Global Network-Centric Warfare Market Outlook to 2030

Region:Global

Author(s):Shambhavi

Product Code:KROD7359

Region:Global

Author(s):Shambhavi

Product Code:KROD7359

December 2024

93

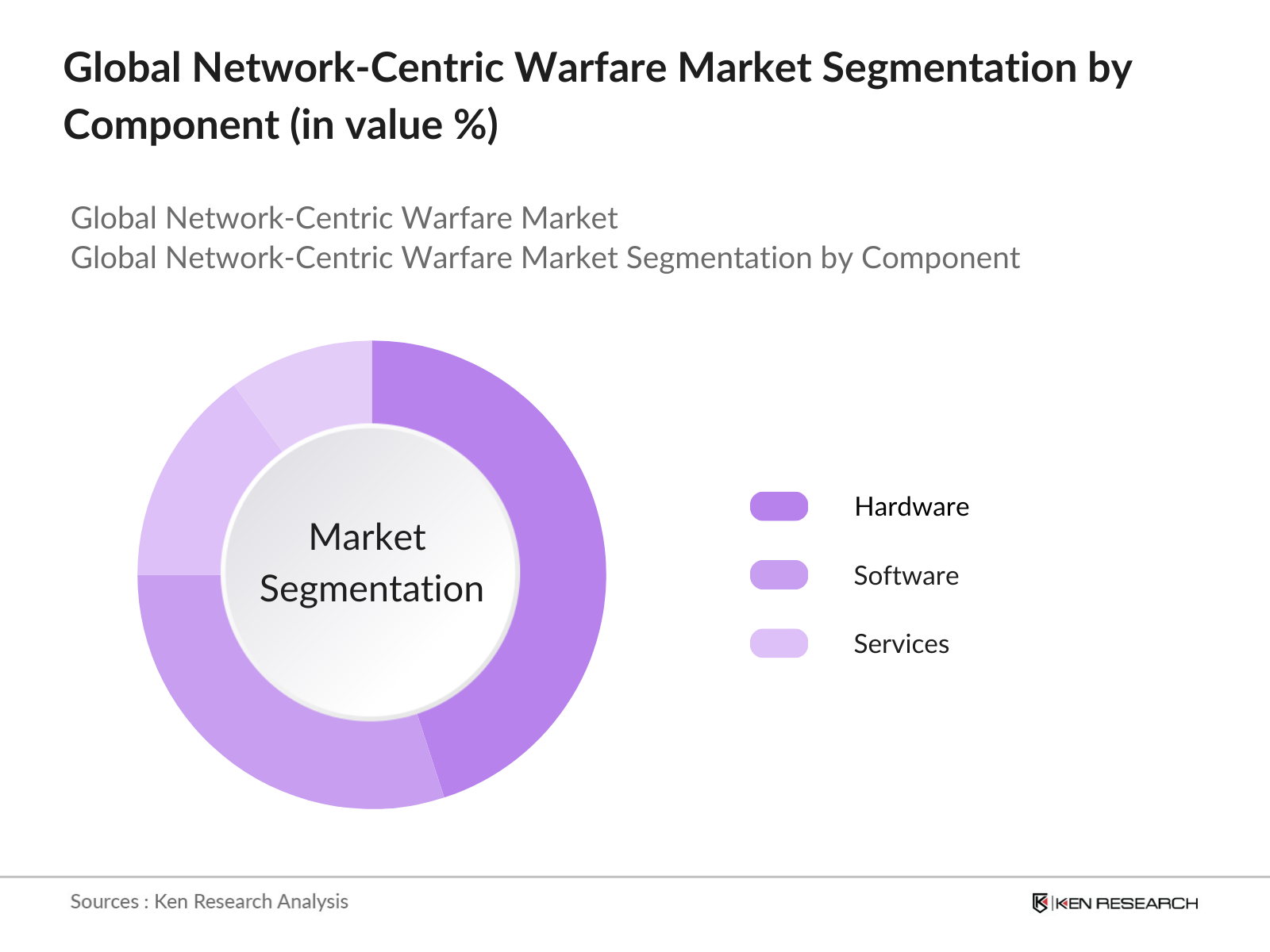

By Component: The Network-Centric Warfare Market is segmented by component into Hardware, Software, and Services. Hardware dominates the market due to its essential role in establishing a robust communication and data transmission infrastructure. Advanced hardware, including servers, satellites, and communication devices, ensures seamless data flow across various military units. High investment in military-grade hardware for resilience and security contributes to this segment's dominance.

