Global Polyethylene Terephthalate Glycol Market Outlook to 2030

Region:Global

Author(s):Mukul Soni

Product Code:KROD5829

December 2024

97

About the Report

Global Polyethylene Terephthalate Glycol Market Overview

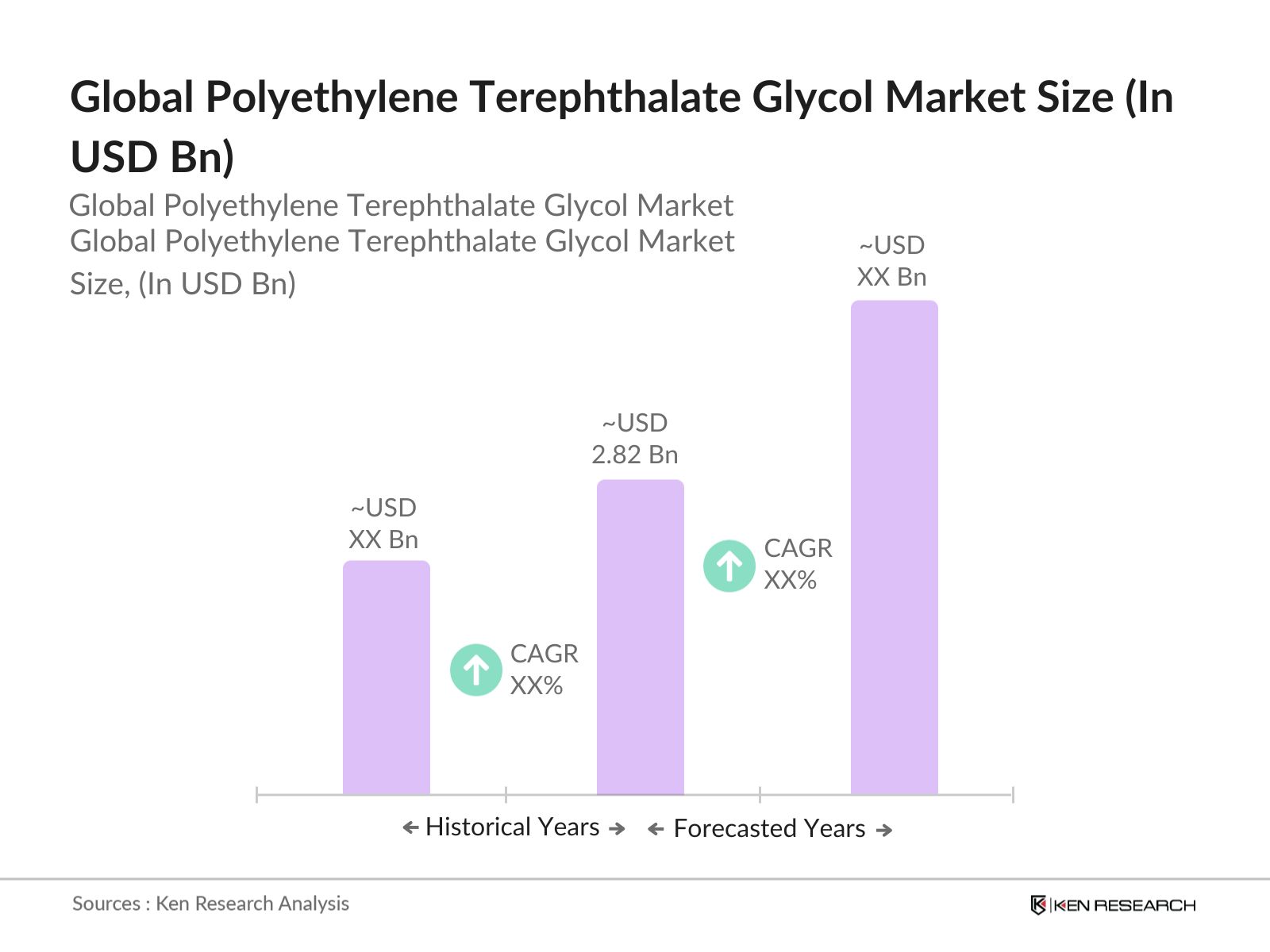

- The Global Polyethylene Terephthalate Glycol (PETG) market is valued at USD 2.82 billion, based on a five-year historical analysis. This market is driven by increasing demand for sustainable and versatile materials in packaging, medical devices, and consumer goods industries. The widespread use of PETG in various applications, particularly in food packaging and 3D printing, is further fueling growth. Companies are focusing on the recyclability and eco-friendly characteristics of PETG, contributing to its expanding demand.

- Countries like China, the United States, and Germany dominate the PETG market due to their advanced manufacturing capabilities, strong industrial infrastructure, and rising demand in the medical and packaging industries. China's dominance is attributed to its massive production capabilities and access to low-cost raw materials. Meanwhile, the U.S. leads in technological advancements and innovation in PETG applications, particularly in the medical and packaging sectors. Germany's position is driven by its focus on high-quality industrial applications and sustainability initiatives.

- The use of PETG in 3D printing has grown significantly in recent years. In 2023, the global 3D printing market reached $15 billion, driven by demand for customizable and high-performance materials. PETG is favored in 3D printing for its ease of use, durability, and flexibility. Industries such as aerospace, healthcare, and automotive are adopting 3D printing technologies at an increasing rate. PETGs ability to produce strong, precise, and lightweight parts makes it an ideal material for 3D printing applications, driving its demand in advanced manufacturing processes.

