Global Plastic Resin Market Outlook to 2030

Region:Global

Author(s):Mukul Soni

Product Code:KROD10383

Region:Global

Author(s):Mukul Soni

Product Code:KROD10383

December 2024

85

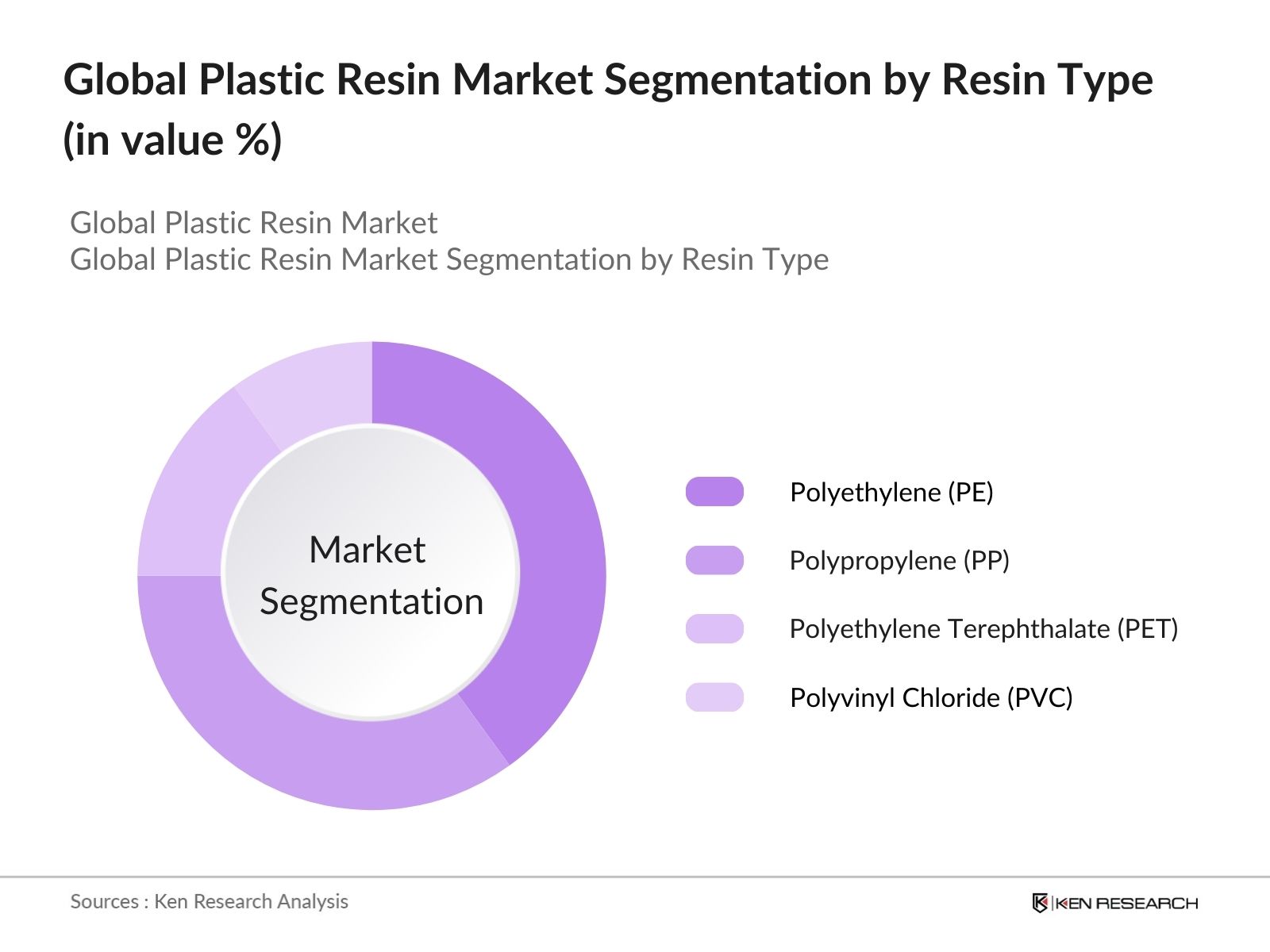

By Resin Type: The global plastic resin market is segmented by resin type into polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyvinyl chloride (PVC), polystyrene (PS), and others (including polyamide and polycarbonate). Polyethylene holds the dominant market share because of its widespread use in packaging, particularly in consumer products and flexible packaging. Its low cost, flexibility, and excellent moisture barrier properties make it a preferred material for packaging applications across multiple industries.

