Global Pipes Market Outlook to 2030

Region:Global

Author(s):Mukul Soni

Product Code:KROD10974

December 2024

95

About the Report

Global Pipes Market Overview

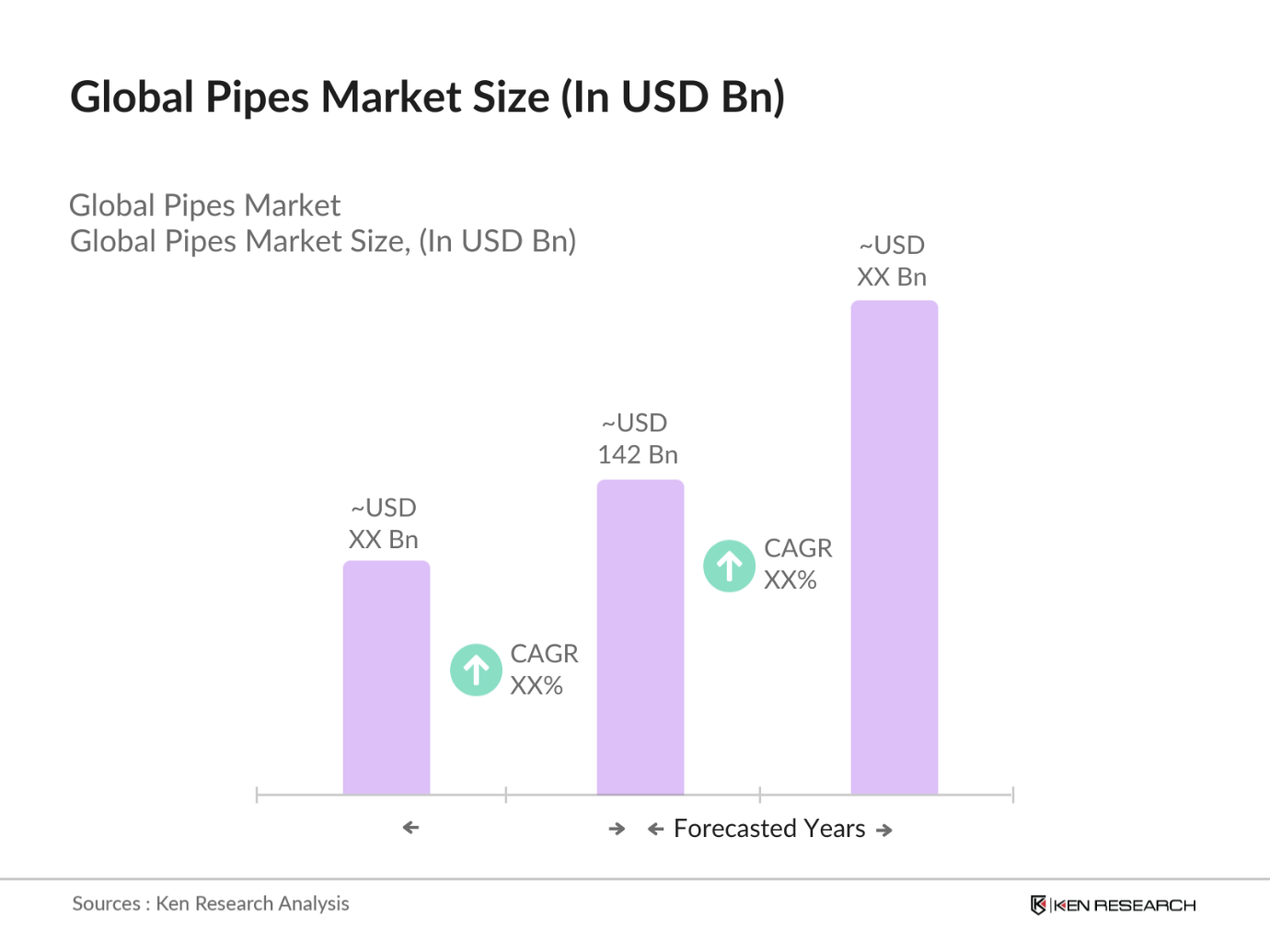

- The global pipes market, valued at USD 142 billion, based on a five-year historical analysis. The market is driven by the rising demand for robust infrastructure development in urban areas, increased use of pipes in oil and gas transmission, and the global emphasis on water management systems. Additionally, governments around the world are investing in the renewal of existing pipeline infrastructure, further driving the demand for various types of pipes.

