Monitoring Technologies

3.1.3. Technological Advancements in Medical Devices

3.2. Challenges

3.2.1. High Cost of Advanced Devices

3.2.2. Regulatory Hurdles

3.3. Opportunities

3.3.1. Expansion of Telehealth Services

3.3.2. Growing Demand for Wearable Devices

3.3.3. Development of AI-Integrated Monitoring Solutions

3.4. Recent Trends

3.4.1. Rise in AI-Driven Monitoring Solutions

3.4.2. Growth of Wearable Health Technology

3.4.3. Increased Use of Remote Patient Monitoring

3.5. Government Initiatives

3.5.1. US FDA's Digital Health Innovation Action Plan

3.5.2. European Union's Digital Health Strategy

3.5.3. Health Canadas Support for Digital Health Technologies

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.1. By Product Type (in Value %)

4.1.1. Wearable Monitoring Devices

4.1.2. Implantable Monitoring Devices

4.1.3. Portable Monitoring Devices

4.2. By End-User (in Value %)

4.2.1. Hospitals

4.2.2. Home Care Settings

4.2.3. Ambulatory Surgical Centers

4.3. By Technology Type (in Value %)

4.3.1. Wireless Monitoring Devices

4.3.2. Bluetooth-Enabled Devices

4.3.3. Standalone Devices

4.4. By Region (in Value %)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia-Pacific (APAC)

4.4.4. Latin America

4.4.5. Middle East & Africa (MEA)

4.5. By Application (in Value %)

4.5.1. Cardiovascular Monitoring

4.5.2. Diabetes Management

4.5.3. Respiratory Monitoring

4.6. By Device Type (in Value %)

4.6.1. Diagnostic Devices

4.6.2. Therapeutic Devices

4.6.3. Monitoring Devices

5.1. Detailed Profiles of Major Companies

5.1.1. Medtronic PLC

5.1.2. GE Healthcare

5.1.3. Philips Healthcare

5.1.4. Abbott Laboratories

5.1.5. Siemens Healthineers

5.1.6. Dexcom Inc.

5.1.7. Johnson & Johnson

5.1.8. Boston Scientific

5.1.9. Nihon Kohden

5.1.10. Masimo Corporation

5.1.11. ResMed

5.1.12. Omron Healthcare

5.1.13. Roche Diagnostics

5.1.14. Hill-Rom Holdings, Inc.

5.1.15. Becton, Dickinson and Company (BD)

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Region (in Value %)

9.2. By Product Type (in Value %)

9.3. By Technology Type (in Value %)

9.4. By End-User (in Value %)

9.5. By Application (in Value %)

9.6. By Device Type (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on the Global Medical Monitoring Devices Market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Global Medical Monitoring Devices Market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple Medical Monitoring Devices and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from Medical Monitoring Devices.

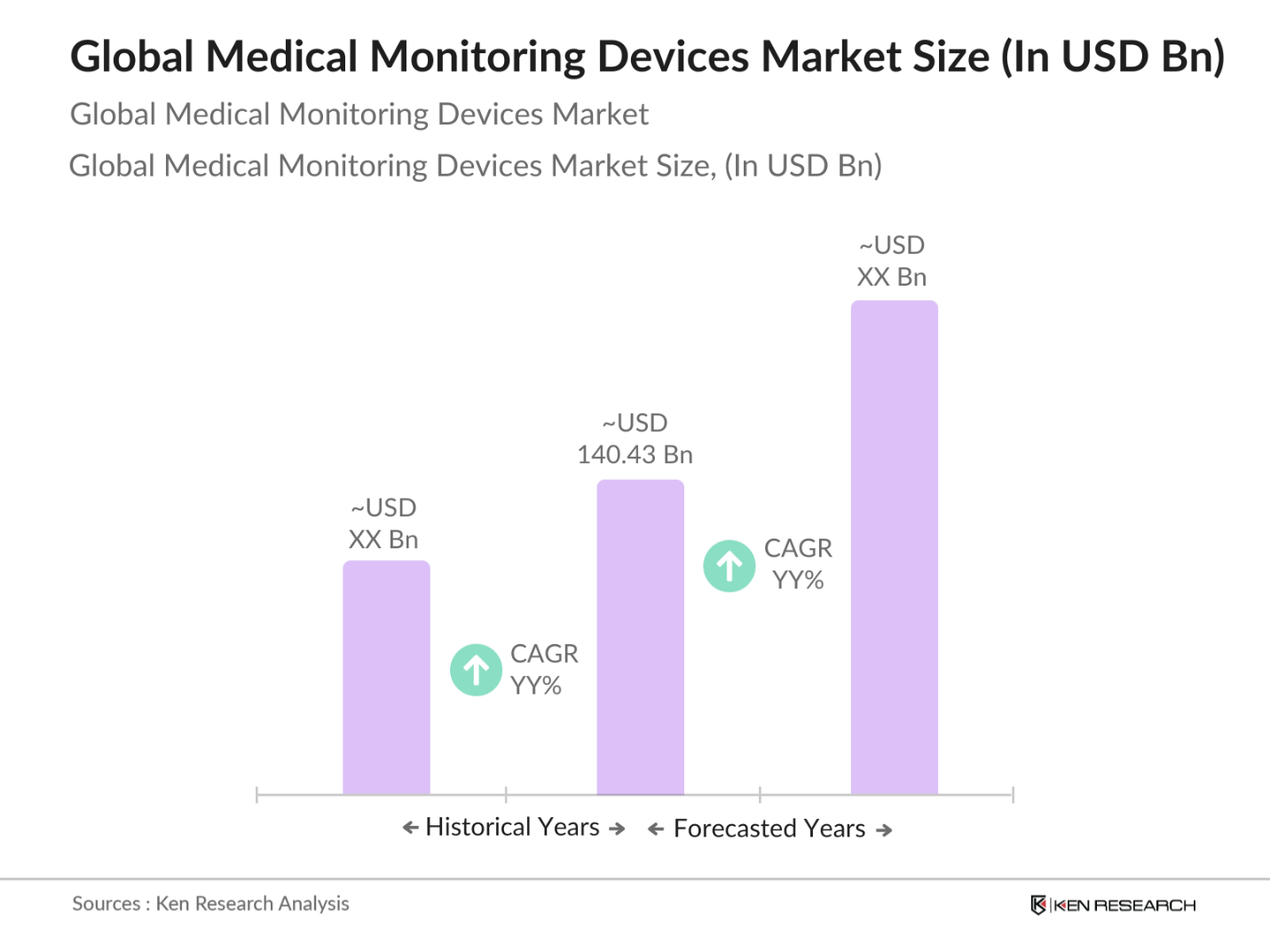

The global medical monitoring devices market was valued at USD 140.43 billion in 2023. It is driven by the increasing prevalence of chronic diseases, rising demand for remote health monitoring, and growing adoption of wearable technology in healthcare.

Challenges include high costs of advanced devices, regulatory hurdles in different regions, and concerns over data privacy and security. Additionally, long approval times for new devices under stringent regulations affect market entry and expansion.

Key players in the market include Medtronic, Philips Healthcare, GE Healthcare, Abbott Laboratories, and Siemens Healthineers. These companies dominate the market due to their innovative product offerings and global distribution networks.

The market is propelled by the rising prevalence of chronic diseases, aging populations worldwide, and increasing government support for healthcare digitization. The shift towards remote patient monitoring is also a key growth driver.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.