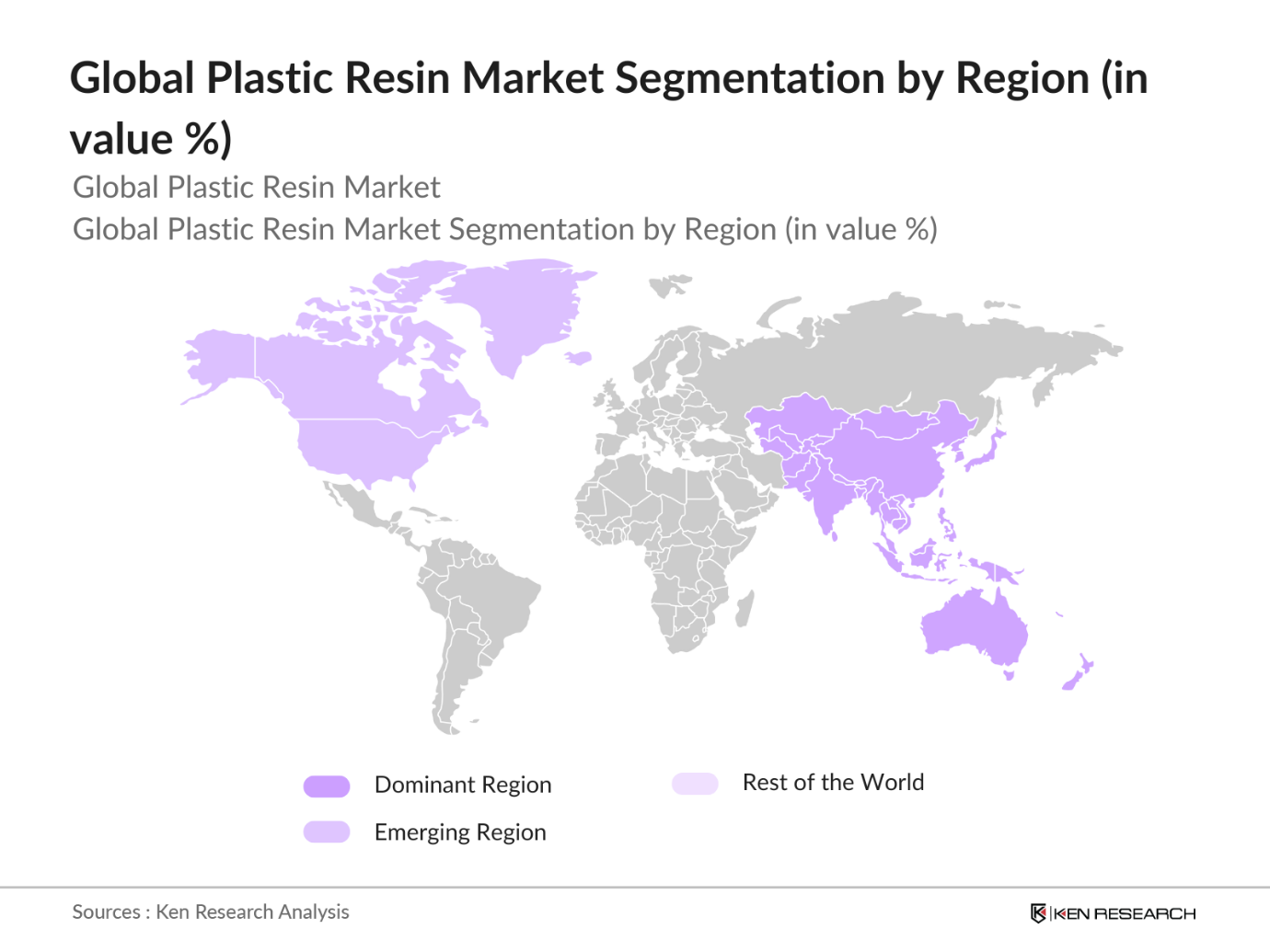

By Region: The global plastic resin market is segmented by region into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific leads the regional segmentation, driven by strong industrialization, significant demand from automotive, packaging, and construction industries, and the presence of key manufacturing hubs in China, India, and Southeast Asia. The region's dominance is also supported by investments in sustainable plastic solutions and expanding consumer goods industries.

By Application: The plastic resin market is segmented by application into packaging, automotive, construction, consumer goods, electrical and electronics, and medical devices. Packaging dominates the application segment, owing to the rapid growth in e-commerce and the demand for lightweight and durable packaging solutions. The increasing adoption of flexible packaging and the shift toward sustainable packaging materials further strengthen this segment's position in the market.

The global plastic resin market is dominated by several key players, with a mixture of international and regional companies leading the charge. The competitive landscape is characterized by innovation in bio-based plastics, expansions in production capacity, and increasing focus on recycling technologies. Companies are strategically investing in R&D and forming partnerships to strengthen their market positions.

|

Company Name |

Establishment Year |

Headquarters |

Product Portfolio |

R&D Investment |

Global Presence |

Sustainability Initiatives |

Production Capacity |

Major Clients |

Revenue |

|

LyondellBasell Industries N.V. |

1985 |

Houston, U.S. |

- |

- |

- |

- |

- |

- |

- |

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

- |

- |

- |

- |

- |

- |

- |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Dow Inc. |

1897 |

Midland, U.S. |

- |

- |

- |

- |

- |

- |

- |

|

ExxonMobil Corporation |

1870 |

Irving, U.S. |

- |

- |

- |

- |

- |

- |

- |

