Global Mobile Satellite Services Market Outlook to 2030

Region:Global

Author(s):Shivani

Product Code:KROD5247

October 2024

83

About the Report

Global Mobile Satellite Services Market Overview

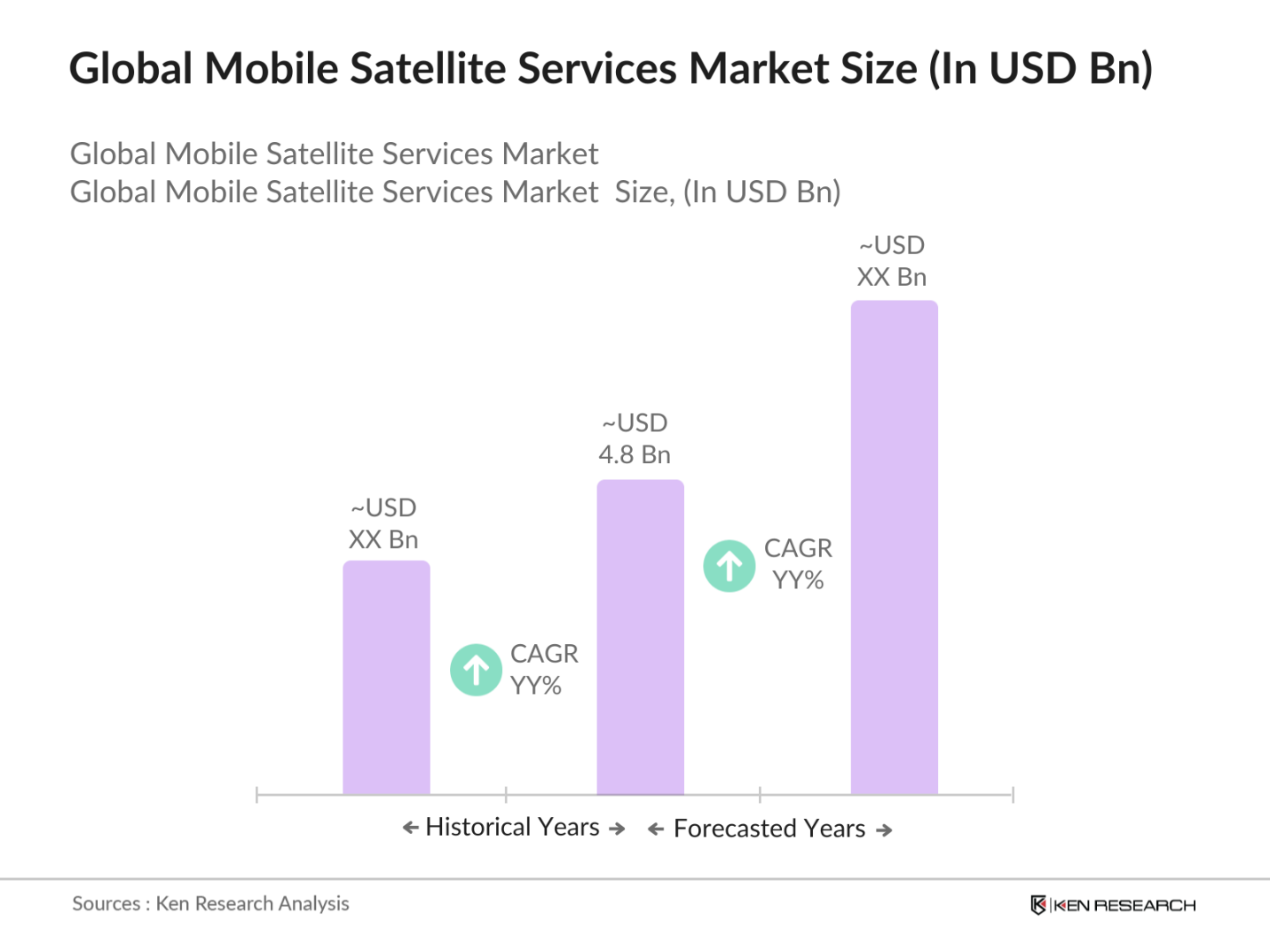

- The Global Mobile Satellite Services (MSS) market is valued at USD 4.8 billion, based on a five-year historical analysis. The market is primarily driven by the increasing demand for reliable communication services in remote and underserved regions. Key contributors to this growth include maritime and aviation industries, government initiatives for enhanced communication infrastructure, and the rise in IoT applications requiring robust satellite connectivity.

