Global Multi-Chip Module (MCM) Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD10536

Region:Global

Author(s):Shivani Mehra

Product Code:KROD10536

December 2024

91

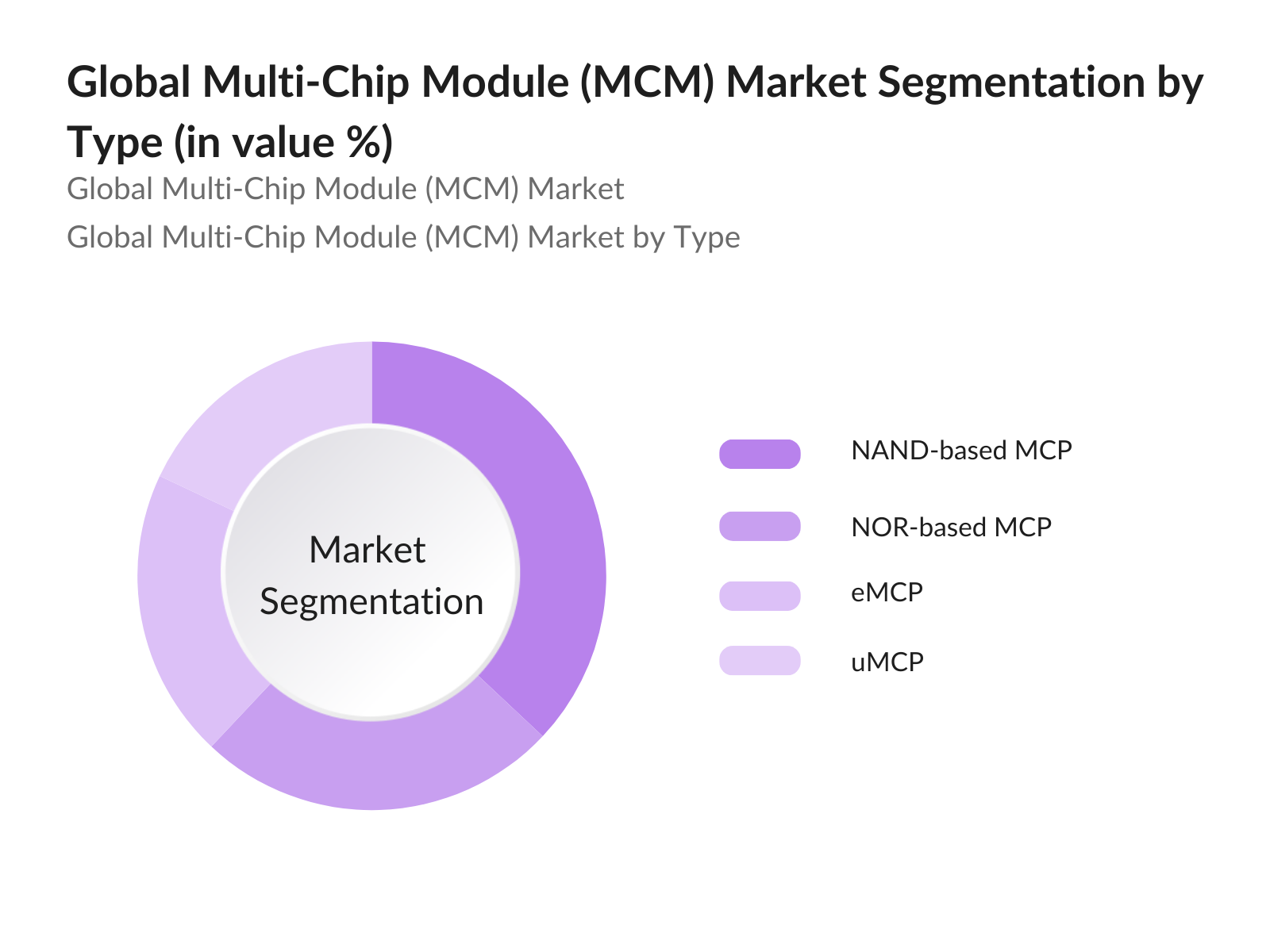

By Type: The Multi-Chip Module market is segmented by type into NAND-based MCP, NOR-based MCP, eMCP, and uMCP. In particular, NAND-based MCP modules are highly demanded for their data storage efficiency, which is crucial in smartphones, memory cards, and USB drives. The need for cost-effective, high-density storage solutions has positioned NAND-based MCPs as a dominant segment in this category.