The global plastic resin market is expected to experience robust growth over the next five years, driven by the increasing demand for lightweight, cost-effective, and versatile materials across multiple industries. Key drivers for growth include the continued expansion of packaging solutions, advancements in bioplastics, and a surge in demand for recycled plastic resins as governments and industries push for more sustainable practices. Regions like Asia Pacific and North America will continue to lead market growth due to their large industrial base and adoption of new technologies.

|

By Resin Type |

Polyethylene (PE) Polypropylene (PP) PET PVC PS Polyamide (PA) Others |

|

By Application |

Packaging Automotive Construction Consumer Goods Electrical & Electronics Medical Devices |

|

By Technology |

Injection Molding Blow Molding Extrusion Thermoforming Rotational Molding |

|

By End-User |

Automotive Construction Packaging Electronics Healthcare |

|

By Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1.1. Rise in Demand for Lightweight Automotive Materials

3.1.2. Expansion of Packaging Industry

3.1.3. Increasing Usage in Consumer Goods and Electronics

3.1.4. Advancements in Biodegradable and Recyclable Resins

3.2. Market Challenges

3.2.1. Volatility in Crude Oil Prices (Key Raw Material)

3.2.2. Stringent Environmental Regulations on Plastic Usage

3.2.3. High Cost of Raw Materials

3.2.4. Complex Recycling Processes

3.3. Opportunities

3.3.1. Adoption of Recycled Plastics in Packaging

3.3.2. Growing Demand for Biodegradable Resins in End-Use Sectors

3.3.3. Investment in Research for Sustainable Alternatives

3.3.4. Emerging Markets in Asia-Pacific and Africa

3.4. Trends

3.4.1. Shift Toward Sustainable and Eco-Friendly Resins

3.4.2. Innovations in Additives and Fillers for Enhanced Properties

3.4.3. Development of Bio-Based Resins

3.4.4. Circular Economy Initiatives in the Plastic Sector

3.5. Government Regulation

3.5.1. Plastic Waste Management and Recycling Policies

3.5.2. Global Ban on Single-Use Plastics

3.5.3. Carbon Footprint Reduction Programs

3.5.4. Incentives for Sustainable Plastic Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers (Oil and Raw Material Suppliers)