Global Polyethylene Terephthalate Glycol Market Segmentation

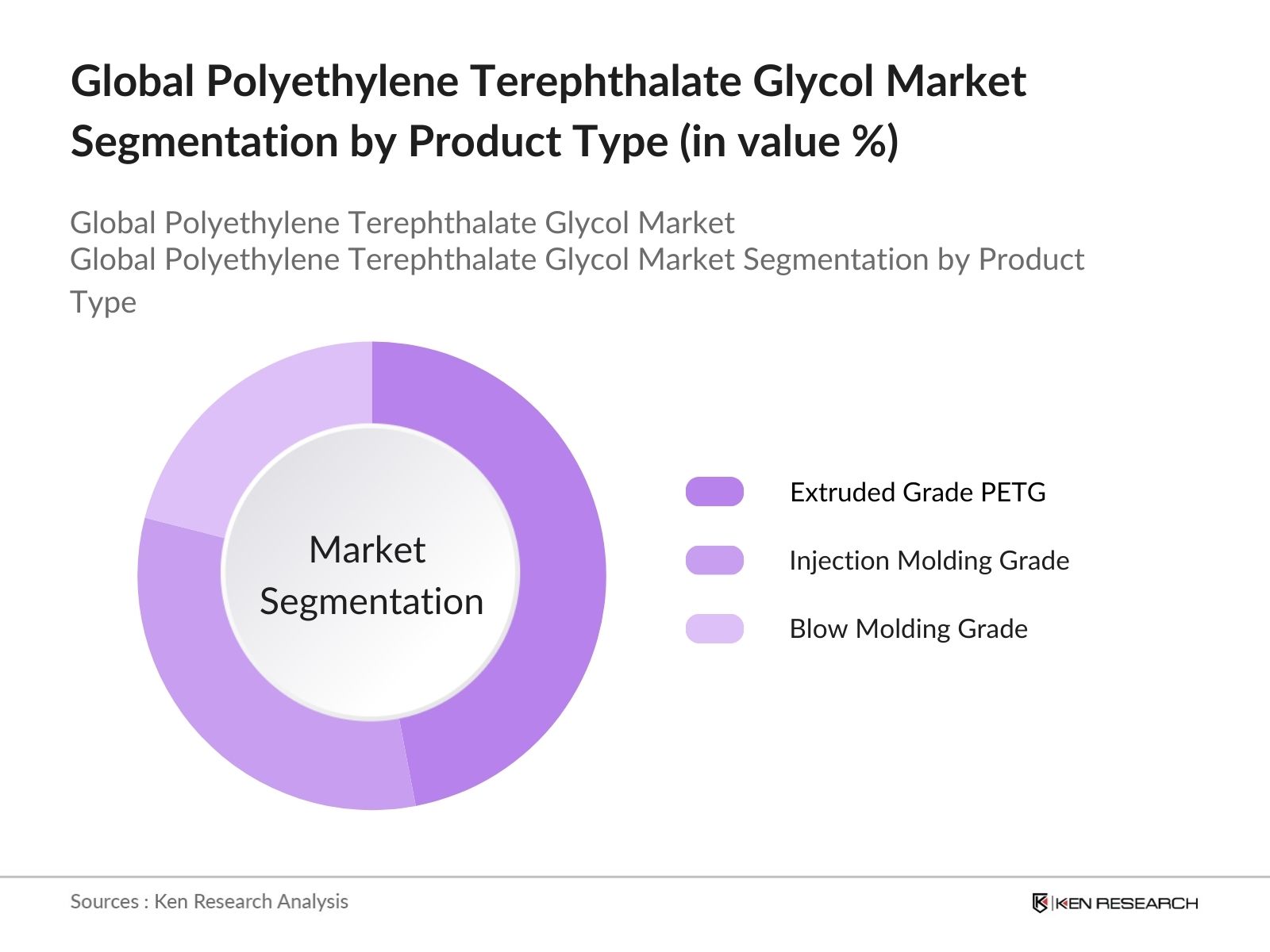

By Product Type: The Global Polyethylene Terephthalate Glycol market is segmented by product type into extruded grade PETG, injection molding grade PETG, and blow molding grade PETG. Currently, extruded grade PETG holds the dominant market share due to its widespread use in the packaging industry. This is primarily driven by the growing demand for rigid packaging solutions that offer strength and clarity, crucial for food packaging and display purposes. Extruded PETG is also favored due to its excellent processability, which enables its use in a wide range of industrial and consumer applications.