- Countries like the United States, China, and Japan dominate the mobile satellite services market due to their advanced technological infrastructure and the presence of leading satellite operators. The United States, in particular, benefits from significant government investments in satellite communication for defense and aerospace. Chinas dominance stems from its growing investment in space technology, along with government initiatives to enhance communication networks in rural areas. Japan plays a vital role due to its advanced innovation in satellite design and the integration of IoT systems for both commercial and defense purposes.

- The International Telecommunication Union (ITU) plays a crucial role in regulating satellite communications globally. The ITU allocates frequency bands and coordinates satellite orbits to ensure efficient use of the spectrum and avoid interference. As of 2024, over 193 countries are members of the ITU, with regulations impacting the deployment and operation of satellite services. Compliance with ITU standards is mandatory for satellite operators, who must ensure their systems do not interfere with other services.

Global Mobile Satellite Services Market Segmentation

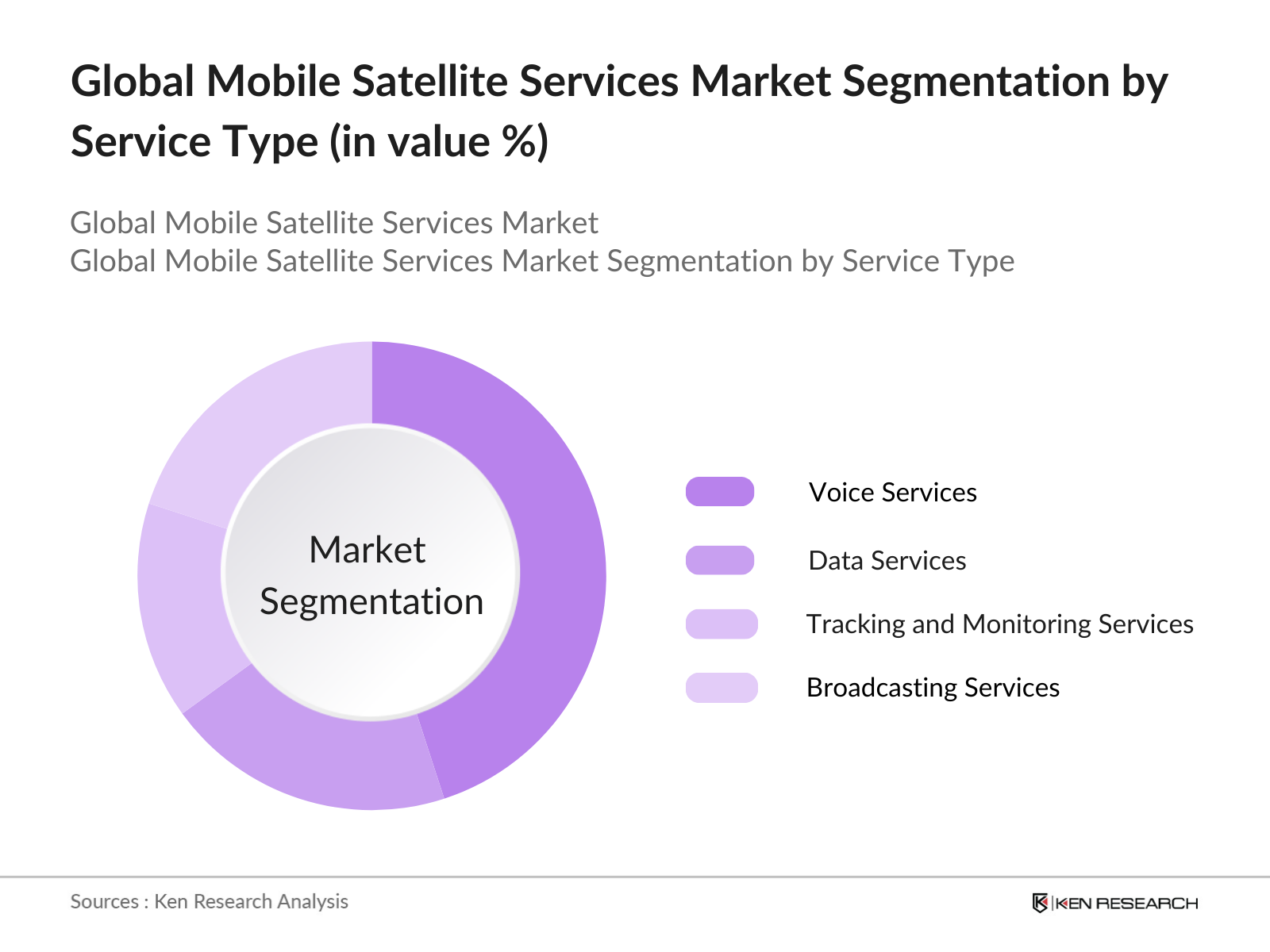

By Service Type: The Global Mobile Satellite Services market is segmented by service type into voice services, data services, tracking and monitoring services, and broadcasting services. Data services currently dominate the market share, attributed to the increasing demand for high-speed internet access in remote locations and the growing need for real-time data transmission for business, defense, and disaster management operations. The rise in the number of connected devices, along with the development of Internet of Things (IoT) ecosystems, has further solidified the position of data services within this segment.

