Global Nutritional Drinks Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD5798

December 2024

88

About the Report

Global Nutritional Drinks Market Overview

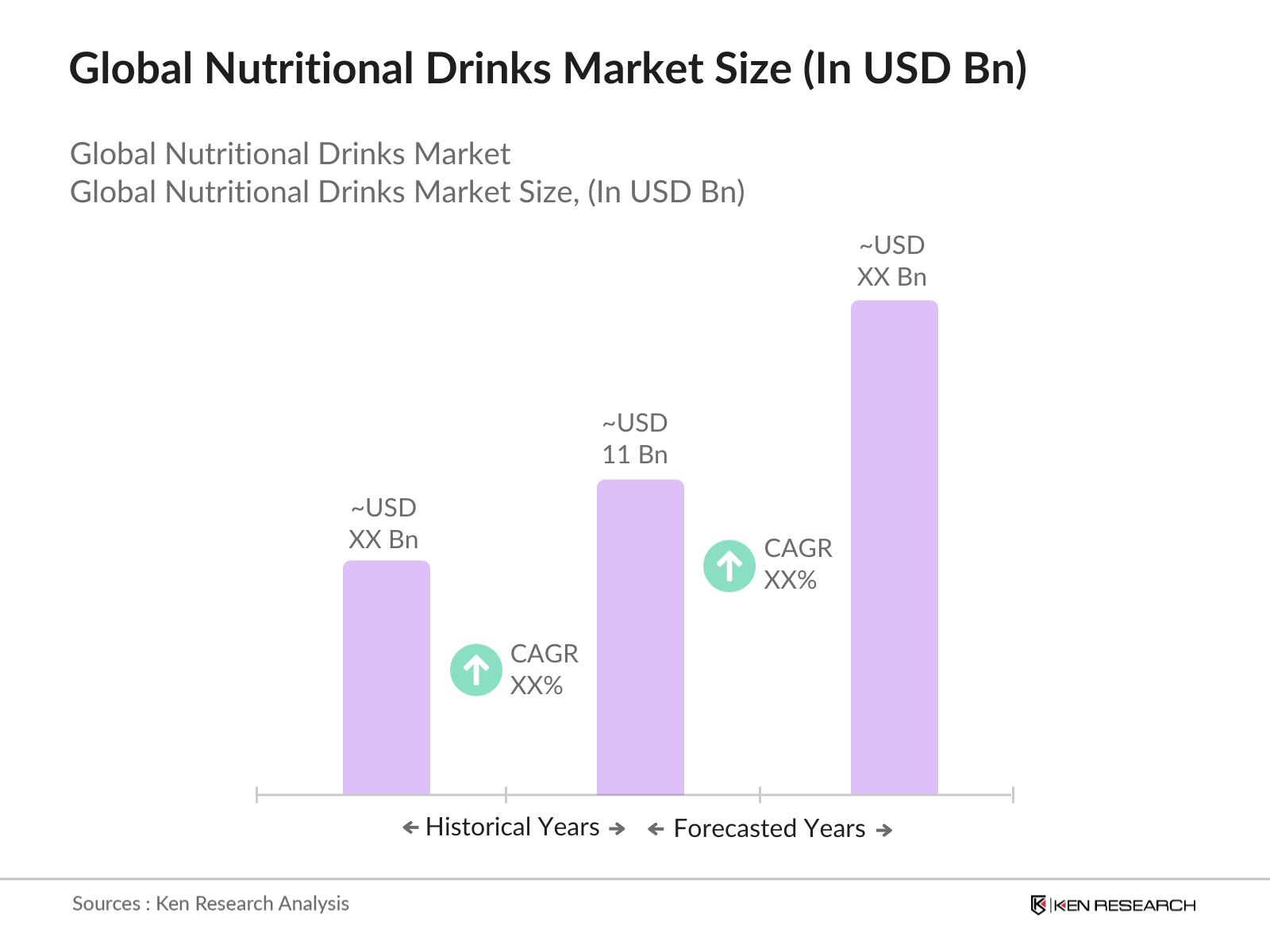

- The global nutritional drinks market is valued at USD 11 billion based on a detailed historical analysis. The market's growth is driven by the rising consumer demand for healthier and more functional beverages that provide essential nutrients. Factors such as an aging population, increased health awareness, and the growing need for meal replacements due to busy lifestyles are contributing to this demand. Innovations in product formulations, such as plant-based protein drinks, are also key drivers in expanding the market.