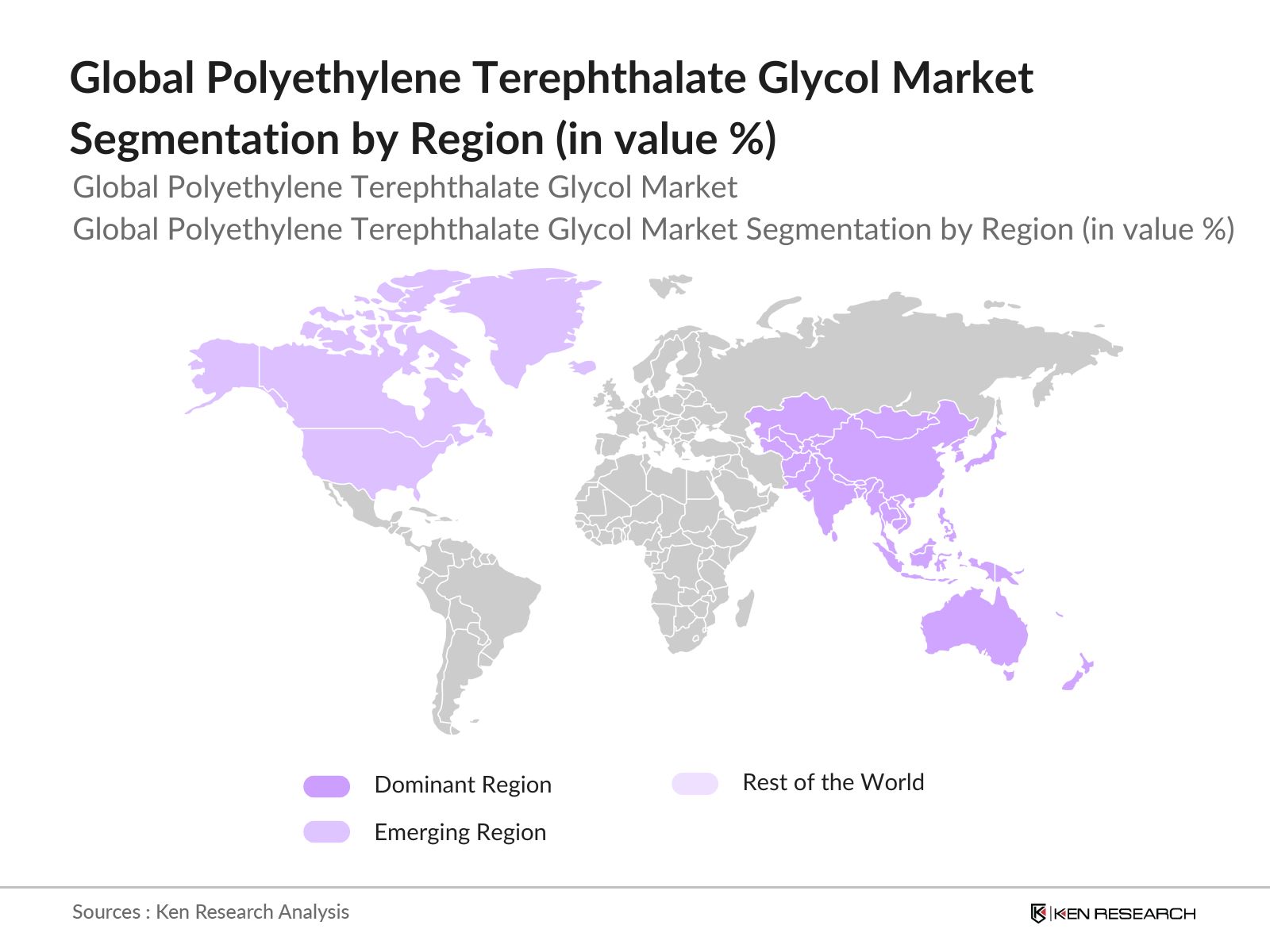

By Region: The PETG market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific is the leading region due to the robust industrial infrastructure in China, India, and Japan. These countries are major players in the packaging and electronics industries, where PETG is widely used. Additionally, the region benefits from low-cost labor and raw materials, making it a key producer and consumer of PETG. Rapid urbanization and a growing middle-class population further fuel demand in this region.

By Application: The PETG market is segmented into packaging, medical devices, electronics, building and construction, and 3D printing. Packaging dominates the market due to PETG's excellent strength, impact resistance, and clarity, which are essential for food and beverage packaging. The increasing shift towards sustainable packaging solutions, particularly in the food and healthcare sectors, has accelerated the adoption of PETG. Moreover, the demand for visually appealing packaging that enhances product shelf life makes PETG a preferred choice for various industries.

Global Polyethylene Terephthalate Glycol Market Competitive Landscape

The PETG market is dominated by a mix of global players and regional manufacturers. Companies are focusing on expanding their production capacity, developing eco-friendly alternatives, and investing in research and development to gain a competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

