Global Photovoltaics Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11119

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11119

December 2024

83

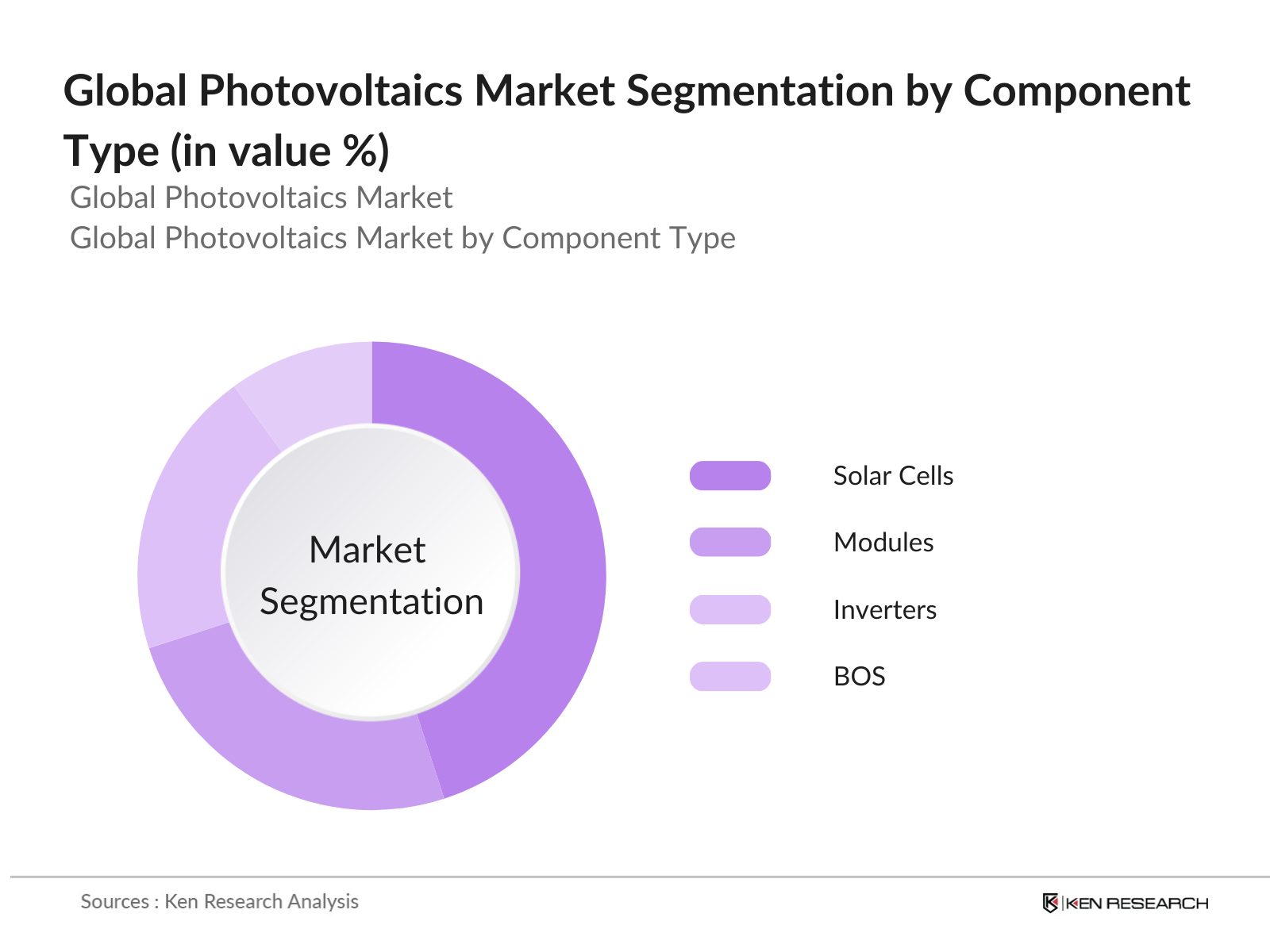

By Component Type: The global photovoltaics market is segmented by component type into solar cells, modules, inverters, and balance of systems (BOS). Solar cells dominate this segment due to continuous technological innovations that have improved energy conversion efficiency, making solar energy more accessible and cost-effective. Additionally, the rising demand for high-performance solar cells, such as those incorporating monocrystalline and polycrystalline technologies, is driving this segment's growth.

