Global Sapphire Market Outlook to 2030

Region:Global

Author(s):Yogita Sahu

Product Code:KROD8578

Region:Global

Author(s):Yogita Sahu

Product Code:KROD8578

December 2024

90

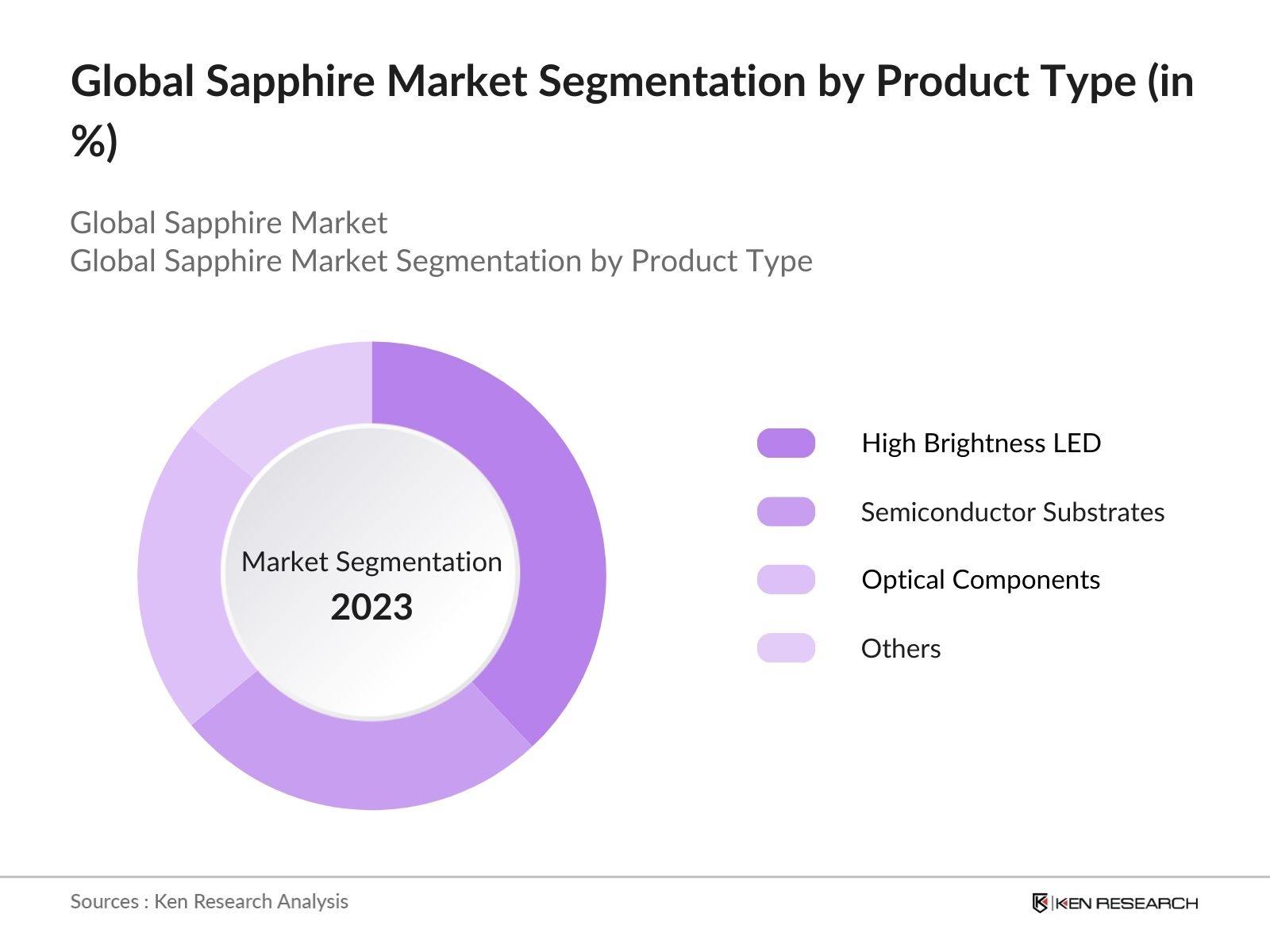

By Product Type: The market is segmented by product type into high-brightness LED manufacturing, semiconductor substrates, and optical components. The high-brightness LED segment dominates the market, driven by the increased adoption of LEDs in lighting and display applications. Sapphires ability to provide excellent thermal conductivity and electrical insulation is crucial for high-performance LED substrates, making it indispensable for the LED industry.