Production Capacity (Tons) |

Product Portfolio |

R&D Expenditure (USD) |

Sustainability Initiatives |

Key Markets |

Number of Employees |

Partnerships/Collaborations |

|

Eastman Chemical Company |

1920 |

Kingsport, USA |

|||||||

|

SK Chemicals |

1969 |

Seongnam, South Korea |

|||||||

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

|||||||

|

LyondellBasell Industries |

1985 |

Houston, USA |

|||||||

|

Indorama Ventures Public Company |

1994 |

Bangkok, Thailand |

Global Polyethylene Terephthalate Glycol Industry Analysis

Growth Drivers

- Increase in Sustainable Packaging Initiatives: The rise of sustainable packaging practices is driving the global Polyethylene Terephthalate Glycol (PETG) market. A recent report by the World Bank estimates that by 2024, over 3.3 billion metric tons of solid waste are generated globally each year. This rapid increase in waste generation is pushing governments to prioritize sustainable packaging solutions, especially in industries like food & beverage and healthcare. PETG's recyclable properties make it a preferred choice among manufacturers shifting towards circular economy models. Government-backed initiatives, like the European Union's goal to recycle 50% of plastic packaging waste, are further accelerating demand.

- Demand for Flexible and Lightweight Materials: Lightweight materials like PETG have become essential across various industries. In 2024, the automotive industry alone saw a 10 million ton reduction in vehicle weight by adopting lightweight materials, resulting in fuel savings worth $1.5 billion, according to the International Energy Agency (IEA). PETG's lightweight and flexible nature offer significant benefits for packaging and transportation, helping industries reduce costs associated with shipping and handling. The food and beverage sector, for example, increasingly uses PETG for bottle manufacturing, due to its cost-effectiveness in transportation and resistance to impact.

- Expansion of PETG Applications in Medical and Food & Beverage Sectors: PETG's versatility, non-reactive properties, and safety make it an ideal material for medical devices and food packaging. The World Health Organization (WHO) notes that global medical device spending surpassed $500 billion in 2022, with a large portion of this growth coming from plastic-based materials like PETG. In the food & beverage industry, over 200 million tons of food-grade packaging were produced globally in 2023. The growing awareness of hygienic packaging solutions, spurred by stricter regulations and demand for safer consumer products, further boosts the usage of PETG.

Market Restraints

- Raw Material Price Volatility: The price of raw materials like crude oil and ethylene glycol, which are integral to PETG production, has been highly volatile. The U.S. Energy Information Administration (EIA) reported that crude oil prices fluctuated between $70 to $100 per barrel in 2023, influencing the cost of petrochemical derivatives like ethylene glycol. This volatility creates uncertainty for PETG manufacturers, impacting overall production costs and profitability. Fluctuations in feedstock prices, due to geopolitical tensions and supply chain disruptions, continue to challenge the market's stability in 2024.

- Complex Recycling Process: Although PETG is recyclable, its recycling process is more complex compared to other materials like PET (Polyethylene Terephthalate). In 2023, a UNEP report noted that only about 20% of all plastic waste is effectively recycled globally, due in part to the technical difficulties of sorting and processing different plastic types. PETG's composition requires specialized recycling facilities, which are limited in many regions. This creates logistical and financial barriers to broader adoption, with high recycling costs acting as a deterrent for manufacturers aiming to adopt more sustainable practices.

Global Polyethylene Terephthalate Glycol Market Future Outlook

Over the next five years, the Global Polyethylene Terephthalate Glycol (PETG) market is expected to experience robust growth. This growth will be driven by advancements in recycling technology, increasing demand for sustainable packaging, and the rising application of PETG in medical devices and 3D printing. The expansion of PETG into niche markets like automotive and industrial applications will also contribute to its sustained growth. Furthermore, initiatives from governments and industry stakeholders to reduce carbon footprints will drive the adoption of PETG as a preferred material in various industries.

Market Opportunities

- Growing Adoption of PETG in Medical Devices and Healthcare Packaging: The healthcare sector's rising demand for non-toxic, durable, and transparent materials has boosted PETG's adoption. As of 2023, global healthcare spending surpassed $10 trillion, according to the World Health Organization (WHO). PETG's non-reactive and sterilizable properties make it ideal for manufacturing medical devices, surgical equipment, and pharmaceutical packaging. Its growing use in healthcare, combined with the increasing emphasis on hygiene and safety standards, positions PETG as a key material for future innovation in the medical sector.

