Global Pipeline and Process Services Market Outlook to 2030

Region:Global

Author(s):Mukul Soni

Product Code:KROD10830

December 2024

89

About the Report

Global Pipeline and Process Services Market Overview

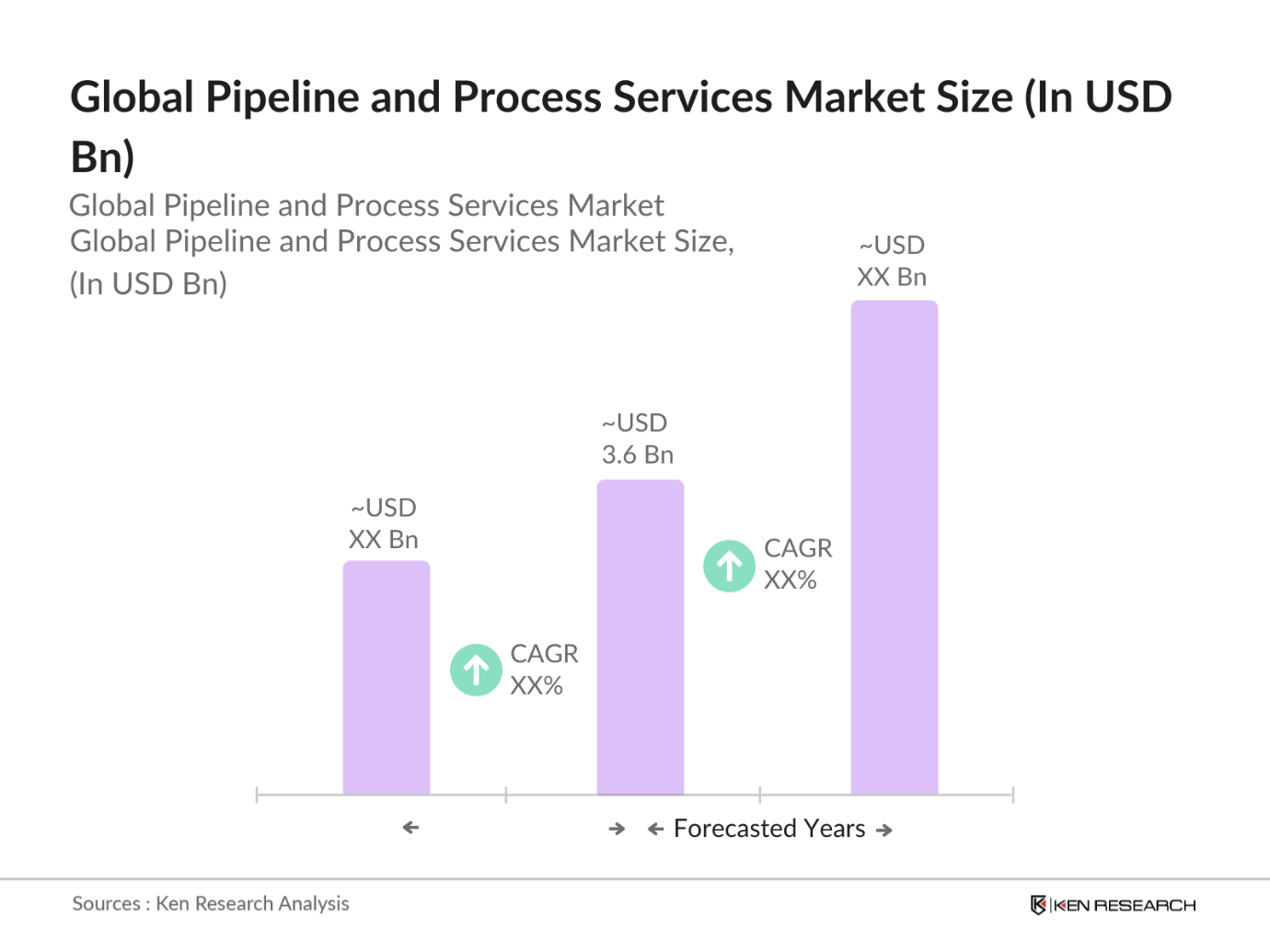

- The Global Pipeline and Process Services Market is valued at USD 3.6 billion, based on a comprehensive five-year historical analysis. The markets growth is largely driven by the robust expansion of the oil and gas industry, particularly in North America and the Middle East. Infrastructure investment in high-demand regions and advancements in pipeline technology, such as intelligent pigging and automated leak detection, also fuel growth as companies prioritize pipeline safety and maintenance.