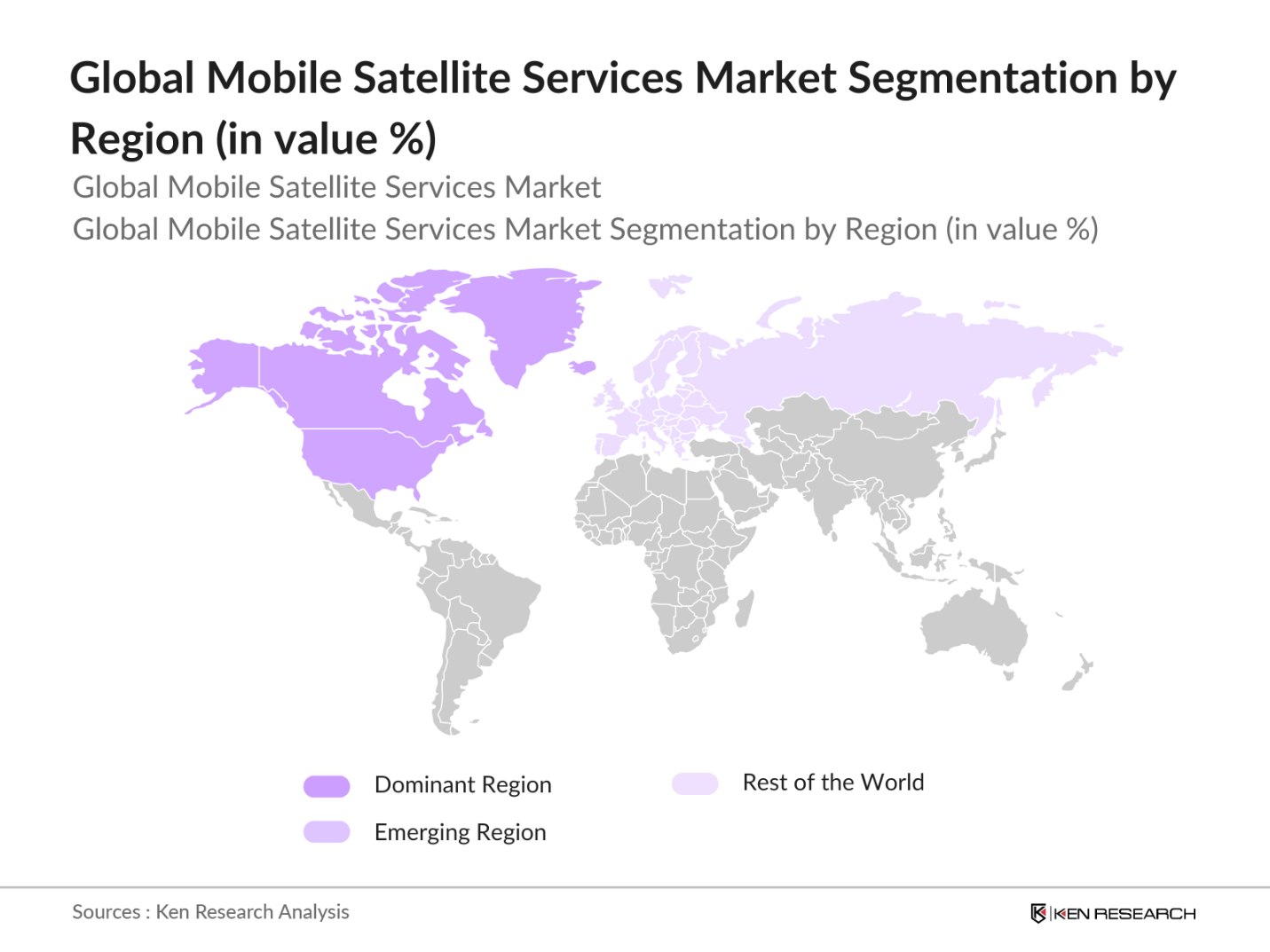

By Region: The Global Mobile Satellite Services market is segmented by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. North America leads the market due to the presence of key satellite service providers such as Inmarsat and Iridium Communications, along with substantial government investments in satellite communication for defense and public safety purposes. Europe follows closely, benefiting from advancements in satellite technology, particularly in IoT integration and environmental monitoring applications. Asia-Pacific is witnessing rapid growth, driven by rising investments in space technology and an increasing need for reliable communication services in rural and disaster-prone areas.

Global Mobile Satellite Services Market Competitive Landscape

The mobile satellite services market is dominated by key global players that account for the majority of market revenue. The competitive landscape is characterized by consolidation, with several mergers and acquisitions shaping the market. Players such as Inmarsat, Iridium Communications, and Global star lead the market due to their extensive satellite fleets and established partnerships with defense and commercial sectors. The rapid innovation in satellite technology and the expansion of satellite constellations, particularly in low-Earth orbits, have enabled these companies to expand their service offerings and increase customer base.

|

Company Name |

Establishment Year |

Headquarters |

Fleet Size |

Revenue (2023) |

Partnerships |

Technology Innovations |

Market Share (2023) |

Services Offered |

Regulatory Compliance |

|

Inmarsat PLC |

1979 |

London, UK |

|||||||

|

Iridium Communications Inc. |

2000 |

McLean, VA, USA |

|||||||

|

Globalstar Inc. |

1991 |

Covington, LA, USA |

|||||||

|

Thuraya Telecommunications |

1997 |

Abu Dhabi, UAE |

|||||||

|

Viasat Inc. |

1986 |

Carlsbad, CA, USA |

Global Mobile Satellite Services Market Analysis

Market Growth Drives