- Market Penetration in Emerging Economies: Emerging economies in the Asia-Pacific and Latin America regions present significant growth opportunities for PETG manufacturers. According to the International Monetary Fund (IMF), Asia-Pacific economies saw an average growth rate of 4.5% in 2023, with rising industrial output and increasing demand for plastic packaging in countries like India, China, and Brazil. As these regions continue to industrialize and urbanize, the demand for lightweight and flexible materials like PETG is expected to grow, especially in sectors like food & beverage and healthcare.

Scope of the Report

|

By Product Type |

Extruded Grade PETG Injection Molding Grade PETG Blow Molding Grade PETG |

|

By Application |

Packaging Medical Devices Electronics Building and Construction 3D Printing |

|

By End-User Industry |

Food and Beverage Healthcare Consumer Goods Automotive Industrial Applications |

|

By Processing Technique |

Extrusion Injection Molding Blow Molding 3D Printing |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

PETG Manufacturers

Packaging Companies

Medical Device Manufacturers

Automotive and Electronics Industries

Raw Material Suppliers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, European Commission, REACH)

Retail and Consumer Goods Companies

Companies

Players Mentioned in the Report:

Eastman Chemical Company

SK Chemicals

SABIC

LyondellBasell Industries

Indorama Ventures Public Company

Mitsubishi Chemical Corporation

Covestro AG

DuPont de Nemours, Inc.

Reliance Industries Limited

PolyOne Corporation

LOTTE Chemical

Selenis

EMS-Chemie Holding AG

Jiangsu Sanfangxiang Group Co., Ltd.

Shanghai Pret Composites Co., Ltd.

Table of Contents

1. Global Polyethylene Terephthalate Glycol (PETG) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Polyethylene Terephthalate Glycol (PETG) Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Polyethylene Terephthalate Glycol (PETG) Market Analysis

3.1. Growth Drivers (Rising Demand for Packaging, Lightweight Properties, Sustainability Trends, Cost-Effectiveness, etc.)

3.1.1. Increase in Sustainable Packaging Initiatives

3.1.2. Demand for Flexible and Lightweight Materials

3.1.3. Expansion of PETG Applications in Medical and Food & Beverage Sectors

3.1.4. Recycling and Circular Economy Push

3.2. Market Challenges (Fluctuating Raw Material Prices, High Recycling Costs, etc.)

3.2.1. Raw Material Price Volatility (Crude Oil, Ethylene Glycol)

3.2.2. Complex Recycling Process

3.2.3. Competition from Substitute Materials (Bio-based Plastics)

3.3. Opportunities (Growth in Emerging Economies, Innovations in PETG Blends, etc.)

3.3.1. Growing Adoption of PETG in Medical Devices and Healthcare Packaging

3.3.2. Market Penetration in Emerging Economies (Asia-Pacific, Latin America)

3.3.3. Technological Advancements in PETG Processing

3.4. Trends (Increased Adoption of Biodegradable Variants, Development of Specialty PETG Grades)

3.4.1. Increased Biodegradable and Recyclable PETG Offerings

3.4.2. Shift Toward High-Performance PETG in Engineering Applications

3.4.3. Use of PETG in 3D Printing Applications

3.5. Government Regulations (Food Contact Standards, Environmental Regulations, etc.)

3.5.1. FDA and EU Approvals for Food-Grade PETG

3.5.2. Plastic Waste Management Policies and Recycling Mandates

3.5.3. Emission Reduction and Environmental Compliance Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. Global Polyethylene Terephthalate Glycol (PETG) Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Extruded Grade PETG

