Global Resistant Starch Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD9241

October 2024

86

About the Report

Global Resistant Starch Market Overview

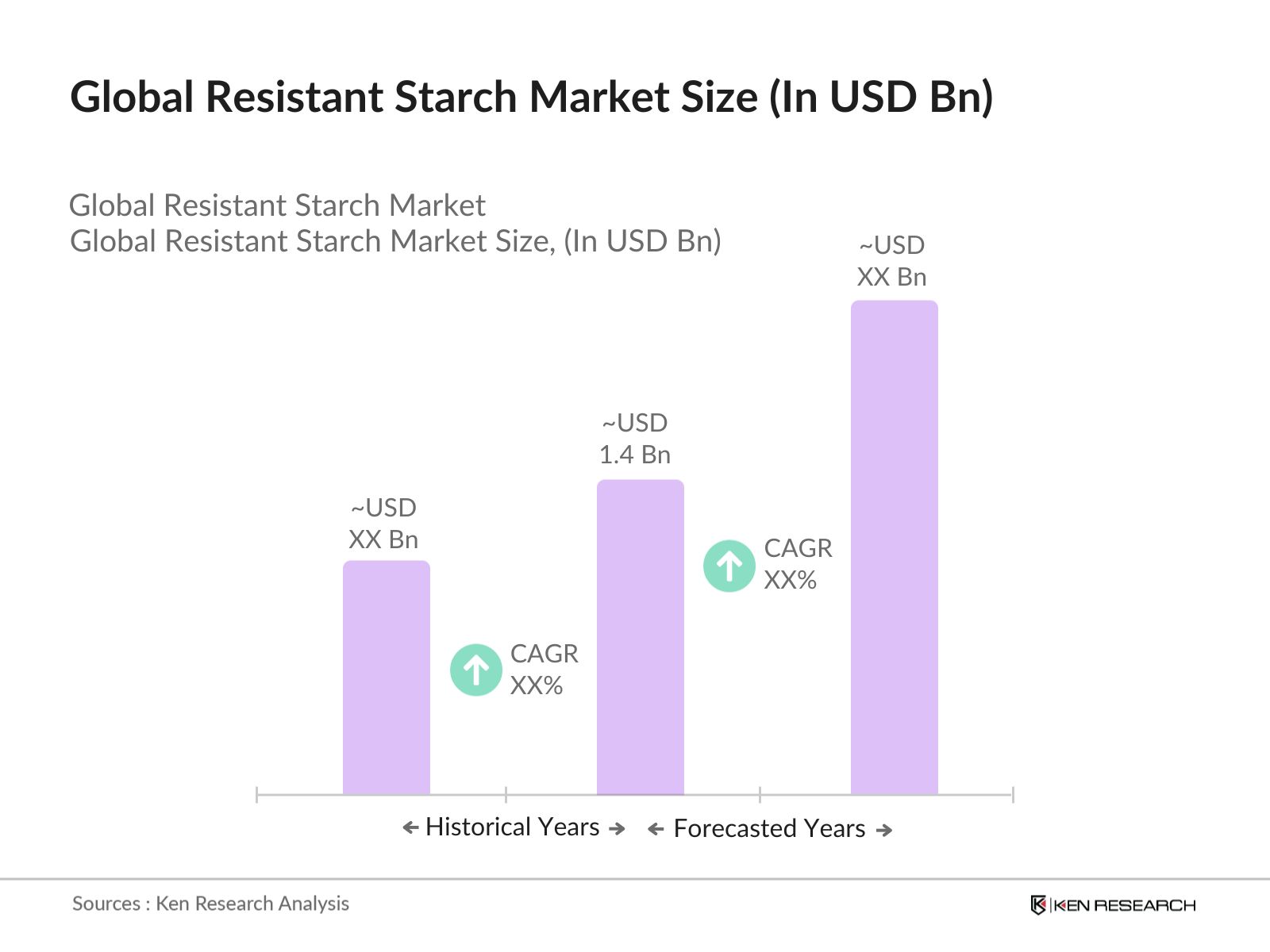

- The global resistant starch market is valued at USD 1.4 billion, based on a five-year historical analysis. The market is primarily driven by the rising demand for functional foods and dietary fibers, particularly in the food and beverage, pharmaceutical, and nutraceutical industries. Resistant starch is gaining popularity due to its health benefits, such as improved gut health, better blood sugar control, and weight management. The market's growth is also fueled by increasing consumer awareness regarding the benefits of incorporating dietary fibers into their diets.