- Increasing Demand for IoT Connectivity: The rising number of connected IoT devices globally is driving the growth of mobile satellite services. By 2024, it is expected that over 19 billion IoT devices will be active worldwide, with applications in sectors such as agriculture, healthcare, and logistics. Mobile satellite services provide critical connectivity for these devices, especially in areas where terrestrial networks are unavailable. For instance, in agriculture, satellites are crucial for tracking and managing resources in remote fields. Governments in emerging markets are also adopting IoT in smart city projects, increasing the demand for satellite IoT connectivity.

- Expansion of Defense and Aerospace Applications: The defense and aerospace sectors continue to invest heavily in satellite services for secure communication, navigation, and reconnaissance. By 2023, global military spending surpassed $2.1 trillion, with a significant portion allocated to satellite-based surveillance and communications infrastructure. The United States Department of Defense remains the largest customer for satellite services, with ongoing investments in geospatial intelligence and defense communication satellites. Similarly, countries like India and China are expanding their space defense capabilities, driving demand for advanced satellite services.

- Government Initiatives in Remote Connectivity: Governments are increasingly prioritizing remote area connectivity to bridge the digital divide. Indias BharatNet program aims to connect over 250,000 rural villages with broadband, a portion of which relies on satellite links. Similarly, in Africa, initiatives such as the African Union's Digital Transformation Strategy aim to improve internet access in rural regions through satellite-based solutions. As of 2024, over 3.7 billion people globally still lack internet access, with satellite services positioned to fill this gap, supported by government-backed programs.

Market Challenges

- High Costs of Satellite Launch and Maintenance: Launching and maintaining satellites remains a significant challenge due to the high capital investment required. The cost of launching a satellite into orbit can range from $10 million to $400 million, depending on the payload and orbit. Maintenance costs are also substantial, with operators spending millions annually on repairs, updates, and operational logistics. This financial barrier limits the ability of smaller operators to enter the market and hinders innovation in satellite technology, despite growing demand for services.

