Global Multi-Mode Receiver Market Outlook to 2030

Region:Global

Author(s):Meenakshi Bisht

Product Code:KROD4359

December 2024

82

About the Report

Global Multi-Mode Receiver Market Overview

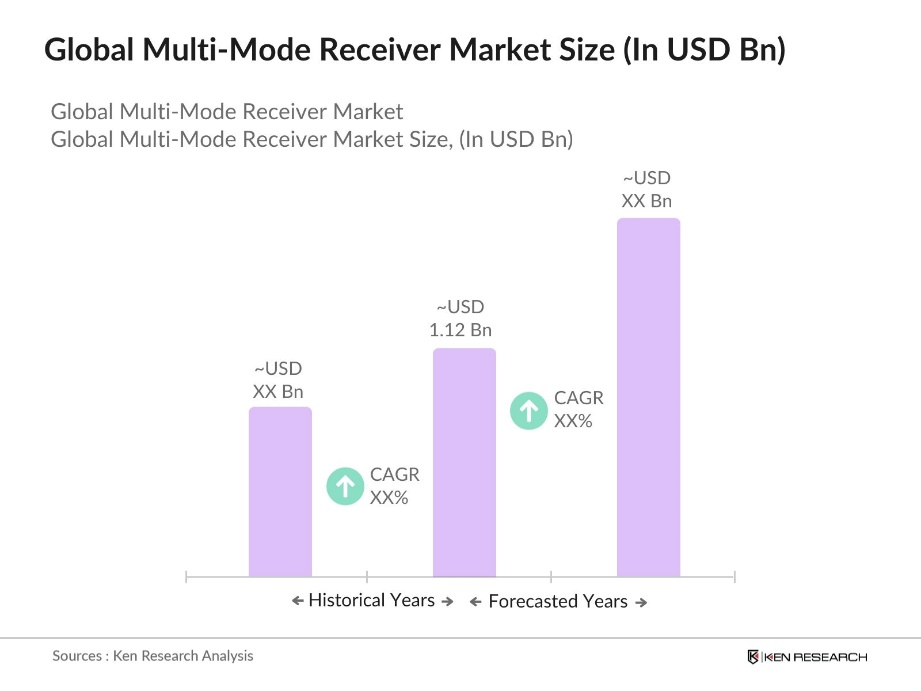

- The Global Multi-Mode Receiver Market is valued at USD 1.12 billion, driven by the increasing demand for advanced avionics systems across commercial and military aviation. This growth is propelled by modernization efforts, such as the NextGen air traffic control initiative, and mandates by international aviation bodies to enhance safety and efficiency in airspace management. The demand for multi-mode receivers is further fueled by the need for precision landing systems, increasing the adoption of GNSS (Global Navigation Satellite Systems) technology in avionics.

- Countries like the United States and Germany dominate the multi-mode receiver market due to their well-established aerospace industries and significant investments in airspace modernization programs. In the U.S., the Federal Aviation Administration's (FAA) NextGen initiative drives innovation and deployment of advanced avionics systems, while Germany benefits from its leadership in the European aviation market, with significant contributions from global aviation giants like Airbus. These nations maintain their dominance through strong governmental support and leading aerospace manufacturers.

- In 2023, the Defence Acquisition Council (DAC) approved various capital acquisition proposals amounting to approximately 2.23 lakh crore (about USD 27 billion). A significant portion of these acquisitions is aimed at enhancing the capabilities of the Indian Armed Forces, including the procurement of advanced navigation systems that utilize multi-mode receivers.