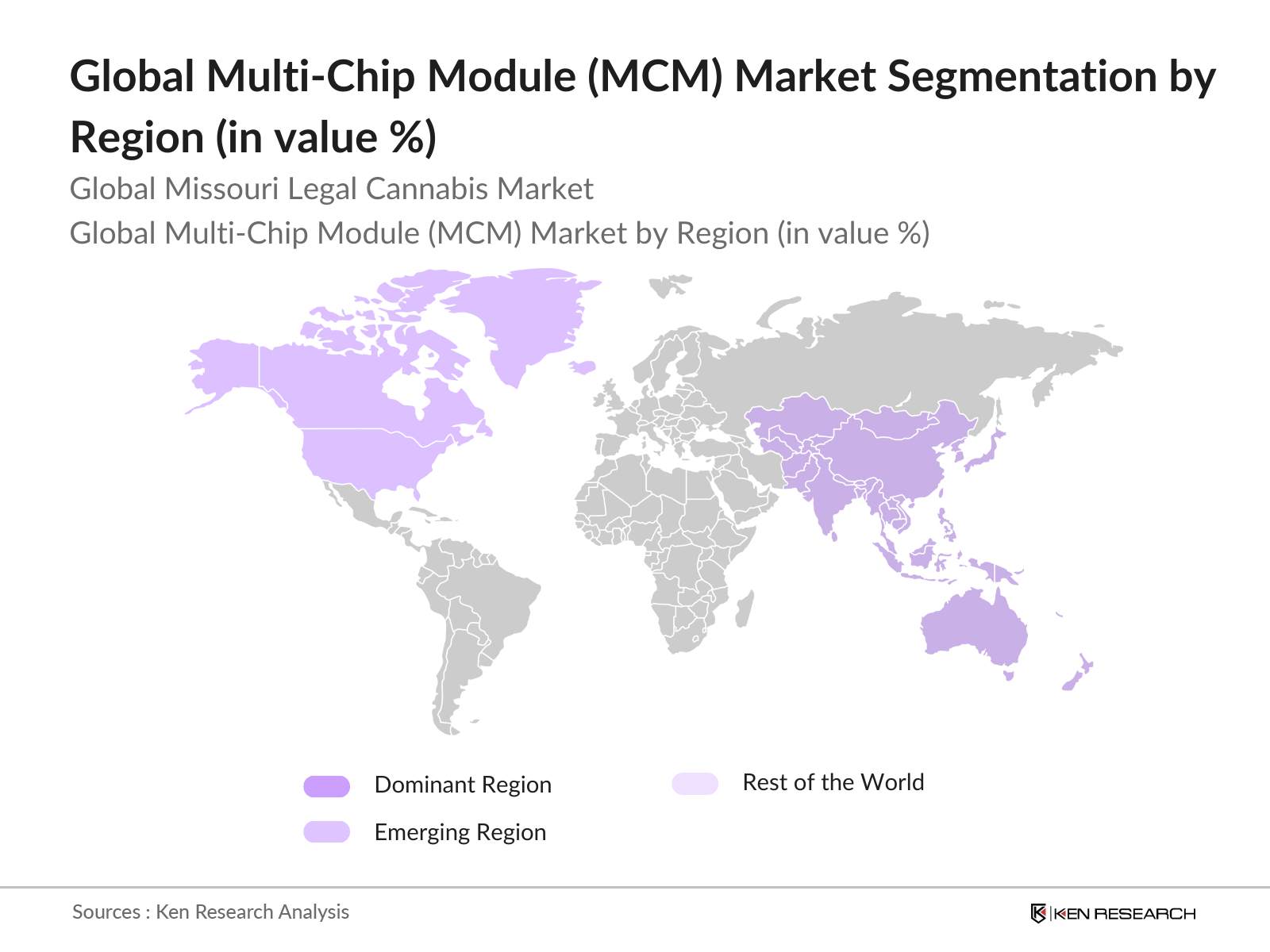

By Region: The MCM market is segmented regionally into North America, Europe, Asia-Pacific, and LAMEA. Asia-Pacific leads with the highest market share due to the presence of major semiconductor manufacturing hubs in countries such as China and Japan. High investments in R&D and manufacturing capabilities position Asia-Pacific as a growth leader in the MCM market.

The global MCM market features a consolidated landscape dominated by established corporations. Companies like Intel and Samsung lead through innovation in 3D integration and heterogeneous packaging, establishing a stronghold in critical sectors. The competitive landscape is marked by vertical integration, research alliances, and focused R&D.

|

Company |

Establishment Year |

Headquarters |

Technology Innovations |

Market Revenue (USD Mn) |

R&D Investments |

Strategic Partnerships |

Manufacturing Locations |

Product Range |

|

Intel |

1968 |

U.S. |

3D Stacking |

- |

- |

- |

- |

- |

|

Samsung Electronics |

1969 |

South Korea |

HBM memory modules |

- |

- |

- |

- |

- |

|

SK Hynix |

1983 |

South Korea |

HBM3 chip |

- |

- |

- |

- |

- |

|

Texas Instruments |

1930 |

U.S. |

Embedded designs |

- |

- |

- |

- |

- |

|

STMicroelectronics |

1987 |

Switzerland |

Power efficiency |

- |

- |

- |

- |

- |

Market Growth Drivers

Market Challenges:

Over the coming years, the Multi-Chip Module market is expected to witness substantial growth, driven by advancements in IoT, automotive applications, and high-performance computing. As industries focus on integrating smart technology, demand for compact and efficient MCMs is likely to rise. Technological advancements, such as the transition to 5G and 3D stacking, will enable companies to meet the increasing performance and density requirements.

Market Opportunities:

|

By Type |

NAND-Based MCP NOR-Based MCP eMCP uMCP |

|

By Industry Vertical |

