Global Rigid Plastic Packaging Market Outlook to 2030

Region:Global

Author(s):Rohit and Nishika

Product Code:KENGR050

Region:Global

Author(s):Rohit and Nishika

Product Code:KENGR050

October 2024

84

The Global Rigid Plastic Packaging Market can be segmented based on several factors:

|

Company |

Establishment Year |

Headquarters |

Geographical Presence |

|

Berry Global Group Inc |

1967 |

Indiana, USA |

38 |

|

ALPA- Werke Alwin Lehner GmbH & Co KG (Not Listed) |

1955 |

Hard,Austria |

47 |

|

Amcor Plc |

1896 |

Victoria, Australia |

41 |

|

Aptar Group |

1992 |

Illinois, USA |

18 |

|

Pactiv Evergreen |

2020 |

Illinois, USA |

2 |

|

Huhtamaki Packaging Company |

1935 |

Espoo, Finland |

38 |

Global Rigid Plastic Packaging Market Growth Drivers:

Global Rigid Plastic Packaging Market Government Initiatives:

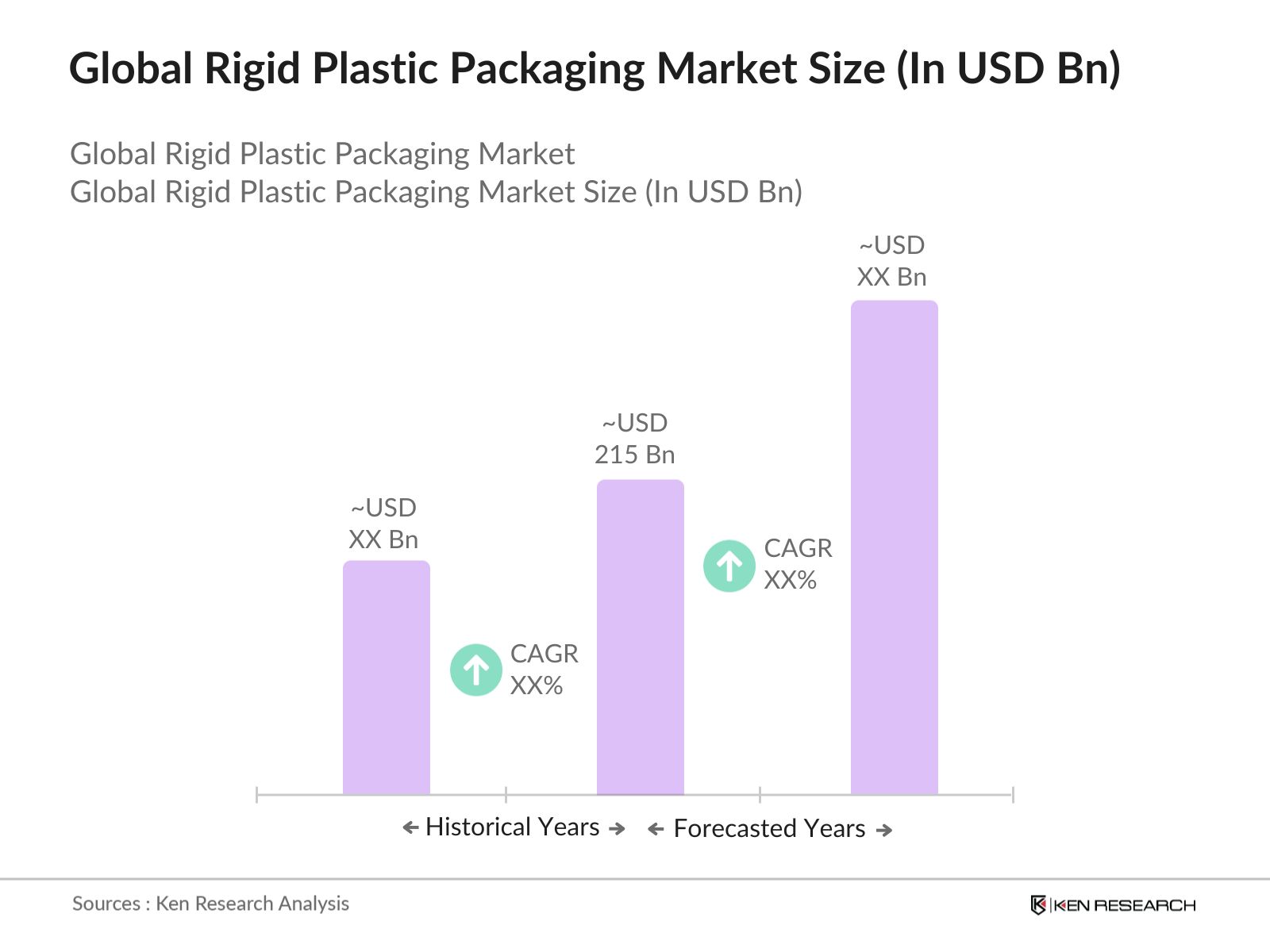

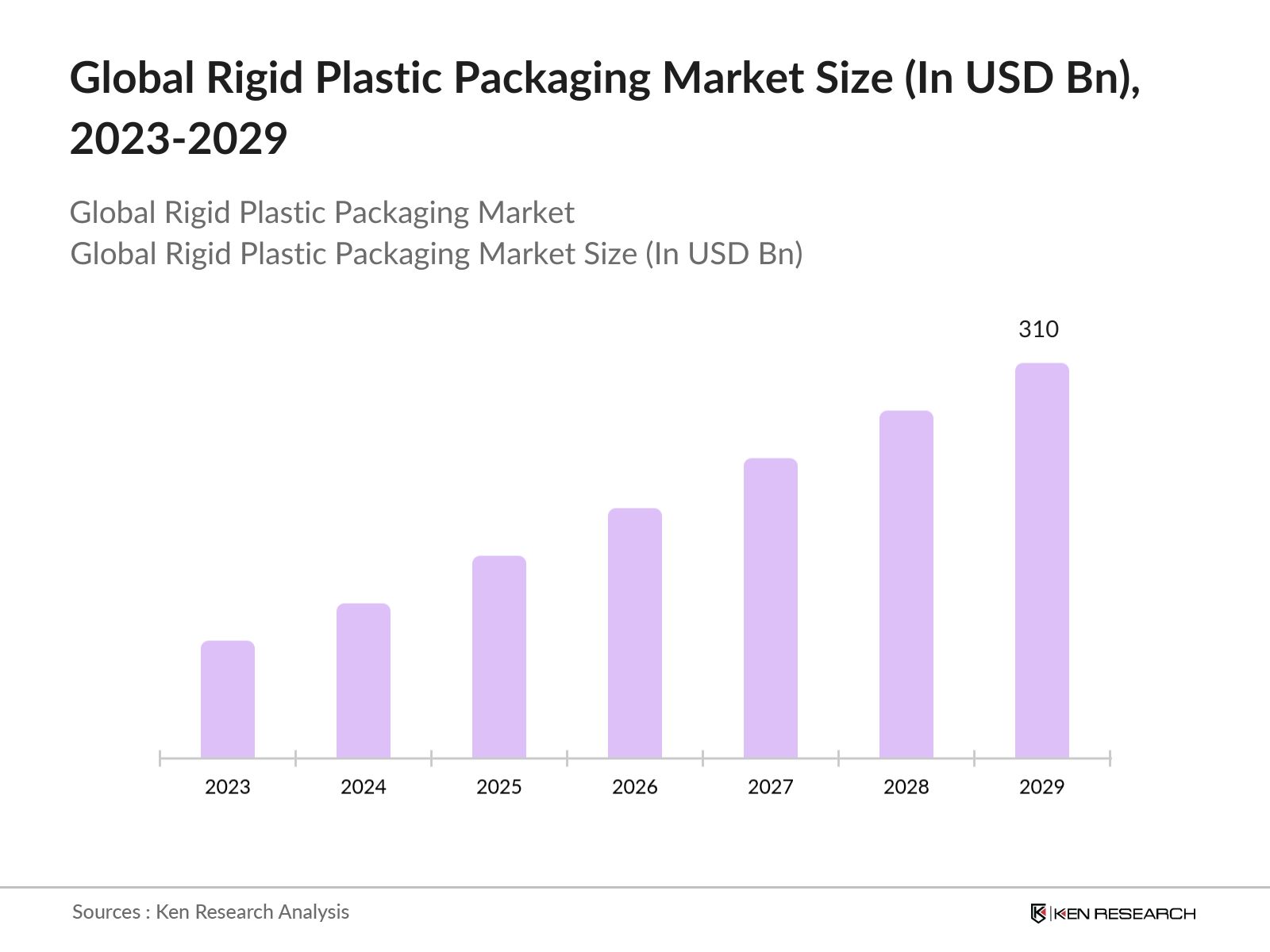

The global rigid plastic packaging market is predicted to grow exceptionally in the forecasted period of 2023-2029 reaching a market size of USD 310 Bn driven by increased adoption of sustainable and recyclable materials, advancements in packaging technologies, and growth in e-commerce and demand for durable packaging.