- North America and the Middle East dominate the market due to their expansive oil and gas infrastructure and regulatory requirements mandating pipeline inspection and safety. North America leads in technological innovations for pipeline integrity management, while the Middle East leverages high-output oilfields, requiring consistent pipeline servicing to maintain production efficiency. Both regions benefit from significant government backing, enhancing their market position.

- Emission reduction standards set by global regulatory agencies are influencing pipeline operations. The European Unions Green Deal, which mandates a reduction in carbon emissions by 55% by 2030, is pushing companies to adopt sustainable practices in pipeline construction and maintenance. In response, operators are investing in emission control systems, with over 2,000 new systems implemented on existing pipelines in Europe alone in 2023, according to the European Commission.

Global Pipeline and Process Services Market Segmentation

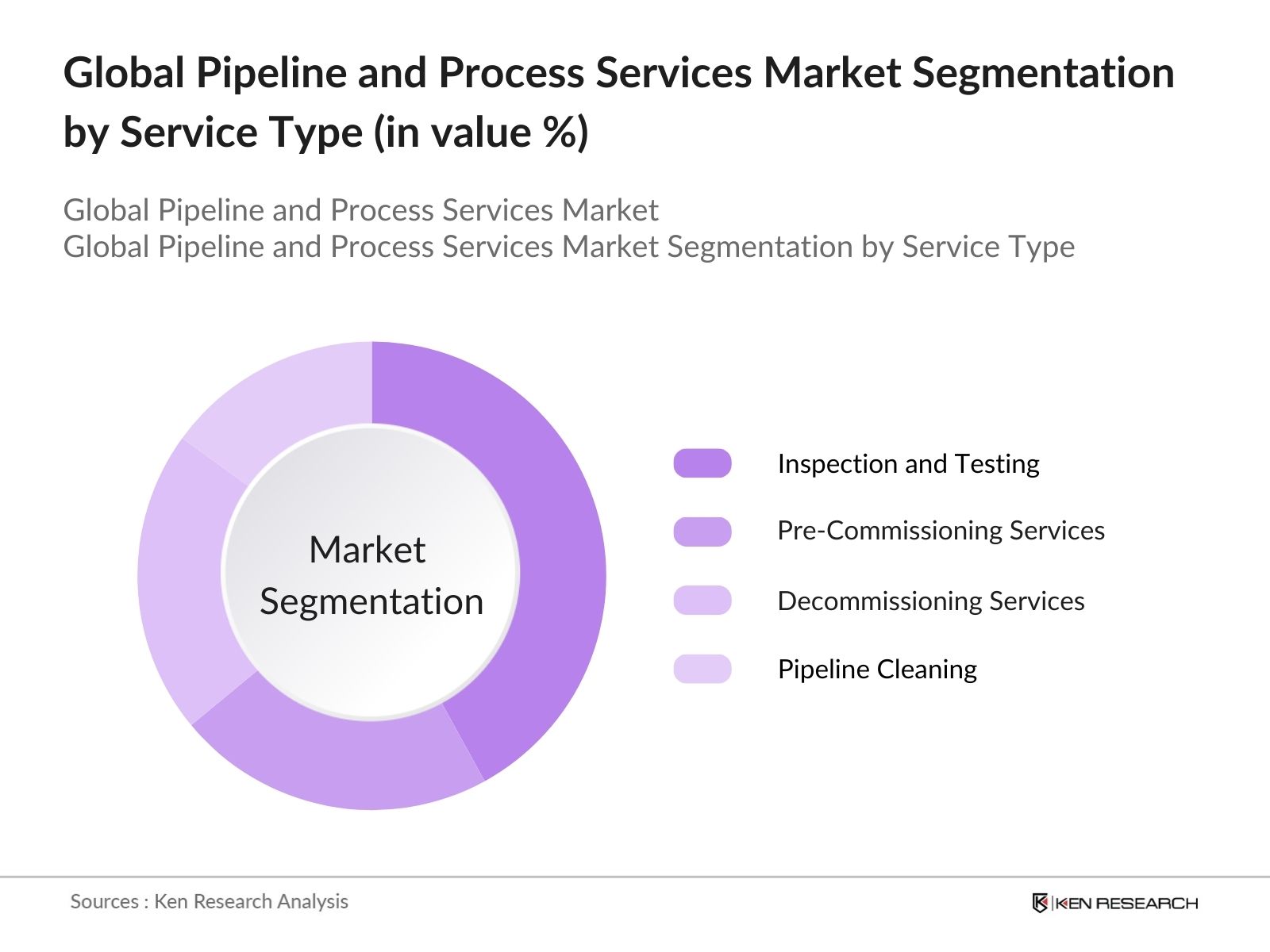

By Service Type: The market is segmented by service type into pre-commissioning services, pipeline cleaning, inspection and testing, and decommissioning services. Currently, inspection and testing hold the dominant share within service type segmentation due to the increasing demand for safety and regulatory compliance in pipelines. Inspection services are vital in identifying potential hazards, ensuring uninterrupted oil and gas transport.

