Global Particle Board Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD4728

Region:Global

Author(s):Mukul

Product Code:KROD4728

December 2024

112

The Global Particle Board market is consolidated, with a few major players holding substantial market shares. Key players operate extensive manufacturing facilities, utilize advanced production technologies, and have strong distribution networks. This consolidation gives these companies a competitive edge in terms of price competitiveness and innovation. Companies such as Kronospan, Egger Group, and Arauco dominate the market through their wide product portfolios and significant geographical reach.

|

Company |

Establishment Year |

Headquarters |

R&D Investments |

Key Technology |

Strategic Partnerships |

Product Portfolio |

Geographic Reach |

Production Scale |

|

Kronospan |

1897 |

Austria |

- |

- |

- |

- |

- |

- |

|

Egger Group |

1961 |

Austria |

- |

- |

- |

- |

- |

- |

|

Arauco |

1970 |

Chile |

- |

- |

- |

- |

- |

- |

|

Georgia-Pacific |

1927 |

United States |

- |

- |

- |

- |

- |

- |

|

West Fraser Timber |

1955 |

Canada |

- |

- |

- |

- |

- |

- |

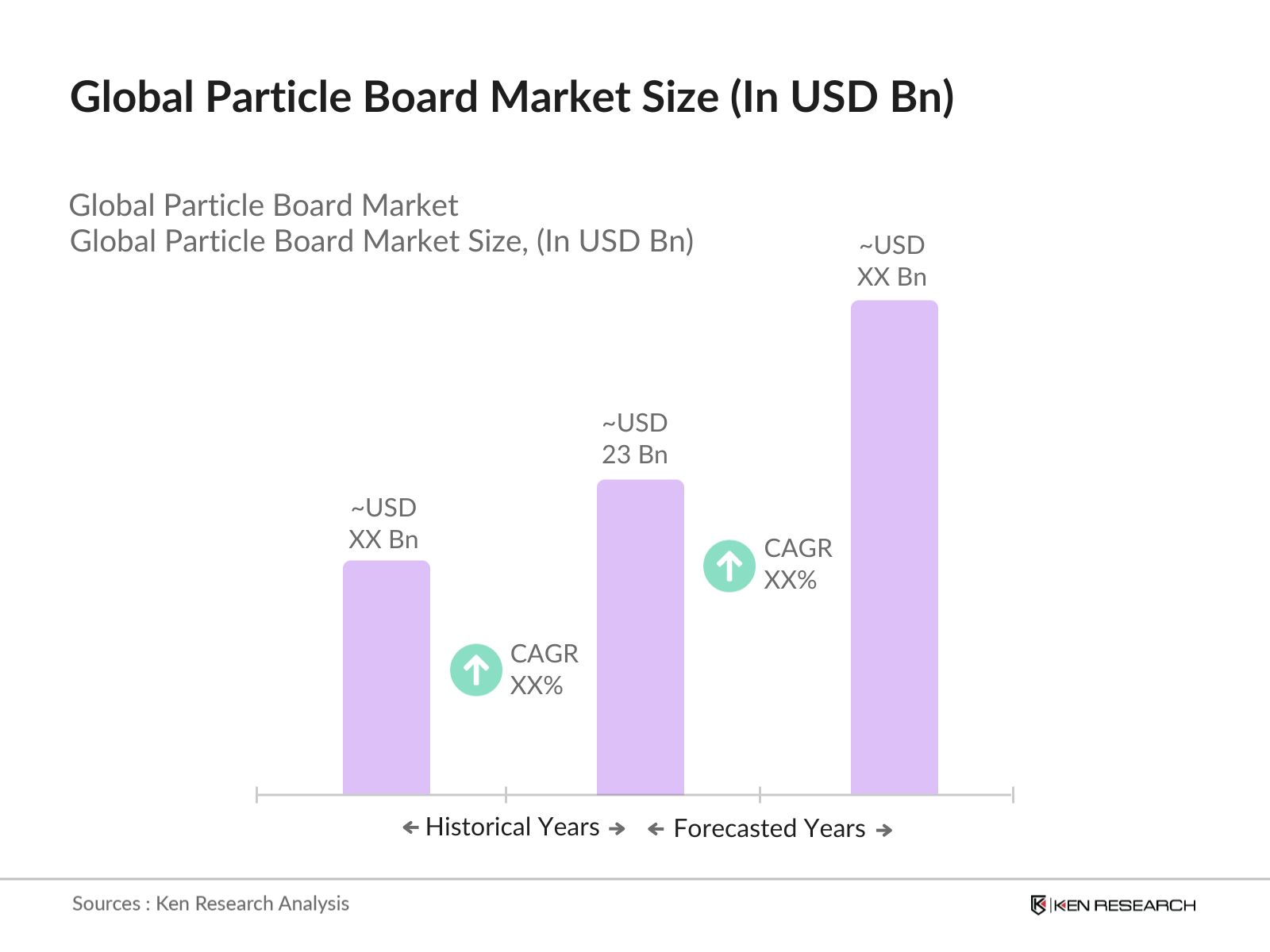

Over the next five years, the Global Particle Board market is expected to experience significant growth, driven by increasing urbanization and construction activities, especially in emerging markets. The rise of modular and affordable furniture, coupled with technological advancements in particle board manufacturing, will further enhance market demand. Sustainable practices, such as the use of recycled wood materials, will also play a critical role in shaping the future of the particle board industry. The integration of lightweight and fire-resistant particle boards into high-performance applications is anticipated to open new avenues for market expansion.

|

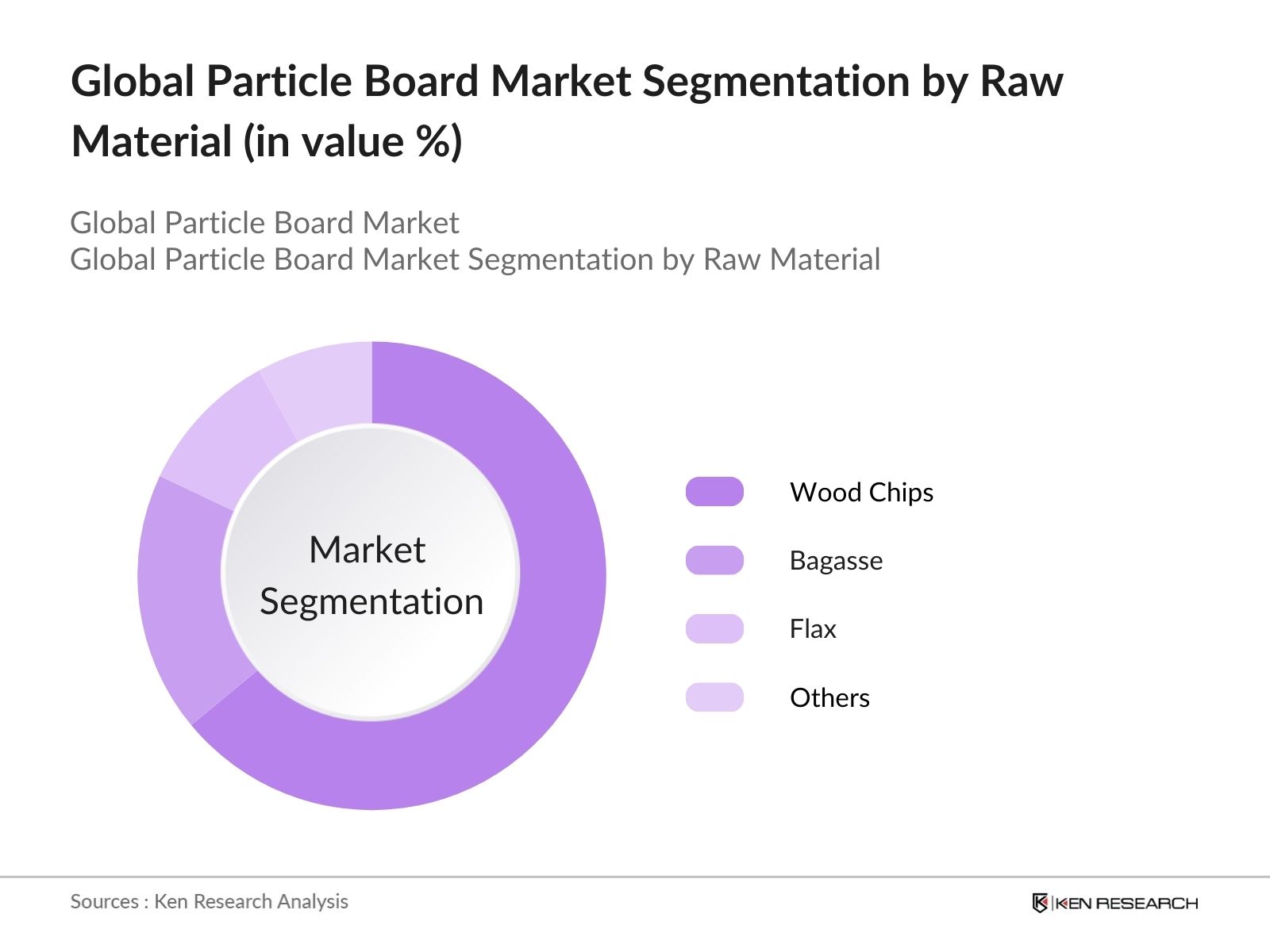

Raw Material |

Wood Chips Bagasse Flax Others |

|

Application |

Furniture Manufacturing Construction Packaging Others |

|

Product Type |

Standard Particle Board Fire-Resistant Particle Board Moisture-Resistant Particle Board |

