Global Military Aircraft Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD7312

Region:Global

Author(s):Mukul

Product Code:KROD7312

November 2024

89

The global military aircraft market is dominated by a few major players who drive innovation and set industry standards. Companies like Lockheed Martin and Boeing maintain their market leadership due to their long-standing relationships with governments and their cutting-edge aircraft technologies. Other key players, such as Airbus and Northrop Grumman, focus on the development of multirole and specialized aircraft that cater to the evolving needs of global defense forces. The presence of these players highlights the competitive nature of the market, with continuous advancements and heavy investments in R&D.

|

Company |

Established |

Headquarters |

Number of Employees |

Revenue (USD Bn) |

Notable Products |

Recent Contracts |

Global Presence |

R&D Expenditure |

|

Lockheed Martin Corporation |

1912 |

Bethesda, Maryland, USA |

||||||

|

Boeing |

1916 |

Chicago, Illinois, USA |

||||||

|

Airbus SE |

1970 |

Leiden, Netherlands |

||||||

|

Northrop Grumman Corporation |

1939 |

Falls Church, Virginia |

||||||

|

Saab AB |

1937 |

Stockholm, Sweden |

Over the next five years, the global military aircraft market is expected to grow significantly due to continuous technological advancements, defense modernization efforts, and increasing defense budgets in emerging economies. Countries are seeking to replace aging aircraft fleets with more advanced, versatile, and cost-efficient alternatives. With the rise of geopolitical tensions, the focus on stealth technology, autonomous systems, and UAVs is likely to drive demand for new aircraft. Collaborative defense programs between allied nations, such as the Eurofighter project, are anticipated to continue shaping the market landscape.

