Global Nanofiltration Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD1186

Region:Global

Author(s):Shreya Garg

Product Code:KROD1186

November 2024

81

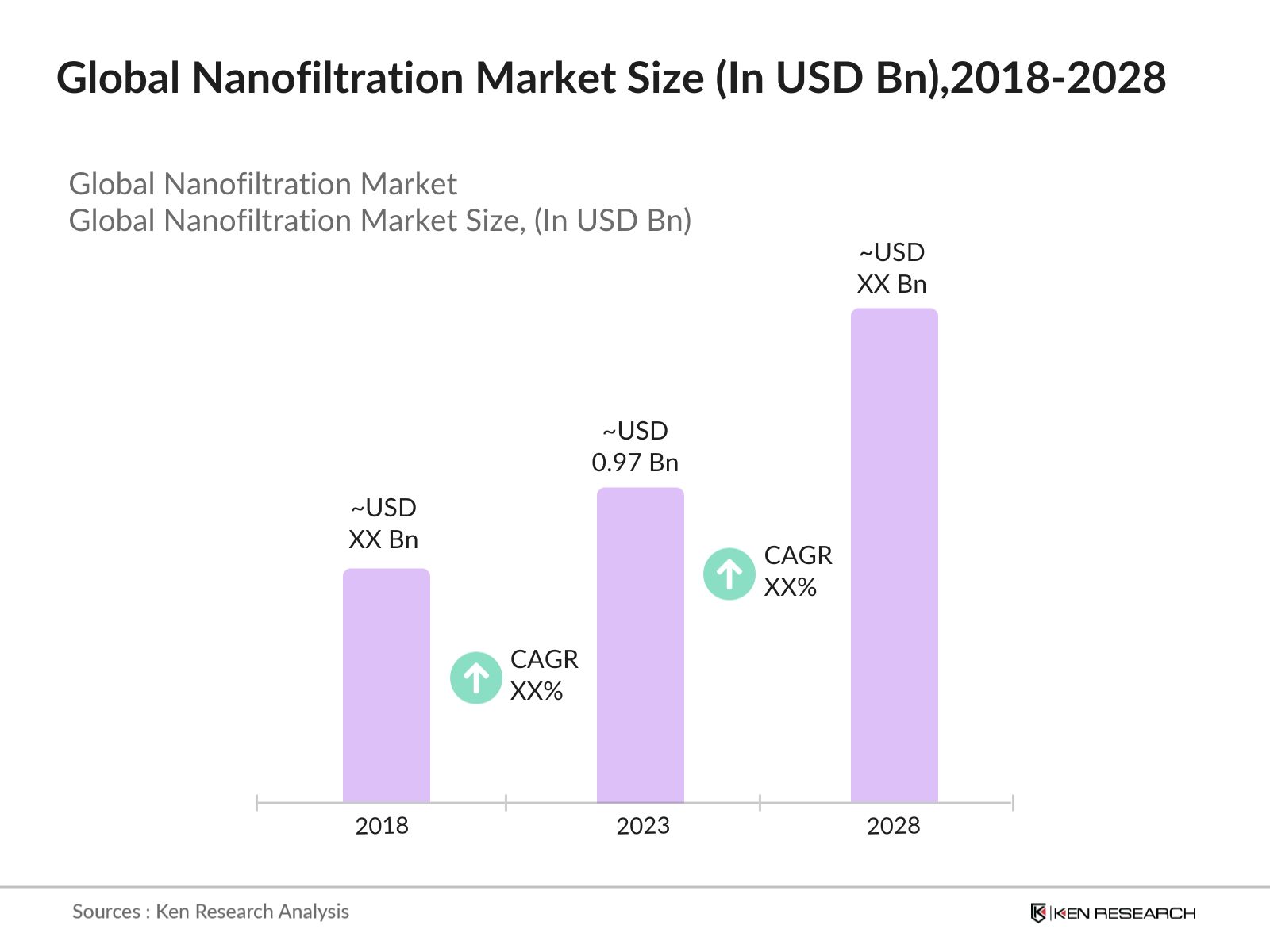

The global nanofiltration market was valued at USD 0.97 Billion in 2023. This growth is driven by the increasing demand for water treatment, particularly in regions facing water scarcity. The market is also being driven by industrial applications such as chemical processing and pharmaceuticals, which rely on nanofiltration membranes to achieve highly specific filtration tasks.