- Regulatory Hurdles (Frequency Spectrum Allocation): Regulatory hurdles related to spectrum allocation remain a challenge for mobile satellite services. The International Telecommunication Union (ITU) manages global spectrum allocation, but each country enforces its own rules, creating a fragmented regulatory environment. For instance, in 2023, countries like India and Brazil introduced stricter frequency allocation regulations, affecting the deployment of satellite services. Moreover, delays in regulatory approvals for new spectrum bands can limit the availability of services, slowing down market growth in various regions.

Global Mobile Satellite Services Market Future Outlook

Over the next five years, the Global Mobile Satellite Services market is expected to witness significant growth driven by the expansion of satellite constellations, advancements in LEO satellite technology, and growing demand for reliable communication services in underserved and remote regions. The integration of mobile satellite services with 5G networks and IoT applications will further drive market growth, enhancing data transmission capabilities and improving service quality. Governments across the globe will continue to invest in satellite infrastructure, with a focus on defense, public safety, and disaster management applications.

Market Opportunities

- Adoption of LEO Satellites for Low-Latency Applications: Low-earth orbit (LEO) satellites are increasingly being adopted for low-latency applications, particularly in real-time communication and financial transactions. As of 2024, LEO satellites have an average latency of 25-50 milliseconds, making them suitable for applications like remote surgery, stock trading, and virtual reality. Companies like SpaceX and OneWeb have launched hundreds of LEO satellites to meet the growing demand for low-latency services, particularly in sectors requiring real-time data transmission.

- Increase in Satellite Constellations: The number of satellite constellations in orbit is rapidly increasing. By 2024, over 7,500 active satellites are expected to be in operation, with a significant proportion belonging to large constellations. These constellations are primarily composed of LEO satellites and are being used to provide global broadband coverage, particularly in rural and remote areas. Governments and private companies alike are investing heavily in satellite constellations to expand their connectivity offerings and meet the growing demand for high-speed internet access.

Scope of the Report

|

By Service Type |

Voice Services Data Services Tracking and Monitoring Services Broadcasting Services |

|

By End-User |

Maritime Aviation Defense & Security Government Enterprise |

|

By Orbit Type |

Geostationary Orbit (GEO) Low Earth Orbit (LEO) Medium Earth Orbit (MEO) |

|

By Frequency Band |

L-Band S-Band C-Band Ku-Band |

|

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

Products

Key Target Audience

Satellite Operators

Telecommunications Providers

Maritime & Aviation Companies

Defense Contractors

Government and Regulatory Bodies (e.g., ITU, FCC)

IoT Solution Providers

Investments and Venture Capitalist Firms

Public Safety and Disaster Management Agencies

Companies

Major Players

Inmarsat PLC

Iridium Communications Inc.

Globalstar Inc.

Thuraya Telecommunications Company

Viasat Inc.

EchoStar Corporation

ORBCOMM Inc.

Intelsat S.A.

SES S.A.

Skylo Technologies

Table of Contents

1. Global Mobile Satellite Services Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Industry Metrics (Spectrum Allocation, Satellite Types, Regulatory Bodies)

1.4. Market Segmentation Overview

2. Global Mobile Satellite Services Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Service Providers, Revenue by Satellite Type)

2.3. Key Market Developments and Milestones

3. Global Mobile Satellite Services Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for IoT Connectivity

3.1.2. Expansion of Defense and Aerospace Applications

3.1.3. Government Initiatives in Remote Connectivity

3.1.4. Emergence of 5G and Hybrid Networks

3.2. Market Challenges

3.2.1. High Costs of Satellite Launch and Maintenance

3.2.2. Regulatory Hurdles (Frequency Spectrum Allocation)

3.2.3. Latency and Bandwidth Constraints

3.3. Opportunities

3.3.1. Partnerships with Telecom Operators

3.3.2. Development of Low-Earth Orbit (LEO) Satellites

3.3.3. Commercial Expansion into Remote Areas

3.4. Trends

3.4.1. Adoption of LEO Satellites for Low-Latency Applications

3.4.2. Increase in Satellite Constellations

3.4.3. Integration with AI and Edge Computing

3.5. Government Regulation

3.5.1. International Telecommunication Union (ITU) Standards

3.5.2. Regional Frequency Licensing Rules

3.5.3. Spectrum Allocation Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Service Providers, Equipment Manufacturers, Regulatory Bodies)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Competition Intensity)