Global Multi-Mode Receiver Market Segmentation

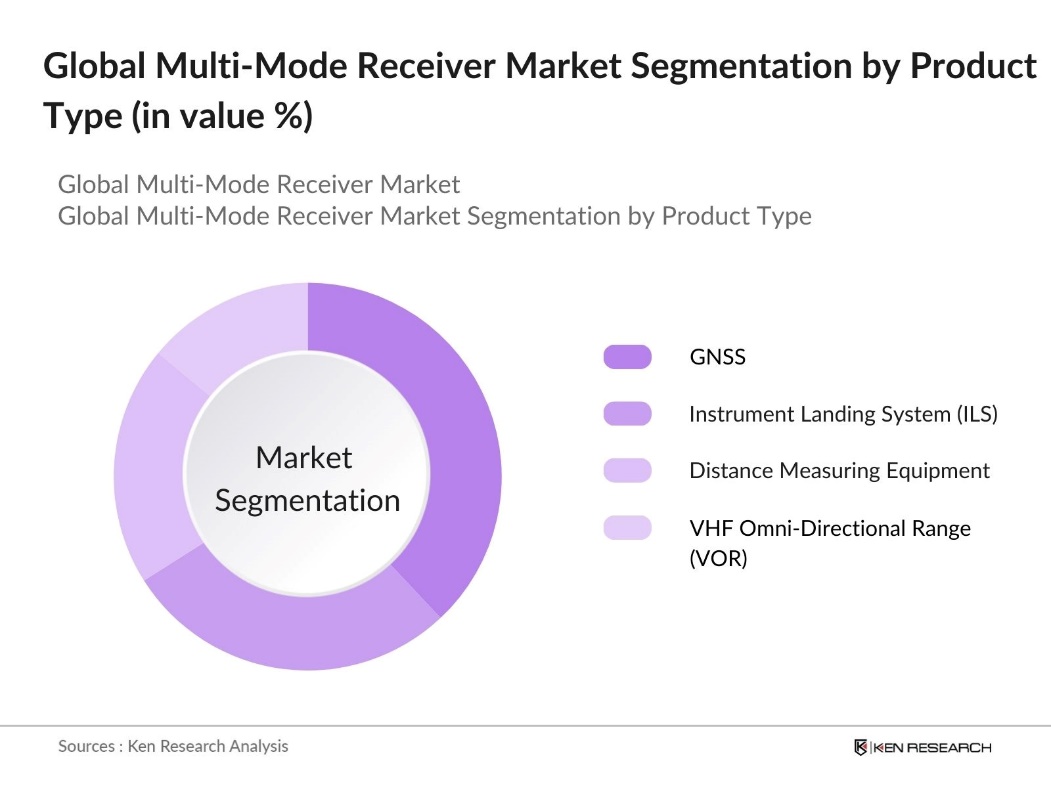

By Product Type: The global multi-mode receiver market is segmented by product type into Instrument Landing System (ILS), Global Navigation Satellite System (GNSS), Distance Measuring Equipment (DME), and VHF Omni-Directional Range (VOR). GNSS holds the largest share of the market due to its versatility in enabling precision navigation and global compatibility. Its dominance is attributed to the increasing reliance on satellite-based systems for navigation and communication in both commercial and military aircraft. GNSS technology is essential for automatic dependent surveillance-broadcast (ADS-B), driving its widespread adoption.