Key players in the global nanofiltration market include companies such as Dow Chemical Company, Suez Water Technologies, Toray Industries, Alfa Laval, and Pall Corporation. These players dominate the market by offering advanced nanofiltration membrane technologies and investing in research and development to expand their product portfolios. Their strong presence across multiple sectors such as water treatment and chemical manufacturing further reinforces their market positions.

Alfa Laval offers two types of NF spiral membranes, the NF and NF99HF, which utilize thin-film composite membranes. These membranes have a rejection capacity of 99% for magnesium sulfate and operate at pressures up to 50-55 bar, allowing them to retain larger ions and most organic components while permitting small ions to pass through.

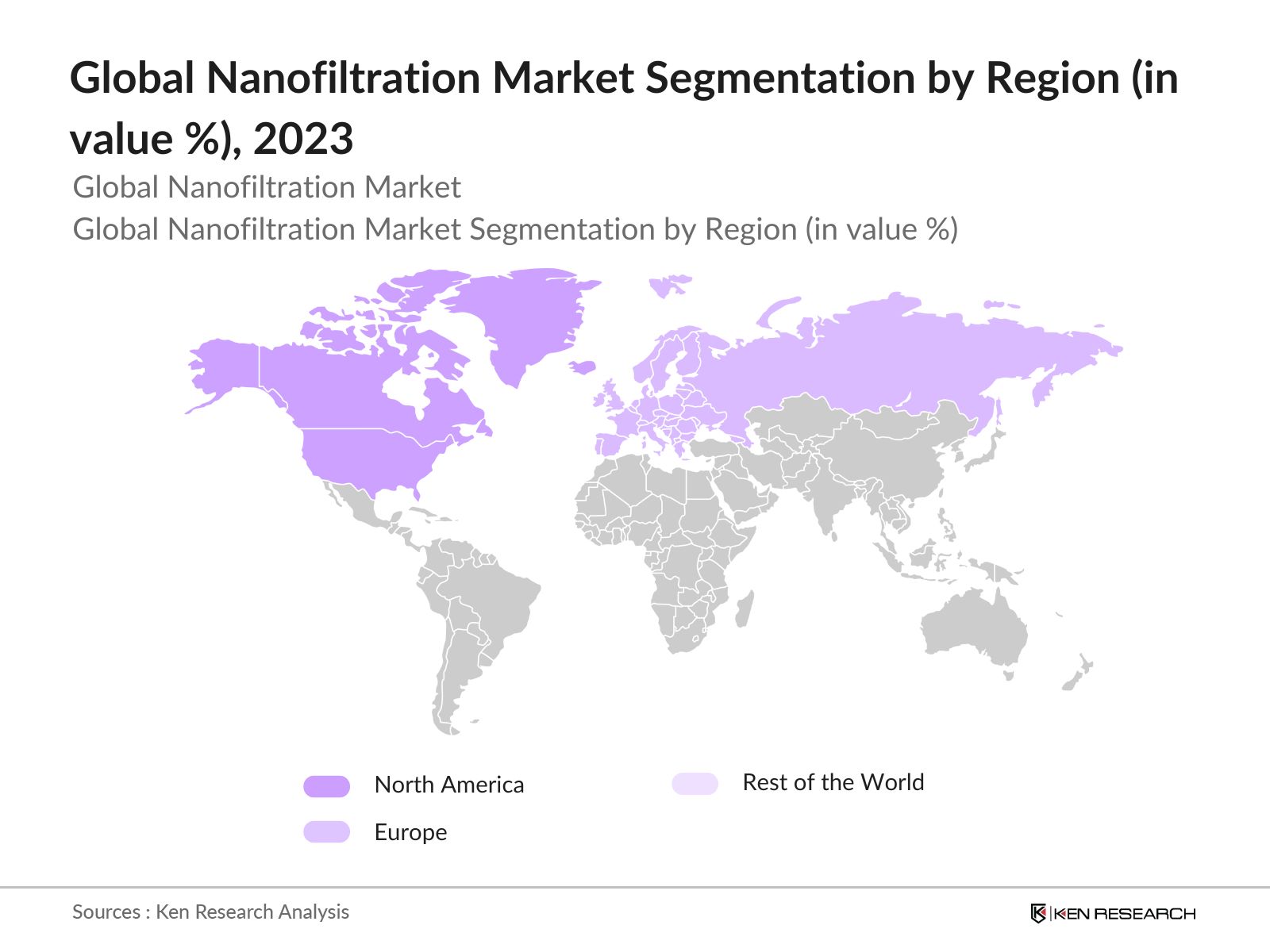

United States, dominated the global nanofiltration industry in 2023. The dominance can be attributed to strict environmental regulations on wastewater treatment, which compel industries to adopt advanced filtration technologies. Additionally, the presence of leading market players and well-established infrastructure further cements North Americas market leadership.