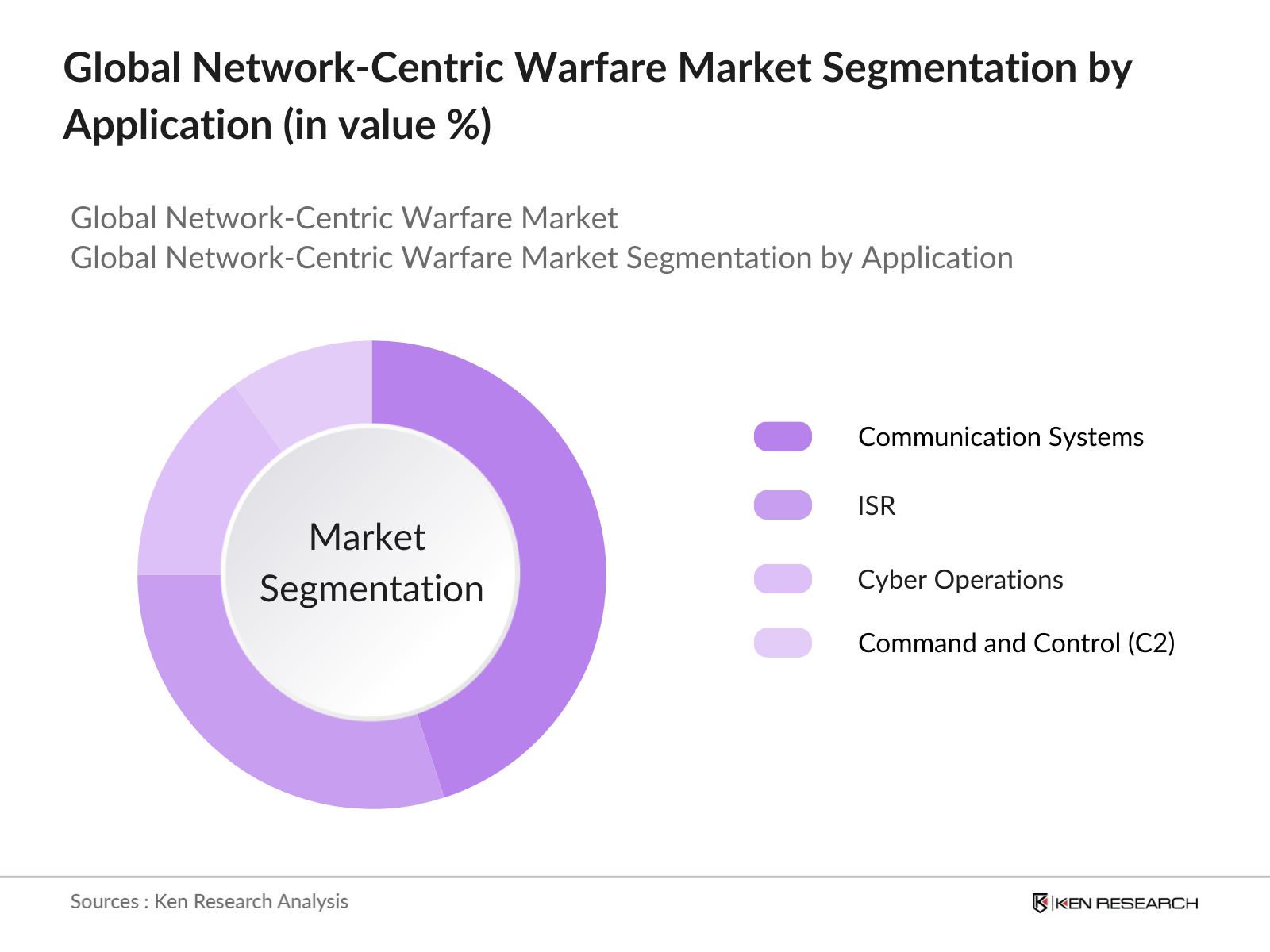

By Application: Network-centric warfare applications include Communication Systems, Intelligence, Surveillance, and Reconnaissance (ISR), Cyber Operations, and Command and Control (C2). ISR leads in application due to the critical need for real-time intelligence in modern warfare. Military forces globally rely on ISR to monitor, assess, and respond to threats, making it essential for both offensive and defensive operations. Investments in advanced sensors and aerial surveillance technologies enhance ISRs effectiveness in combat scenarios.