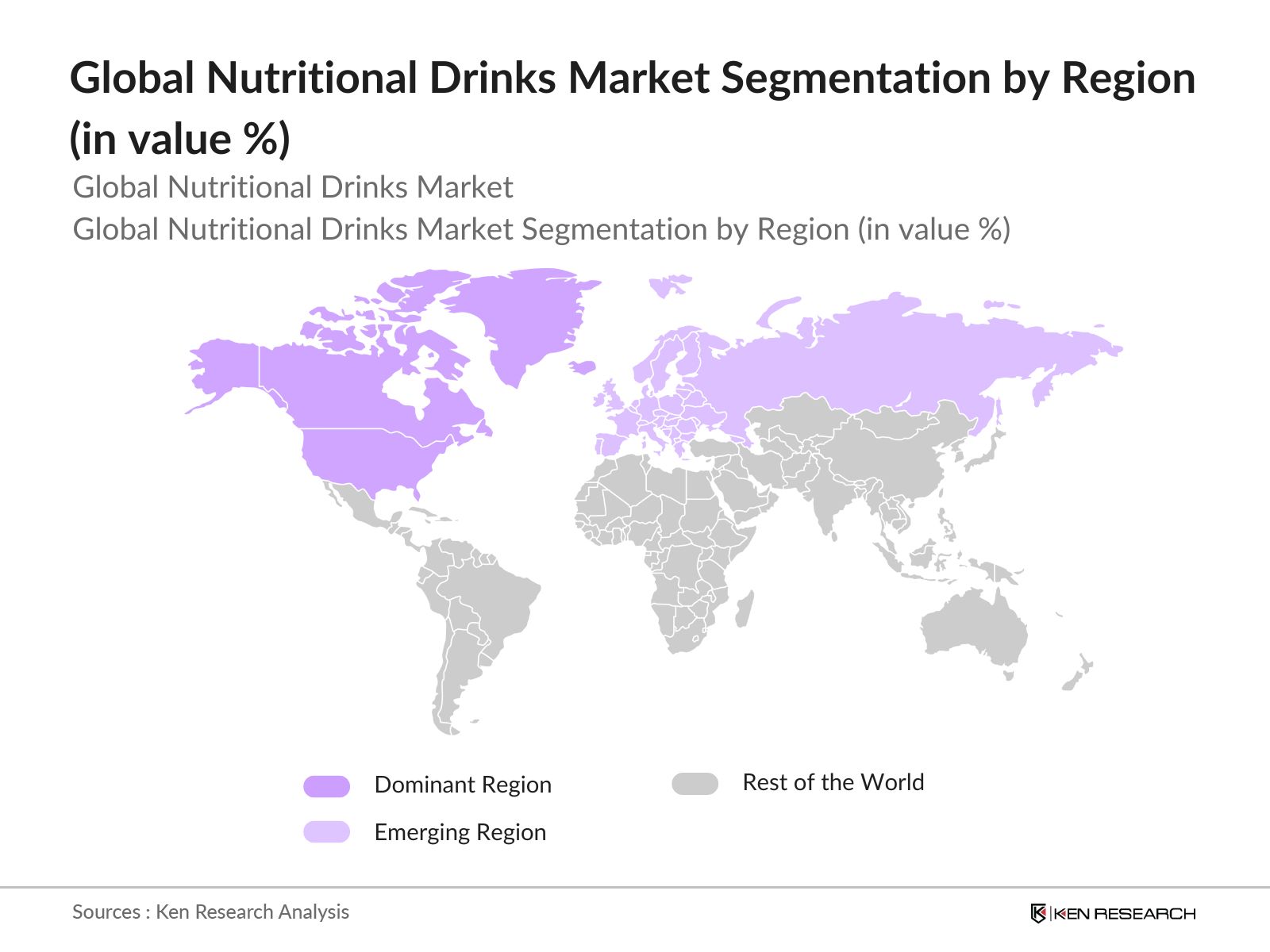

- North America and Europe are the leading regions in the global nutritional drinks market. These regions dominate due to their advanced healthcare systems, higher disposable income, and consumer preference for health-focused products. Countries like the U.S. and Germany have a strong presence of key players, coupled with high levels of awareness and adoption of functional beverages. Additionally, the increasing trend toward fitness and wellness in these countries supports the continuous demand for nutritional drinks.

- Several governments, particularly in developing nations, are implementing subsidized nutritional programs to combat malnutrition. In 2024, India is expected to expand its "Poshan Abhiyaan" initiative, aimed at providing affordable nutritional supplements to children and pregnant women. This will drive the demand for nutritional drinks formulated for specific nutritional deficiencies.