The global nanofiltration market is segmented into various sectors such as application, membrane type, region etc.

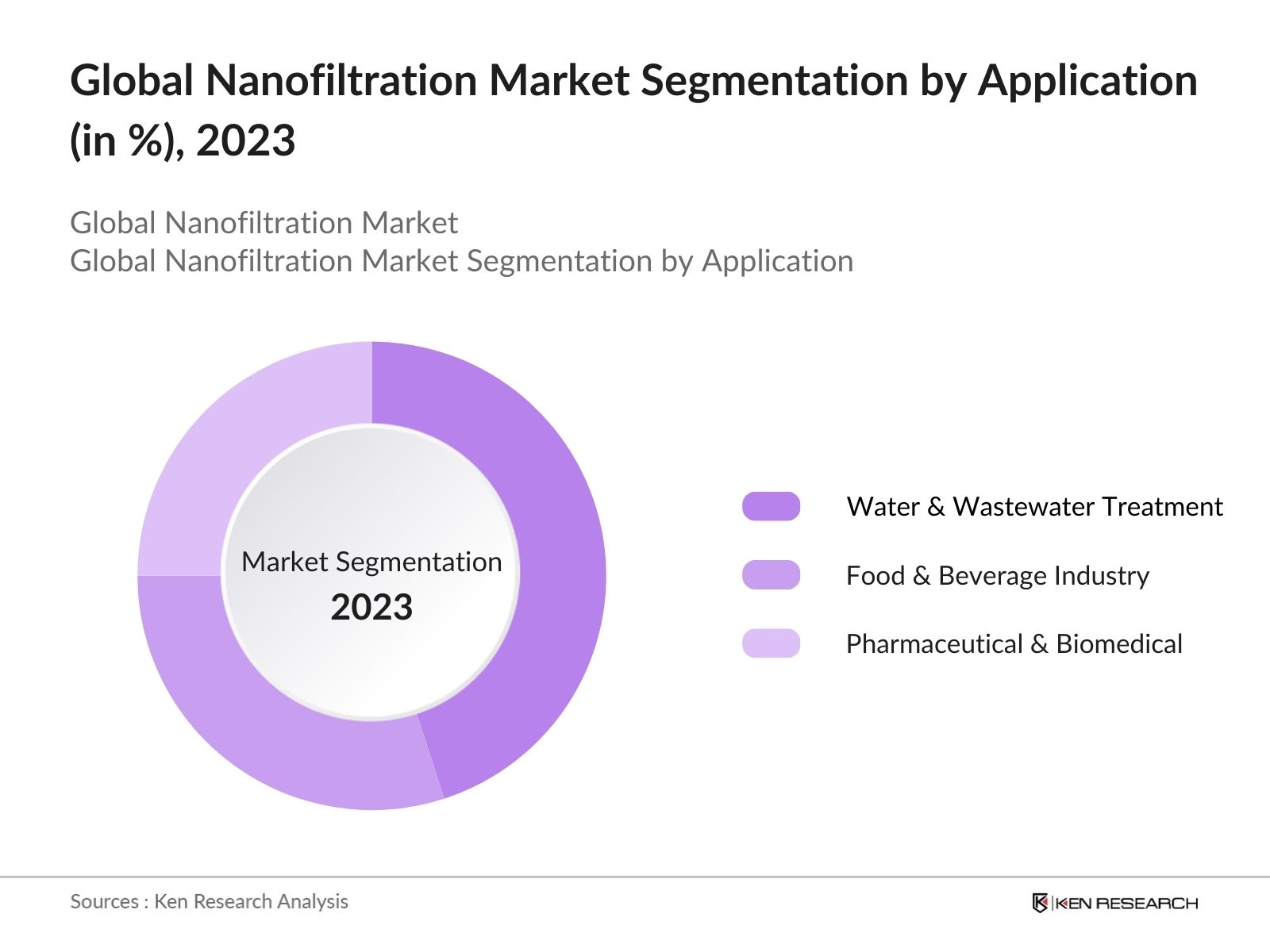

By Application: The market is segmented by application into Water & Wastewater Treatment, Food & Beverage Industry, and Pharmaceutical & Biomedical Industry. Recently, Water & Wastewater Treatment dominated the market share. The increasing need for clean water, rising governmental regulations, and growing desalination projects contribute to the dominance of this segment. The use of nanofiltration for removing contaminants and recovering materials makes it a preferred choice in the water sector.

