Global Next Generation Firewall (NGFW) Market Outlook to 2030

Region:Global

Author(s):Sanjana

Product Code:KROD514

Region:Global

Author(s):Sanjana

Product Code:KROD514

October 2024

81

The Global Next Generation Firewall (NGFW) Market can be segmented based on several factors:

By Deployment Type: The market is segmented by deployment type into On-Premise, Cloud-based & Hybrid. In 2023, On-Premise accounts for the largest value share. This dominance is attributed to the preference of large enterprises and government organizations for maintaining control over their security infrastructure. On-premises NGFWs are favored due to their ability to provide high levels of customization and integration with existing network systems.

By Industry Vertical: The market is segmented by industry verticals into BFSI, Healthcare, IT & Telecom, Retail & Government. In 2023, BFSI dominates the market due to the industry's stringent regulatory requirements and the critical need for protecting sensitive financial data from cyber-attacks. The BFSI sector's ongoing digital transformation and increasing adoption of cloud services further necessitate advanced NGFW solutions to safeguard against potential security breaches.

By Industry Vertical: The market is segmented by industry verticals into BFSI, Healthcare, IT & Telecom, Retail & Government. In 2023, BFSI dominates the market due to the industry's stringent regulatory requirements and the critical need for protecting sensitive financial data from cyber-attacks. The BFSI sector's ongoing digital transformation and increasing adoption of cloud services further necessitate advanced NGFW solutions to safeguard against potential security breaches.