|

Thickness |

Less than 15mm 15-20mm Above 20mm |

|

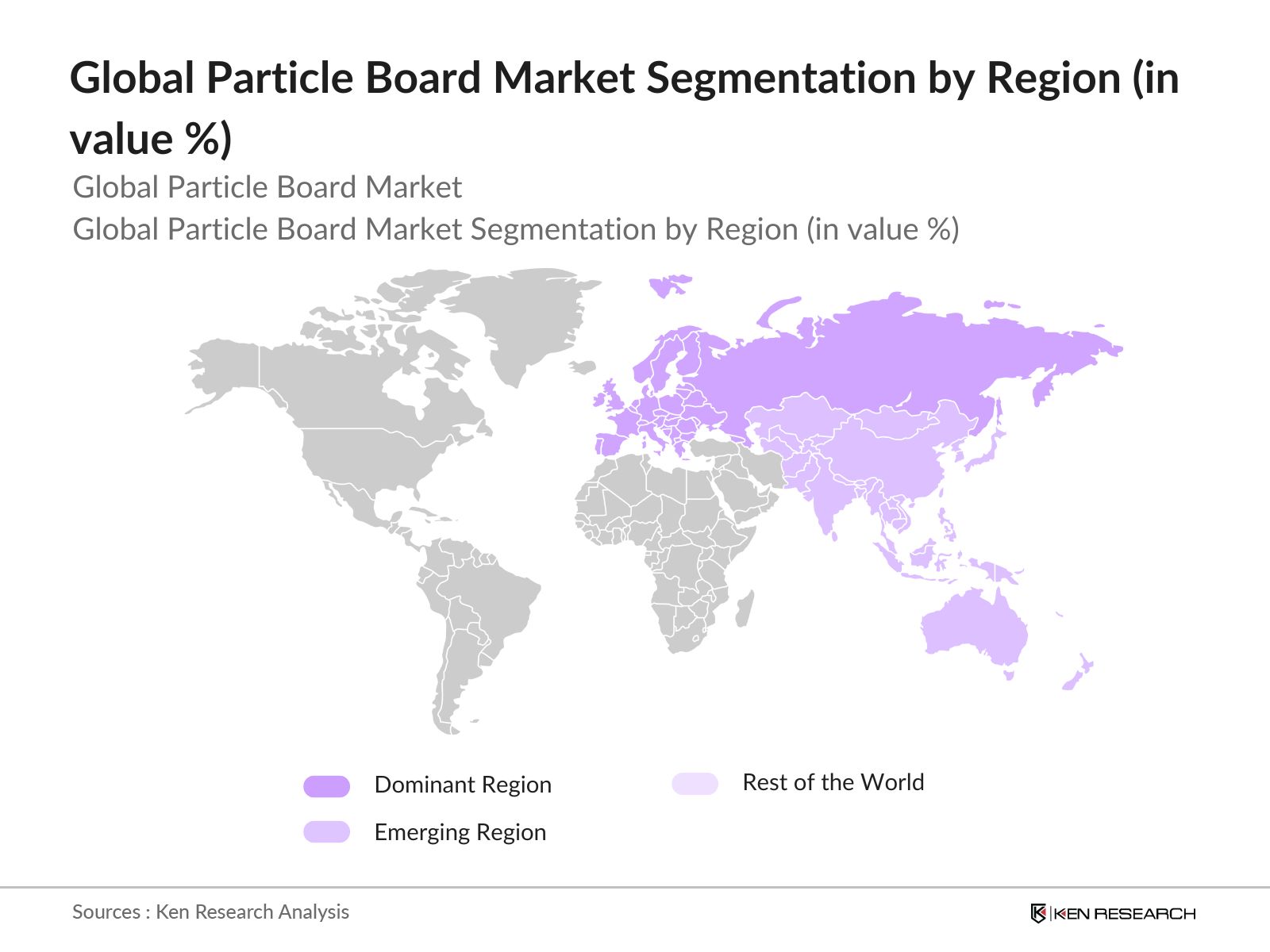

Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1 Definition and Scope

1.2 Market Taxonomy (By Raw Material, Application, Region)

1.3 Market Growth Rate (Global, Regional)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis (Capacity Utilization, Global Production Volume)