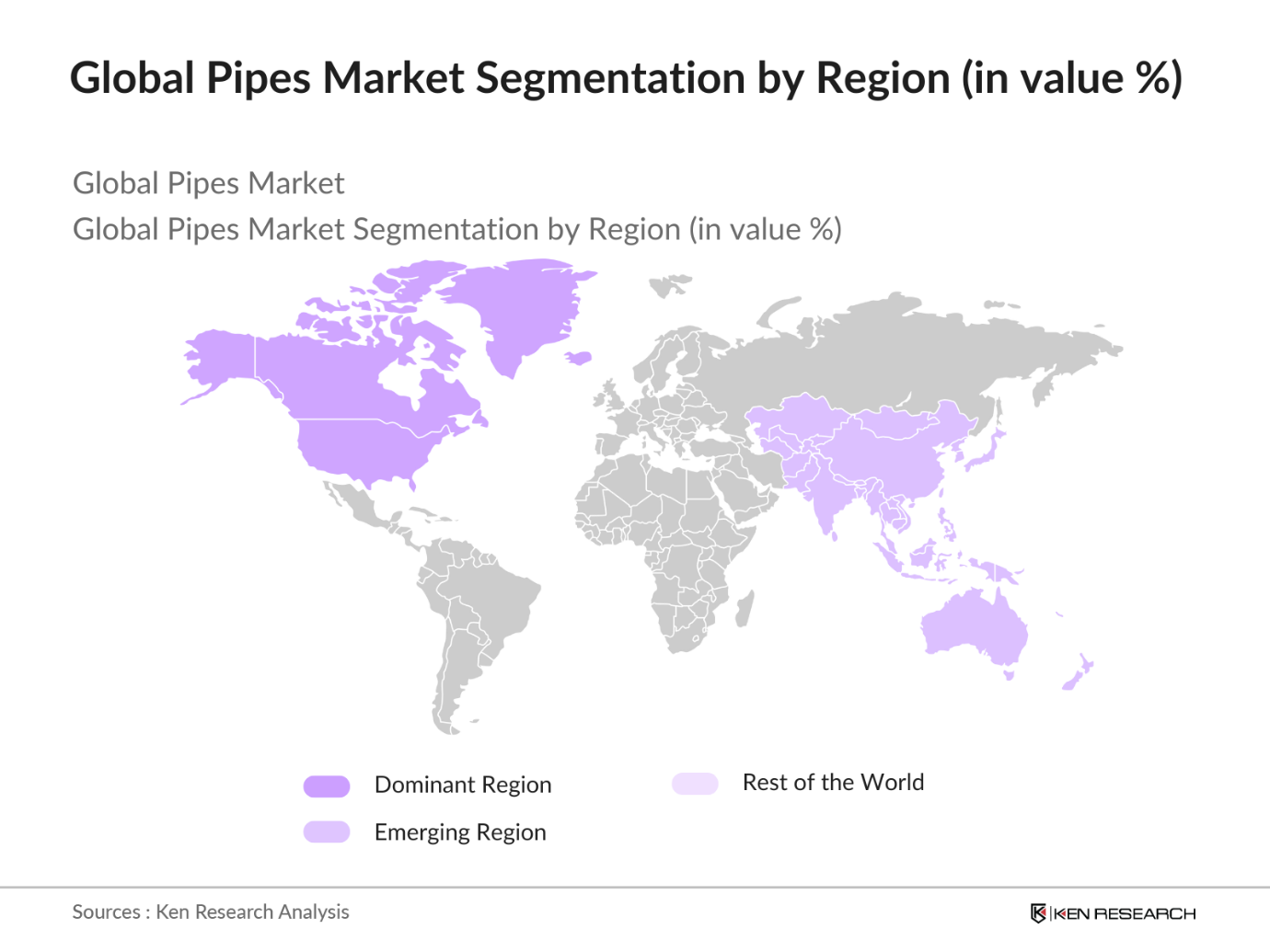

- The dominant regions in the pipes market include North America, Asia-Pacific, and Europe. North America leads due to the extensive oil and gas network, particularly in the United States, which accounts for large-scale pipeline projects. Meanwhile, Asia-Pacific, driven by rapid industrialization in countries like China and India, has become a key market player due to the rising need for improved water and wastewater management systems. Europe, with its growing environmental sustainability projects, also remains significant in the sector.