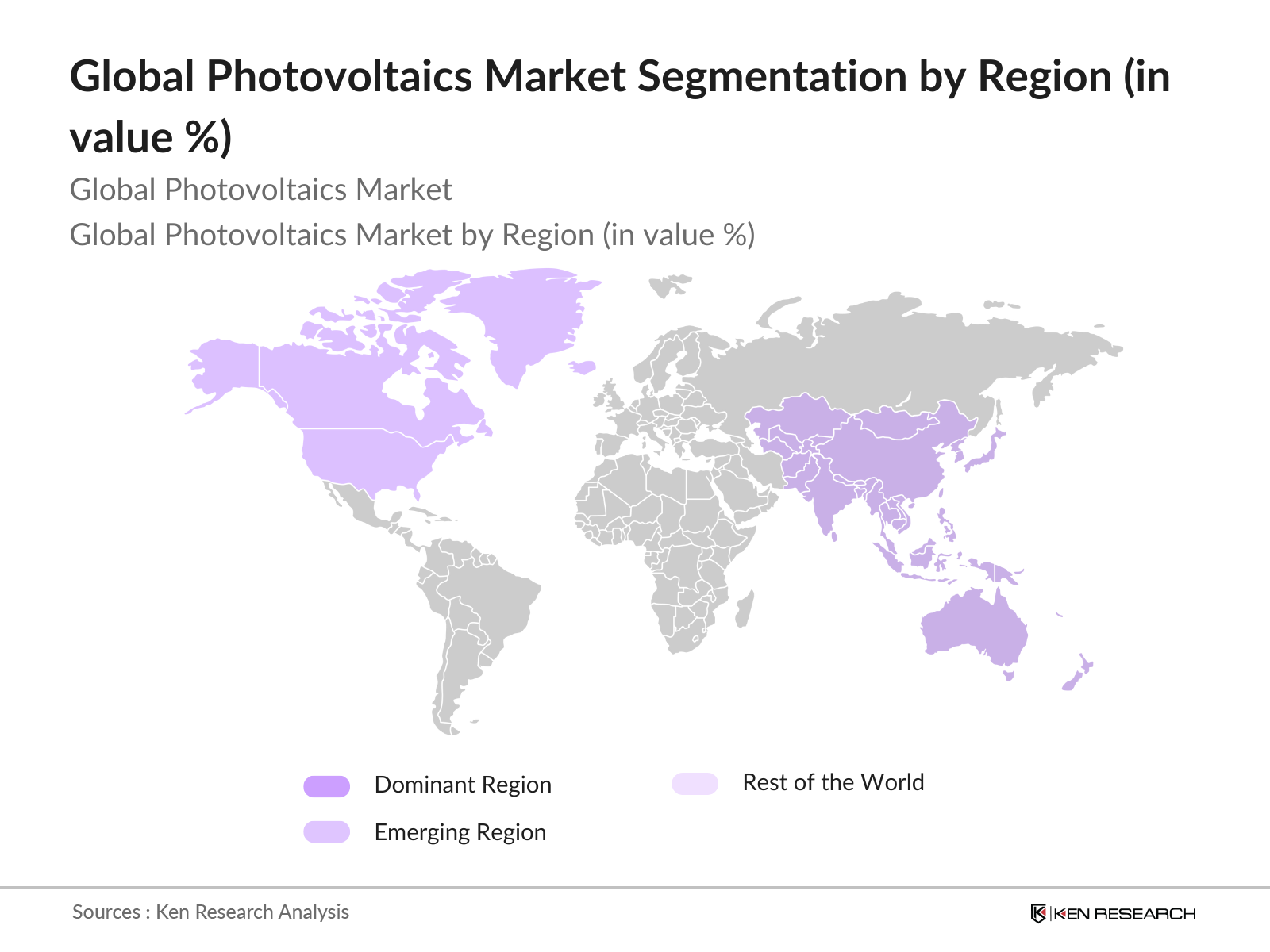

By Region: The global photovoltaics market is segmented by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. Asia-Pacific leads the global photovoltaics market due to the significant presence of key players in the region, especially in China, which is the largest manufacturer and consumer of solar energy. Government-backed initiatives and lower production costs further drive Asia-Pacifics dominance in the global market.

The global photovoltaics market is dominated by a few major players, which include both local and international companies. Chinas manufacturing giants play a significant role, while international corporations from the U.S. and Europe contribute through innovation and technology advancements. This consolidation highlights the significant influence of these key companies in shaping the global market landscape.

|

Company Name |

Established Year |

Headquarters |

Installed Capacity |

Revenue (USD Bn) |

Global Market Penetration |

Solar Efficiency Rate |

R&D Investments (USD Mn) |

Government Contracts |

Production Plants |

|

First Solar, Inc. |

1999 |

Arizona, USA |

|||||||

|

Jinko Solar Holdings Co., Ltd. |

2006 |

Shanghai, China |

|||||||

|

Canadian Solar Inc. |

2001 |

Ontario, Canada |

|||||||

|

Trina Solar Limited |

1997 |

Jiangsu, China |

|||||||

|

SunPower Corporation |

1985 |

California, USA |

Market Growth Drivers

Market Challenges

The global photovoltaics market is expected to continue its growth trajectory, driven by advancements in solar energy technology, increasing energy demand, and continuous government support. Significant growth is anticipated due to innovations in solar panel efficiency, storage technologies, and the rising adoption of decentralized energy systems. Governments across the globe are increasingly prioritizing clean energy, which will further drive investments into the photovoltaic market. Additionally, increased efforts to reduce the cost of solar energy will contribute to its widespread adoption.