- Countries such as the United States, China, and Brazil dominate the global resistant starch market. The dominance of these countries can be attributed to their large populations, advanced food processing industries, and rising health-conscious consumer bases. Additionally, the presence of key manufacturers and extensive research and development in food technology in these regions has solidified their positions as leaders in the market.

- Countries are implementing stricter labeling regulations to ensure consumers are better informed about the nutritional content of their food. In 2022, the EU introduced mandatory nutrition labeling for all products containing more than 2 grams of dietary fiber per serving. Similar regulations are expected in the U.S. and Canada by 2024, which will directly impact how resistant starch products are marketed and labeled, ensuring transparency in fiber content for consumers.

Global Resistant Starch Market Segmentation

- By Product Type: The global resistant starch market is segmented by product type into Resistant Starch Type 1 (RS1), Resistant Starch Type 2 (RS2), Resistant Starch Type 3 (RS3), and Resistant Starch Type 4 (RS4). Among these, RS2 has a dominant market share, owing to its high prevalence in naturally occurring food sources like bananas and potatoes, and its growing use in functional foods and beverages. RS2 is preferred due to its high resistance to digestion, making it beneficial for gut health and reducing the glycemic index of foods.

- By Region: Regionally, the global resistant starch market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds a dominant market share due to the strong presence of health-conscious consumers and advanced food processing technologies. The region's well-established regulatory framework for food safety and labeling also supports the widespread use of resistant starch in food products.

- By Source: The global resistant starch market is also segmented by source into corn, potatoes, bananas, rice, and wheat. Corn dominates the market in terms of source due to its wide availability and versatility in food applications. Corn-based resistant starch is extensively used in the food processing industry, especially for baked goods, cereals, and snacks, where it acts as a fat replacer and helps in calorie reduction without compromising texture.

Global Resistant Starch Market Competitive Landscape

The global resistant starch market is characterized by the presence of a few major players, with companies like Ingredion Incorporated, Tate & Lyle, and Cargill leading the market. These companies invest heavily in research and development to innovate new products and meet the growing consumer demand for healthier food options. The competitive landscape is marked by product differentiation, strategic collaborations, and expansions into emerging markets.

|

Company |

Established Year |

Headquarters |

R&D Investment |

Revenue (USD Bn) |

Market Share |

Product Portfolio |

Global Presence |

Strategic Initiatives |

|

Ingredion Incorporated |

1906 |

Illinois, USA |

||||||

|

Tate & Lyle |

1921 |

London, UK |

||||||

|

Cargill |

1865 |

Minnesota, USA |

||||||

|

Roquette Frres |

1933 |

Lestrem, France |

||||||

|

Avebe |

1919 |

Veendam, Netherlands |

Global Resistant Starch Industry Analysis

Growth Drivers

- Rising Consumer Demand for Functional Foods: The demand for functional foods with health benefits, such as those containing resistant starch, has significantly increased due to a growing awareness of the role of diet in overall health. In 2024, the global functional food market is set to see a notable uptick, driven by consumer demand for gut health-enhancing products. Countries like the United States, with a functional food consumption rate of 23 kg per capita, are leading this trend. The World Bank reported that consumer expenditure on health-related products in the U.S. alone reached $3.9 trillion in 2022.

- Increasing Awareness of Gut Health: Rising consumer interest in gut health has accelerated the demand for resistant starch, a well-known prebiotic fiber that promotes digestive health. In 2023, the global digestive health products market was worth over $12 billion, highlighting the increasing awareness of gut health's importance. The number of people seeking products for digestive health support has risen by 15 million between 2022 and 2024, especially in markets like Europe and North America, where gastrointestinal disorders are more prevalent.

- Rising Prevalence of Obesity and Diabetes: With over 500 million people globally suffering from obesity and 530 million affected by diabetes in 2024, the health crisis surrounding these conditions is driving the need for better dietary interventions. Resistant starch, known for aiding blood sugar control and weight management, is seeing increased use. The Middle East and North Africa (MENA) region, for example, has over 100 million diabetes patients, creating a massive demand for dietary solutions like resistant starch.