|

By Region |

North America Europe APAC Latin America MEA |

|

By Product |

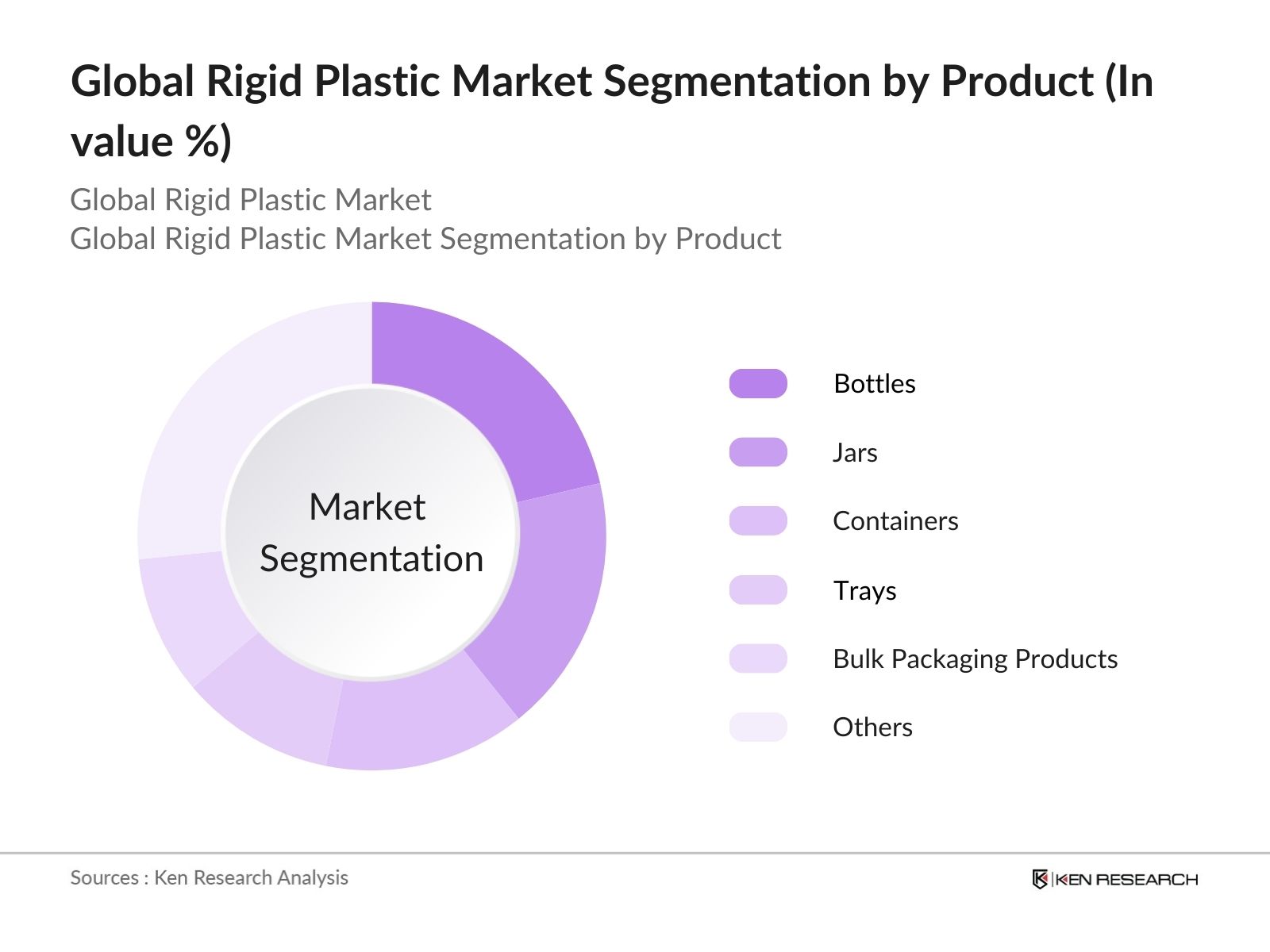

Bottles Jars Containers Trays Bulk Packaging Products Tubs, Cups & Pots Caps & Closures Others ( includes Blisters, Clamshell Packs & Tubes) |