|

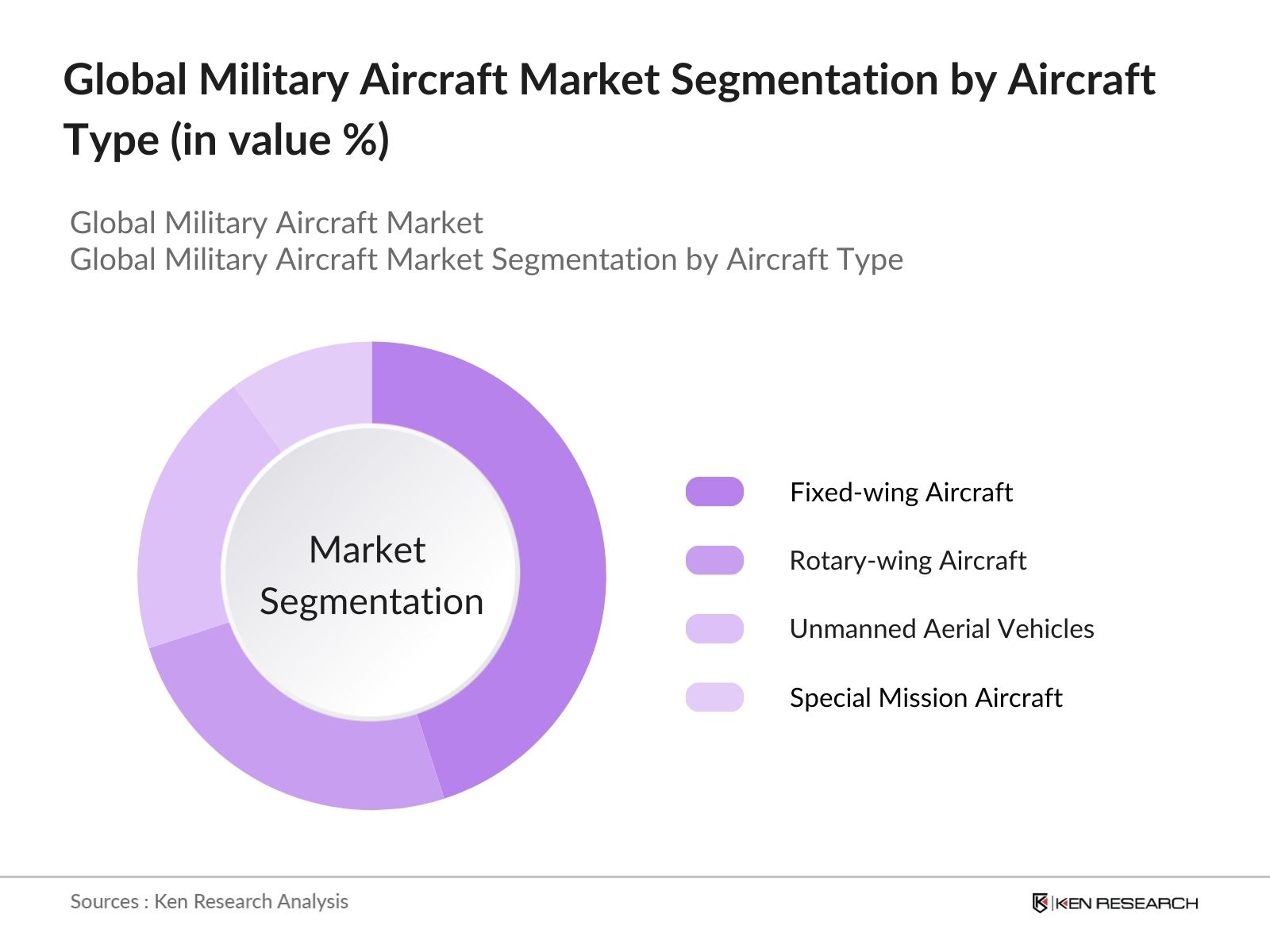

By Aircraft Type |

Fixed-wing Aircraft |

|

Rotary-wing Aircraft |

|

|

Unmanned Aerial Vehicles (UAVs) |

|

|

Special Mission Aircraft |

|

|

By Application |

Combat |

|

Transport |

|

|

Surveillance and Reconnaissance |

|

|

Training |

|

|

By Technology |

Stealth |

|

Supersonic |

|

|

Hypersonic |

|

|

Electric Propulsion |

|

|

By Platform |

Airborne Early Warning & Control |

|

Multirole Fighter |

|

|

Airlift Aircraft |

|

|

Refueling Aircraft |

|

|

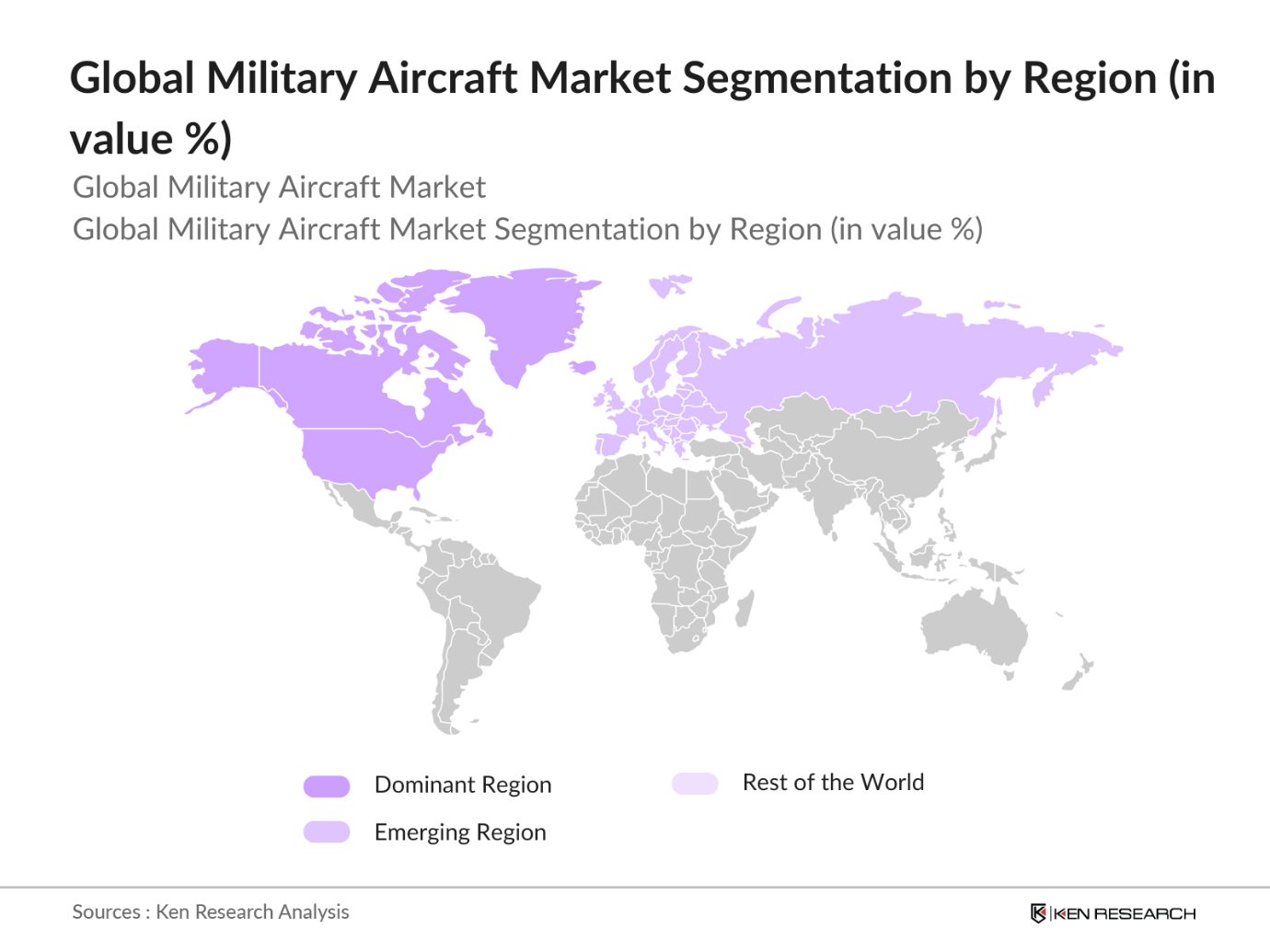

By Region |

North America |

|

Europe |

|

|

Asia Pacific |

|

|

Middle East & Africa |

|

|

Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy (By Aircraft Type, By Technology, By Application)

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Demand for Modernization, Geopolitical Tensions, Defense Budget Allocations)

3.1.1. Increasing Defense Spending (Country-specific budgets)

3.1.2. Rising Need for Technologically Advanced Aircraft (5th Gen Fighters, UAVs, etc.)

3.1.3. Ongoing Military Operations (Global and Regional)

3.2. Market Challenges (High Development Costs, Supply Chain Disruptions, Regulatory Hurdles)

3.2.1. Stringent International Regulations (ITAR, Export Control)

3.2.2. Long Production Cycles

3.2.3. Dependency on Specialized Materials

3.3. Opportunities (Emerging Markets, Collaborative Programs, UAV Integration)

3.3.1. Growth of UAVs in Defense Applications

3.3.2. Modernization in Developing Nations

3.3.3. Opportunities for Collaborations (Joint Ventures, International Defense Partnerships)

3.4. Trends (Stealth Technologies, AI Integration, Modular Aircraft Designs)

3.4.1. Stealth and Low-Observable Technologies

3.4.2. AI and Autonomous Aircraft Developments

3.4.3. Use of Additive Manufacturing (3D Printing)

3.5. Government Regulations (Defense Procurement Policies, Export Controls, Safety Certifications)

3.5.1. ITAR and Other Export Regulations

3.5.2. Defense Offsets Programs

3.5.3. Military Aircraft Certification Processes

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Defense Ministries, Global Contractors)

3.8. Porters Five Forces (Supplier Bargaining Power, Buyer Influence, Competitive Rivalry)

3.9. Competition Ecosystem (OEMs, Subcontractors, System Integrators)

4.1. By Aircraft Type (In Value %)