3.9. Competition Ecosystem (Global and Regional Competitors)

4. Global Mobile Satellite Services Market Segmentation

4.1. By Service Type (In Value %)

4.1.1. Voice Services

4.1.2. Data Services

4.1.3. Tracking and Monitoring Services

4.1.4. Broadcasting Services

4.2. By End-User (In Value %)

4.2.1. Maritime

4.2.2. Aviation

4.2.3. Defense & Security

4.2.4. Government

4.2.5. Enterprise

4.3. By Orbit Type (In Value %)

4.3.1. Geostationary Orbit (GEO)

4.3.2. Low Earth Orbit (LEO)

4.3.3. Medium Earth Orbit (MEO)

4.4. By Frequency Band (In Value %)

4.4.1. L-Band

4.4.2. S-Band

4.4.3. C-Band

4.4.4. Ku-Band

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5. Global Mobile Satellite Services Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Inmarsat PLC

5.1.2. Iridium Communications Inc.

5.1.3. Thuraya Telecommunications Company

5.1.4. Globalstar Inc.

5.1.5. Viasat Inc.

5.1.6. EchoStar Corporation

5.1.7. ORBCOMM Inc.

5.1.8. Intelsat S.A.

5.1.9. SES S.A.

5.1.10. Skylo Technologies

5.1.11. Telesat

5.1.12. Eutelsat Communications

5.1.13. Lockheed Martin Corporation

5.1.14. L3Harris Technologies

5.1.15. SpaceX

5.2. Cross Comparison Parameters (Fleet Size, Service Coverage, Revenue, Partnerships, Innovation Index)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Contracts and Defense Deals

5.8. Private Equity Investments

5.9. Venture Capital Funding

6. Global Mobile Satellite Services Market Regulatory Framework

6.1. ITU Regulations

6.2. National and Regional Frequency Allocation Policies

6.3. Certification and Compliance Requirements

7. Global Mobile Satellite Services Future Market Size (In USD Bn)

7.1. Market Projections by Service Type

7.2. Key Growth Drivers for Future Market Expansion

8. Global Mobile Satellite Services Future Market Segmentation

8.1. By Service Type (In Value %)

8.2. By End-User (In Value %)

8.3. By Orbit Type (In Value %)

8.4. By Frequency Band (In Value %)

8.5. By Region (In Value %)

9. Global Mobile Satellite Services Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Marketing and Expansion Strategies

9.4. Future Strategic Collaborations

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step in our research methodology involves constructing a comprehensive ecosystem map of the global mobile satellite services market. This includes identifying major stakeholders, such as satellite operators, telecommunications providers, and government regulatory bodies, through extensive desk research and proprietary databases.

Step 2: Market Analysis and Construction

In this phase, historical data on market penetration and revenue generation is analyzed. The markets structure is assessed by evaluating satellite service offerings, technology integration, and regional growth. Service quality metrics are also reviewed to ensure the accuracy of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses developed from historical data are validated through consultations with industry experts from major satellite companies. These consultations offer key insights into satellite performance, customer trends, and the regulatory landscape, ensuring a well-rounded analysis.

Step 4: Research Synthesis and Final Output

The final phase of research involves engaging directly with satellite operators and service providers to collect detailed data on technology innovations, service performance, and market trends. This process validates the bottom-up approach, ensuring accuracy in the reports findings.

Frequently Asked Questions

01. How big is the Global Mobile Satellite Services Market?

The Global Mobile Satellite Services market was valued at USD 4.8 billion in 2023, driven by increasing demand for connectivity in remote regions and advancements in LEO satellite technology.

02. What are the challenges in the Global Mobile Satellite Services Market?

The primary challenges include high satellite deployment costs, spectrum allocation issues, and latency concerns, especially in remote locations where terrestrial network access is limited.

03. Who are the major players in the Global Mobile Satellite Services Market?

Key players in the market include Inmarsat, Iridium Communications, Thuraya Telecommunications, Globalstar, and Viasat, who dominate due to their strong satellite networks and global service offerings.

04. What are the growth drivers of the Global Mobile Satellite Services Market?

The market is propelled by advancements in LEO satellite technology, increasing demand for IoT services, and government investments in satellite communication infrastructure, particularly for defense and public safety.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.