By Production Method: The market is segmented by production method into KY (Kyropoulos), CZ (Czochralski), HEM (Heat Exchanger Method), EFG (Edge-defined Film-fed Growth), and VHGF (Vertical Horizontal Gradient Freezing). The KY method is the most dominant, accounting for the highest market share in 2023. The methods ability to produce high-quality large sapphire crystals with fewer defects makes it ideal for industries like LEDs and semiconductors. Additionally, KY is cost-effective and widely used across different regions due to its efficiency.

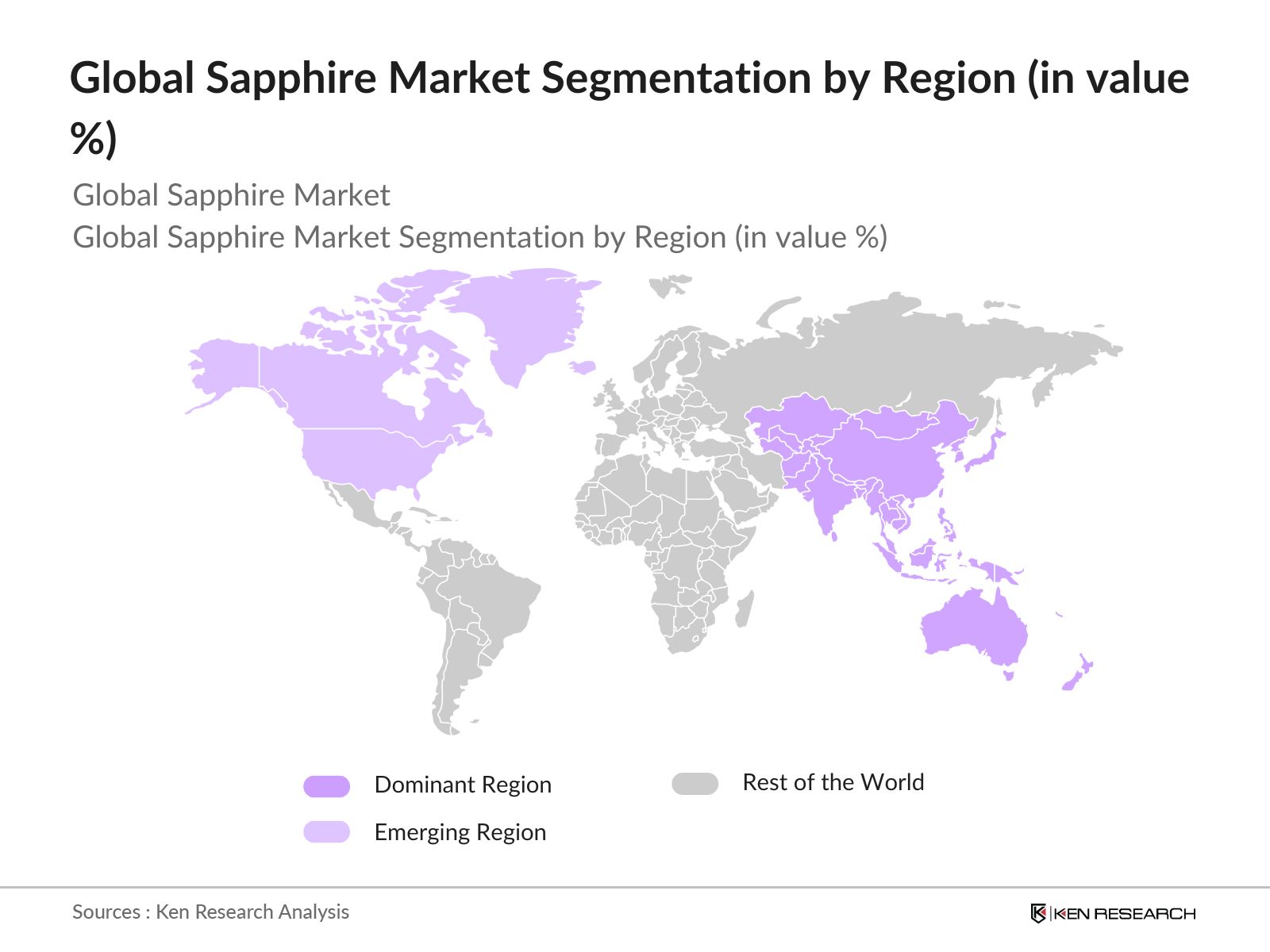

By Region: The market is geographically segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East & Africa. Asia-Pacific leads the global market, primarily due to the presence of manufacturing hubs for consumer electronics and semiconductors. This region is expected to continue its dominance, driven by increasing investments in technological advancements in China, South Korea, and Japan.