|

By End-User |

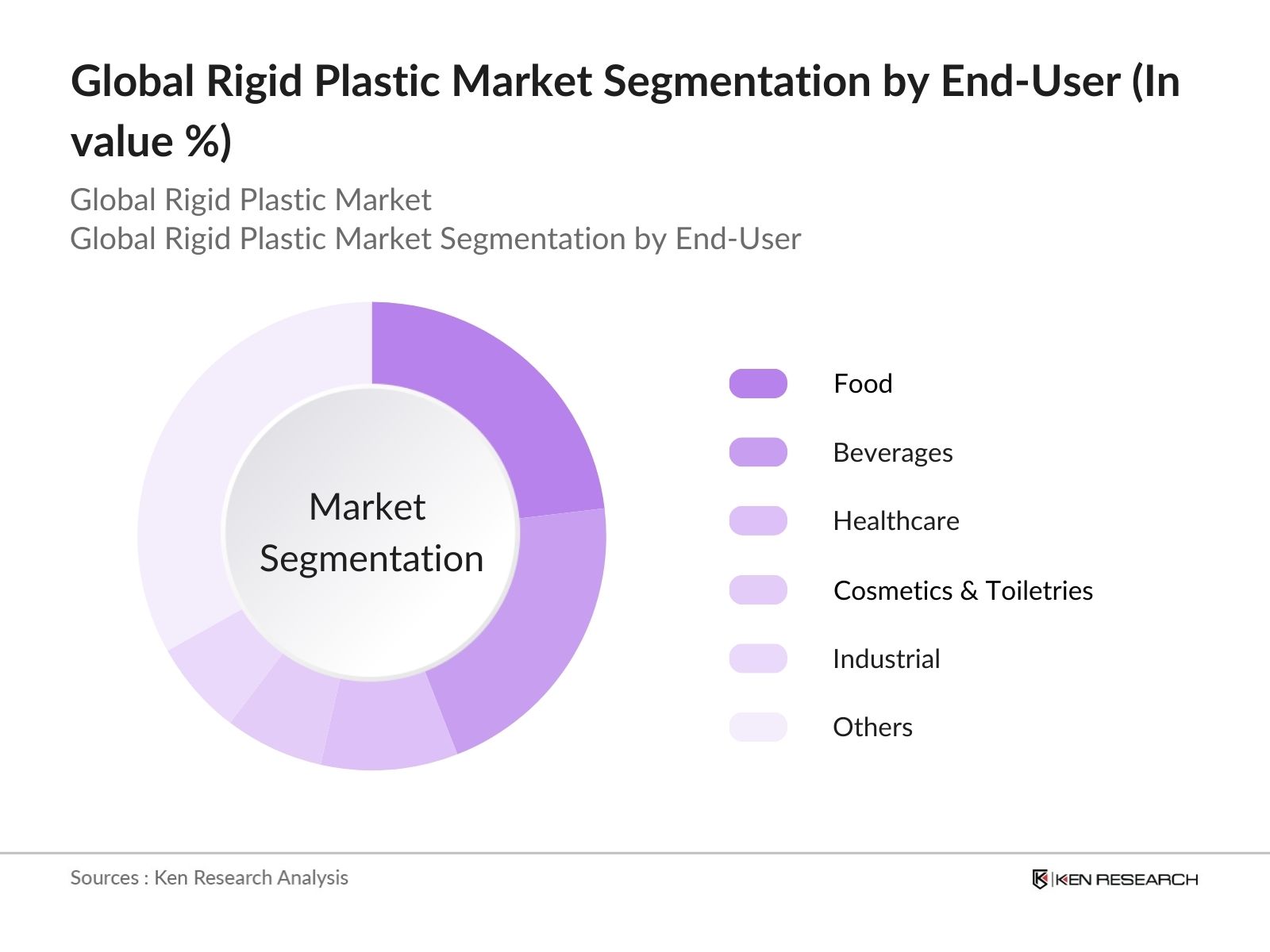

Food Beverages Healthcare Cosmetics & Toiletries Industrial Personal Care Consumer Goods Construction Automotive Pharmaceuticals Others (includes Electrical & Electronics) |