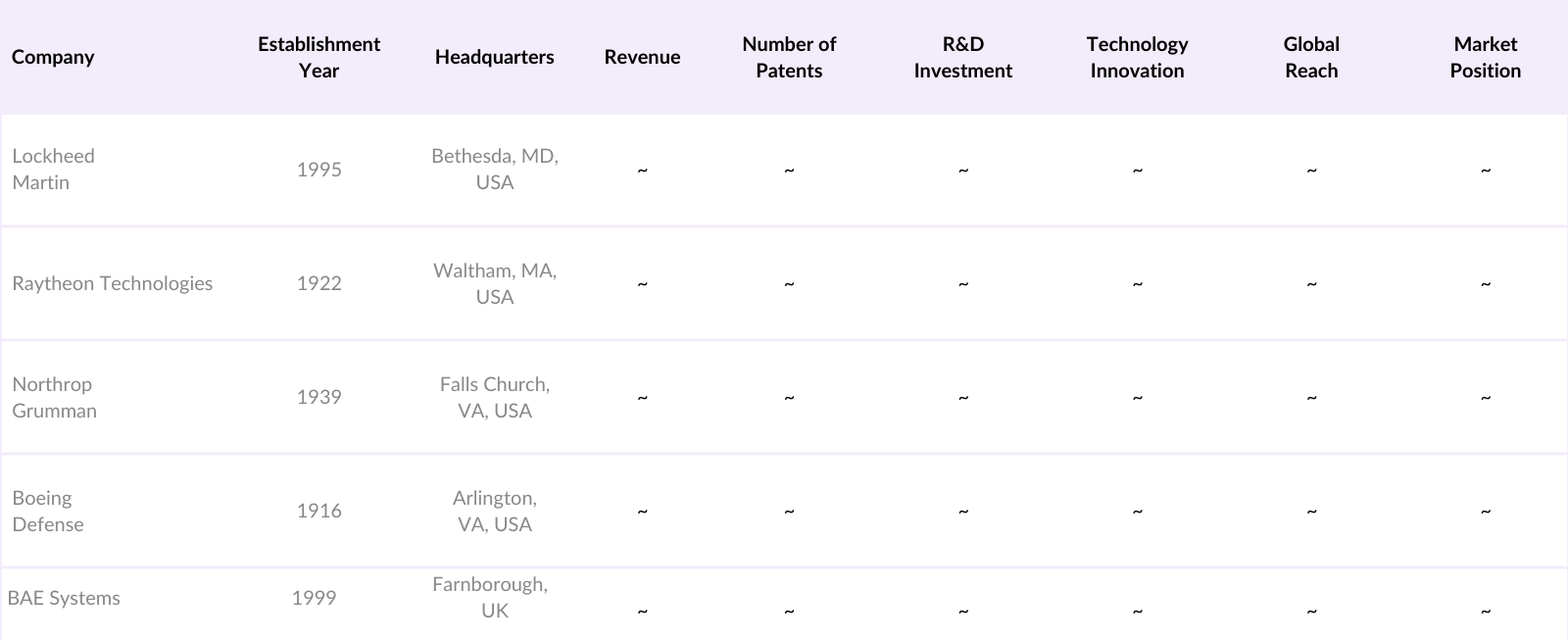

The Global Network-Centric Warfare Market is dominated by a few key players, with established companies like Lockheed Martin, Raytheon Technologies, and Northrop Grumman leading due to extensive R&D investments and high-tech offerings. These firms are known for their cutting-edge technologies, which provide critical communication and surveillance solutions within network-centric frameworks.