The market is dominated by a few key players who focus on expanding their product portfolio through technological advancements and strategic partnerships. These companies are leveraging the growing demand for sapphire in LED, semiconductor, and optical applications to increase their market share.

|

Company Name |

Established Year |

Headquarters |

Number of Employees |

Revenue (USD Mn) |

Production Capacity |

Key Product Lines |

Partnerships |

R&D Investments |

|

Rubicon Technology |

2001 |

Bensenville, USA |

||||||

|

Kyocera |

1959 |

Kyoto, Japan |

||||||

|

Monocrystal |

1999 |

Stavropol, Russia |

||||||

|

GT Advanced Technologies |

1994 |

Merrimack, USA |

||||||

|

Saint-Gobain |

1665 |

Paris, France |

Over the next five years, the global sapphire industry is expected to experience growth, driven by the expansion of the consumer electronics and semiconductor industries. The increasing use of sapphire in optical and industrial applications, particularly in high-performance LEDs and semiconductors, will further propel market demand.

|

Product Type |

High Brightness LED Manufacture Semiconductor Substrates Optical Components Medical Devices Special Industrial |

|

Application |

Consumer Electronics Special Industrial Medical Devices High Brightness LED Manufacturing Semiconductor Substrates |

|

Production Method |

KY CZ HEM EFG VHGF |

|

Distribution Channel |

Direct Sales Distributors & Resellers |

|

Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Macroeconomic Factors Impacting the Market

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand for Sapphire in LEDs (High Brightness LED Manufacturing)

3.1.2. Expansion in Consumer Electronics (Smartphones, Wearables)

3.1.3. Use in Optical Components and Laser Devices (Enhanced Optical Clarity)

3.1.4. Technological Advancements in Sapphire Production Methods (KY and CZ Techniques)

3.2. Market Challenges

3.2.1. High Production Costs (Impact on Profit Margins)

3.2.2. Competition from Alternative Materials (Emerging Glass Substitutes)

3.2.3. Supply Chain Disruptions (Raw Material Price Volatility)

3.3. Opportunities

3.3.1. Rising Demand in Special Industrial Applications (Durability and Thermal Resistance)

3.3.2. Increased Penetration into Emerging Markets (Asia-Pacific Expansion)

3.4. Trends

3.4.1. Collaboration with Semiconductor Industry (R&D Synergies)

3.4.2. Growing Adoption in Medical Devices (Laser Surgery Applications)

3.5. Government Regulations

3.5.1. Environmental Compliance Standards (Production Emissions)

3.5.2. Intellectual Property Protection (Innovation in Production Methods)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

4.1. By Product Type (In Value %)

4.1.1. High Brightness LED Manufacture

4.1.2. Semiconductor Substrates

4.1.3. Optical Components

4.2. By Application (In Value %)

4.2.1. Consumer Electronics

4.2.2. Medical Devices

4.2.3. Special Industrial

4.3. By Production Method (In Value %)

4.3.1. KY Method

4.3.2. CZ Method

4.3.3. HEM Method

4.4. By Distribution Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Distributors & Resellers

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. Rubicon Technology

5.1.2. Kyocera

5.1.3. Monocrystal

5.1.4. GT Advanced Technologies

5.1.5. Saint-Gobain

5.1.6. Thermal Technology

5.1.7. Sapphire Technology Company

5.1.8. CrystalTech HK

5.1.9. Crystaland

5.1.10. Namiki Precision Jewel

5.1.11. Omega Crystals

5.1.12. SF Tech

5.1.13. Daiichi Kiden

5.1.14. IntElorg Pte

5.1.15. Harbin Aurora Optoelectronics

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, R&D Expenditure, Market Share, Product Innovations, Strategic Partnerships, Key Clients)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Acquisitions)

5.5. Investment Analysis

5.6. Venture Capital Funding

5.7. Government Grants

5.8. Private Equity Investments

6.1. Environmental Standards

6.2. Intellectual Property Regulations

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Production Method (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunity Identification

This stage involved mapping out the stakeholders and dynamics of the global sapphire market. Extensive desk research was conducted using secondary sources like industry reports and proprietary databases to define the core variables that drive market trends.

In this phase, we compiled historical data on the sapphire market, evaluating production capacities, consumer demand, and supply chain disruptions. This helped in identifying key trends, challenges, and opportunities that influence market growth.

Market assumptions were validated by consulting industry experts from leading companies in the sapphire market. These consultations helped refine data accuracy and verify trends based on firsthand market insights.

The final step involved synthesizing all gathered data and insights into a comprehensive report. This ensured the accuracy of market size estimates, competitive landscape analysis, and future growth projections.