Global Nutritional Drinks Market Segmentation

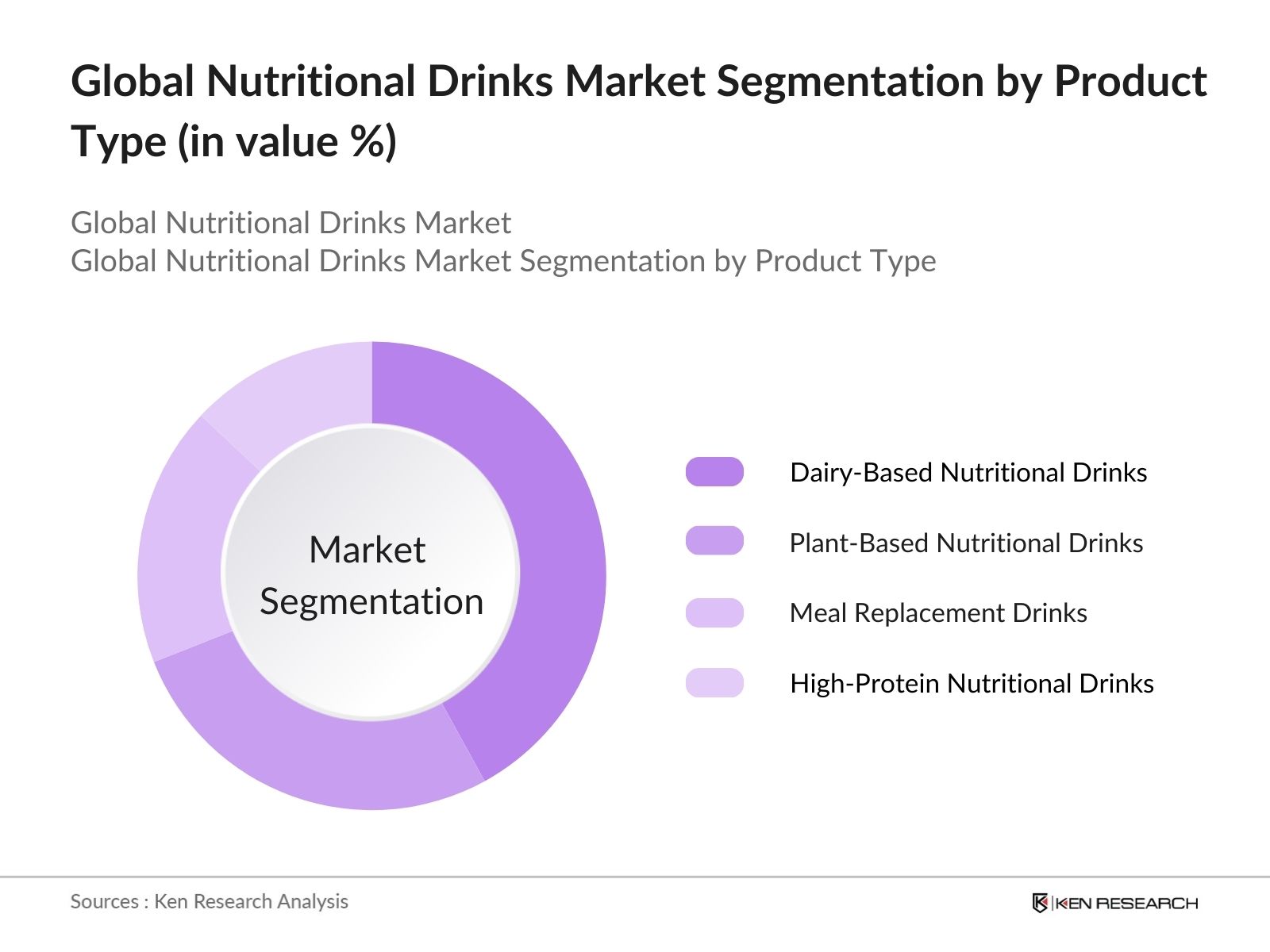

By Product Type: The global nutritional drinks market is segmented by product type into dairy-based nutritional drinks, plant-based nutritional drinks, meal replacement drinks, and high-protein nutritional drinks. Dairy-based nutritional drinks have a dominant market share under the product type segmentation. This dominance can be attributed to their longstanding presence in the market and the fact that they are widely perceived as a reliable source of essential nutrients like calcium and protein. Moreover, established brands such as Ensure and Boost have built strong consumer trust, making these products a preferred choice, particularly among older adults seeking nutritional support.

By Region: The market is segmented by region into North America, Asia-Pacific, Europe, Latin America and the Middle East and Africa. North America stands as the dominant region, largely driven by the high consumer awareness of health and wellness, coupled with significant disposable income levels. The region is home to key players such as Abbott Laboratories and PepsiCo, who have established strong distribution networks and are continuously innovating with new product formulations. Additionally, the aging population in North America contributes to the increasing demand for nutritional drinks aimed at improving health outcomes.

By Age Group: The market is also segmented by age group into adults, children, and seniors. Nutritional drinks for seniors lead the market in terms of share under this segmentation. This is due to the increasing global aging population and the specific dietary needs of this demographic, such as higher protein intake and calcium for bone health. Brands have been targeting this age group with specialized formulas that address common health concerns like muscle maintenance and immunity boosting, driving the popularity of these products among seniors.

Global Nutritional Drinks Market Competitive Landscape