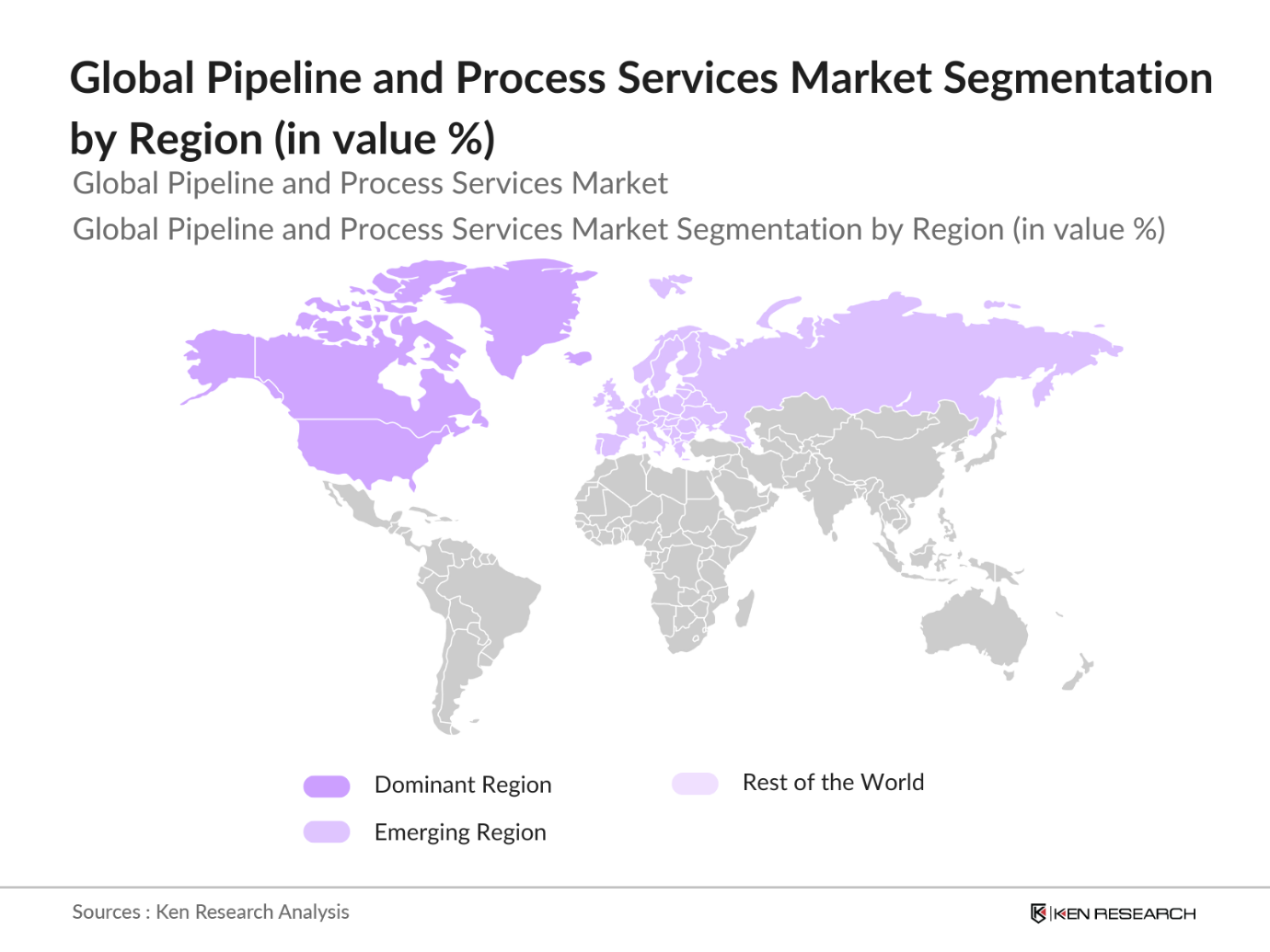

By Region: The market by region includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America. North America leads with its extensive pipeline network and stringent regulatory oversight, which drives demand for services focused on integrity management and environmental compliance.

By Application: Segmented by application, the market covers offshore pipelines, onshore pipelines, downstream facilities, and midstream facilities. Offshore pipelines currently dominate due to the complex servicing requirements in harsh marine environments, necessitating advanced maintenance techniques and technologies.

Global Pipeline and Process Services Market Competitive Landscape

The global pipeline and process services market is dominated by several key players, with Halliburton, Schlumberger, and Baker Hughes at the forefront due to their comprehensive service offerings and advanced technology. The market remains competitive, focusing on technological advancement and service diversification to address complex operational challenges.

Global Pipeline and Process Services Industry Analysis

Growth Drivers

- Expansion of Oil & Gas Infrastructure: The expansion of oil and gas infrastructure is a major growth driver in the Global Pipeline and Process Services Market. According to data from the U.S. Energy Information Administration, global energy demand is projected to rise to nearly 665 quadrillion British thermal units (BTUs) by 2024, prompting investments in pipeline infrastructure to sustain energy transport demands. Additionally, increased energy production, especially in the U.S. and the Middle East, requires enhanced infrastructure for transporting crude oil and natural gas.