2.3 Key Market Developments and Milestones (Technological Advancements, Production Methods)

3.1 Growth Drivers

3.1.1 Increasing Demand in Furniture Industry

3.1.2 Rising Construction Activities

3.1.3 Cost-Efficiency of Particle Board (compared to Plywood, MDF)

3.1.4 Sustainable and Eco-Friendly Manufacturing Practices

3.2 Market Challenges

3.2.1 Volatility in Raw Material Prices (Wood Chips, Adhesives)

3.2.2 Competition from Alternatives (MDF, Plywood)

3.2.3 Lack of Skilled Workforce in Emerging Economies

3.3 Opportunities

3.3.1 Growth in the Modular Furniture Segment

3.3.2 Adoption of Advanced Manufacturing Technologies

3.3.3 Expanding Applications in Packaging and Construction

3.4 Trends

3.4.1 Growing Use of Recycled Materials in Particle Board Production

3.4.2 Integration of Lightweight Particle Boards in Construction

3.4.3 Shift Towards Zero-Waste Manufacturing

3.5 Government Regulations

3.5.1 Wood-Based Panel Regulations (Emission Standards)

3.5.2 Forest Conservation Policies

3.5.3 Certifications (FSC, PEFC)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis (Raw Material Suppliers, Buyers, Substitutes, Competition)

3.9 Competition Ecosystem

4.1 By Raw Material (In Value and Volume %)

4.1.1 Wood Chips

4.1.2 Bagasse

4.1.3 Flax

4.1.4 Others

4.2 By Application (In Value and Volume %)

4.2.1 Furniture Manufacturing

4.2.2 Construction

4.2.3 Packaging

4.2.4 Others

4.3 By Product Type (In Value and Volume %)

4.3.1 Standard Particle Board

4.3.2 Fire-Resistant Particle Board

4.3.3 Moisture-Resistant Particle Board

4.4 By Thickness (In Value and Volume %)

4.4.1 Less than 15mm

4.4.2 15-20mm

4.4.3 Above 20mm

4.5 By Region (In Value and Volume %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Middle East & Africa

4.5.5 Latin America

5.1 Detailed Profiles of Major Competitors

5.1.1 Kronospan

5.1.2 Egger Group

5.1.3 Arauco

5.1.4 Georgia-Pacific

5.1.5 Boise Cascade

5.1.6 Roseburg Forest Products

5.1.7 Greenpanel Industries

5.1.8 Pfleiderer

5.1.9 Sonae Arauco

5.1.10 West Fraser Timber Co.

5.1.11 Swiss Krono

5.1.12 Norbord Inc.

5.1.13 Tolko Industries

5.1.14 Duratex

5.1.15 Uniboard

5.2 Cross Comparison Parameters (Market Share, Global Production Volume, Manufacturing Facilities, Supply Chain Strength, Technology Investments, Strategic Alliances, Distribution Network, Certifications)

5.3 Market Share Analysis (Region-wise, Application-wise)

5.4 Strategic Initiatives (Mergers & Acquisitions, Joint Ventures, Partnerships)

5.5 Investment Analysis (New Manufacturing Plants, Expansion Plans)

5.6 Venture Capital Funding and Private Equity Investments

6.1 Environmental Standards and Emission Regulations (Formaldehyde Emission Limits)

6.2 Certification Processes (FSC, PEFC Certifications)

6.3 Health and Safety Standards

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Urbanization, Green Building Initiatives)

8.1 By Raw Material (In Value %)

8.2 By Application (In Value %)

8.3 By Product Type (In Value %)

8.4 By Thickness (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 White Space Opportunity Analysis

9.3 Customer Cohort Analysis

9.4 Go-to-Market Strategies (Distribution Channels, Partner Ecosystems)

Disclaimer Contact Us

This initial phase involves the identification and analysis of key variables, including raw material supply chain dynamics, production technologies, and consumer demand trends in the Global Particle Board Market. Extensive secondary research from government databases, industry journals, and proprietary databases was conducted to understand the ecosystem.

The second phase focused on analyzing historical data on production capacity, regional market penetration, and consumption patterns. The market construction was built using a bottom-up approach, examining individual company performance and aggregating market data to generate reliable revenue estimates.

In this step, interviews were conducted with key market players, including manufacturers and distributors, to validate the initial market assumptions. These insights were used to refine the market forecast and adjust for market-specific variables.

The final phase involved synthesizing the collected data and producing a comprehensive report. Statistical validation and forecasting models were applied to ensure data accuracy. The final output provides an in-depth analysis of the Global Particle Board Market, covering market size, trends, and competitive landscape.

The Global Particle Board Market is valued at USD 23 billion based on a five-year historical analysis, driven by rising demand in the furniture manufacturing and construction industries.

Challenges in the market include volatility in raw material prices, competition from alternative products like MDF and plywood, and environmental regulations around deforestation and wood usage.

Major players in the market include Kronospan, Egger Group, Arauco, Georgia-Pacific, and West Fraser Timber. These companies dominate due to their technological advancements, extensive distribution networks, and strategic alliances.

Growth in the market is driven by the increasing use of particle boards in affordable furniture, rising construction activities, and the growing trend towards sustainable and eco-friendly building materials.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.