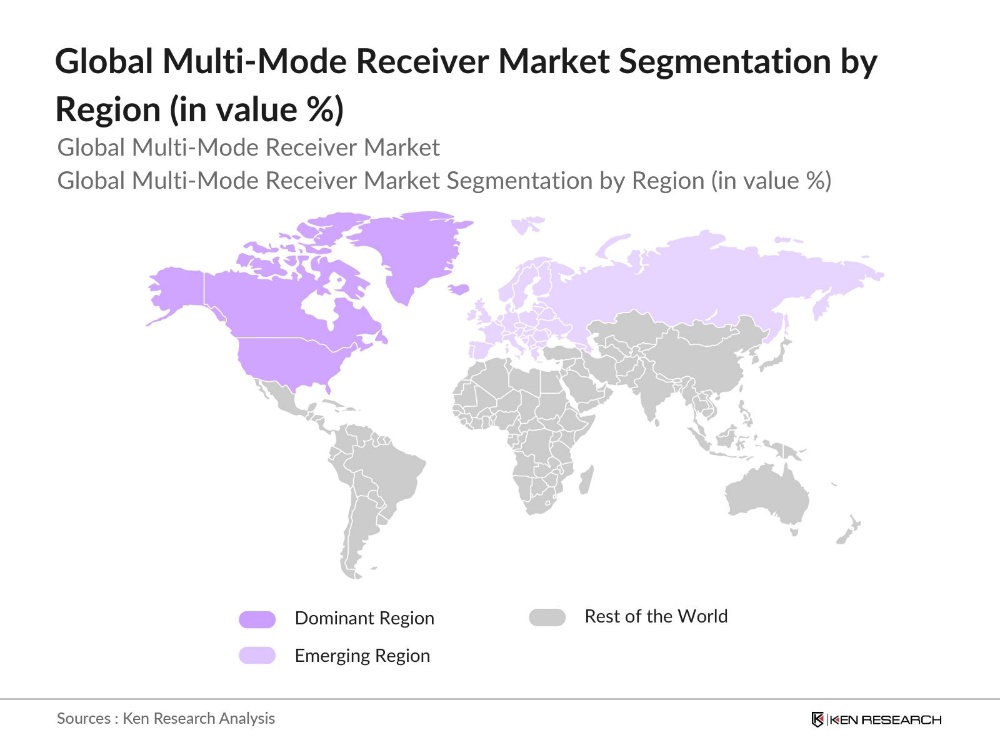

By Region: The global multi-mode receiver market is segmented by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. North America leads the market with the largest share due to the presence of leading avionics manufacturers and extensive investments in airspace modernization programs such as the FAAs NextGen initiative. Europe follows closely, with significant contributions from its strong aerospace manufacturing base and regulatory support from the European Aviation Safety Agency (EASA). Asia-Pacific is witnessing rapid growth, driven by increasing air travel demand and emerging economies investing in aviation infrastructure.

Global Multi-Mode Receiver Market Competitive Landscape

The market is characterized by a few dominant players, including Honeywell International, Thales Group, and Collins Aerospace, with these companies leveraging their technological expertise and expansive product portfolios to maintain a competitive edge. The market also sees significant contributions from regional players that specialize in specific avionics solutions. This consolidation highlights the importance of technological capabilities, partnerships, and innovation in maintaining market leadership.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

Revenue |

Product Portfolio |

Technological Capabilities |

Recent Innovations |

|

Honeywell International Inc. |

1906 |

Charlotte, USA |

|||||

|

Thales Group |

1893 |

Paris, France |

|||||

|

Collins Aerospace |

2018 |

Charlotte, USA |

|||||

|

Garmin Ltd. |

1989 |

Olathe, USA |

|||||

|

Rohde & Schwarz GmbH |

1933 |

Munich, Germany |

Global Multi-Mode Receiver Industry Analysis

Growth Drivers

- Increasing Air Traffic: The International Civil Aviation Organization (ICAO) reported an increase in military air operations across various regions. This increase in both commercial and military air traffic directly contributes to the demand for multi-mode receivers, which are essential for navigation and landing. In 2023, major aircraft manufacturers like Boeing and Airbus reported significant increases in deliveries, with Boeing delivering 528 aircraft and Airbus delivering 735 aircraft.

- Adoption of Advanced Avionics Systems: The aviation industry is rapidly adopting advanced avionics systems, including multi-mode receivers, due to evolving technology and the need for accurate navigation. The FAA is actively looking to improve communication infrastructure at airports nationwide. Its NextGen infrastructure is expected to cost nearly $35 billion through 2030. These advancements ensure enhanced precision, reliability, and safety for aircraft operations, supporting the significant role of multi-mode receivers in modern air travel.

- Expansion of Airspace Modernization Programs: Governments around the world are significantly investing in airspace modernization initiatives to improve the efficiency and safety of air travel. These programs are focused on upgrading airspace infrastructure and incorporating advanced avionics systems like multi-mode receivers. These receivers are essential for ensuring precision navigation and supporting both commercial and military aircraft operations. Modernization efforts are critical for managing growing air traffic, optimizing airspace use, and enhancing flight safety.

Market Challenges

- High Initial Costs of Avionics Equipment: The installation and certification of avionics systems, including multi-mode receivers, involve substantial costs for manufacturers and airlines. These high upfront expenses can be a significant financial burden, especially for smaller airlines and emerging market operators. The cost factor limits the broader adoption of these advanced systems, as upgrading fleets to meet regulatory standards requires considerable investment.