4.1.2. Injection Molding Grade PETG

4.1.3. Blow Molding Grade PETG

4.2. By Application (In Value %)

4.2.1. Packaging

4.2.2. Medical Devices

4.2.3. Electronics

4.2.4. Building and Construction

4.2.5. 3D Printing

4.3. By End-User Industry (In Value %)

4.3.1. Food and Beverage

4.3.2. Healthcare

4.3.3. Consumer Goods

4.3.4. Automotive

4.3.5. Industrial Applications

4.4. By Processing Technique (In Value %)

4.4.1. Extrusion

4.4.2. Injection Molding

4.4.3. Blow Molding

4.4.4. 3D Printing

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Polyethylene Terephthalate Glycol (PETG) Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Eastman Chemical Company

5.1.2. SK Chemicals

5.1.3. SABIC

5.1.4. LyondellBasell Industries

5.1.5. Reliance Industries Limited

5.1.6. DuPont de Nemours, Inc.

5.1.7. Indorama Ventures Public Company Limited

5.1.8. Mitsubishi Chemical Corporation

5.1.9. PolyOne Corporation

5.1.10. LOTTE Chemical

5.1.11. Selenis

5.1.12. Covestro AG

5.1.13. EMS-Chemie Holding AG

5.1.14. Jiangsu Sanfangxiang Group Co., Ltd.

5.1.15. Shanghai Pret Composites Co., Ltd.

5.2 Cross Comparison Parameters (Annual Revenue, Market Share, Production Capacity, Product Portfolio, Manufacturing Facilities, Number of Employees, Strategic Initiatives, R&D Spending)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Mergers, Acquisitions, Partnerships, and Collaborations)

5.5 Mergers And Acquisitions

5.6 Investment Analysis (Private Equity, Government Grants, Venture Capital)

6. Global Polyethylene Terephthalate Glycol (PETG) Market Regulatory Framework

6.1 Environmental Standards and Certification Requirements (REACH, RoHS, FDA Approvals)

6.2 Compliance Requirements for Packaging and Food-Contact Materials

6.3 Recycling Policies and Circular Economy Regulations

7. Global Polyethylene Terephthalate Glycol (PETG) Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Global Polyethylene Terephthalate Glycol (PETG) Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By End-User Industry (In Value %)

8.4 By Processing Technique (In Value %)

8.5 By Region (In Value %)

9. Global Polyethylene Terephthalate Glycol (PETG) Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping the PETG ecosystem, identifying all major stakeholders. This was achieved through extensive desk research, combining secondary and proprietary databases to gather industry-specific information. Key variables, such as product types, applications, and regulatory policies, were defined.

Step 2: Market Analysis and Construction

Historical data for the PETG market was compiled, focusing on market penetration, production capacities, and revenue generation. The data analysis included evaluating market share trends and assessing the quality of PETG products in various regions.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through interviews with industry experts, leveraging computer-assisted telephone interviews (CATI). These discussions provided insights into product performance and financial metrics.

Step 4: Research Synthesis and Final Output

The final phase involved direct consultations with PETG manufacturers and suppliers, which were used to confirm and refine the findings. The data was synthesized to provide a comprehensive analysis of the PETG market.

Frequently Asked Questions

01. How big is the Global Polyethylene Terephthalate Glycol (PETG) Market?

The Global Polyethylene Terephthalate Glycol (PETG) market was valued at USD 2.82 billion. This market is driven by the growing demand for sustainable packaging solutions and expanding applications in medical devices and 3D printing.

02. What are the challenges in the Global PETG Market?

Challenges in the PETG market include fluctuating raw material prices, particularly crude oil, which impacts production costs. Additionally, recycling and sustainability issues present hurdles for market growth.

03. Who are the major players in the Global PETG Market?

Key players include Eastman Chemical Company, SK Chemicals, SABIC, LyondellBasell Industries, and Indorama Ventures. These companies dominate due to their extensive production capacities and focus on sustainability initiatives.

04. What are the growth drivers for the Global PETG Market?

The PETG market is driven by factors such as increasing demand for sustainable packaging materials, growth in the medical device sector, and expanding applications in 3D printing and electronics.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.