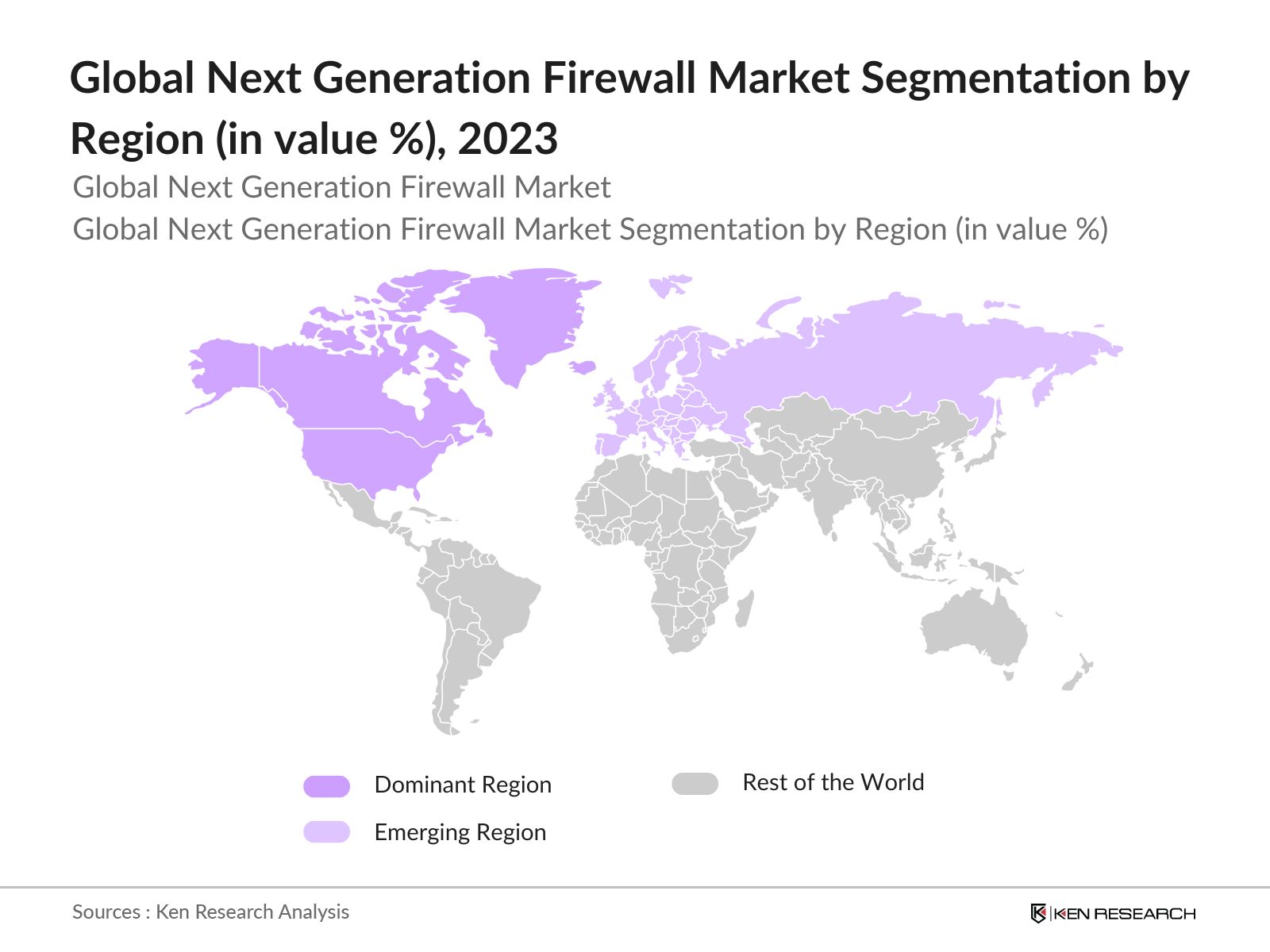

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, LAMEA and Middle East & Africa (MEA). In 2023, North America dominates the Global Next Generation Firewall (NGFW) market due to the presence of key NGFW vendors, a high level of cybersecurity awareness, and significant investments in network security infrastructure. The increasing frequency of cyberattacks on critical infrastructure and enterprises has led to heightened demand for NGFWs in the USA, making it the largest market globally.