- Government safety regulations are becoming more stringent to ensure the durability and safety of pipelines. In 2022, the U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA) implemented new guidelines that increased material standards and pressure tolerance limits for pipelines over 2,000 kilometers long. These measures are designed to reduce the risk of accidents and ensure that pipelines can withstand extreme conditions. In the EU, similar regulations were adopted in 2023 to improve pipeline safety, with a particular focus on corrosion resistance and environmental safety

Global Pipes Market Segmentation

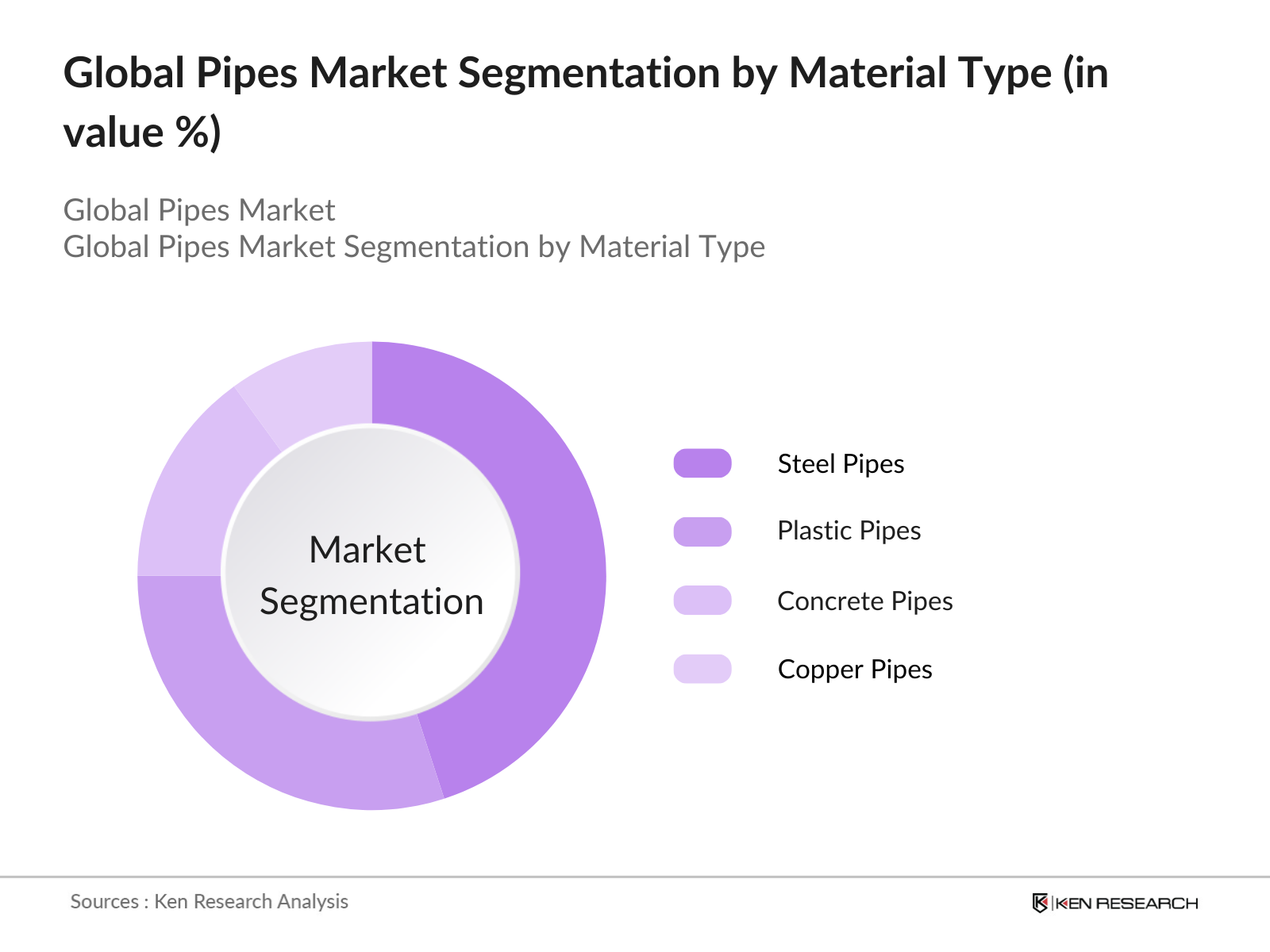

By Material Type: The global pipes market is segmented by material type into steel pipes, plastic pipes (PVC, CPVC, HDPE), concrete pipes, copper pipes, and cast iron pipes. Steel pipes dominate this segmentation due to their extensive application in industries such as oil and gas and construction. Their strength and durability make them the preferred choice for high-pressure applications, particularly in pipeline transportation for petroleum and natural gas. Additionally, the growing industrial infrastructure in emerging economies has boosted the demand for steel pipes.