- Stringent Certification and Regulatory Compliance: The certification process for avionics systems, including multi-mode receivers, is complex and time-consuming, with strict regulatory requirements imposed by aviation authorities. Compliance with global aviation standards adds to the duration and cost of bringing these systems to market. This rigorous certification process can pose challenges for manufacturers, especially new entrants, as it requires navigating multiple layers of regulation across different regions.

Global Multi-Mode Receiver Market Future Outlook

Over the next few years, the global multi-mode receiver market is expected to witness robust growth, driven by technological advancements in satellite-based navigation systems and increasing demand for avionics systems that comply with regulatory mandates. The adoption of next-generation air traffic control systems and the rise in commercial air traffic are key drivers, alongside rising investments in military aviation. Furthermore, emerging markets such as India and China are likely to play a significant role in driving future market expansion, as these regions prioritize upgrading their aviation infrastructure.

Market Opportunities

- Growth in Emerging Aviation Markets: Emerging markets, particularly in regions like China, India, and Southeast Asia, are experiencing rapid growth in aviation activities. The rising demand for air travel, driven by expanding middle-class populations and government-backed aviation initiatives, is leading to a surge in air traffic. This growth creates a significant demand for advanced avionics systems, including multi-mode receivers, which are essential for navigation and landing in increasingly complex airspaces.

- Technological Integration with Satellite-Based Navigation Systems: Multi-mode receivers are being increasingly integrated with satellite-based navigation systems, such as the Global Navigation Satellite System (GNSS), to enhance the efficiency and safety of aviation operations. This integration supports advancements in communication and navigation, enabling aircraft to rely on more precise and reliable systems, particularly in areas with limited ground-based infrastructure. The growing reliance on satellite networks, combined with the capabilities of multi-mode receivers, offers significant opportunities for the aviation industry to improve flight safety, optimize landing systems, and support modern airspace management initiatives.

Scope of the Report

|

Product Type |

Instrument Landing System (ILS) Global Navigation Satellite System (GNSS) Distance Measuring Equipment (DME) VHF Omni-Directional Radio Range (VOR) Others (ADF, Marker Beacons) |

|

Application |

Commercial Aviation Military Aviation General Aviation UAV |

|

Component |

Hardware Software Services |

|

Platform |

Fixed-Wing Aircraft Rotary-Wing Aircraft Unmanned Aerial Vehicles |

|

Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

Products

Key Target Audience

Aircraft Manufacturing Companies

Private Aviation Companies

Airlines Industry

Banks and Financial Institutions

Government and Regulatory Bodies (FAA, EASA)

Investment and Venture Capitalist Firms

Companies

Players Mentioned in the Roport

Honeywell International Inc.

Thales Group

Collins Aerospace

Garmin Ltd.

Rohde & Schwarz GmbH

BAE Systems

Indra Sistemas S.A.

Leonardo S.p.A.

Raytheon Technologies

General Dynamics Corporation

Northrop Grumman Corporation

Saab AB

Safran Electronics & Defense

Elbit Systems Ltd.

Curtiss-Wright Corporation

Table of Contents

1. Global Multi-Mode Receiver Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Multi-Mode Receiver Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Multi-Mode Receiver Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Air Traffic (Commercial and Military)