|

Company |

Establishment Year |

Headquarters |

|

Palo Alto Networks |

2005 |

Santa Clara, USA |

|

Fortinet |

2000 |

Sunnyvale, USA |

|

Cisco Systems |

1984 |

San Jose, USA |

|

Check Point Software |

1993 |

Tel Aviv, Israel |

|

Juniper Networks |

1996 |

Sunnyvale, USA |

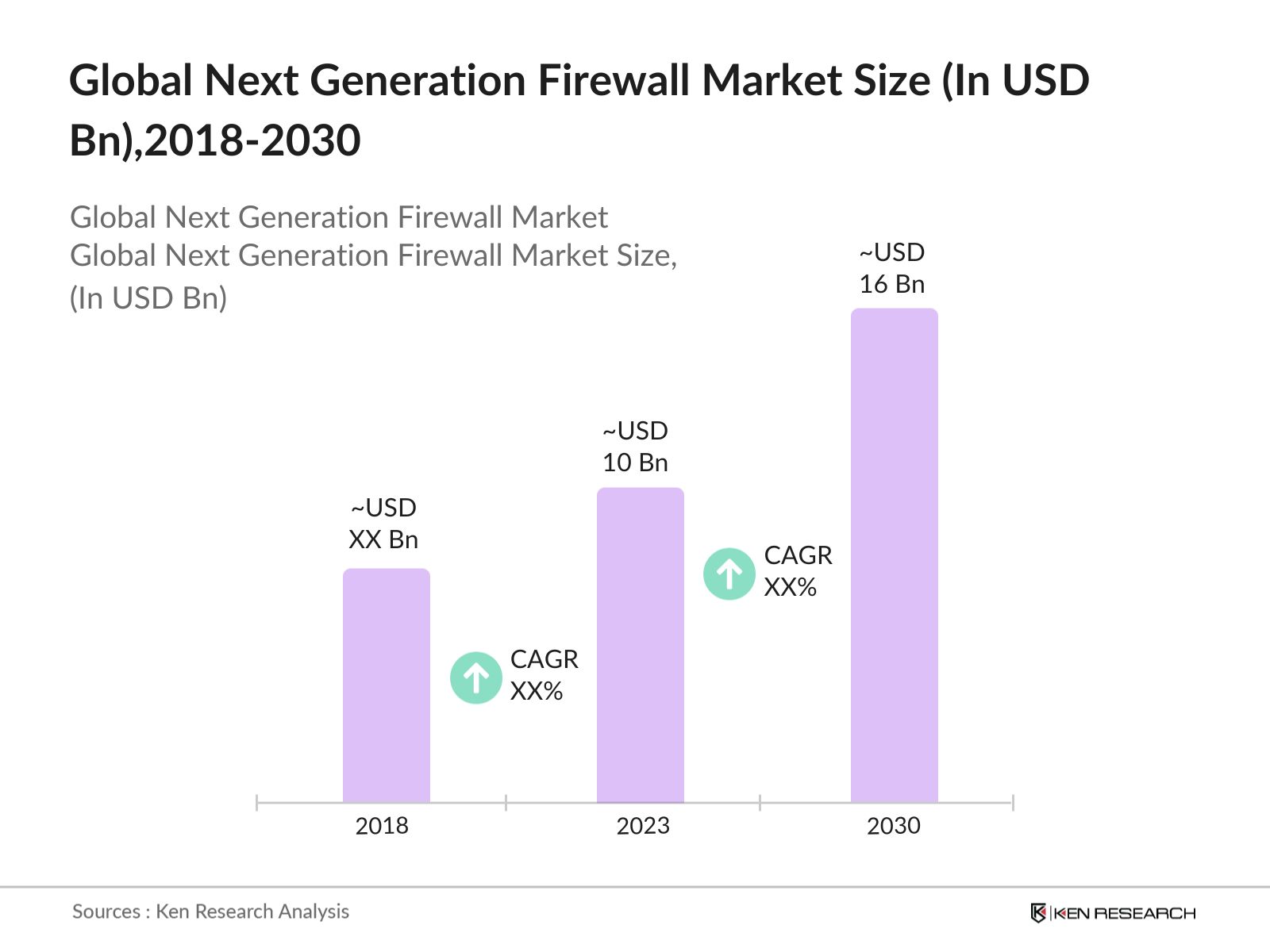

The market is expected to reach USD 16 Bn by 2030 driven by the increasing demand for advanced cybersecurity solutions in the face of evolving cyber threats. The integration of machine learning and AI into NGFWs will enable organizations to proactively defend against sophisticated attacks, reducing response times and improving overall network security.