The global nutritional drinks market is characterized by the presence of several key players. These companies have established a significant market presence through product innovation, strategic partnerships, and widespread distribution networks. The consolidation of market leaders has further strengthened their influence on the global stage.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD Bn) |

Product Range |

R&D Investments |

Partnerships |

Global Reach |

|

Abbott Laboratories |

1888 |

U.S. |

||||||

|

Nestl S.A. |

1867 |

Switzerland |

||||||

|

The Kraft Heinz Company |

2015 |

U.S. |

||||||

|

Danone S.A. |

1919 |

France |

||||||

|

Glanbia Plc |

1997 |

Ireland |

Global Nutritional Drinks Market Analysis

Growth Drivers

- Health and Wellness Trends: The increasing global focus on health and wellness is driving the demand for nutritional drinks. Consumers are seeking beverages that provide functional health benefits such as immunity boosts and digestive support. The World Bank reports that in 2024, over 1.4 billion individuals worldwide are expected to experience lifestyle-related health issues like obesity and heart disease, further increasing the demand for nutritional products that promote healthier lifestyles. This trend is particularly strong in developed markets where consumers have high disposable income to invest in wellness products.

- Rising Demand for Functional Beverages: Functional beverages, including nutritional drinks, are gaining popularity due to their added benefits beyond hydration, such as enhanced nutrition and energy boosts. The global population in 2024 is projected to exceed 8 billion, creating a significant consumer base for such products. This surge in demand is also seen in fitness-oriented segments, where nutritional drinks are tailored to improve physical performance and recovery.

- Aging Population and Nutritional Needs: The growing aging population, particularly in countries like Japan and Germany, is driving the consumption of nutritional drinks that cater to specific dietary needs, such as bone health and muscle maintenance. In 2024, the United Nations estimates that over 1.1 billion people globally will be aged 60 or older, representing a substantial market for age-specific nutritional beverages that address nutrient deficiencies and support healthier aging.