3.8.2. Bargaining Power of Buyers (Automotive, Packaging, Consumer Goods)

3.8.3. Threat of New Entrants (Emerging Bioplastics Players)

3.8.4. Threat of Substitutes (Metal, Glass)

3.8.5. Industry Rivalry (High Competition Among Global Manufacturers)

3.9. Competition Ecosystem

4.1. By Resin Type (In Value %)

4.1.1. Polyethylene (PE)

4.1.2. Polypropylene (PP)

4.1.3. Polyethylene Terephthalate (PET)

4.1.4. Polyvinyl Chloride (PVC)

4.1.5. Polystyrene (PS)

4.1.6. Polyamide (PA)

4.1.7. Others (Acrylonitrile Butadiene Styrene (ABS), Polycarbonate (PC))

4.2. By Application (In Value %)

4.2.1. Packaging

4.2.2. Automotive

4.2.3. Construction

4.2.4. Consumer Goods

4.2.5. Electrical & Electronics

4.2.6. Medical Devices

4.3. By Technology (In Value %)

4.3.1. Injection Molding

4.3.2. Blow Molding

4.3.3. Extrusion

4.3.4. Thermoforming

4.3.5. Rotational Molding

4.4. By End-User Industry (In Value %)

4.4.1. Automotive

4.4.2. Construction

4.4.3. Packaging

4.4.4. Electronics

4.4.5. Healthcare

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. LyondellBasell Industries N.V.

5.1.2. SABIC

5.1.3. BASF SE

5.1.4. Dow Inc.

5.1.5. ExxonMobil Corporation

5.1.6. INEOS Group Ltd.

5.1.7. TotalEnergies SE

5.1.8. Chevron Phillips Chemical Co.

5.1.9. Reliance Industries Ltd.

5.1.10. Formosa Plastics Corporation

5.1.11. Borealis AG

5.1.12. Westlake Chemical Corporation

5.1.13. Arkema S.A.

5.1.14. Covestro AG

5.1.15. LG Chem Ltd.

5.2. Cross Comparison Parameters

5.2.1. No. of Employees

5.2.2. Headquarters

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. Product Portfolio

5.2.6. Global Presence

5.2.7. Recent Developments

5.2.8. Key Partnerships

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Resin Type (In Value %) 8.2. By Application (In Value %) 8.3. By Technology (In Value %) 8.4. By End-User Industry (In Value %) 8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial step involved creating an ecosystem map that includes major stakeholders in the global plastic resin market. We utilized a combination of secondary and proprietary databases to gather in-depth industry insights. This stage aimed to pinpoint and define the essential variables that affect the market, including resin types and major applications.

This phase focused on compiling historical data on the global plastic resin market. Market penetration in key industries such as automotive and packaging was assessed, alongside revenue contributions. Service quality metrics were evaluated to ensure the reliability and validity of the revenue estimates.

Market hypotheses were formulated based on historical data and expert opinions. These were validated through interviews with industry professionals across the resin supply chain. This phase was crucial for gaining operational insights and refining data models for market analysis.

Finally, data from plastic resin manufacturers were gathered to obtain detailed insights into sales performance and consumer preferences. This data was cross-verified with bottom-up approaches to deliver a comprehensive and validated analysis of the global plastic resin market.