|

By Plastic Type |

PET PE PP PVC PS EPS Others (PC, Polyamide) |

|

By Production Technology |

Extrusion Injection Molding Blow Molding Thermoforming |

1.1 Global Rigid Plastic Packaging Market

1.2 Global Plastic Market

2.1 Overview of Global Economics

2.2 Overview of Global Rigid Plastic Packaging Industry

2.3 Global Rigid Plastic Packaging Revenue

2.4 Global Rigid Plastic Packaging Infrastructure

3.1 Ecosystem

3.2 Value Chain

3.3 Case Study

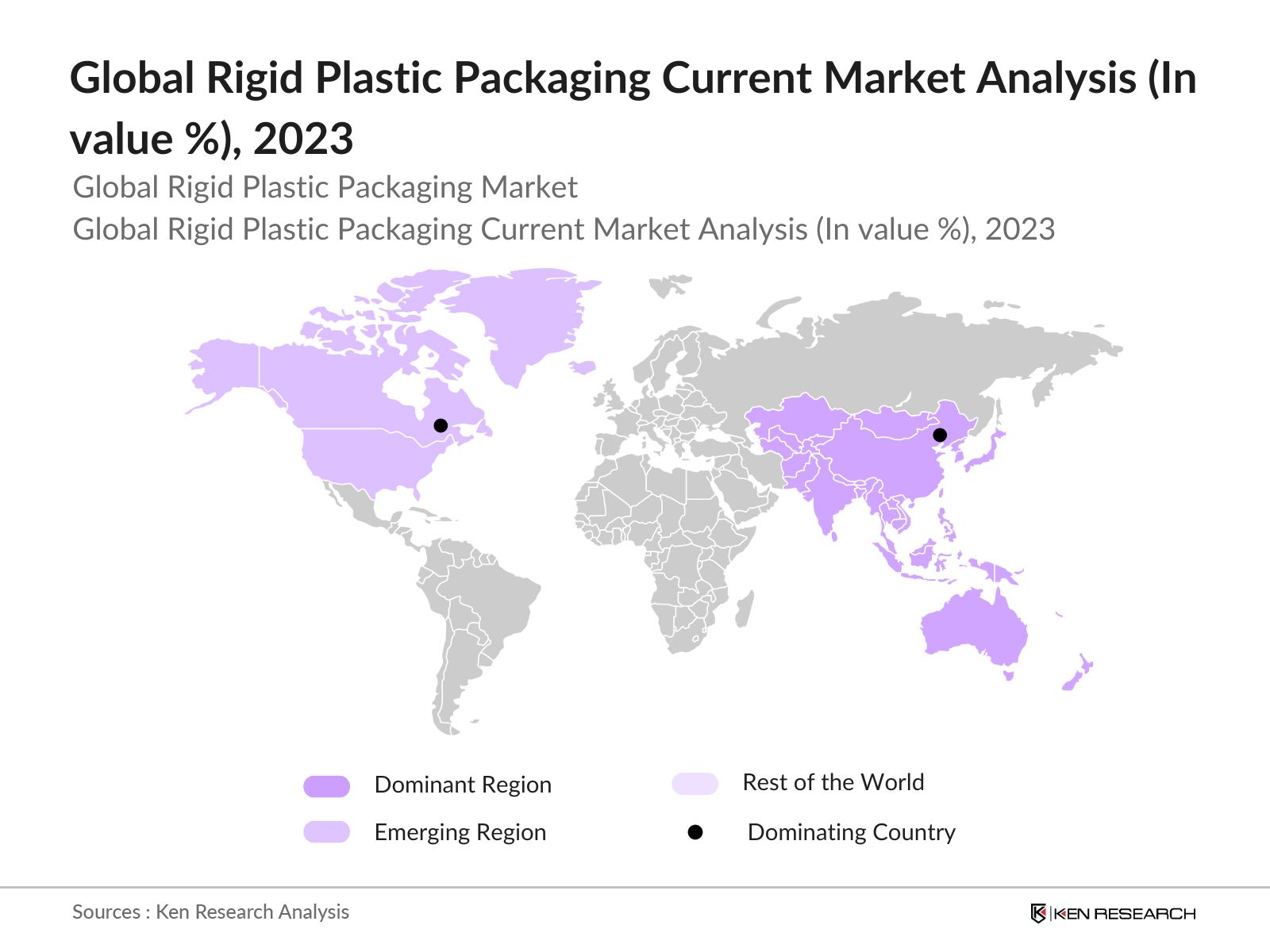

5.1 By Region (North America, Europe, APAC, Latin America and MEA) in value %, 2018-2023

5.2 By Product (Bottles, Jars, Containers, Trays, Bulk Packaging Products, Tubs, Cups & Pots, Caps & Closures, and Others) in value%, 2018-2023

5.3 By End-User (Food, Beverages, Healthcare, Cosmetics & Toiletries, Industrial, Personal Care, Consumer Goods, Construction, Automotive, Pharmaceuticals, and Others) in value %, 2018-2023

5.4 By Plastic (PET, PE, PP, PVC, PS, EPS, and Others) in value %, 2018-2023

5.5 By Production Technology (Extrusion, njection Molding, Blow Molding, and Thermoforming) in value %, 2018-2023

6.1 Market Share Analysis

6.2 Market Heat Map Analysis (By Technology)

6.3 Market Heat Map Analysis (By Offerings)

6.4 Market Cross Comparison

6.5 Comparison Matrix

6.6 Investment Landscape

7.1 Growth Drivers

7.2 Challenges

7.3 Trends

7.4 Case Studies

7.5 Strategic Initiatives

9.1 By Region (North America, Europe, APAC, Latin America and MEA) in value %, 2023-2029

9.2 By Product (Bottles, Jars, Containers, Trays, Bulk Packaging Products, Tubs, Cups & Pots, Caps & Closures, and Others) in value%, 2023-2029