Market Opportunities:

|

By Component |

Solar Cells Modules Inverters Balance of Systems (BOS) |

|

By Installation |

Residential Commercial Utility-Scale |

|

By Application |

Grid-Connected PV Systems Off-Grid PV Systems Hybrid PV Systems |

|

By Material |

Crystalline Silicon Thin Film Organic PV |

|

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Market-Specific Parameters)

3.1.1. Increasing Adoption of Renewable Energy

3.1.2. Government Subsidies and Incentives

3.1.3. Technological Advancements in Solar Panel Efficiency

3.1.4. Expansion of Distributed Energy Resources (DER)

3.2. Market Challenges (Market-Specific Parameters)

3.2.1. High Initial Investment Costs

3.2.2. Supply Chain Disruptions in Key Raw Materials

3.2.3. Energy Storage and Grid Integration Issues

3.3. Opportunities (Market-Specific Parameters)

3.3.1. Expansion into Emerging Markets

3.3.2. Integration of Photovoltaics with Smart Grids

3.3.3. Development of Floating Solar Farms

3.4. Trends (Market-Specific Parameters)

3.4.1. Adoption of Bifacial Solar Panels

3.4.2. Increasing Use of Artificial Intelligence for Solar Performance Optimization

3.4.3. Rise of Solar PPA (Power Purchase Agreement) Contracts

3.5. Government Regulation (Market-Specific Parameters)

3.5.1. National Solar Missions and Roadmaps

3.5.2. International Commitments to Carbon Neutrality

3.5.3. Financial Support for Solar Energy Projects

3.5.4. Grid Integration Policies for Renewable Energy

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Component Type (In Value %)

4.1.1. Solar Cells

4.1.2. Modules

4.1.3. Inverters

4.1.4. Balance of Systems (BOS)

4.2. By Installation Type (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Utility-Scale

4.3. By Application (In Value %)

4.3.1. Grid-Connected PV Systems

4.3.2. Off-Grid PV Systems

4.3.3. Hybrid PV Systems

4.4. By Material Type (In Value %)

4.4.1. Crystalline Silicon

4.4.2. Thin Film

4.4.3. Organic PV

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. First Solar, Inc.

5.1.2. SunPower Corporation

5.1.3. Canadian Solar Inc.

5.1.4. Jinko Solar Holdings Co., Ltd.

5.1.5. Trina Solar Limited

5.1.6. LONGi Solar

5.1.7. Tesla, Inc. (SolarCity)

5.1.8. Hanwha Q Cells

5.1.9. JA Solar Technology Co., Ltd.

5.1.10. Enphase Energy, Inc.

5.1.11. ABB Ltd.

5.1.12. SMA Solar Technology AG

5.1.13. Risen Energy Co., Ltd.

5.1.14. GCL-Poly Energy Holdings Limited

5.1.15. Yingli Green Energy Holding Company Limited

5.2. Cross Comparison Parameters (Market-Specific: Installed Capacity, Revenue, Solar Efficiency Rate, Global Market Penetration, Headquarters, Founding Year, Renewable Energy Initiatives, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Energy Efficiency Standards

6.2. Solar Certification Processes

6.3. Renewable Energy Compliance Requirements

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Component Type (In Value %)

8.2. By Installation Type (In Value %)

8.3. By Application (In Value %)

8.4. By Material Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsIn the initial phase, we mapped out the ecosystem of stakeholders within the global photovoltaics market. Extensive desk research was carried out using secondary databases to gather industry-level insights. This step was critical to identify the key variables affecting market dynamics, including regulatory policies, technological advancements, and market drivers.

The next phase involved gathering and analyzing historical data related to market penetration, installed capacity, and revenue generation. This analysis covered various segments, including residential, commercial, and utility-scale installations, providing a holistic view of the market.

Market hypotheses were constructed and validated through interviews with industry experts. These consultations provided operational insights that contributed to refining and corroborating the market estimates.

In the final phase, engagement with photovoltaic manufacturers and energy providers helped obtain detailed insights into product segments, sales performance, and consumer trends. This step ensured the data's reliability and completeness, leading to an accurate market analysis.