4.1.1. Fixed-wing Aircraft

4.1.2. Rotary-wing Aircraft

4.1.3. Unmanned Aerial Vehicles (UAVs)

4.1.4. Special Mission Aircraft

4.2. By Application (In Value %)

4.2.1. Combat

4.2.2. Transport

4.2.3. Surveillance and Reconnaissance

4.2.4. Training

4.3. By Technology (In Value %)

4.3.1. Stealth

4.3.2. Supersonic

4.3.3. Hypersonic

4.3.4. Electric Propulsion

4.4. By Platform (In Value %)

4.4.1. Airborne Early Warning & Control

4.4.2. Multirole Fighter

4.4.3. Airlift Aircraft

4.4.4. Refueling Aircraft

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. Lockheed Martin Corporation

5.1.2. The Boeing Company

5.1.3. Airbus SE

5.1.4. Northrop Grumman Corporation

5.1.5. BAE Systems

5.1.6. Saab AB

5.1.7. Dassault Aviation

5.1.8. Leonardo S.p.A

5.1.9. United Aircraft Corporation (UAC)

5.1.10. General Dynamics Corporation

5.1.11. Embraer Defense & Security

5.1.12. Textron Aviation

5.1.13. HAL (Hindustan Aeronautics Limited)

5.1.14. Bombardier Defense

5.1.15. Thales Group

5.2. Cross Comparison Parameters (Revenue, Number of Aircraft Delivered, Contract Wins, Technological Advancements, Defense Partnerships, Regional Market Share, Workforce Size, R&D Spending)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Collaborations, Military Programs)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Contracts & Grants

5.8. Defense Budget Allocations

5.9. Private Equity and Venture Capital Investments

6.1. Military Procurement Policies

6.2. Export Control Laws

6.3. Safety and Airworthiness Standards

6.4. Defense Offset Policies

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8.1. By Aircraft Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Platform (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Product Differentiation Strategies

9.4. White Space Opportunity Analysis

The first phase involved mapping the military aircraft market ecosystem, identifying key stakeholders such as manufacturers, government bodies, and contractors. Extensive secondary research was conducted using both proprietary databases and government reports to gather industry-specific data.

Historical market data on military aircraft deliveries, defense contracts, and technological advancements were compiled to assess market dynamics. Additionally, the ratio of military budget allocations to specific aircraft programs was analyzed.