- Regulatory Compliance and Environmental Safety: Increased focus on environmental regulations and safety measures is spurring investments in pipeline infrastructure improvements. The Environmental Protection Agency (EPA) mandates strict guidelines for pipeline emissions and safety, with standards such as the Clean Air Act directing operators to adopt environmentally safe practices. Pipeline operators in the U.S. and EU are now integrating advanced environmental safety solutions to comply with these standards. In 2023, over 50,000 miles of pipeline were subject to stricter regulatory compliance checks in the U.S., with further expansion expected in 2024.

- Adoption of Smart Technologies in Operations: Smart technology integration has become critical for enhancing pipeline monitoring and efficiency. Technologies like AI-based sensors and data analytics are transforming operations, helping companies detect leaks and maintain optimal pipeline conditions. For instance, the global adoption rate of digital sensors has increased, with over 15 million new sensors expected to be deployed on oil and gas pipelines in 2024, as noted by the International Energy Agency (IEA). This technological push is being driven by the need for safety and efficiency in resource extraction and transportation.

Market Restraints

- Risk Management in High-Pressure Pipelines: Managing risks in high-pressure pipelines remains a significant challenge due to potential hazards and operational difficulties. Data from the U.S. Department of Transportations Pipeline and Hazardous Materials Safety Administration (PHMSA) indicated over 1,300 incidents of leaks in high-pressure oil and gas pipelines in 2023, emphasizing the need for stronger risk management frameworks. The incidents resulted in substantial financial and environmental impacts, prompting regulatory bodies to implement stricter operational standards to mitigate risks associated with pipeline pressure management.