Market Restraints

- High Production Costs: The high production costs associated with resistant starch pose a significant challenge to its wider adoption, especially in emerging markets. Processing resistant starch requires advanced technologies that drive up production expenses. For instance, in countries like India and China, production costs for starch-based ingredients increased by 12% in 2022 due to inflation and rising energy prices, making it harder for manufacturers to maintain competitive pricing in the market.

- Limited Consumer Awareness: Despite growing demand for functional foods, there is limited awareness among consumers about the specific benefits of resistant starch. A 2022 survey by the European Union's Consumer Insights division indicated that only 35% of the population in Europe is aware of resistant starchs health benefits. This lack of awareness is particularly evident in emerging markets, where health literacy on specific ingredients like resistant starch remains low, potentially stifling market growth.

Global Resistant Starch Market Future Outlook

Over the next five years, the global resistant starch market is expected to experience significant growth, driven by the increasing demand for healthier, functional food products. The rising prevalence of obesity, diabetes, and digestive health issues is likely to accelerate the adoption of resistant starch in various food and beverage applications. Additionally, advancements in food processing technologies and growing consumer awareness of the health benefits of dietary fibers are expected to further drive market expansion.

Market Opportunities

- Expansion into Emerging Markets: The growing health consciousness in emerging markets presents a significant opportunity for the resistant starch industry. For example, in 2024, Brazil's health-conscious population grew by 8 million, with increasing demand for products that promote gut health. The Asian market, particularly India and China, also shows vast potential, with over 1.2 billion consumers in these countries showing an increased interest in dietary fibers. The economic stability and growing disposable incomes in these regions make them prime markets for expansion.

- Innovations in Product Formulations: Innovations in resistant starch formulations are creating new opportunities in various sectors, especially pharmaceuticals and nutraceuticals. Recent breakthroughs in microencapsulation technology have allowed for better integration of resistant starch into processed foods and supplements. The pharmaceutical industry, valued at over $1.4 trillion in 2023, is increasingly incorporating resistant starch in formulations aimed at enhancing gut health, showcasing the potential of this ingredient in medical and therapeutic products.

Scope of the Report

|

Product Type |

Resistant Starch Type 1 (RS1) |

|

Resistant Starch Type 2 (RS2) |

|

|

Resistant Starch Type 3 (RS3) |

|

|

Resistant Starch Type 4 (RS4) |

|

|

Source |

Corn |

|

Potatoes |

|

|

Bananas |

|

|

Rice |

|

|

Wheat |

|

|

Application |

Food and Beverages |

|

Pharmaceuticals |

|

|

Animal Feed |

|

|

Nutraceuticals |

|

|

Form |

Powder |

|

Granules |

|

|

Liquid |

|

|

Region |

North America |

|

Europe |

|

|

Asia Pacific |

|

|

Latin America |

|

|

Middle East & Africa |

Products

Key Target Audience

Food & Beverage Manufacturers

Pharmaceuticals & Nutraceutical Manufacturers

Animal Feed Producers

Government Regulatory Bodies (US FDA, European Food Safety Authority)

Ingredient Suppliers

Health & Wellness Brands

Research & Development Organizations

Investor and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Ingredion Incorporated

Cargill

Tate & Lyle

Roquette Frres

MGP Ingredients

Archer Daniels Midland Company

Grain Processing Corporation

Avebe

Emsland Group

Biomin

Glico Nutrition

Ingredion ANZ

Matsutani Chemical Industry Co., Ltd.

CFF GmbH & Co. KG

SunOpta Inc.

Table of Contents

1. Global Resistant Starch Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (in % CAGR)

1.4. Market Segmentation Overview

2. Global Resistant Starch Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (in %)

2.3. Key Market Developments and Milestones

3. Global Resistant Starch Market Analysis

3.1. Growth Drivers (Resistant starch applications in food, pharmaceuticals, etc.)

3.1.1. Rising Consumer Demand for Functional Foods

3.1.2. Increasing Awareness of Gut Health

3.1.3. Rising Prevalence of Obesity and Diabetes

3.1.4. Government Support for Healthier Diets

3.2. Market Challenges (Low awareness, pricing issues)

3.2.1. High Production Costs

3.2.2. Limited Consumer Awareness

3.2.3. Competition from Other Fibers

3.3. Opportunities (New applications, emerging markets)

3.3.1. Expansion into Emerging Markets

3.3.2. Innovations in Product Formulations

3.3.3. Increased Use in Pharmaceutical and Nutraceuticals

3.4. Trends (Rising demand in processed foods, new R&D developments)

3.4.1. Rising Adoption in Gluten-Free Products

3.4.2. Increasing Use in Prebiotic Supplements

3.4.3. Growing Preference for Organic Sources

3.5. Government Regulation (Food safety, labeling)

3.5.1. Food Safety Regulations on Starch Ingredients

3.5.2. Nutrition Labeling Standards

3.5.3. Regulatory Approvals for New Sources of Resistant Starch

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Suppliers, manufacturers, consumers)