|

By Region |

North America Europe APAC Latin America MEA |

|

By Component |

Solutions Services |

|

By Deployment Type |

On-premise Cloud Hybrid |

|

By Industry |

BFSI Healthcare IT & Telecom Retail Government |

|

By Organization Size |

Large Organization Small & Medium Enterprises (SMEs) |

1.1 Definition and Scope

1.1. Market Definition

1.2. Market Scope and Boundaries

3.1. Historical CAGR (2018-2023)

3.2. Projected CAGR (2023-2030)

4.1 Historical Market Size

4.2 Year-on-Year Growth Analysis

4.3 Key Market Developments and Milestones

5.1 Growth Drivers

5.1.1. Rising Cybersecurity Threats

5.1.2. Regulatory Compliance and Standards

5.1.3. Adoption of Cloud-Based Services

5.2 Restraints

5.2.1. High Implementation Costs

5.2.2. Complexity of Integration with Existing Systems

5.2.3. Evolving Cyber Threats

5.4 Opportunities

5.4.1. Growth in AI and Machine Learning Integration

5.4.2. Increasing Demand for Managed Security Services

5.4.3. Expansion into Emerging Markets

5.5 Trends

5.5.1. Shift towards Zero Trust Architecture

5.5.2. Adoption of Cloud-Native Security Solutions

5.5.3. Integration with IoT and Smart Devices

5.6 Government Regulations

5.6.1 U.S. Cybersecurity Modernization Initiative (2023)

5.2. European Union Cybersecurity Resilience Act (2024)

5.3. National Cybersecurity Policies in Emerging Markets

5.7 SWOT Analysis

5.7.1. Strengths

5.7.2. Weaknesses

5.7.3. Opportunities

5.7.4. Threats

5.8 Stakeholder Ecosystem

5.8.1. Key Stakeholders

5.8.2. Role of Value Chain Participants

5.9 Competition Ecosystem

5.9.1. Competitive Landscape Overview

5.9.2. Market Positioning of Key Players

6.1 By Deployment Type (in Value %)

6.1.1. On-Premises

6.1.2. Cloud-Based

6.1.3. Hybrid

6.2 By Industry Vertical (in Value %)

6.2.1. BFSI

6.2.2. Healthcare

6.2.3. IT & Telecom

6.2.4. Government

6.2.5. Retail

6.3 By Technology (in Value %)

6.3.1. Deep Packet Inspection (DPI)

6.3.2. Application Control

6.3.3. User Identity Management

6.4 By Region (in Value %)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia-Pacific

6.4.4. Latin America

6.4.5. Middle East & Africa

7.1 Detailed Profiles of Major Companies

7.1.1. Palo Alto Networks

7.1.2. Fortinet

7.1.3. Cisco Systems

7.1.4. Check Point Software Technologies

7.1.5. Juniper Networks

7.1.6 Barracuda Networks

7.1.7 SonicWall

7.1.8 Forcepoint

7.1.9 WatchGuard Technologies

7.1.10 Sophos Group

7.1.11 Hillstone Networks

7.1.12 Huawei Technologies Co., Ltd.

7.1.13 Zscaler

7.1.14 AhnLab

7.1.15 Sangfor Technologies

7.2 Cross Comparison Parameters

7.2.1. No. of Employees

7.2.2. Headquarters

7.2.3. Inception Year

7.2.4. Revenue

8.1 Market Share Analysis

8.1.1. Market Share by Key Players

8.1.2. Regional Market Share

8.2 Strategic Initiatives

8.2.1. Product Launches and Innovations

8.2.2. Strategic Partnerships and Collaborations

8.2.3. Geographical Expansions

8.3 Mergers and Acquisitions

8.3.1. Recent M&A Deals

8.3.2. Impact on Market Dynamics

9.1 Cybersecurity Standards and Compliance

9.1.1. National and International Standards

9.1.2. Industry-Specific Compliance Requirements

9.2 Certification Processes

9.2.1. Certification Bodies

9.2.2. Certification Requirements and Procedures

9.3 Impact of Regulatory Changes

9.3.1. Impact on Product Development

9.3.2. Impact on Market Entry and Expansion

10.1 Future Market Size Projections

10.1.1. Market Size by Year (2023-2028)

10.1.2. Market Size by Key Segments

10.2 Key Factors Driving Future Market Growth

10.2.1. Technological Advancements

10.2.2. Increased Regulatory Focus on Cybersecurity

10.2.3. Growth in Cloud Computing and IoT

11.1 By Deployment Type (in Value %)

11.2 By Industry Vertical (in Value %)

11.3 By Technology (in Value %)

11.4 By Region (in Value %)

12.1 TAM/SAM/SOM Analysis

12.2 Customer Cohort Analysis

12.3 Marketing Initiatives

12.4 White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on next generation firewall market over the years, penetration of marketplaces and service providers ratio to compute revenue generated next generation firewall market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple next generation firewall companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from next generation firewall companies.

In 2023, the Global Next Generation Firewall (NGFW) Market was valued at USD 10 Bn driven by the growing demand for advanced security solutions due to increasing cyber threats and data breaches.

Challenges in the Global Next Generation Firewall (NGFW) market include high implementation costs, complexity in integration and evolving cyber threat landscape. Integrating NGFWs into existing IT infrastructure can be a complex process, particularly for organizations with legacy systems.

Major players in the NGFW market include Palo Alto Networks, Fortinet, Cisco Systems, Check Point Software Technologies, and Juniper Networks. These companies have a significant market share due to their strong product portfolios and extensive customer base.

The market is propelled by the rise in cloud computing adoption, cybersecurity threats & strict regulatory requirements. The increasing frequency and sophistication of cyber-attacks globally are driving the demand for Next Generation Firewalls (NGFW).

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.