- Limited Access to Specialized Equipment: Access to specialized equipment necessary for pipeline construction and maintenance is limited, especially in remote regions. In 2023, the global equipment availability for pipeline services was estimated to cover only about 60% of demand in certain emerging markets, as reported by the International Energy Agency (IEA). The constrained access results in delayed project timelines, particularly in regions with underdeveloped infrastructure, impacting the pace of expansion for critical energy supply lines.

Global Pipeline and Process Services Market Future Outlook

The Global Pipeline and Process Services Market is expected to grow significantly over the coming years. This growth is anticipated due to increasing investments in oil and gas infrastructure, enhanced regulatory focus on environmental safety, and technological advancements in pipeline integrity management. Additionally, emerging economies in the Asia Pacific region are projected to boost demand as they expand their pipeline networks for improved energy distribution.

Market Opportunities

- Digital Pipeline Management Solutions: The adoption of digital solutions for pipeline management offers a significant opportunity for market growth. With the global Internet of Things (IoT) market value projected to reach nearly USD 1 trillion by 2024, IoT technologies are increasingly applied to real-time pipeline monitoring, leak detection, and predictive maintenance. Digital transformation has enabled pipeline operators to reduce operational risks and streamline processes, with a noted reduction in unscheduled maintenance events by nearly 15% in IoT-enabled systems in 2023.

- Investment in Process Improvement: Investments in process improvements, including enhanced pipeline integrity assessments and optimized flow management, provide considerable growth prospects. As of 2023, over USD 15 billion was invested globally in upgrading pipeline integrity systems, according to data from the World Bank. These improvements address both operational efficiency and compliance with stricter environmental standards, providing a dual benefit of increased safety and cost reduction.

Scope of the Report

|

Service Type |

Pre-Commissioning Services Pipeline Cleaning Inspection and Testing Services Decommissioning Services |

|

Application |

Offshore Pipelines Onshore Pipelines Downstream Facilities Midstream Facilities |

|

End-Use Sector |

Oil & Gas Industry Chemical Sector Water & Wastewater Industry Power Generation |

|

Technology Type |

Intelligent Pigging Magnetic Flux Leakage Ultrasonic Testing Pipeline Leak Detection |

|

Region |

North America Europe Asia Pacific Middle East and Africa Latin America |

Products

Key Target Audience

Investor and venture capitalist firms

Government and regulatory bodies (e.g., Environmental Protection Agency, U.S. Department of Energy)

Pipeline operators

Oil and gas companies

Infrastructure development firms

Pipeline inspection and safety equipment manufacturers

Environmental safety organizations

Technology providers for pipeline management solutions

Companies

Players Mentioned in the Report:

Halliburton

Schlumberger

Baker Hughes

TechnipFMC

Aegion Corporation

IKM Group

EnerMech

Altus Intervention

Bluefin Services

SGS SA

Stork

TDW Services Inc.

Hydratight Limited

Onstream Pipeline Inspection Services Inc.

NDT Global

Table of Contents

1. Global Pipeline and Process Services Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Global Pipeline and Process Services Market Size (in USD Million)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Global Pipeline and Process Services Market Analysis