By Region: Regionally, the global pipes market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and Latin America. North America dominates the market due to its extensive network of pipelines for oil and gas transmission, followed closely by Asia-Pacific, where rapid industrialization and infrastructural development are key growth drivers. The rising focus on water management systems and environmental sustainability projects is propelling demand for pipes in Europe.

By End-Use Industry: The market is further segmented by end-use industry into oil & gas, construction, water and wastewater management, chemical and petrochemical, and agriculture. The oil & gas sector holds the dominant market share under this segmentation. The increasing demand for energy and the need for efficient transportation of oil, gas, and petroleum products have led to significant investment in pipelines across major oil-producing countries. The construction sector also shows robust demand due to rising urbanization and infrastructure development.

Global Pipes Market Competitive Landscape

The global pipes market is characterized by the presence of several prominent players who dominate the market due to their global reach, technological innovations, and sustainable practices. The competitive landscape shows consolidation among major manufacturers and suppliers, contributing to economies of scale and enhancing their market position.

Global Pipes Industry Analysis

Growth Drivers

- Urbanization and Infrastructure Growth (Length of Pipelines Laid, New Installations): Urbanization continues to drive infrastructure projects globally, with notable growth in pipeline installations. For example, in 2023, India alone commissioned over 8,500 kilometers of gas pipelines under its National Gas Grid Project, contributing significantly to the global total of over 200,000 kilometers of pipelines laid that year. Additionally, China's Belt and Road Initiative facilitated the construction of over 12,000 kilometers of oil and gas pipelines across Asia and Europe in 2022. Such projects are part of wider urban development efforts, with governments prioritizing robust pipeline networks to support economic and urban growth.

- Growth in Oil & Gas Industry (Pipeline Kilometers, Oil Transmission Volumes): The global oil and gas industry is a major driver of pipeline growth, particularly in countries rich in natural resources. In 2022, the U.S. added over 4,000 kilometers of pipelines, facilitating oil transmission volumes that reached 17.7 million barrels per day, according to the U.S. Energy Information Administration (EIA). In the Middle East, Saudi Arabia reported the expansion of its pipeline infrastructure by more than 2,500 kilometers in the same period. Increased demand for oil and gas transmission continues to spur investment in long-distance pipeline projects.

- Government Regulations Supporting Pipe Installations: Government-backed regulations and tax incentives have played a crucial role in boosting pipeline installations. In 2023, the U.S. federal government implemented the "Infrastructure Investment and Jobs Act," providing tax benefits for pipeline projects aimed at expanding water and energy infrastructure. Similarly, in Europe, the European Green Deal allocated significant funding for sustainable infrastructure, resulting in the installation of over 2,200 kilometers of new pipelines adhering to green building codes. These policies not only accelerate infrastructure projects but also ensure compliance with high safety and environmental standards.

Market Restraints

- Fluctuating Raw Material Prices (Steel, Copper): Raw material price volatility, especially for steel and copper, poses a significant challenge for the global pipes market. In 2023, the price of steel increased by 25%, reaching an average of USD 1,400 per metric ton, according to the World Bank Commodities Price Data. Copper, widely used in water and gas pipelines, saw a price surge of 30%, reaching USD 8,600 per metric ton by mid-2024. These fluctuations make it difficult for pipeline manufacturers and contractors to manage costs effectively, particularly in long-term infrastructure projects.

- High Installation Costs (Cost per Meter): High installation costs are a major hurdle in pipeline projects, with costs varying significantly depending on geography and the materials used. In the U.S., the average cost of pipeline installation increased to approximately USD 500,000 per kilometer in 2023, influenced by inflation and labor shortages. In developing regions like Sub-Saharan Africa, costs can exceed USD 1 million per kilometer, due to the logistical challenges of laying pipelines in remote areas. These rising costs deter investment in large-scale infrastructure projects, especially in less economically developed regions.

Global Pipes Market Future Outlook

Over the next five years, the global pipes market is expected to experience substantial growth due to increasing infrastructure investments, urbanization, and the need for efficient water and wastewater management systems. The continuous development in oil and gas transportation pipelines, coupled with technological innovations in material sciences for pipe manufacturing, is set to boost the demand. Furthermore, the growing adoption of eco-friendly and sustainable piping materials will open new avenues for market growth, particularly in regions like Europe and North America, where sustainability is a key focus.