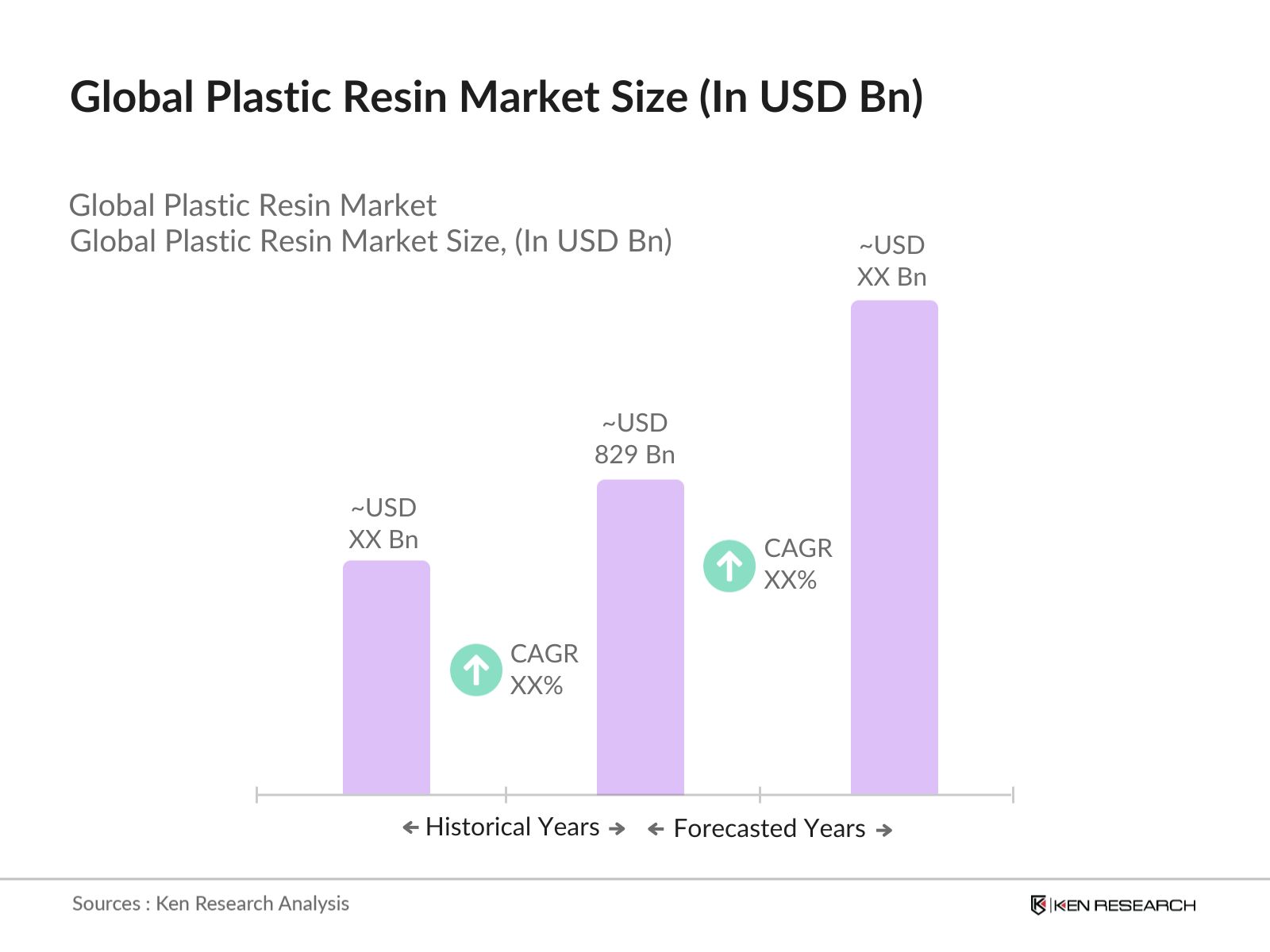

The global plastic resin market is valued at USD 829 billion, driven by demand from industries like automotive, construction, and packaging. Increasing environmental concerns and the push for recyclable resins are also influencing market dynamics.

Challenges include price volatility in raw materials such as crude oil, the environmental impact of plastic waste, and stringent regulations on plastic usage. Complex recycling processes also pose significant barriers to market expansion.

Key players in the market include LyondellBasell Industries, SABIC, BASF SE, Dow Inc., and ExxonMobil. These companies dominate through advanced production technologies, high investments in R&D, and strong global distribution networks.

The market is driven by rising demand for lightweight materials in automotive manufacturing, growth in e-commerce driving packaging demand, and innovations in bio-based and sustainable plastic resins. Additionally, increased consumer awareness about environmental sustainability is boosting demand for recyclable materials.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.