To validate market assumptions, in-depth interviews were conducted with military procurement officials and executives from leading aircraft manufacturers. These insights helped in refining the market estimates and providing a more comprehensive understanding of market trends.

The final phase involved the synthesis of all data gathered from primary and secondary research to generate an accurate market analysis. The insights from aircraft manufacturers were integrated to ensure the robustness of the findings.

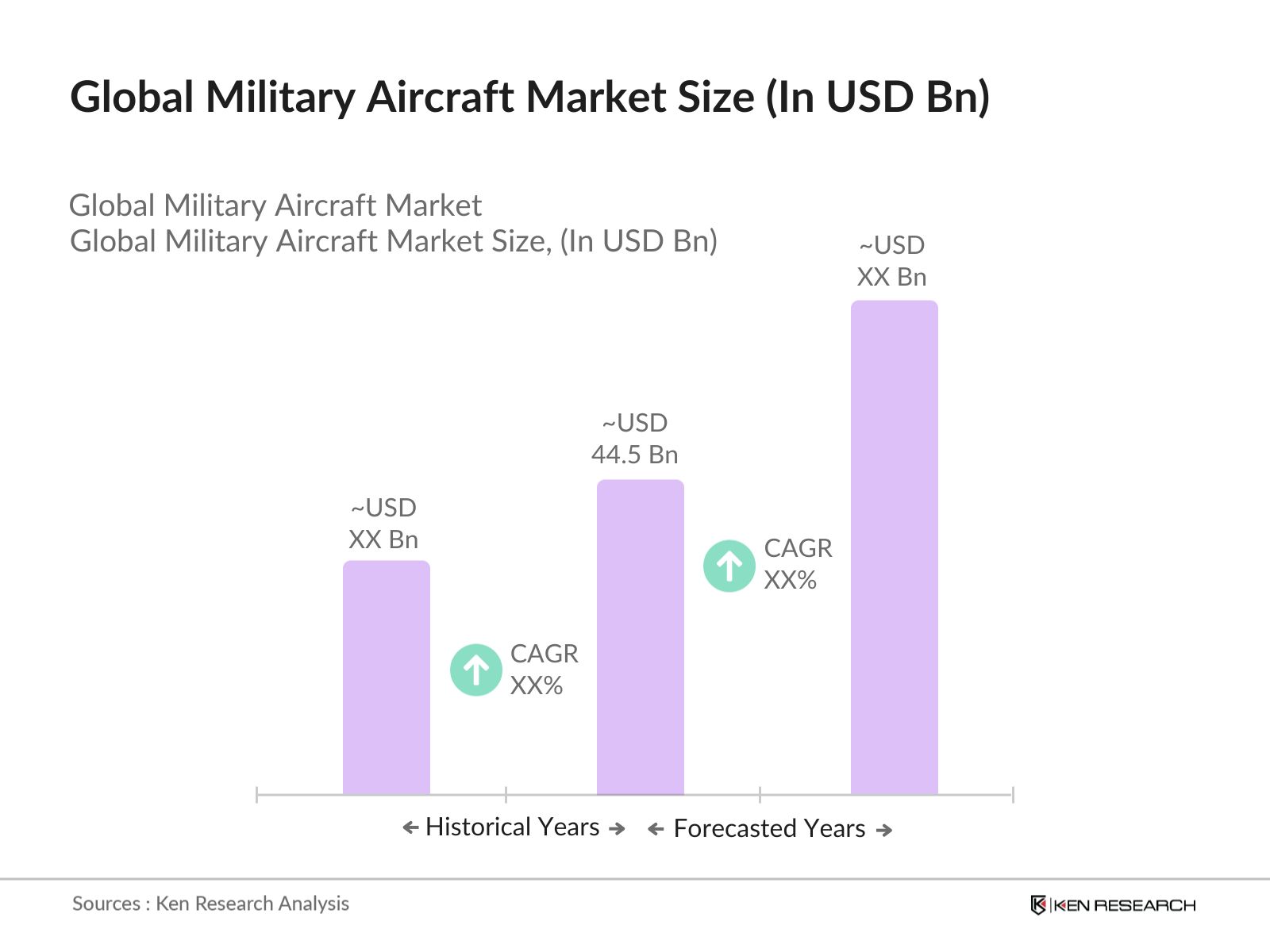

The global military aircraft market is valued at USD 44.5 billion and is driven by rising defense budgets and the need for technologically advanced aircraft.

Challenges include high development costs, stringent regulatory frameworks, and the long production cycles associated with military aircraft.

Key players include Lockheed Martin, Boeing, Airbus SE, Northrop Grumman, and Saab, which dominate the market due to their advanced technologies and strong relationships with defense agencies.

The market is driven by the need for fleet modernization, increasing defense budgets, and advancements in stealth and autonomous technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.