Market Challenges

- High Competition and Price Sensitivity: The nutritional drinks market is highly competitive, with numerous local and global players offering similar products. Price sensitivity remains a key challenge, especially in emerging markets, where consumers prioritize affordability over premium nutrition. As of 2024, data indicates that emerging markets such as India and Brazil will see increased competition, particularly from domestic players who offer lower-priced alternatives.

- Regulatory Barriers in Nutritional Claims: Strict regulations governing nutritional claims pose a challenge for companies operating in the market. In markets like the European Union and the United States, regulatory bodies like the FDA enforce stringent guidelines that limit the marketing of health claims. This has led to product delays and reformulation costs. In 2024, regulatory restrictions are expected to further impact product innovation, particularly in regions where compliance costs remain high.

Global Nutritional Drinks Market Future Outlook

Over the next five years, the global nutritional drinks market is expected to experience significant growth, driven by continuous innovations in product formulations, such as plant-based and organic options, as well as the growing focus on personalized nutrition. The market will also benefit from increasing consumer awareness around health and wellness, especially in emerging markets where nutritional deficiencies remain prevalent.

Future Market Opportunities

- Expansion in Plant-Based Nutritional Drinks: There is a rising consumer preference for plant-based nutritional drinks, driven by concerns over sustainability and lactose intolerance. The global plant-based market is projected to see significant growth, with new product innovations catering to diverse dietary needs. In 2024, with a global population of over 1.5 billion individuals being lactose intolerant, plant-based alternatives will continue to gain traction, particularly in regions like Asia-Pacific, where the lactose intolerance rate is among the highest.

- Growing Demand in Asia-Pacific: The Asia-Pacific region presents significant growth opportunities due to increasing health awareness and a growing middle-class population. In countries like China and India, the demand for nutritional drinks is expected to rise significantly, driven by urbanization and changing consumer preferences. In 2024, the number of urban dwellers in China is estimated to surpass 850 million, creating a large consumer base for health-focused beverages.

Scope of the Report

|

By Product Type |

Dairy-Based Nutritional Drinks Plant-Based Nutritional Drinks Meal Replacement Drinks High-Protein Nutritional Drinks Vitamin and Mineral-Enriched Drinks |

|

By Age Group |

Adults Children Seniors |

|

By Distribution Channel |

Supermarkets and Hypermarkets Pharmacies and Drugstores Online Retail Specialized Nutrition Stores |

|

By Packaging Type |

Bottles Tetra Packs Cans Sachets |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Global Nutritional Drinks Key Target Audience

Nutritional Beverage Manufacturers

Healthcare Providers and Nutritionists

Sports and Fitness Industry Professionals

Hospitals and Healthcare Institutions

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., FDA, EFSA)

Supermarkets and Hypermarkets

Retail Pharmacies and Specialized Nutrition Stores

Companies

Global Nutritional Drinks Major Players

Abbott Laboratories

Nestl S.A.

The Kraft Heinz Company

Danone S.A.

Glanbia Plc

Herbalife Nutrition Ltd.

Amway Corp.

PepsiCo, Inc.

Huel Inc.

Orgain, Inc.

Table of Contents

Global Nutritional Drinks Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

Global Nutritional Drinks Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

Global Nutritional Drinks Market Analysis

3.1. Growth Drivers

Health and Wellness Trends

Rising Demand for Functional Beverages

Aging Population and Nutritional Needs

Technological Advancements in Nutrient Delivery Systems

3.2. Market Challenges

High Competition and Price Sensitivity

Regulatory Barriers in Nutritional Claims

Fluctuations in Raw Material Costs

Limited Awareness in Emerging Markets

3.3. Opportunities

Expansion in Plant-Based Nutritional Drinks

Growing Demand in Asia-Pacific

Innovations in Packaging for Enhanced Shelf Life

Partnerships Between Healthcare Providers and Beverage Companies

3.4. Trends

Increasing Use of Personalized Nutrition

Integration of Functional Ingredients (e.g., Probiotics, Collagen)