By Membrane Type: The market is segmented by membrane type into Polymeric Membranes, Ceramic Membranes, and Hybrid Membranes. Polymeric segment held more than half of the market share, primarily due to its cost-effectiveness and widespread use in various industries, including water treatment and pharmaceuticals. Their flexibility and compatibility with different filtration systems make them the most popular type of membrane.

By Region: The market is divided into North America, South America, Europe, Asia-Pacific, and Rest of the World. North America led the global nanofiltration market share due to strict regulatory standards on water and wastewater treatment. The presence of key market players also strengthens the region's dominance.

|

Company |

Establishment Year |

Headquarters |

|---|---|---|

|

Dow Chemical Company |

1897 |

Midland, Michigan, USA |

|

Suez Water Technologies |

2000 |

Paris, France |

|

Toray Industries |

1926 |

Tokyo, Japan |

|

Alfa Laval |

1883 |

Lund, Sweden |

|

Pall Corporation |

1946 |

New York, USA |

The global nanofiltration market is expected to grow exponentially. The growth will be driven by stringent government regulations on wastewater treatment, the rise of industries in developing nations, and technological advancements in membrane efficiency. Increased investment in desalination projects and pharmaceutical applications will also play a significant role in expanding market demand.

|

By Application |

Water & Wastewater Treatment Food & Beverage Industry Pharmaceutical & Biomedical Industry |

|

By Membrane Type |

Polymeric Membranes Ceramic Membranes Hybrid Membranes |

|

By Region |

North America South America Europe APAC MEA |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Industrial Water Treatment Demand

3.1.2. Pharmaceutical Sector Expansion

3.1.3. Chemical Processing Industry Demand

3.1.4. Government Infrastructure Investments

3.2. Restraints

3.2.1. High Installation Costs

3.2.2. Membrane Fouling and Replacement Costs

3.2.3. Limited Adoption in Developing Economies

3.3. Opportunities

3.3.1. Technological Advancements in Membranes

3.3.2. Increasing Adoption in Emerging Markets

3.3.3. Expansion of Desalination Projects

3.4. Trends

3.4.1. Rise in Industrial Water Reuse

3.4.2. Focus on Sustainability and Efficiency

3.4.3. Development of Hybrid Membranes

3.5. Government Regulation

3.5.1. Water Treatment Standards

3.5.2. Pharmaceutical and Industrial Filtration Compliance

3.5.3. Public-Private Partnerships in Desalination Projects

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.1. By Application (in Value %)

4.1.1. Water & Wastewater Treatment

4.1.2. Food & Beverage Industry

4.1.3. Pharmaceutical & Biomedical Industry

4.2. By Membrane Type (in Value %)

4.2.1. Polymeric Membranes

4.2.2. Ceramic Membranes

4.2.3. Hybrid Membranes

4.3. By Region (in Value %)

4.3.1. North America

4.3.2. Europe

4.3.3. Asia-Pacific

4.3.4. Rest of the World

5.1. Detailed Profiles of Major Companies

5.1.1. Dow Chemical Company

5.1.2. Suez Water Technologies

5.1.3. Toray Industries

5.1.4. Alfa Laval

5.1.5. Pall Corporation

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Application (in Value %)

9.2. By Membrane Type (in Value %)

9.3. By Region (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Global Nanofiltration industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different Nanofiltration companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple nanofiltration companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such Nanofiltration companies.

The global nanofiltration market was valued at USD 1.2 billion in 2023, driven by the growing demand for advanced water treatment systems, industrial filtration, and pharmaceutical applications.

Challenges in the global nanofiltration market include high installation and maintenance costs, membrane fouling issues, limited adoption in developing countries, and regulatory barriers in emerging markets, which hinder widespread adoption of nanofiltration systems.

Key players in the global nanofiltration market include Dow Chemical Company, Suez Water Technologies, Toray Industries, Alfa Laval, and Pall Corporation. These companies dominate the market due to their advanced technologies, extensive R&D investments, and strong market presence.

The global nanofiltration market is propelled by the increasing need for water treatment in regions with water scarcity, expanding chemical industry applications, growing pharmaceutical sector demand for high-purity filtration, and government investment in desalination projects.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.