Market Opportunities

- Technological Advancements in Pipe Coating (Corrosion-Resistant Coatings): Technological innovations, particularly in pipe coatings, present significant opportunities for the global pipes market. Corrosion-resistant coatings, essential for increasing the lifespan of pipes in harsh environments, are being rapidly adopted. In 2022, over 60,000 kilometers of pipelines globally were treated with advanced anti-corrosion coatings, particularly in the oil and gas industry. These coatings are critical in regions with extreme temperatures, such as Russia and Canada, where pipelines face severe weather conditions. This technology is crucial for reducing maintenance costs and extending the operational life of pipelines.

- Increasing Demand for Underground Pipes (Urban Infrastructure Projects): Underground pipelines are becoming increasingly important for urban infrastructure development. By 2023, over 55% of new pipeline installations in the U.S. were underground, driven by urbanization and the need for efficient space utilization. The growing demand for underground water and sewage pipelines has been particularly pronounced in Asia, where India alone installed over 20,000 kilometers of underground pipes for municipal water systems between 2022 and 2023. The development of subterranean infrastructure helps reduce urban congestion and improves the reliability of essential services.

Scope of the Report

|

Material Type |

Steel Pipes Plastic Pipes (PVC, CPVC, HDPE) Concrete Pipes Copper Pipes Cast Iron Pipes |

|

End-Use Industry |

Oil & Gas Construction Water and Wastewater Management Chemical and Petrochemical Agriculture |

|

Application |

Transmission Pipes Distribution Pipes Structural Pipes Industrial Pipes Sanitation Pipes |

|

Diameter |

Small-Diameter Pipes Medium-Diameter Pipes Large-Diameter Pipes |

|

Region |

North America Europe Asia Pacific Middle East and Africa Latin America |

Products

Key Target Audience

Oil and Gas Companies

Construction Companies

Water and Wastewater Management Firms

Government and Regulatory Bodies (e.g., U.S. Environmental Protection Agency, European Environment Agency)

Chemical and Petrochemical Industries

Agriculture and Irrigation Equipment Manufacturers

Investor and Venture Capitalist Firms

Infrastructure Development Agencies (e.g., World Bank, Asian Development Bank)

Companies

Players Mentioned in the Report:

ArcelorMittal

Tata Steel

Nippon Steel Corporation

Tenaris

JFE Steel Corporation

China National Petroleum Corporation

Vallourec

Saudi Steel Pipe Company

Aliaxis Group

Georg Fischer Piping Systems

Welspun Corp

ISCO Industries

JM Eagle

Mueller Water Products

Mexichem SAB

Table of Contents

1. Global Pipes Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Tonnes, Market Value)

1.4. Market Segmentation Overview

2. Global Pipes Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Pipeline Projects, Infrastructure Developments)

3. Global Pipes Market Analysis

3.1. Growth Drivers

3.1.1. Urbanization and Infrastructure Growth (Length of Pipelines Laid, New Installations)

3.1.2. Growth in Oil & Gas Industry (Pipeline Kilometers, Oil Transmission Volumes)

3.1.3. Government Regulations Supporting Pipe Installations (Regulation Codes, Tax Incentives)

3.1.4. Increasing Adoption of Sustainable Materials (Green Building Code Compliance)

3.2. Market Challenges

3.2.1. Fluctuating Raw Material Prices (Steel, Copper)

3.2.2. High Installation Costs (Cost per Meter)

3.2.3. Lack of Skilled Workforce (Pipe Welding, Skilled Fitters)

3.3. Opportunities

3.3.1. Technological Advancements in Pipe Coating (Corrosion-Resistant Coatings)

3.3.2. Increasing Demand for Underground Pipes (Urban Infrastructure Projects)

3.3.3. Expansion of Industrial Applications (Water Treatment, Desalination Plants)

3.4. Trends

3.4.1. Use of Recycled Materials in Pipe Manufacturing

3.4.2. Digitization and Smart Pipelines (IoT Integration for Pipeline Monitoring)

3.4.3. Expansion of Multilayer Pipes for Durability

3.5. Government Regulation

3.5.1. Pipeline Safety Regulations (Material Standards, Pressure Tolerances)

3.5.2. Wastewater Management Guidelines (Sanitation Pipe Standards)

3.5.3. Sustainable Infrastructure Initiatives (Green Pipes, Renewable Energy Integration)

3.5.4. Trade Policies Affecting Pipe Imports/Exports

3.6. SWOT Analysis

3.7. Supply Chain Ecosystem (Steel Suppliers, Distributors, End-users)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Global Pipes Market Segmentation