Rise of Online and Direct-to-Consumer Sales Channels

Growing Preference for Organic and Clean-Label Products

3.5. Government Regulation

Labeling and Nutritional Content Regulations

Compliance with Food Safety Standards

Impact of International Trade Policies on Nutritional Drinks

Government Initiatives to Promote Healthy Diets

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

Global Nutritional Drinks Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Dairy-Based Nutritional Drinks

4.1.2. Plant-Based Nutritional Drinks

4.1.3. Meal Replacement Drinks

4.1.4. High-Protein Nutritional Drinks

4.1.5. Vitamin and Mineral-Enriched Drinks

4.2. By Age Group (In Value %)

4.2.1. Adults

4.2.2. Children

4.2.3. Seniors

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets and Hypermarkets

4.3.2. Pharmacies and Drugstores

4.3.3. Online Retail

4.3.4. Specialized Nutrition Stores

4.4. By Packaging Type (In Value %)

4.4.1. Bottles

4.4.2. Tetra Packs

4.4.3. Cans

4.4.4. Sachets

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

Global Nutritional Drinks Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Abbott Laboratories

5.1.2. Nestl S.A.

5.1.3. The Kraft Heinz Company

5.1.4. Danone S.A.

5.1.5. Glanbia Plc

5.1.6. Herbalife Nutrition Ltd.

5.1.7. Amway Corp.

5.1.8. PepsiCo, Inc.

5.1.9. Kellogg Company

5.1.10. Unilever Group

5.1.11. General Mills, Inc.

5.1.12. Huel Inc.

5.1.13. GlaxoSmithKline Plc

5.1.14. Orgain, Inc.

5.1.15. The Simply Good Foods Company

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Product Portfolio, R&D Investments, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

Global Nutritional Drinks Market Regulatory Framework

6.1. Food Safety Standards (FSSAI, FDA, EFSA)

6.2. Labeling Guidelines

6.3. Certification Requirements (Organic, Non-GMO, Gluten-Free)

6.4. Compliance with International Export/Import Regulations

Global Nutritional Drinks Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

Global Nutritional Drinks Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Age Group (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Packaging Type (In Value %)

8.5. By Region (In Value %)

Global Nutritional Drinks Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, an ecosystem map of the global nutritional drinks market is constructed, identifying all major stakeholders, including manufacturers, distributors, and consumers. This is achieved through extensive secondary research using proprietary databases to define critical market dynamics.

Step 2: Market Analysis and Construction

The next phase involves analyzing historical data on market penetration, consumer demand, and revenue generation across different segments. This data will be evaluated to ensure accuracy in estimating market shares and consumer preferences.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are tested through in-depth interviews with key industry experts, including representatives from major nutritional drinks companies. These consultations offer insights into market challenges and growth drivers.

Step 4: Research Synthesis and Final Output

In the final stage, direct interaction with leading nutritional drink manufacturers ensures comprehensive validation of the findings, culminating in a detailed, reliable, and data-backed market report.

Frequently Asked Questions

01. How big is the Global Nutritional Drinks Market?

The global nutritional drinks market is valued at USD 11 billion, driven by the increasing demand for health and wellness products, alongside the rising trend of functional beverages that provide essential nutrients.

02. What are the challenges in the Global Nutritional Drinks Market?

Challenges in the market include high competition among brands, regulatory restrictions regarding health claims, and price fluctuations of key ingredients like dairy and plant-based proteins.

03. Who are the major players in the Global Nutritional Drinks Market?

Major players in the global nutritional drinks market include Abbott Laboratories, Nestl S.A., The Kraft Heinz Company, Danone S.A., and Glanbia Plc, all of whom hold strong positions due to their global presence and product innovations.

04. What are the growth drivers of the Global Nutritional Drinks Market?

Key growth drivers include increasing health consciousness among consumers, rising demand for meal replacement drinks, and innovations in plant-based and protein-enriched beverages. These factors are further supported by the aging population's growing nutritional needs.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.