3.8. Porters Five Forces (Market structure and competition)

3.9. Competition Ecosystem (Market structure)

4. Global Resistant Starch Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Resistant Starch Type 1 (RS1)

4.1.2. Resistant Starch Type 2 (RS2)

4.1.3. Resistant Starch Type 3 (RS3)

4.1.4. Resistant Starch Type 4 (RS4)

4.2. By Source (In Value %)

4.2.1. Corn

4.2.2. Potatoes

4.2.3. Bananas

4.2.4. Rice

4.2.5. Wheat

4.3. By Application (In Value %)

4.3.1. Food and Beverages

4.3.2. Pharmaceuticals

4.3.3. Animal Feed

4.3.4. Nutraceuticals

4.4. By Form (In Value %)

4.4.1. Powder

4.4.2. Granules

4.4.3. Liquid

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Resistant Starch Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Ingredion Incorporated

5.1.2. Cargill

5.1.3. Tate & Lyle

5.1.4. MGP Ingredients

5.1.5. Archer Daniels Midland Company

5.1.6. Roquette Frres

5.1.7. Avebe

5.1.8. Emsland Group

5.1.9. Grain Processing Corporation

5.1.10. Biomin

5.1.11. Glico Nutrition

5.1.12. Ingredion ANZ

5.1.13. CFF GmbH & Co. KG

5.1.14. Matsutani Chemical Industry Co., Ltd.

5.1.15. SunOpta Inc.

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, R&D Expenditure, Market Share, Product Launches, Strategic Collaborations)

5.3. Market Share Analysis (In %)

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Including government grants, venture capital funding)

6. Global Resistant Starch Market Regulatory Framework

6.1. Compliance and Certification (Food Safety Certification)

6.2. Regional Regulatory Standards (US, EU, APAC)

6.3. Certification Requirements (ISO, HACCP, etc.)

7. Global Resistant Starch Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global Resistant Starch Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Source (In Value %)

8.3. By Application (In Value %)

8.4. By Form (In Value %)

8.5. By Region (In Value %)

9. Global Resistant Starch Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Key Growth Strategies

9.3. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involved mapping the entire resistant starch ecosystem, identifying key stakeholders across the food and beverage, pharmaceutical, and nutraceutical industries. This was accomplished through desk research and analysis of proprietary databases, allowing us to identify critical variables influencing the market, such as production capacity, innovation trends, and consumer demand.

Step 2: Market Analysis and Construction

In this phase, historical data on the resistant starch market was compiled and analyzed to assess the penetration of resistant starch products across different applications. This data was used to project market share for each segment, ensuring a comprehensive understanding of the market structure and key growth areas.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were formulated and validated through interviews with industry experts and stakeholders, including food scientists, product managers, and key decision-makers in the resistant starch market. These consultations provided valuable insights into industry trends, market challenges, and growth drivers.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the data gathered from various sources and consultations into a coherent market report. This process included validating revenue estimates, understanding the competitive landscape, and analyzing product segments to deliver a final, accurate market report.

Frequently Asked Questions

01. How big is the Global Resistant Starch Market?

The global resistant starch market is valued at USD 1.4 billion, driven by the rising demand for functional foods and the growing health-conscious consumer base.

02. What are the challenges in the Global Resistant Starch Market?

Key challenges in the market include high production costs, limited consumer awareness about resistant starch benefits, and competition from other dietary fibers and functional ingredients.

03. Who are the major players in the Global Resistant Starch Market?

The major players include Ingredion Incorporated, Tate & Lyle, Cargill, Roquette Frres, and MGP Ingredients. These companies dominate due to their extensive product portfolios and global market presence.

04. What are the growth drivers for the Global Resistant Starch Market?

The growth of the resistant starch market is propelled by the increasing demand for functional foods, rising consumer awareness about gut health, and advancements in food processing technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.