Consumer Electronics Automotive Healthcare Aerospace & Defense Industrial |

|

By Technology |

3D Integration Fan-Out Wafer-Level Packaging (FOWLP) Embedded Passives Flip Chip |

|

By Application Areas |

Data Storage Processing Units Sensor Integration Connectivity Modules Displays |

|

By Region |

North America Europe Asia-Pacific LAMEA |

This phase involved mapping out the MCM market ecosystem, identifying stakeholders, and defining core industry variables. It included desk research using proprietary databases to gather comprehensive industry insights, enabling the identification of key market drivers.

In this stage, historical data was analyzed, focusing on industry penetration and segment growth. Data was corroborated through revenue assessments, comparing service quality and supplier data to validate accuracy.

Industry hypotheses were tested using CATI interviews with experts from leading MCM firms, providing operational insights. These consultations were vital for confirming projections and understanding market nuances.

The concluding phase involved engaging with multiple MCM manufacturers, validating product segment data, and examining consumer preferences. This final synthesis provided a robust framework for presenting an accurate, verified market analysis.

The global Multi-Chip Module market is valued at approximately USD 1.4 billion, driven by demand from consumer electronics and automotive applications.

Challenges include raw material shortages, complex manufacturing processes, and supply chain bottlenecks, impacting production timelines and scaling efforts.

Leading players include Intel, Samsung Electronics, and SK Hynix, dominating due to advanced R&D, high-performance product lines, and strategic partnerships with automotive and telecommunications sectors.

Key growth drivers include the miniaturization demand from consumer electronics and 5G technology advancements, which require compact and high-speed solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.