The Global Network-Centric Warfare Market is poised for substantial growth, driven by continuous advancements in communication technologies, AI integration, and increased global defense budgets. Countries worldwide are enhancing their military capabilities with network-centric solutions to meet rising cybersecurity threats and complex modern warfare requirements. Enhanced interoperability and real-time data processing capabilities will likely shape the sectors development, as military forces seek to maximize decision-making speed and efficiency on the battlefield.

|

Segment |

Sub-Segments |

|

Platform |

- Land-Based |

|

Application |

- Intelligence, Surveillance, and Reconnaissance (ISR) |

|

Architecture |

- Hardware |

|

Communication Network |

- Wired |

|

Mission Type |

- Tactical |

|

Region |

- North America |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Technological Advancements in Defense Systems

3.1.2 Increasing Defense Budgets Globally

3.1.3 Rising Geopolitical Tensions

3.1.4 Integration of AI and Machine Learning in Warfare

3.2 Market Challenges

3.2.1 High Implementation Costs

3.2.2 Cybersecurity Threats

3.2.3 Interoperability Issues Among Defense Systems

3.3 Opportunities

3.3.1 Development of Unmanned Platforms

3.3.2 Expansion into Emerging Markets

3.3.3 Collaboration Between Defense Contractors and Tech Firms

3.4 Trends

3.4.1 Adoption of Cloud-Based Solutions

3.4.2 Emphasis on Cyber Defense Capabilities

3.4.3 Shift Towards Multi-Domain Operations

3.5 Government Regulations

3.5.1 Defense Acquisition Policies

3.5.2 International Arms Trade Agreements

3.5.3 Data Protection and Privacy Laws

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4.1 By Platform (Value %)

4.1.1 Land-Based

4.1.2 Naval-Based

4.1.3 Air-Based

4.1.4 Unmanned Systems

4.2 By Application (Value %)

4.2.1 Intelligence, Surveillance, and Reconnaissance (ISR)

4.2.2 Communications

4.2.3 Command and Control

4.2.4 Computers

4.2.5 Cyber Operations

4.2.6 Electronic Warfare

4.3 By Architecture (Value %)

4.3.1 Hardware

4.3.2 Software

4.4 By Communication Network (Value %)

4.4.1 Wired

4.4.2 Wireless

4.5 By Mission Type (Value %)

4.5.1 Tactical

4.5.2 Strategic

4.6 By Region (Value %)

4.6.1 North America

4.6.2 Europe

4.6.3 Asia-Pacific

4.6.4 Middle East and Africa

4.6.5 Latin America

5.1 Detailed Profiles of Major Companies

5.1.1 Lockheed Martin Corporation

5.1.2 Northrop Grumman Corporation

5.1.3 Raytheon Technologies Corporation

5.1.4 BAE Systems plc

5.1.5 Thales Group

5.1.6 General Dynamics Corporation

5.1.7 L3Harris Technologies, Inc.

5.1.8 Elbit Systems Ltd.

5.1.9 Leonardo S.p.A.

5.1.10 Saab AB

5.1.11 Airbus SE

5.1.12 Boeing Defense, Space & Security

5.1.13 CACI International Inc.

5.1.14 Booz Allen Hamilton Holding Corporation

5.1.15 Leidos Holdings, Inc.

5.2 Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, R&D Expenditure, Market Share, Key Contracts, Technological Capabilities)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Defense Procurement Regulations

6.2 Compliance Requirements

6.3 Certification Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Platform (Value %)

8.2 By Application (Value %)

8.3 By Architecture (Value %)

8.4 By Communication Network (Value %)

8.5 By Mission Type (Value %)

8.6 By Region (Value %)

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThis initial stage involves mapping out the ecosystem of stakeholders in the Global Network-Centric Warfare Market. Through desk research using proprietary and secondary sources, we identify and categorize variables such as technology adoption rates, military spending trends, and defense capabilities to establish a baseline for analysis.

Here, historical data is analyzed, focusing on factors influencing market dynamics like service quality, revenue generation, and adoption rates. This stage leverages the detailed breakdown of segment contributions, compiling data to construct a clear market representation.

Hypotheses are established based on the preliminary findings, which are then validated through consultations with industry experts and stakeholders. These interactions provide crucial insights into operational and financial aspects, adding depth to the data analysis.

In this final phase, the insights gathered from various sources are synthesized into a comprehensive, validated report. The bottom-up approach ensures data reliability, and cross-referencing findings with industry standards strengthens the overall analysis.