3.1.2. Adoption of Advanced Avionics Systems

3.1.3. Expansion of Airspace Modernization Programs

3.1.4. Regulatory Mandates for Multi-Mode Receivers

3.2. Market Challenges

3.2.1. High Initial Costs of Avionics Equipment

3.2.2. Stringent Certification and Regulatory Compliance

3.2.3. Limited Skilled Workforce for Avionics Maintenance

3.3. Opportunities

3.3.1. Growth in Emerging Aviation Markets

3.3.2. Technological Integration with Satellite-Based Navigation Systems

3.3.3. Rising Demand for Enhanced Safety and Precision Landing Systems

3.4. Trends

3.4.1. Increasing Adoption of Software-Defined Radios

3.4.2. Integration of Multi-Mode Receivers with UAVs

3.4.3. Shift towards 5G Connectivity in Aviation

3.5. Government Regulations

3.5.1. ICAO Standards and Recommendations

3.5.2. European Aviation Safety Agency (EASA) Directives

3.5.3. Federal Aviation Administration (FAA) Policies

3.5.4. NextGen Airspace Initiatives

4. Global Multi-Mode Receiver Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Instrument Landing System (ILS)

4.1.2. Global Navigation Satellite System (GNSS)

4.1.3. Distance Measuring Equipment (DME)

4.1.4. VHF Omni-Directional Radio Range (VOR)

4.1.5. Others (Including ADF, Marker Beacons)

4.2. By Application (In Value %)

4.2.1. Commercial Aviation

4.2.2. Military Aviation

4.2.3. General Aviation

4.2.4. UAV

4.3. By Component (In Value %)

4.3.1. Hardware

4.3.2. Software

4.3.3. Services

4.4. By Platform (In Value %)

4.4.1. Fixed-Wing Aircraft

4.4.2. Rotary-Wing Aircraft

4.4.3. Unmanned Aerial Vehicles

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5. Global Multi-Mode Receiver Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Honeywell International Inc.

5.1.2. Thales Group

5.1.3. Rockwell Collins (Collins Aerospace)

5.1.4. Garmin Ltd.

5.1.5. Indra Sistemas S.A.

5.1.6. BAE Systems

5.1.7. Leonardo S.p.A.

5.1.8. Raytheon Technologies

5.1.9. Saab AB

5.1.10. General Dynamics Corporation

5.1.11. Northrop Grumman Corporation

5.1.12. Rohde & Schwarz GmbH & Co KG

5.1.13. Elbit Systems Ltd.

5.1.14. Safran Electronics & Defense

5.1.15. Curtiss-Wright Corporation

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Market Share, Technological Capabilities, Product Portfolio, Recent Innovations)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Multi-Mode Receiver Market Regulatory Framework

6.1. International Aviation Regulatory Bodies

6.2. Compliance with Aviation Safety Standards

6.3. Certification Processes for Multi-Mode Receivers

7. Global Multi-Mode Receiver Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Multi-Mode Receiver Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Component (In Value %)

8.4. By Platform (In Value %)

8.5. By Region (In Value %)

9. Global Multi-Mode Receiver Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial stage involves mapping the ecosystem of the global multi-mode receiver market, identifying major stakeholders such as manufacturers, system integrators, and end-users. This step is supported by desk research, incorporating secondary sources such as government publications and proprietary databases to outline market dynamics and growth factors.

Step 2: Market Analysis and Construction

This phase includes compiling historical data on the multi-mode receiver market, analyzing technological developments, and assessing market penetration. The construction of this dataset focuses on product adoption rates, geographic distribution, and emerging trends, ensuring accuracy in the market sizing process.

Step 3: Hypothesis Validation and Expert Consultation

We developed and refined our market hypotheses through interviews with industry experts, including senior executives and product managers at leading avionics firms. These consultations provide critical insights into the operational aspects of the market, validating the data collected during earlier phases.

Step 4: Research Synthesis and Final Output

The final phase entails synthesizing research findings and engaging directly with avionics manufacturers to confirm product trends, sales data, and future growth projections. This process ensures that the final output is comprehensive, accurate, and well-validated for industry stakeholders.

Frequently Asked Questions

01. How big is the Global Multi-Mode Receiver Market?

The Global Multi-Mode Receiver Market is valued at USD 1.12 billion, with demand primarily driven by modernization efforts in commercial and military aviation.

02. What are the challenges in the Global Multi-Mode Receiver Market?

Challenges in Global Multi-Mode Receiver Market include high initial costs associated with multi-mode receiver technology, stringent regulatory compliance, and limited availability of skilled avionics professionals.

03. Who are the major players in the Global Multi-Mode Receiver Market?

Major players in Global Multi-Mode Receiver Market include Honeywell International Inc., Thales Group, Collins Aerospace, Garmin Ltd., and Rohde & Schwarz GmbH, all of which leverage advanced avionics systems to maintain a competitive edge.

04. What are the growth drivers of the Global Multi-Mode Receiver Market?

The Global Multi-Mode Receiver Market growth drivers include the increasing adoption of GNSS technology in aviation, the modernization of air traffic management systems, and rising investments in military aviation.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.