3.1 Growth Drivers (Pipeline Development Rate, Offshore Drilling Advancements, Technological Innovations)

3.1.1 Expansion of Oil & Gas Infrastructure

3.1.2 Regulatory Compliance and Environmental Safety

3.1.3 Adoption of Smart Technologies in Operations

3.2 Market Challenges (Operational Hazards, Infrastructure Deficiencies, Skilled Labor Shortage)

3.2.1 Risk Management in High-Pressure Pipelines

3.2.2 Limited Access to Specialized Equipment

3.3 Opportunities (Digitalization, Strategic Collaborations, Emerging Markets)

3.3.1 Digital Pipeline Management Solutions

3.3.2 Investment in Process Improvement

3.4 Trends (Artificial Intelligence Integration, Predictive Maintenance, 3D Imaging Technologies)

3.4.1 Automation of Pipeline Monitoring

3.4.2 Expansion into Digital Twin Technologies

3.5 Regulatory Landscape (Environmental Standards, Compliance Requirements, Certification Processes)

3.5.1 Emission Reduction Standards

3.5.2 Pipeline Safety and Inspection Policies

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces

3.9 Competitive Landscape

4. Global Pipeline and Process Services Market Segmentation

4.1 By Service Type (in Value %)

4.1.1 Pre-Commissioning Services

4.1.2 Pipeline Cleaning

4.1.3 Inspection and Testing Services

4.1.4 Decommissioning Services

4.2 By Application (in Value %)

4.2.1 Offshore Pipelines

4.2.2 Onshore Pipelines

4.2.3 Downstream Facilities

4.2.4 Midstream Facilities

4.3 By End-Use Sector (in Value %)

4.3.1 Oil & Gas Industry

4.3.2 Chemical Sector

4.3.3 Water & Wastewater Industry

4.3.4 Power Generation

4.4 By Technology Type (in Value %)

4.4.1 Intelligent Pigging

4.4.2 Magnetic Flux Leakage

4.4.3 Ultrasonic Testing

4.4.4 Pipeline Leak Detection

4.5 By Region (in Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia Pacific

4.5.4 Middle East and Africa

4.5.5 Latin America

5. Global Pipeline and Process Services Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Halliburton

5.1.2 Schlumberger

5.1.3 Baker Hughes

5.1.4 TechnipFMC

5.1.5 Aegion Corporation

5.1.6 IKM Group

5.1.7 EnerMech

5.1.8 Altus Intervention

5.1.9 Bluefin Services

5.1.10 SGS SA

5.1.11 Stork

5.1.12 TDW Services Inc.

5.1.13 Hydratight Limited

5.1.14 Onstream Pipeline Inspection Services Inc.

5.1.15 NDT Global

5.2 Cross-Comparison Parameters (Headquarters Location, Establishment Year, Revenue, Workforce Strength, Market Presence, Regional Diversification, Core Services, Technology Innovation)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Incentives

5.8 Private Equity and Venture Funding

6. Global Pipeline and Process Services Market Regulatory Framework

6.1 Pipeline Construction Standards

6.2 Safety and Compliance Guidelines

6.3 Environmental Protection Mandates

7. Global Pipeline and Process Services Future Market Size (in USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Global Pipeline and Process Services Market Analysts Recommendations

8.1 TAM/SAM/SOM Analysis

8.2 Customer Cohort Analysis

8.3 Marketing Initiatives

8.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This initial phase focuses on mapping the ecosystem of the Global Pipeline and Process Services Market. This involves desk research and using proprietary databases to identify critical variables impacting market dynamics, including service types, application environments, and technology trends.

Step 2: Market Analysis and Construction

This step analyzes historical data on the market, including regional deployment trends, growth rates, and major service providers. By evaluating past trends, we establish a reliable model for understanding revenue generation and segment performance.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses are developed and validated through consultations with industry professionals via phone and email. This process ensures that market data aligns with industry insights, enhancing report accuracy.

Step 4: Research Synthesis and Final Output

In the final step, we engage with multiple service providers and technology vendors to validate the market segmentation, service adoption rates, and revenue data, ensuring that insights are comprehensive and data-backed.

Frequently Asked Questions

01. How big is the Global Pipeline and Process Services Market?

The Global Pipeline and Process Services Market is valued at USD 3.6 billion, driven by extensive infrastructure development and strict regulatory compliance demands.

02. What challenges does the Global Pipeline and Process Services Market face?

Key challenges include stringent environmental regulations, operational risks in harsh environments, and high maintenance costs, impacting the profitability of service providers.

03. Who are the major players in the Global Pipeline and Process Services Market?

Major players include Halliburton, Schlumberger, Baker Hughes, TechnipFMC, and Aegion Corporation, leading due to technological innovation and strong client networks.

04. What are the growth drivers of the Global Pipeline and Process Services Market?

The markets growth is propelled by rising energy demand, investments in oil and gas infrastructure, and advancements in pipeline inspection technologies, ensuring safe and efficient operations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.