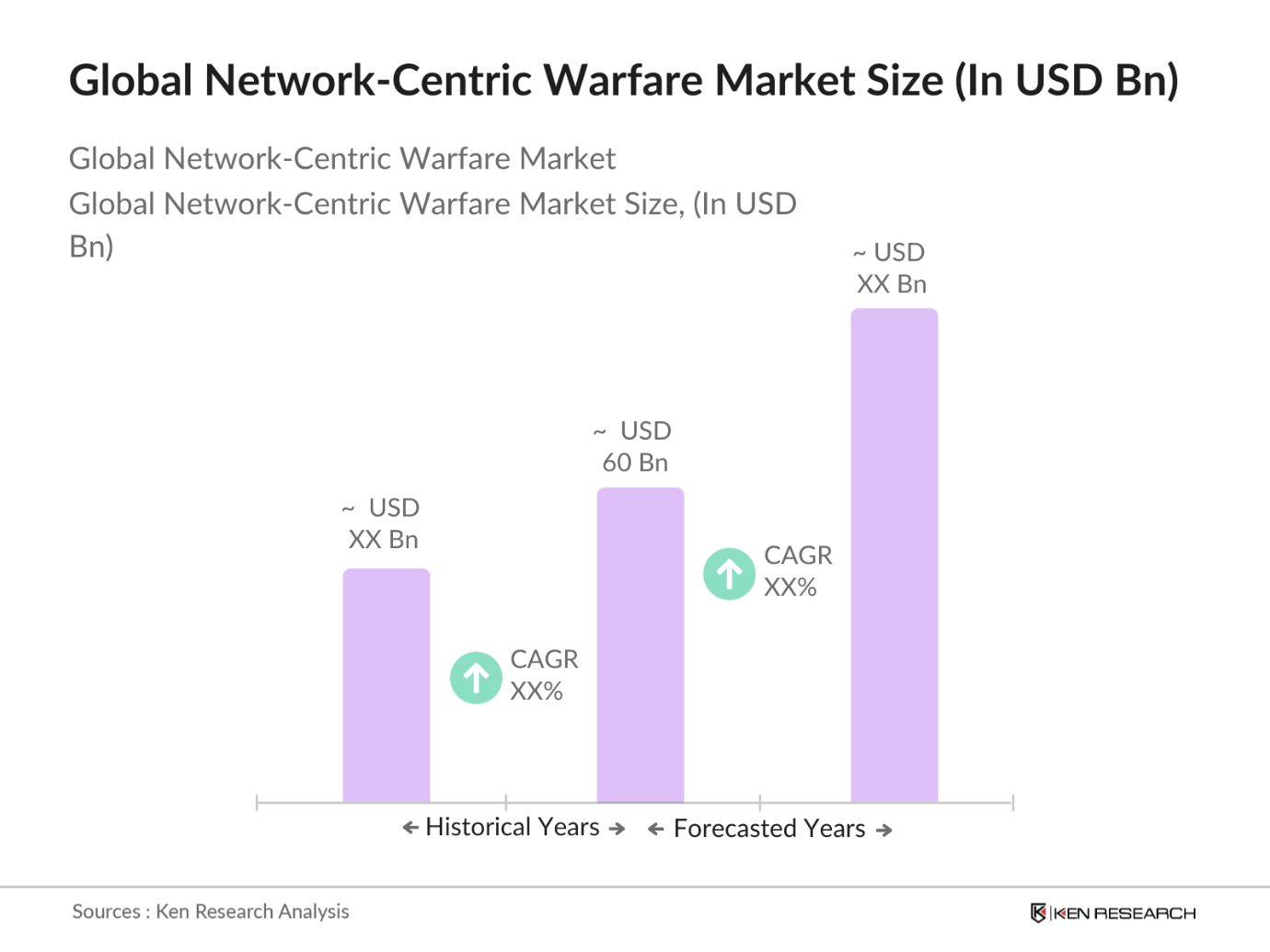

The Global Network-Centric Warfare Market is valued at USD 60 billion, driven by an increase in military spending and the demand for integrated, high-speed communication solutions.

Key challenges include high initial investment costs, integration complexities, and data security concerns, which can hinder seamless deployment and scalability.

Prominent companies include Lockheed Martin, Raytheon Technologies, Northrop Grumman, Boeing Defense, and BAE Systems. These firms dominate due to their extensive experience, technological innovation, and government contracts.

The market is propelled by rising cyber threats, the need for real-time data processing, and increasing defense budgets worldwide, which together support the adoption of network-centric warfare capabilities.

ISR (Intelligence, Surveillance, and Reconnaissance) and Hardware components lead in market dominance due to their critical roles in gathering intelligence and enabling communication infrastructure.

Future growth is expected due to advancements in AI, increased government spending on cybersecurity, and the global trend toward modernization of military communication systems.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.