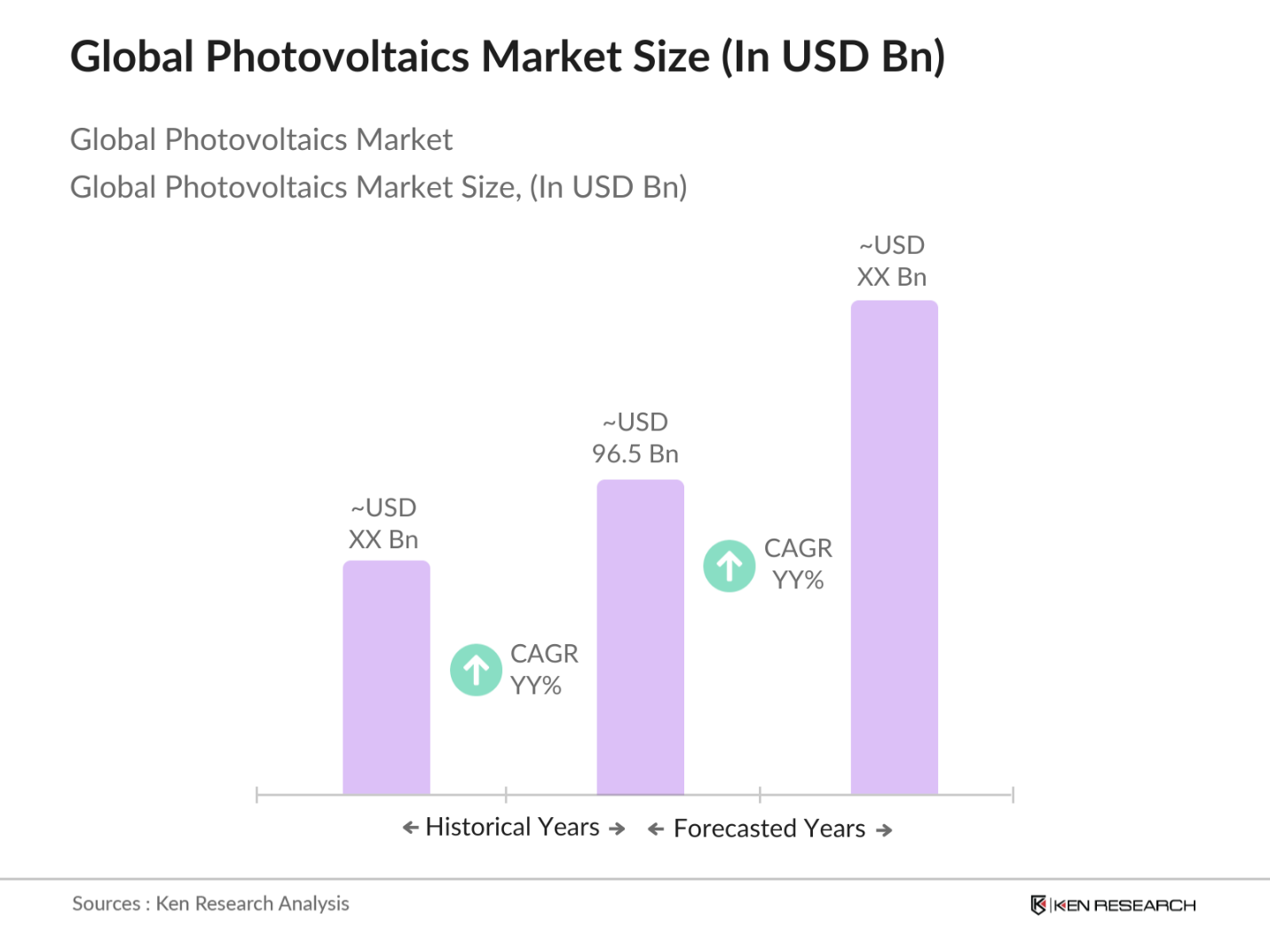

The global photovoltaics market was valued at USD 96.5 billion, It is driven by technological advancements, government incentives, and increasing energy demand across residential, commercial, and utility sectors.

Key challenges include high initial investment costs, supply chain disruptions, and technical difficulties related to energy storage and grid integration. These issues have created barriers for widespread adoption, especially in developing regions.

Major players include First Solar, SunPower Corporation, Canadian Solar, Jinko Solar, and Trina Solar. These companies dominate due to their large production capacities, technological innovations, and strong government contracts.

The market is driven by increasing global demand for clean energy, advancements in solar technologies, government-backed renewable energy policies, and financial support for large-scale solar projects.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.