9.3 By End-User (Food, Beverages, Healthcare, Cosmetics & Toiletries, Industrial, Personal Care, Consumer Goods, Construction, Automotive, Pharmaceuticals, and Others) in value %, 2023-2029

9.4 By Plastic (PET, PE, PP, PVC, PS, EPS, and Others) in value %, 2023-2029

9.5 By Production Technology (Extrusion, njection Molding, Blow Molding, and Thermoforming) in value %, 2023-2029

Objective: Identify players, revenue, product offerings of key players, and average pricing to calculate the market size.

Objective: Confirm market revenue, margins, segmentations, distribution, and future projections to gauge insights in the current market trends.

The global rigid plastic packaging market was valued at USD 220 billion in 2023, driven by the rising demand for durable and cost-effective packaging solutions across various industries, including food, beverages, healthcare, and personal care.?

Challenges in the global rigid plastic packaging market include environmental concerns related to plastic waste, stringent government regulations on plastic use, and increasing competition from alternative packaging materials like flexible packaging and glass.?

Key players in the global rigid plastic packaging market include Amcor Limited, Berry Global Group, Inc., RPC Group Plc, and ALPLA Werke Alwin Lehner GmbH & Co KG. These companies lead the market due to their innovative packaging solutions, extensive global presence, and strong customer base.?

The global rigid plastic packaging market is driven by factors such as the increasing demand for lightweight and durable packaging solutions, the growing popularity of single-serve packaging in the food industry, and advancements in recycling technologies that promote the use of recycled materials.?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.