4.1. By Material Type (In Value and Volume)

4.1.1. Steel Pipes

4.1.2. Plastic Pipes (PVC, CPVC, HDPE)

4.1.3. Concrete Pipes

4.1.4. Copper Pipes

4.1.5. Cast Iron Pipes

4.2. By End-Use Industry (In Value)

4.2.1. Oil & Gas

4.2.2. Construction

4.2.3. Water and Wastewater Management

4.2.4. Chemical and Petrochemical

4.2.5. Agriculture

4.3. By Application (In Value and Volume)

4.3.1. Transmission Pipes

4.3.2. Distribution Pipes

4.3.3. Structural Pipes

4.3.4. Industrial Pipes

4.3.5. Sanitation Pipes

4.4. By Diameter (In Value and Volume)

4.4.1. Small-Diameter Pipes

4.4.2. Medium-Diameter Pipes

4.4.3. Large-Diameter Pipes

4.5. By Region (In Value)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. Latin America

5. Global Pipes Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. ArcelorMittal

5.1.2. Tata Steel

5.1.3. Nippon Steel Corporation

5.1.4. Tenaris

5.1.5. JFE Steel Corporation

5.1.6. China National Petroleum Corporation

5.1.7. Vallourec

5.1.8. Saudi Steel Pipe Company

5.1.9. Aliaxis Group

5.1.10. Georg Fischer Piping Systems

5.1.11. Welspun Corp

5.1.12. ISCO Industries

5.1.13. JM Eagle

5.1.14. Mueller Water Products

5.1.15. Mexichem SAB

5.2 Cross Comparison Parameters (Revenue, Production Capacity, Manufacturing Facilities, Number of Employees, Global Presence, Material Innovation, Industry Collaboration, Sustainability Initiatives)

5.3. Market Share Analysis (In Percentage)

5.4. Strategic Initiatives (Partnerships, Joint Ventures)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Pipes Market Regulatory Framework

6.1. Environmental Standards (Emission Standards, Material Usage Regulations)

6.2. Compliance Requirements (ISO Certifications)

6.3. Certification Processes (Industry Specific Certifications)

7. Global Pipes Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Pipes Future Market Segmentation

8.1. By Material Type (In Value)

8.2. By End-Use Industry (In Value)

8.3. By Application (In Value)

8.4. By Diameter (In Value)

8.5. By Region (In Value)

9. Global Pipes Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial stage focuses on mapping the ecosystem of the global pipes market, identifying major stakeholders, including suppliers, manufacturers, and end-users. This is achieved through comprehensive desk research and leveraging proprietary databases to understand market dynamics and critical variables such as demand for different materials and applications.

Step 2: Market Analysis and Construction

Historical market data is analyzed to identify trends in pipeline installations, infrastructure projects, and material usage. The analysis also considers regulatory developments and technological advancements influencing the market. Market penetration and pipeline network expansion across regions are evaluated to estimate revenue generation.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses are developed and validated through consultations with industry experts, including pipeline manufacturers, oil and gas operators, and construction firms. These interviews provide operational and financial insights, which refine market data and enhance the accuracy of market forecasts.

Step 4: Research Synthesis and Final Output

The final stage involves direct engagement with key market players to collect data on sales performance, production capacity, and material innovations. This data is synthesized with insights from desk research to produce a validated and comprehensive report on the global pipes market.

Frequently Asked Questions

01. How big is the global pipes market?

The global pipes market was valued at USD 142 billion, driven by increasing demand for robust infrastructure, pipeline transportation in oil and gas, and water management systems.

02. What are the challenges in the global pipes market?

Challenges include fluctuating raw material prices, high installation costs, and the need for skilled labor in pipe installation and maintenance. Regulatory changes regarding environmental sustainability also pose challenges for certain materials.

03. Who are the major players in the global pipes market?

Key players in the market include ArcelorMittal, Tata Steel, Nippon Steel Corporation, Tenaris, and JFE Steel Corporation. These companies dominate the market due to their extensive global reach and advanced manufacturing capabilities.

04. What are the growth drivers of the global pipes market?

The market is driven by factors such as urbanization, infrastructure development, increased oil and gas pipeline installations, and the rising demand for efficient water and wastewater management systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.