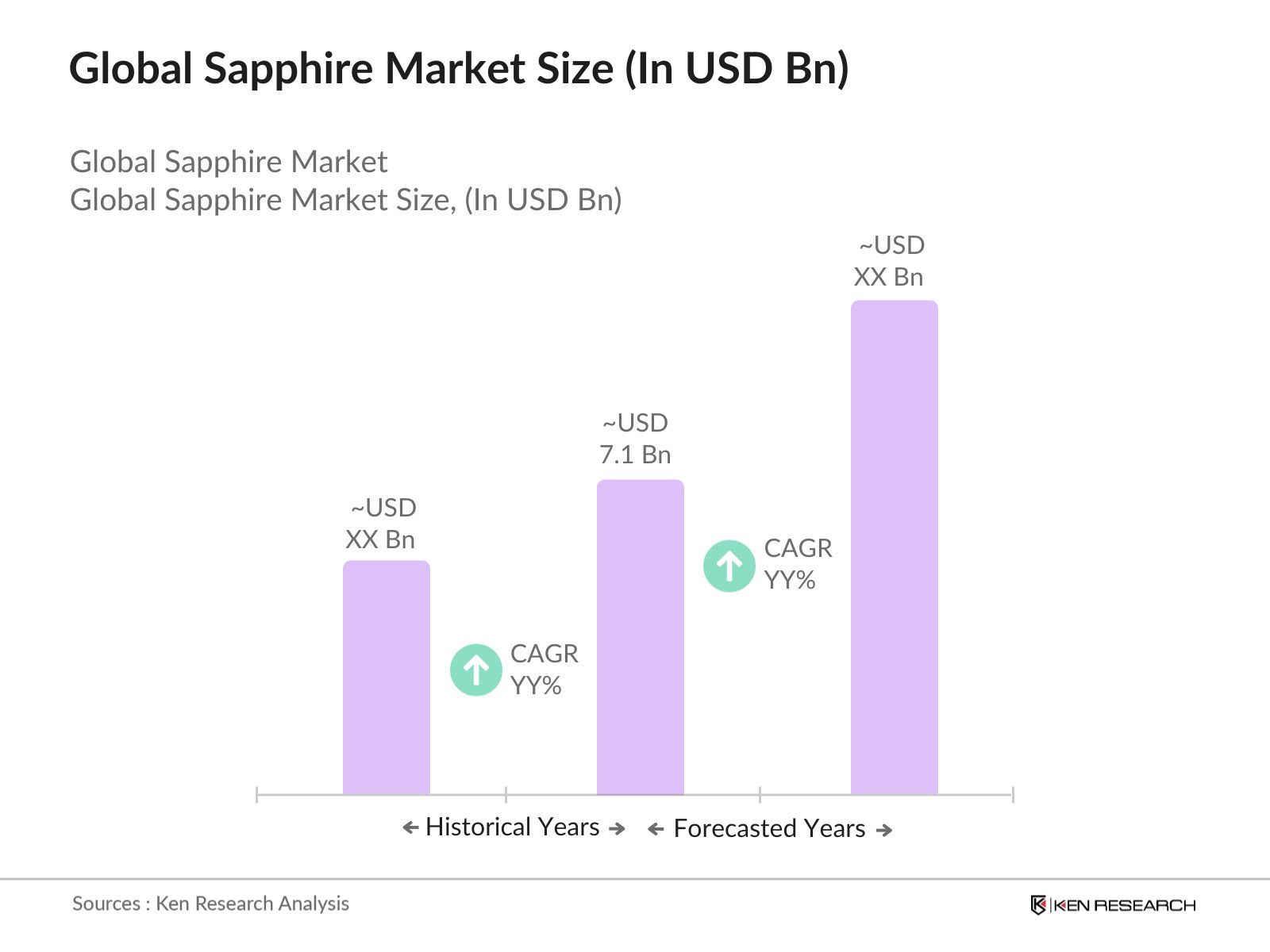

The global sapphire market is valued at USD 7.1 billion in 2023, driven by its increasing use in consumer electronics, semiconductors, and LED lighting applications.

Challenges in the global sapphire market include high production costs, supply chain volatility, and growing competition from alternative materials. Additionally, the complex production processes associated with sapphire hinder market growth.

Key players in the global sapphire market include Rubicon Technology, Kyocera, Monocrystal, GT Advanced Technologies, and Saint-Gobain, which dominate the market due to their technological advancements and production capacities.

The sapphire market is propelled by rising demand for high-performance materials in LEDs, semiconductors, and consumer electronics, as well as advancements in production technologies.

Sapphire is widely used in LED manufacturing, semiconductor substrates, optical components, and medical devices due to its durability, optical clarity, and high thermal conductivity.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.